Macro focus – Can the incoming PM reset the UK’s national mood? Weak survey data points to limited growth momentum in the UK, with domestic political uncertainty offsetting an improved external backdrop. Starmer’s resignation this week has now cleared the path for a swift transition to Andy Burnham as new UK PM. The lack of a leadership contest would remove some tail risks but it also leaves markets with limited visibility on his actual economic policies. We expect the PM-to-be will blend more left-leaning instincts with market pragmatism in an effort to avoid volatility. But there are clear risks that speculation and uncertainty will weigh on UK sentiment, as has been the case around recent Budgets. We see UK growth at a relatively muted 1.1% this year.

What we’re watching next week: Away from UK politics we will be focused on euro area inflation data and the ECB’s communication at its Sintra forum. Headline HICP could edge lower on falling energy prices and officials will be encouraged by limited signs of second-round risks in various survey data. Our baseline remains one additional rate hike this year, with market pricing increasingly aligned with that view.

Macro Focus: Can Burnham reset the UK’s national mood?

The PM-to-be needs to prevent policy speculation from weighing on activity – while also keeping investors on side

Another week, another soft UK data release. The composite UK PMI edged down to 49.4 in June which was the weakest reading since last April’s US tariff announcement. The services figure, at 48.7, slumped to a 41-month low with further deterioration in the employment component. Output price pressures also eased, supporting our decision to drop all BoE tightening this year from our call (see here).

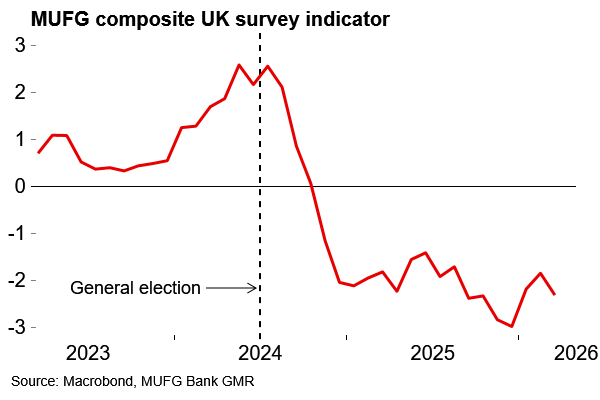

Zooming out, our composite indicator of a swathe of business and household surveys shows that UK sentiment has been consistently weak since the start of the Labour government. Outgoing PM Starmer said immediately after his election victory that “painful” fiscal measures were required. A big unforced error. It triggered heightened speculation around the first Budget, which weighed on spending and investment, before some by relief when consolidation was not bad as feared. The cycle was essentially repeated the following year. The effect of this is clearly visible in the bumpy UK GDP profile, which we think reflects ‘policy seasonality’ rather than a failure of seasonal adjustment.

Whether this actually matters for growth is debatable. Sentiment may have been weak, but the UK has grown faster than all G7 economies bar the US since the 2024 election. Still, the PMI release noted domestic political uncertainty as a headwind for sentiment and PM-to-be Andy Burnham will be desperate to lift the national mood.

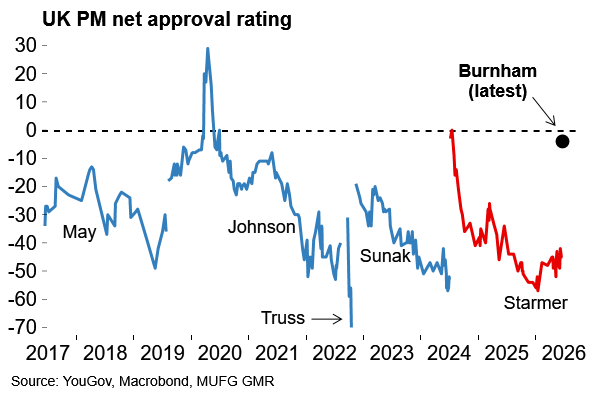

Burnham starts from a position of relative popularity...

...but can he change the vibes?

The rapid transition comes with limited visibility around Burnham's economic policies

We now have some clarity in that Starmer announced his resignation rather than clinging on after the decisive Makerfield by-election. As a result, Burnham is set to become UK PM as early as mid-July. If he goes unchallenged, as seems likely, then a drawn-out and potentially fractious leadership contest with risk of expansive spending pledges will be avoided (as will a period of policy drift under a lame duck PM).

But the lack of a contest also means there will be a rapid transition which leaves us largely in the dark around Burnham’s economic policies. While that is the case, speculation is likely to weigh on spending and investment decisions. Burnham is expected to make a speech next week to set out his priorities. Let’s see how much detail there is at this early stage. What we know is that the ex-mayor of Manchester is keen on devolving powers to local authorities. More broadly, he reportedly advocates ‘business-friendly socialism’.

That label feels like an effort to balance his left-leaning instincts (which are stronger than Starmer’s) with market pragmatism. His pick for chancellor will reveal a lot about which way he is likely to tilt. Market participants would fret about the appointment of Ed Miliband or another candidate from the left of the party. The range of names in the frame from across the Labour Party suggest that Burnham has not yet decided, but the implied probability of Miliband as next chancellor has risen to around 50% on Polymarket.

The UK will continue to face a tight fiscal backdrop

Whoever Burnham picks will have to confront the reality of the UK’s tight fiscal backdrop. In March, the OBR estimated that headroom to the primary fiscal rule increased marginally to around 24bn GBP. Despite the recent rally in gilts, our best guess is that this may be reduced by as much as 10bn due to higher rates relative to the previous reference period and the borrowing overshoot early in the fiscal year. That is before higher spending demands, e.g. on defence, are considered.

Significantly, Burnham has indicated that he will retain the current fiscal rules. These require that 1) the current budget (i.e. day-to-day spending) is in surplus in the third projection year, and 2) that debt (specifically public sector net financial liabilities) is expected to fall as a share of GDP over the same horizon.

There is some leeway for more capital investment under that framework but there will be a temptation to game the rules and carve out more space. The gilt market will be the ultimate judge of what’s sustainable and a modest degree of rule-bending for high-multiplier capex might be tolerated. But investors would look dimly on a lack of transparency or ‘fiscal fiction’ via further backloading consolidation. We are also reassured that Burnham has some heavyweight advisers on board such as Andy Haldane, the ex-BoE chief economist, who bring a degree of credibility. Ultimately, the Liz Truss episode remains a cautionary tale and we suspect Burnham and team will be well aware of the importance of keeping markets on their side.

Turning back to the immediate growth outlook, the PMI numbers mentioned above are consistent with flat growth across Q2 as a whole. We are tracking growth at 0.2%, however, following reasonable momentum in hard data earlier in the year. That would still represent a considerable slowdown from the 0.6% Q/Q growth recorded in Q1 and we see UK growth at a relatively muted 1.1% across the year as a whole. Meanwhile, inflation is also set to nudge above 3% over coming months, despite the retracement in crude prices as Hormuz reopens, due to the lagged household energy price cap and other lagged pass-through effects.

In short, there will be a whiff of stagflation around the outlook for some time. It could be worse, i.e. without Middle East de-escalation, but it’s not the easiest economic inheritance for PM-to-be Burnham. He starts from a point of relative popularity (see e.g., polling here), is a stronger communicator than Starmer and has better political instincts which reduces the likelihood of damaging policy U-turns. But he will need to play his cards right to prevent heightened policy uncertainty and market volatility further weighing on the outlook.

What we’re watching next week

ECB officials convene in Sintra amid signs of fading second-round inflation risks

Away from UK politics and Burnham’s policy signals, our focus next week will be on the preliminary estimates of euro area inflation in June. Lower energy costs mean that the headline rate is likely to edge lower (MUFG: 3.1%, from 3.2% previously). There is a risk that core inflation edges higher, however, as the energy shock continues to percolate through the economy. Even under the ECB’s milder scenario, which is conditioned on pricing similar to the current oil curve, core inflation is seen at 2.3% next year. Still, ECB officials have, in the round, sounded more dovish since this month’s rate hike (which came just before key US-Iran progress). Since then, survey data, such as prices charged in the services PMI and household near-term inflation expectations, have pointed to reduced second-round inflation risks. We’ll be watching to see how Lagarde and co frame it at next week’s Sintra forum. As it stands, we continue to expect one more rate hike (see here) and market pricing is increasingly converging around that mark.

Key data releases and events (week commencing Monday 29 June)

Day | Time | Region | Event | Period | Consensus | MUFG | Previous |

Mon 29 Jun | 10:00 | EC | Economic Confidence | Jun | 94.5 | 95.2 | 93.5 |

Mon 29 Jun | 18:30 | EC | ECB's Lagarde Speaks in Sintra | - | - | - |

|

Tue 30 Jun | 7:45 | FR | CPI EU Harmonized YoY | Jun P | 2.3 | 2.4 | 2.8 |

Tue 30 Jun | 8:55 | GE | Unemployment Change (000's) | Jun | 7.5k | 0.0k | -12.0k |

Tue 30 Jun | 10:00 | IT | CPI EU Harmonized YoY | Jun P | 3.2 | 3.2 | 3.2 |

Tue 30 Jun | 13:00 | GE | CPI EU Harmonized YoY | Jun P | 2.7 | 2.6 | 2.7 |

Wed 1 Jul | 10:00 | EC | CPI YoY | Jun P | 3.1 | 3.1 | 3.2 |

Thu 2 Jul | 10:00 | EC | Unemployment Rate | May | 6.3 | 6.3 | 6.3 |

Fri 3 Jul | 9:30 | UK | DMP 1 Year CPI Expectations | Jun | - | - | 3.7 |

Note: All times are GMT+1 (London). Source: Bloomberg, MUFG GMR