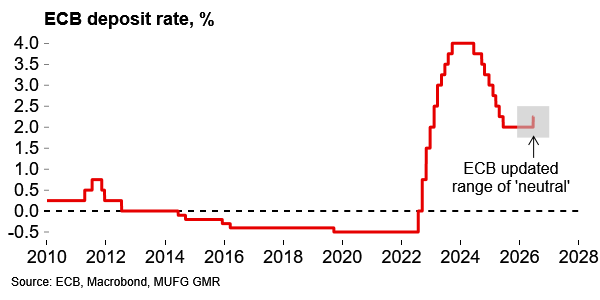

Macro focus – The ECB reopens the debate on neutral: This week the ECB chief economist suggested that the euro area neutral rate could be as high as 2.5% - above the previously published official estimate. It’s always eye-catching when a central banker shows any willingness to quantify neutral. The policy implications here are clear: the case for an additional rate hike is strengthened and the bar has been raised for any subsequent easing. In terms of rationale, Lane did not set out the details, but there is certainly a case for neutral moving higher on the back of stronger investment demand relating to AI and defence. Europe may not be at the epicentre of the former, but neutral rates are strongly anchored by global trends. Uncertainty around these estimates will always be high but signalling effects also matter here – by entertaining a higher neutral rate the ECB (and other central banks) could ultimately shape expectations in a way that reinforces the outcome.

What we’re watching next week: UK politics will be in focus following Andy Burnham’s decisive by-election win. That result has increased the likelihood that he replaces Starmer as UK PM this year. While a contest is possible, we expect that Starmer will ultimately be pressured by the cabinet to set out a timetable for his departure now, with the September party conference remaining the hard deadline. In terms of data releases, it’s a light schedule next week with euro area and UK flash PMIs for June being the highlight. We expect signs of relief following US-Iran de-escalation but will be watching for any sign of broadening inflation pressures.

Macro Focus: The ECB reopens the debate on neutral

The ECB’s chief economist has given another signal that further tightening will be needed

Parsing through the BoE’s communications yesterday we couldn’t help but reflect on the Fed’s shift to more streamlined communication (see here) and the contrast with how much noise there was around the BoE’s relatively simple “wait and see” core message (see here). The individual MPC comments essentially give nine different versions of forward guidance, raising risks of mixed signals and over-interpretation.

As we were working through the comments we saw an eye-catching piece of central bank communication, of another sort, from ECB chief economist Philip Lane. He said that the nominal neutral rate may be as high as 2.50%. It is rare for central bankers to attach precise numbers on the neutral rate – only last week Lagarde was saying that the ECB has “not discussed the neutral rate nor the range of the neutral rate”.

Lane suggested that the upper end of the 1.75-2.25% neutral range published early last year may have “crept up” to 2.50%. This matters for the ECB’s reaction function and the policy implications are clear. First, the case for another 25bp hike is strengthened if policy is less likely to be restrictive than previously assumed. Second, and more importantly for the medium-term outlook, the bar for any subsequent easing has been raised. If neutral is seen as higher, then rates need not fall as far, or as quickly, as previously assumed if the all-clear is declared on second-round inflation risks.

As far as we can see Lane didn’t provide any details about why the neutral rate range may have risen, but it is logical. The standard framework suggests that changes in equilibrium interest rates are determined by shifts in desired investment relative to desired savings (or vice versa). It seems very plausible to our minds that the AI-related investment boom and broader desire to lift defence and infrastructure spending will push up the neutral rate. That may be at least partially offset by a sense of higher uncertainty and volatility (e.g. in response to conflicts) increasing demand for precautionary saving and dampening upward pressure on neutral.

The ECB now thinks the neutral rate might be as high as 2.5%

With Europe certainly not at the epicentre of the current AI-investment cycle, it is also worth bearing in mind that neutral rates are strongly anchored by global trends. In integrated capital markets, shifts in investment demand and saving behaviour in the US and elsewhere will spill over into euro area equilibrium rates, reinforcing the upward pressure.

On the argument that AI-related productivity growth may dampen inflation and reduce the need for further tightening, we are certainly sceptical. While stronger supply dynamics could weigh on inflation, in equilibrium higher productivity growth should push neutral rates higher. Policymakers with a medium-term focus should take this into account.

It’s also worth stressing that any estimate of the neutral rate carries a high degree of uncertainty – it is hard to know where neutral was even with hindsight, let alone in real time. As a result, economists and market participants do look to central banks for guidance. There are potentially feedback loops here. In the years following the GFC, central banks emphasised that policy rates would remain at, or close to, the effective lower bound, implicitly signalling a weak underlying economic environment. That may have weighed on private sector confidence and hence spending and investment decisions – and so added further downward pressure on the neutral rate. The reverse may become true: by openly entertaining the possibility that neutral rates are higher, policymakers such as Lane may, at the margin, influence expectations and behaviour in a way that helps validate that outcome.

Central bankers, we suspect, will be comfortable with rates settling at current or somewhat higher levels, as this would increase the room for manoeuvre when the next shock arrives. In terms of the immediate ECB outlook, a back-to-back move has clearly become less likely following the US–Iran deal and the subsequent retracement in energy prices. We nevertheless continue to expect one further and final hike in Q3.

What we’re watching next week

The UK is on course to have a new PM

Our focus next week will be on UK political developments. Yesterday Labour’s Andy Burnham won the key Makerfield by-election comfortably with 54.8% of the vote, ahead of Reform (34.5%) and Restore (6.8%). Turnout was relatively high for a by-election. While the result itself was expected, this was a huge swing for Labour relative to the local elections. Burnham outperformed the polls and demonstrated an ability to take on Nigel Farage’s Reform party. The implied probability of Burnham becoming UK PM this year has now risen above 90% on Polymarket.

In terms of timing, the party conference (27 September) looks the hard deadline for a leadership transition. For that to be the case, a contest must be triggered by mid-July. We imagine Burnham has sufficient support among Labour MPs to launch a challenge when he chooses, but it's been suggested that he will initially give Starmer space to set out a timetable for his departure. While Starmer has stated that he would run in any leadership election, our view is that a ‘managed coronation’ now seems the most likely scenario with the cabinet telling Starmer that his position is no longer tenable.

A contest would introduce more uncertainty. It would test Burnham and force him to set out his policy platform (and potentially expensive spending packages) in more detail. We are reassured by reports that he's now being advised by ex-BoE chief economist Haldane and the ex-OBR boss Richard Hughes, who bring credibility.

Further ahead, Burnham’s pick for chancellor would be key. It's not inconceivable he retains Reeves in an effort to get markets on his side from the start. There would be jitters about inflationary policies if he goes for someone from the soft left of the party such as Miliband/Rayner. Still, Burnham has already committed to keeping the existing fiscal rules and these provide limited leeway.

The other constraining factor will be Labour’s manifesto pledges. Our assumption is that Burnham wouldn’t seek a new mandate via a general election (but it is a tail risk). So the bottom line is that Burnham’s strong result today has made it very likely that the UK will have a new PM this year, but we still see guardrails in place against a radical fiscal policy shift in terms of tax and spend.

PMIs the focus in a relatively light week of data releases:

In terms of releases, the data flow will be relatively light next week. The flash June PMIs will be the focus. The numbers will likely show relief at US-Iran de-escalation. From a monetary policy perspective, the focus will be on signs of second-round inflation pass-through e.g. in the services output price components. ECB household inflation expectations gauges will also be released, as well as the German Ifo survey.

Key data releases and events (week commencing Monday 22 June)

Day | Time | Region | Event | Period | Consensus | MUFG | Previous |

Mon 22 Jun | 15:00 | EC | Consumer Confidence | Jun P | -18 | -16 | -19 |

Tue 23 Jun | 08:15 | FR | S&P Global France Composite PMI | Jun P | 46.0 | 48.0 | 44.9 |

Tue 23 Jun | 08:30 | GE | S&P Global Germany Composite PMI | Jun P | 49.8 | 50.1 | 48.8 |

Tue 23 Jun | 09:00 | EC | S&P Global Eurozone Composite PMI | Jun P | 49.1 | 50.0 | 48.5 |

Tue 23 Jun | 09:30 | UK | S&P Global UK Composite PMI | Jun P | 50.5 | 51.2 | 49.7 |

Wed 24 Jun | 09:00 | GE | IFO Business Climate | Jun | 85.5 | 85.9 | 84.9 |

Thu 25 Jun | 07:00 | GE | GfK Consumer Confidence | Jul | -28 | -27.5 | -29.8 |

Thu 25 Jun | 07:45 | FR | Consumer Confidence | Jun | 83 | 84 | 82 |

Fri 26 June | 09:00 | EC | ECB 1 Year CPI Expectations | May | 3.9 | - | 4.0 |

Note: All times are GMT+1 (London). Source: Bloomberg, MUFG GMR