BoE Review: A higher bar for action

Macro view: The BoE left rates unchanged at 3.75%, as expected, with a 7-2 vote split and no change to the core guidance. The tone of the statement and messaging reinforced a clear ‘wait and see’ stance. Since the last meeting, softer UK data and the retracement in energy pricing after the US-Iran deal have reduced the urgency for action. The majority of officials are still comfortable that tighter financial conditions will sufficiently counter energy-driven inflation risks. It now seems that the hawks have lost the argument for a proactive, ECB-style hike and we ultimately believe that second-round risks will remain contained given the extent of UK labour market slack. We are therefore dropping our call for tightening this year with the BoE set for a prolonged hold before resuming gradual easing in 2027.

Markets view: UK yields and the GBP have continued to correct lower after today’s MPC meeting. The recent US-Iran deal and softer UK economic data have helped to ease pressure on the BoE to raise rates in response to the energy price shock. The BoE indicated today that they were not in a hurry to tighten policy and wanted time to assess the fallout for the UK economy. We have dropped our own forecast for two BoE hikes this year. It leaves room for the UK yields and the GBP to continuing moving lower as BoE rate hike expectations are scaled back especially against the USD after the Fed opened the door for hikes overnight. UK political uncertainty could add to downside risks for the GBP and gilts after today’s Makerfield by-election.

Macro view: No urgency to act – a prolonged hold is now our base case

The BoE is firmly in ‘wait and see’ mode as it watches for second-round risks

The BoE left rates unchanged at 3.75%, as expected. The 7-2 vote split was in line with our view and the consensus, with Greene joining Pill in voting for a hike. There was no change to the core guidance (the MPC will monitor the impact of the Middle East situation on the economy from and “stands ready to act”). For now, it was noted that “most members” judged that the tightening in financial conditions “provided insurance against inflation risks” but it was “too early to conclude one way or the other” on second-round effects.

In short, this is a central bank firmly in ‘wait and see’ mode. Officials remain happy for now that an “active hold” (i.e. tighter financial conditions relative to pre-conflict expectation for easing) will lean sufficiently against energy-driven inflation risks.

There were no real surprises either in the individual members’ comments. Greene, who voted for a hike, reiterated her hawkish speech this month and called for a “proactive hike” to anchor inflation expectations. Catherine Mann seems closest to siding with Greene and Pill, twice mentioning the possibility that an “activist hike” might be needed in the future. But the other six members are happy to stand pat. Governor Bailey noted that he would “respond promptly” to any signals of second-round effects but is “content at the present time with holding”.

The lack of urgency reflects developments since the last meeting. The BoE may have been ready to act, but there is no pressing need to do so. The US-Iran deal has emerged alongside a string of dovish UK data, including back-to-back downside CPI surprises (see here). Today’s labour market numbers were also soft. There was a favourable revision to the too-bad-to-be-true April payrolls estimate (from -100k to -53k) but there has still been a hefty decline in employment in recent months, despite support from the public sector. The release also showed vacancies declined by 4.2% Y/Y and the slowest rate of private sector regular wage growth since the pandemic (2.9%).

On energy pricing, oil futures are now below even the BoE’s most optimistic Scenario A from April (and indeed our own scenario assumptions). Today’s MPC statement noted that “CPI inflation was now expected to be a little under 3% in 2026 Q3 and pick up to a little over 3¼% in Q4. This was below the path expected in the April Report, reflecting both lower energy and non-energy prices”. That sort of peak rate would be much easier for policymakers to look past (indeed headline inflation reached 3.8% last year – which didn’t stop the BoE from cutting).

Changing our call: we no longer expect any tightening

Our call during the conflict period was for 50bp of front-loaded tightening this year. The run of soft data and a lack of urgency from Bailey in public appearances meant that our conviction around that call was waning even before the US-Iran agreement and energy price retracement. In the absence of any hawkish surprise at today’s meeting, we’re now dropping the call for any tightening completely.

The way we see it is this: there was a reasonable case for ECB-style pre-emptive, measured tightening on a risk management basis. Core inflation has exceeded the target since July 2021 and concerns about structural shifts are valid. Yes, UK monetary policy was mildly restrictive coming into the conflict, but an “active hold” is a technical concept to communicate. We thought policymakers would want to send a clearer signal to firms and households about the intention to keep a lid on inflation risks after another energy shock.

However, the US-Iran deal and sharp retracement in oil pricing, as well as the dovish domestic data flow, have raised the bar for action. It is now clear that the hawks on the MPC have lost the argument for early action. Forward-looking survey numbers have remained broadly benign and our assumption is that second-round effects will ultimately contained in the context of ample labour market slack.

The extension of this change to our call is that we now expect the next BoE move will be a cut. We look back to our pre-conflict call for two further cuts on the back of labour market softness to a terminal rate of 3.25%. All else equal, it will be some time before the BoE is prepared to declare the all-clear on second-round risks. We expect a prolonged pause. But if the US-Iran deal holds, broader domestic price pressures remain contained and 2027 annual pay settlements are target-consistent then the BoE would be back on track to resume quarterly rate cuts from Q1 2027.

Markets view: GBP & UK yields to continue correcting lower

US-Iran deal & softer UK data have helped to ease pressure on BoE to hike rates

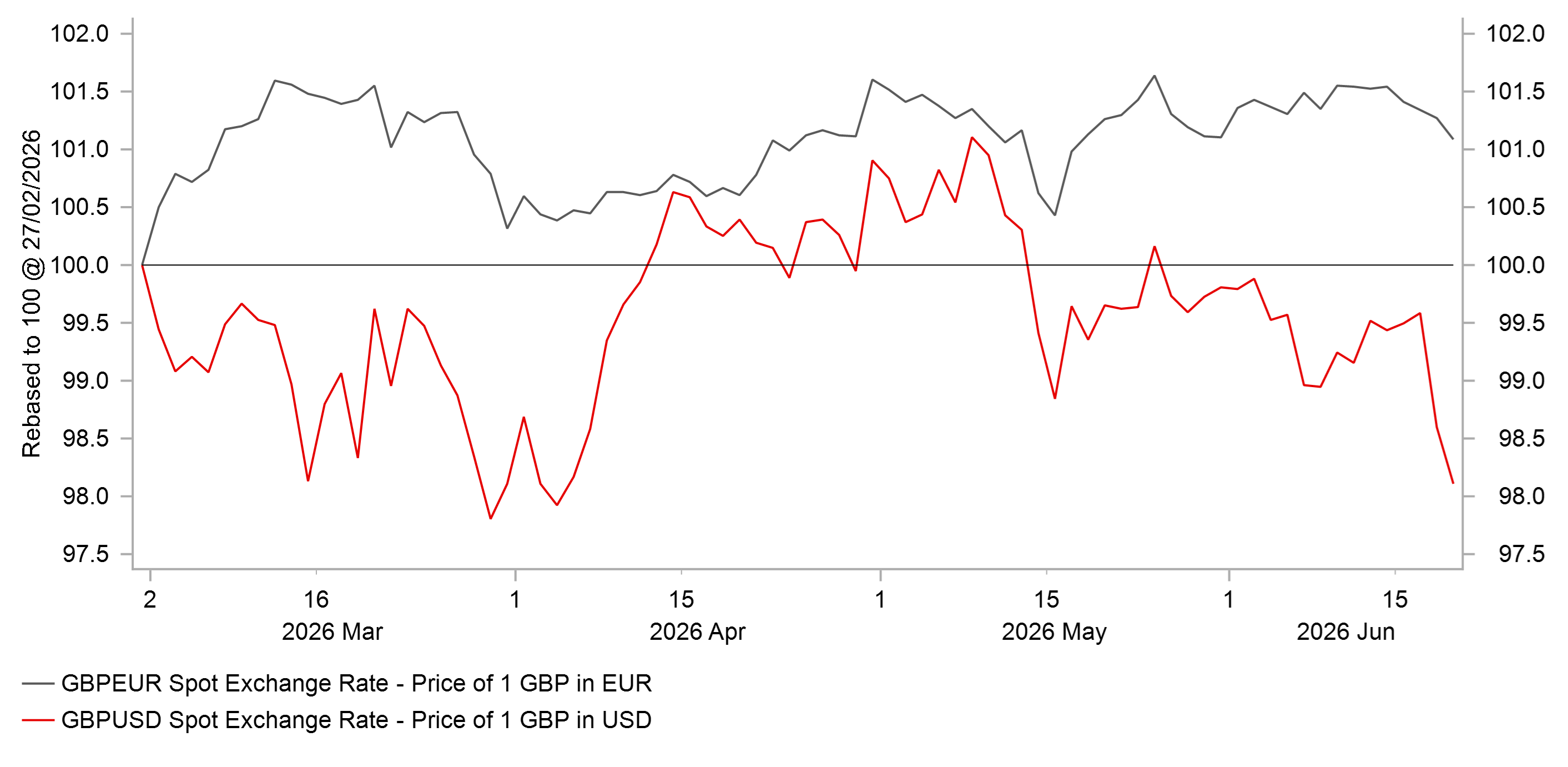

Today’s MPC update has reinforced the recent decline in UK yields, driven by the scaling back of Bank of England (BoE) rate hike expectations, alongside falling energy prices and lower market-based measures of inflation expectations. Since the MPC meeting, 2-year and 10-year gilt yields have declined modestly by around 2–3bps. Market participants have become less confident that the BoE will raise rates in response to the energy price shock. The UK rates market is now assigning slightly less than a 50:50 probability of a rate hike by September, while the likelihood of a hike as soon as next month is negligible. The UK rates market had already begun to price in a lower path for UK rates ahead of today’s MPC meeting, following the announcement of the US–Iran deal over the weekend. In addition, the latest UK CPI and labour market reports released this week have provided the BoE with greater scope to keep rates on hold.

While MPC member Megan Greene joined Chief Economist Huw Pill in voting for a rate hike, the majority of MPC members appeared less concerned about upside inflation risks and emphasised the need to allow more time to assess the impact of the energy price shock on the UK economy. Among those who voted to keep rates on hold, only Catherine Mann appeared close to supporting a hike. As a result, there now appears to be a higher hurdle for the majority to shift in favour of a rate increase as soon as next month. Assuming the US–Iran deal holds, the Strait of Hormuz reopens soon, and there is limited evidence of second-round inflation effects, the case for higher rates is likely to continue weakening. Recent developments have prompted us to revise our forecast, dropping the expectation of two BoE rate hikes this year. Instead, we now expect the BoE to leave rates on hold. This creates scope for UK yields to continue adjusting lower, particularly at the short end of the curve helping to re-steepen the UK yield curve.

Lower UK yields are exerting downward pressure on the GBP. Over the past 24 hours, the GBP has fallen most sharply against the US dollar, reflecting the divergence between today’s BoE policy update and the Fed’s hawkish stance overnight (click here). Cable is currently testing support around the 1.3200 level, where the lows from late March and early April are located. The next key support level then lies at 1.3000 if the USD rebound extends further. We also expect the GBP to weaken against the EUR, albeit more modestly. EUR/GBP has traded within a relatively narrow range between 0.8600–0.8800 this year, and we expect the pair to drift back towards the upper end of that range. The ECB raised rates ahead of the BoE last week, and policymakers have indicated that another hike in the autumn remains possible, despite the ongoing decline in energy prices.

An additional downside risk for the GBP stems from UK political developments. Andy Burnham’s bid to become the next leader of the Labour Party faces an important test today. Opinion polls suggest he holds a 5–12ppt lead in the Makerfield by-election, although the race could prove closer than expected. If Burnham wins, it has been reported that he would quickly put pressure on Prime Minister Keir Starmer to outline a plan for a transition of leadership. Should Starmer be unwilling to step aside, a formal leadership challenge would likely follow, with the aim of installing Burnham as leader ahead of the Labour Party conference in September. Conversely, if Burnham fails to become an MP, it could open the door for another left-leaning Labour figure, such as former Deputy Prime Minister Angela Rayner, to mount a leadership challenge. The uptick in political uncertainty could weigh on both gilts and the GBP. However, Burnham’s recent commitment to adhere to the government’s fiscal rules is helping to mitigate near-term downside risks.

CABLE MOVES BACK TOWARDS MIDDLE EAST CONFLICT LOWS

Source: Bloomberg, Macrobond & MUFG GMR