BoE Review: Ready to act

- Macro view: The BoE left rates unchanged at today’s meeting and made some effort to sound more composed after the surprisingly hawkish March meeting. But this was an “active hold” which left little doubt that future tightening is on the cards. While there was only one vote in favour of a hike at this point, most MPC members continue to signal a readiness to raise rates if supported by data. The BoE also presented new scenarios, skewed towards more persistent inflation pressures that would be hard to look past. We have added an extra hike to our call and now see 50bp of BoE tightening this year. There is sufficient groundwork in place for a hike as soon as June, we think, with the case for a hike at the next meeting likely to get stronger if upcoming data were to show any sign of rising wage pressures.

- Markets view: The BoE’s communications today were broadly consistent with rates market pricing ahead of the meeting and hence there has been no jump in yields in response to the strong signal of rate hikes to come. Today has also seen some broad-based US dollar selling, in part following dollar-selling intervention by the MoF/BoJ in Japan (not confirmed officially but highly likely). We see risks to the pound still skewed to the downside with yield / FX dynamics less clear during periods of uncertainty. Raising rates in circumstances of weak economic conditions can be undermine currencies and increased market volatility and the potential for increased political uncertainties in the UK could weigh on GBP performance ahead even in circumstances of two rate hikes ahead.

Macro view: ‘Ready to act’ – the BoE maintains a clear tightening bias

We continue to expect a moderate degree of tightening

The BoE left rates unchanged, as expected, in what was essentially a continuation of previous messaging. The margin of dissent was smaller than we anticipated. Only Huw Pill voted for a hike at this point in an 8-1 split (we expected 7-2, as set out here: BoE preview – Trying to sound calm). Some of the language used also seemed more sober than last time, and Governor Bailey noted that policy is in a “reasonable place”. But we interpret that as an effort to convey a relative sense of patience and composure after the misjudged communication in March, rather than shift in thinking.

As Bailey himself put it, it was an “active hold”, and the BoE maintains its clear tightening bias. There was no pushback against market expectations for multiple hikes this year. While it was just Pill voting for a hike at this juncture, almost all the individual member comments suggested a willingness to raise rates in certain scenarios.

To our minds, the most pertinent fact for policymakers is that it has been over two months since the start of the conflict and the Strait of Hormuz remains essentially closed. The challenge of fully restoring normal shipping conditions looks increasingly difficult which makes inflationary risks increasingly hard to look through. Despite that, there was no discernible change in rhetoric from the BoE today in order to dial up the sense of urgency. However, as noted above, the March meeting was surprisingly (and perhaps unintentionally) hawkish, which makes steady messaging more understandable.

At the time of writing, market participants have priced ~15bp of hikes at the June meeting. We see June as the most likely point for the first hike. By then, there will likely be further evidence of energy price pass-through and associated second-round risks, so the argument for patience will become less tenable. Several MPC members cited the tightening in financial conditions on the back of hike expectations as something which grants them time to assess the data. But at some point this will need to be backed up by actual action (with obvious credibility risks for the BoE if not, unless supported by a significant improvement in the inflation outlook).

Pre-meeting, our call was for one hike this year, but as noted in the preview, we were leaning towards adding another if communication at this meeting supported it. That’s the case and we now see 50bp of BoE rate hikes this year. Two hikes would take rates into meaningfully restrictive territory, while also sending a clear message on the BoE’s intentions to get ahead of risks related to inflation expectations. Further tightening is plausible, but our assumption is that it will get harder later in the year as the UK demand backdrop weakens.

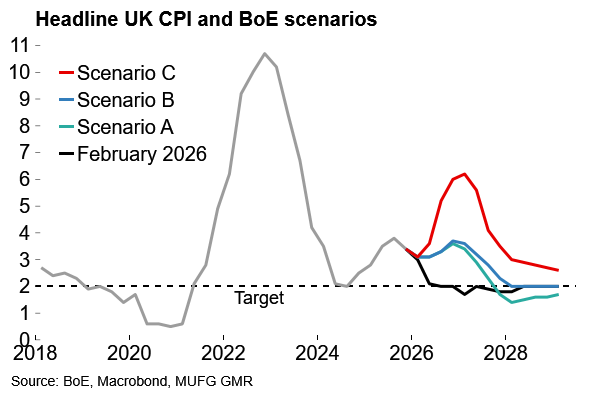

The BoE is working on the basis of scenarios rather than forecasts

In our preview, we wrote that the BoE would likely downplay the significance of its updated central projections and instead focus on a range of scenarios given elevated uncertainty. At the finish, no central projection was presented at all, with three scenarios (A, B and C) laid out instead: “In Scenario A, energy prices were assumed to follow market futures curves, while in Scenarios B and C, these were higher and more persistent than the futures paths to varying degrees.”

The chart below shows the estimated inflation path under each. The main difference between Scenario A and B is persistence. Both show inflation peaking around 4% around the turn of the year (which is close to but slightly below our current central assumption), but B has a more gradual return to target. Inflation is estimated to peak slightly above 6% in Scenario C. That is similar to our own scenario analysis of plausible worst-case inflation scenarios with clear second-round effects e.g. in wage growth.

The BoE’s new inflation scenarios show varying degrees of persistence

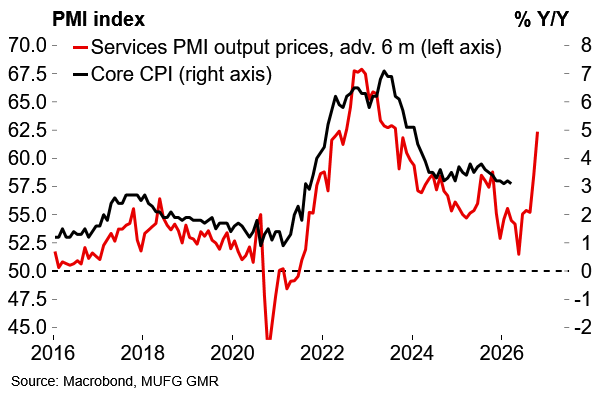

Survey data is already pointing to rising second-round risks

Almost all MPC members are open to rate hikes if required

Looking through the individual members’ comments, most officials judge Scenario B to be the central scenario here. Only the most dovish members are placing weight on Scenario A, while the hawks are leaning towards C.

All MPC members apart from Alan Taylor show a willingness to tighten policy if required (Taylor sees neutral at 3% and hence policy is already restrictive to his mind). Our quick take – and these comments might be qualified by officials in upcoming speeches – is that there are three members who would be likely to vote for a hike in June (Pill, Greene, Mann) but others would join them if evidence of second-round risks continues to mount. Lombardelli is certainly hawkish but seems willing to wait for data. Breeden is open to hikes too but will be guided by the data.

Governor Bailey was slightly more neutral/balanced than we expected, emphasising the trade-off between growth and inflation (agan, possibly that is in response to criticism of the communication around the March meeting). But Bailey does state that if second-round effects were to increase then “policy should focus on returning inflation back to target more quickly” and he could credibly vote for tightening in June based on these comments.

Future votes are likely to be tight – no change there on a divided MPC! – but the bottom line is that, on balance, the BoE continued to suggest it will place more weight on rising second-round inflation risks than growth risks. There are plenty of inflation pressures in the pipeline and expectations have already risen markedly, as we discussed in the preview. In the absence of swift and credibly durable de-escalation in the Middle East, we continue to expect that the BoE will follow through on its messaging by delivering a moderate degree of tightening this year.

Markets view: How rate hikes unfold key for pound

FX & yields not clearcut

As laid out above, the BoE sees it as most plausible that some degree of monetary tightening will probably need to be delivered given the shift in inflation risks to the upside following the surge in energy prices. I think the financial market reaction needs to be viewed in the context of what’s gone before. In particular, the 2-year Gilt yield from the closing low-point on 17th April had jumped 45bps to yesterday’s close and the OIS market had added 40bps of tightening by the BoE through the remainder of the year to fully priced three rate hikes by year-end. While we would describe the outcome of today’s MPC meeting as generally hawkish, there was nothing dramatically surprising to encourage market participants to add to the three rate hikes priced going into the meeting. In addition, crude oil prices after surging increasing yesterday have given back some of those gains today which is helping drive yields lower globally. The OIS curve is still pricing between two and three hikes from the BoE through the remainder of the year, which to us looks about right based on the outcome of the meeting.

Furthermore, the move higher in UK yields is already considerably more than the moves we have seen in Europe or the US. Since the conflict began, the 2-year Gilt yield closed yesterday over 100bps higher. Over the same period, the German equivalent yield was up 75bps and the US 2-year was up 58bps. Most of the MPC members appears to be Scenario B camp that points to between two and three hikes and hence the market was already well priced.

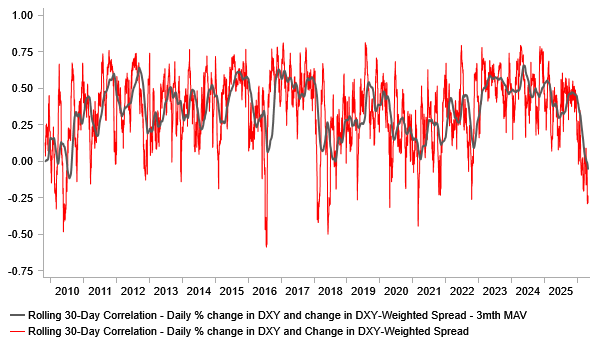

For the pound, the yield / FX dynamic is not particularly reliable in times of uncertainty related to non-macro factors like geopolitics and/or an energy-driven shock. Indeed, our DXY vs dxy-weighted 2-year swap spread correlation has weakened significantly to levels we haven’t seen since the GFC. In any case, with the ECB set to deliver a similar degree of tightening yield-driven GBP demand may not be that notable. Furthermore, if the conflict / closure of the Strait of Hormuz is extended, risk conditions are likely to worsen and, in that scenario, we would expect the pound to underperform. The MPC tightening in a higher volatility backdrop would likely see the pound suffer. Similarly, UK political uncertainty could also be about to rise with PM Starmer position possibly under threat following the local election results next week and that dynamic would take precedent over yield. So, while we are adding another rate hike from the BoE to our forecast profile, we see GBP risks still skewed to the downside and expect EUR/GBP to drift higher through the remainder of this year.

USD & YIELD SPREAD CORRELATION HAS WEAKENED SHARPLY

Source: Bloomberg, Macrobond & MUFG GMR