We expect the Bank of England will hold rates this week while attempting to convey a sense of patience and composure. But it will be hard to dial back the hawkish tone set in March. The Strait of Hormuz remains effectively closed and recent data shows both rising inflation expectations and better-than-expected growth momentum since the start of the year. Against this backdrop, we look for a 7-2 vote split, with two members dissenting in favour of a hike. That would lay the groundwork for a hike as soon as June, especially if upcoming data shows hints of rising wage pressures. We continue to expect modest tightening this year with the BoE seeking to get ahead of rising second-round inflation risks.

A hold, but hawkish developments will be hard to ignore

We expect the BoE will leave policy unchanged at this week’s meeting but leave little doubt that rate hikes are on the radar. The BoE’s initial reaction to the Iran conflict was on the clumsy side (we expected balanced messaging in March but it was a surprisingly hawkish hold – see here). Policymakers will likely try to convey a message of patience this time, emphasising that there is time to assess for second-round inflation risks in the data. The relatively contained move in natural gas prices since the start of the conflict (front-month prices have retraced since the last meeting) does reduce the urgency.

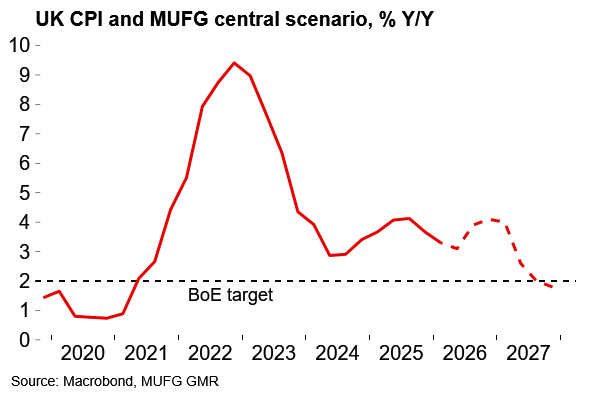

But to our minds the most pertinent fact for policymakers is that six weeks on, the Strait of Hormuz remains essentially closed. Oil pricing is very similar to where we were at that hawkish March meeting. Prediction markets currently imply less than 40% probability that the Strait opens by end-May. Policymakers will be very aware that the longer that disruption continues, the more likely that structural shifts in price- and wage-setting will become. As things stand, as we set out here, we see UK inflation peaking just north of 4% on our current energy assumptions, with waves of price pressures ahead.

Since the last meeting, a range of data points to the UK economy carrying considerably more momentum at the start of the conflict than expected. We are tracking Q1 GDP growth at 0.55% Q/Q and the PMI data for April suggests surprisingly resilient activity this month. On inflation, the headline rate increased by 30bp to 3.3% in March, broadly in line with the BoE’s expectations (“close to 3½%”).

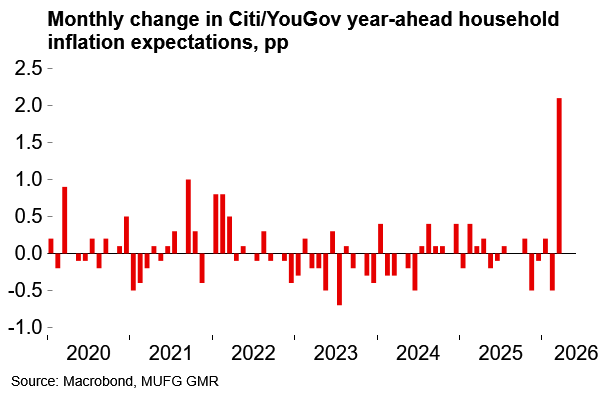

In many ways, spot inflation doesn’t really matter. Higher fuel prices quickly and mechanically lift headline rates. From a monetary policy perspective, the focus is squarely on second-round risks. Again, the numbers have been on the hawkish side. The Citi-YouGov year-ahead measure of household inflation expectations surged by 2.1pp in March. That outsized move adds to the sense that the 2022 energy shock and policy-driven ‘hump’ in inflation last year are fresh in households’ memories. Meanwhile, the output price component of the services PMI is now at the highest level since February 2023.

There was a counterweight to these numbers in last week’s DMP survey of firms which showed expected wage growth unchanged at 3.5%. Only a net 10% of firms expect wages to increase in response to the energy price shock. The latest labour market data also showed further declines in payroll employment, and the single-month rate of private sector pay easing to 2.8% Y/Y, the lowest figure since 2020. But, on balance, we see the flow of data since the previous meeting as having reinforced the hawkish side of the policy debate.

So, for all the likelihood that the BoE will seek to project calm, we think it will be difficult to credibly row back on the hawkish messaging from the March meeting. It will certainly be hard to get the tone right, especially with the hawks likely to become more vocal in light of the data set out above. Our immediate focus will be on the vote split and the individual member comments of non-dissenters on the plausibility and possible timing of hikes.

We look for a 7-2 vote split with two dissenters for a hike

On the vote, we expect a 7-2 split with chief economist Pill and external member Mann both voting for a hike. Pill recently said that the BoE must “entertain the possibility that more [restriction] may be required” which clearly opens the door to a dissent. Mann, meanwhile, is a self-styled ‘activist’ member of the MPC and we suspect she will be keen to emerge as one of the first to vote for a hike. There is a chance that Mann holds fire for now before later voting for a bumper 50bp move – but that loses its impact if others are already voting for hikes. Lombardelli is another potential dissenter – a 6-3 vote wouldn’t be a huge shock, to our minds. We might have gone that way if the DMP survey showed rising wage growth expectations, which we think is the key for policymakers right now. Even a slight increase in those numbers would be seen as a cause for concern.

It’s also worth noting that this is a quarterly projection meeting. But we expect that the BoE will downplay the significance of its updated central projections and instead focus on a range of scenarios, which could give some clues about its reaction function.

We expect UK CPI will peak above 4% before normalising relatively quickly…

…but household inflation expectations have surged and the BoE will be mindful of structural risks

Outlook – Tightening ahead, with June in play

Looking ahead, we expect the BoE will ultimately deem that a modest rise in interest rates is appropriate, and that moving relatively early reduces the risk that more forceful action will be required later. Our base case is that there will be a hike in June, but we’d expect another tight vote which could come down to Bailey’s interpretation of the balance of risks. July is plausible – normally we’d emphasise that it’s a projection meeting, but as noted above, the BoE is likely to downplay its central scenario given elevated uncertainty.

Beyond that, our current call is for just one 25bp hike this year – our sense was that the BoE would move early to try to send a clear message, but that a US-Iran peace settlement and weaker domestic demand backdrop would make it harder to tighten policy after the summer. But we are now leaning towards adding another hike this year given the apparent resilience of the UK economy coming into this crisis and the length of disruption in the Strait of Hormuz. We will assess the call after the meeting.