- Macro focus – Where will UK inflation peak? UK headline inflation rose to 3.3% in March, driven by energy prices. Looking ahead, the near-term profile will be bumpy with various downward pressures in April, but we expect the upward trend to resume as the energy shock propagates through the economy. We see headline rates peaking slightly above 4% at the turn of 2026/27, before favourable base effects support normalisation next year.

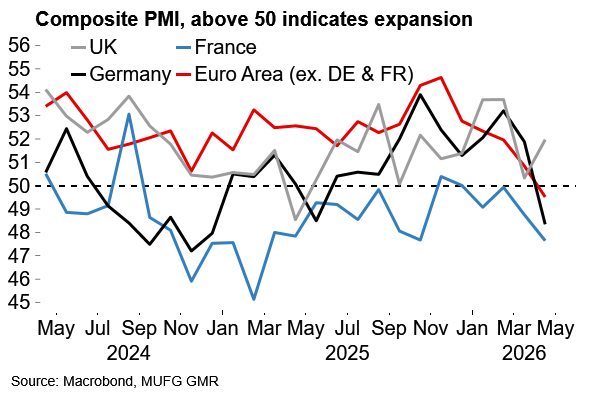

- The week that was – Surveys start to show the damage: The euro area PMIs weakened sharply in April, pointing to limited growth momentum once front‑loaded manufacturing support fades. At the same time, there was clear evidence of mounting cost pressures with output prices in the services sector, especially in Germany, raising second-round inflation concerns. The UK PMIs showed similar cost pressures as well as surprising signs of stronger near‑term activity. However, softer labour market data and easing pay growth numbers earlier in the week helped to offset some of the hawkish implications for the BoE from the PMI data.

- What we’re watching next week: Another ECB/BoE double-header on Thursday is likely to see both central banks leave rates unchanged while keeping the door open to hikes down the line. On the data side, energy effects are set to push headline euro area inflation higher, but markets will likely focus less on spot inflation prints for now and more on signs of second‑round pressures in surveys.

Macro Focus: Where will UK inflation peak?

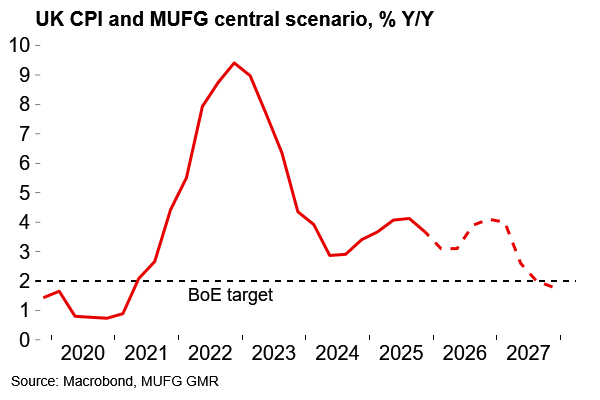

We expect UK CPI to move above 4% by year-end

UK inflation jumped from 3.0 to 3.3% Y/Y in March (consensus: 3.3%, MUFG: 3.4%), mostly driven by motor fuels and heating oil. There was also an airfare effect related to the timing of Easter (all prices were collected before the conflict). Softer core goods inflation (0.8% Y/Y), especially in clothing, limited the overall rise in the headline rate. On the other hand, underlying services inflation edged slightly higher to 4.2% on our calculations. But there were no major surprises overall. The headline figure is in line with the BoE’s view at the last policy meeting that inflation would be “close to 3½% in March”.

Looking ahead, we expect the April number will come in lower, driven by favourable base effects, the reduction in the household energy price cap (which reflects pre-Iran wholesale costs), and government energy policies announced at the Autumn 2025 Budget. But these factors are likely to provide only temporary relief. Following the immediate pass-through from the conflict to fuel costs, we expect further waves of inflationary pressures as the energy shock propagates through the economy. The household energy cap will increase (~15%) in July. Meanwhile, jet fuel and other specific shortages (e.g. plastics, chemicals) are set to increasingly show up in the CPI over coming months. Diesel costs will likely push up core goods prices more generally and higher fertiliser costs will gradually feed through to food prices too.

We expect UK CPI will peak above 4% before normalising relatively quickly…

…but household inflation expectations have surged and the BoE will be mindful of structural risks

Putting it all together, we expect UK CPI to average 3.5% in 2026 with monthly rates peaking above 4% around the turn of the year into 2027. This assumes that 1) energy prices will remain well above our pre-conflict baseline, reflecting persistently higher risk premia and physical supply issues following damage to infrastructure, 2) there will be limited fiscal support (but some BoE tightening), and 3) there will be unexpected ‘extra’ channels of inflationary pressures from protracted Hormuz disruption. Even with those assumptions we think it’s unlikely that inflation will go much north of 4%, in the absence of more adverse energy developments.

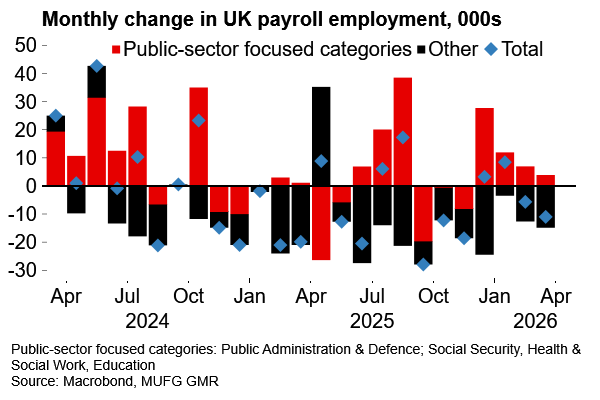

Further ahead, favourable base effects are then likely to bring headline rates down relatively quickly under our central energy scenario. Indeed, we expect a broadly similar inflation profile in terms of peak and duration to the ‘hump’ seen in 2025 (see chart below). This is not 2022 and the scope for second-round effects is more limited, despite some hawkish signs in this week’s April PMI on services price pressures and activity more broadly. The UK jobs data out this week was on the soft side and points to plenty of slack coming into the conflict period – private-sector focused payroll employment is down 120k over the past year – so employee bargaining power is likely to be relatively limited. Our current expectation is that headline inflation will ease and dip just below target by end-2027.

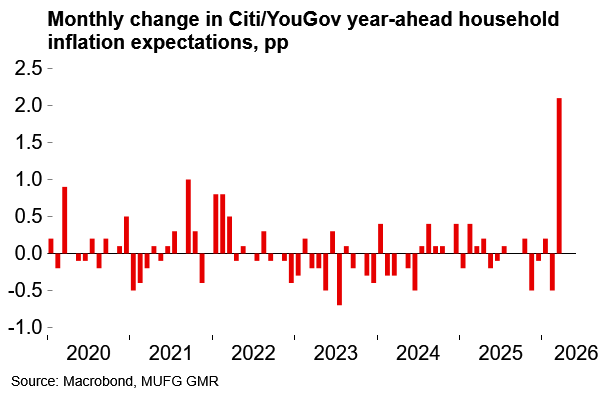

But we still lean towards there being some precautionary tightening (i.e. at least one hike) from the BoE given high uncertainty around the scope for structural changes in wage- and price-setting behaviour. The risk that higher inflation may increasingly be seen as the new normal is clear. On our forecasts, UK headline inflation will average over 5% in 2022-26. Year-ahead household inflation expectations have already surged from 3.3% to 5.4% and today’s BoE DMP survey data showed firms’ selling price expectations have also risen sharply.

It will be some time before there is definitive evidence on second-round inflation effects, or to what extent the inflationary pressures described above actually seep into wage growth. Given that, our view remains that policymakers will see greater risks of a policy error in being slow to react relative to the risks of early tightening and then calibrating lower if second-round pressures do not materialise.

Against that background, it will be hard for the BoE to get the tone right next week. We see scope for several MPC members to vote for a hike, prompted by recent survey data. That would give a clear hawkish slant to proceedings, even if the central communication is relatively more balanced. Note we will release a full BoE preview on Monday.

The week that was

Euro area survey data starts to show the damage

The flash April PMIs were weaker than expected. The euro area composite number slid from 50.7 to 48.6. The euro area composite PMI fell to 48.3 in the April flash numbers (cons: 50.1, MUFG: 49.6), a 17-month low. This weakness is despite some front-loading boost to manufacturing ahead of anticipated disruption to come. That will reverse and likely weigh further on survey numbers later in the year. Meanwhile the services sector looks particularly weak (47.4, 62-month low), which raises some concerns around underlying consumer demand. That said, for now at least, the employment numbers are showing resilience with a small improvement in the euro area number. But, overall, these PMIs, assuming a constant profile through the quarter, would be consistent with a mild contraction in Q2. A range of other survey data (e.g. the German ZEW and Ifo, national consumer confidence numbers) also softened notably.

In terms of inflationary pressures, there was no surprise to see input prices rise sharply in the PMIs. But the rise in services output price expectations, driven by Germany, will have raised eyebrows at the ECB as officials mull over the threat from second-round inflation risks.

Further weakness in the euro area PMIs

There is still plenty of slack in the UK labour market

The UK economy is carrying more momentum than expected

There was a notable positive surprise in the UK PMI with the headline index rising from 50.3 to 52.0 (cons: 49.8, MUFG 49.7). Manufacturing was temporarily boosted by front-loading, as in the euro area. But services rising from 50.5 to 52.0 is certainly surprising and harder to explain. The UK economy seems to have better underlying momentum than we assumed, at least at the start of Q2. We still expect activity will fade over coming months as the energy shock increasingly bites but it is a better-than-expected starting point. As noted last week (here), we have recently lifted our 2026 GDP assumption from 0.5% to 0.8%.

On prices, as was the case with the German numbers, UK services output prices rose sharply, to the highest level since early 2023. That will raise concerns of second-round risks and, combined with the resilient activity numbers and last week’s GDP beat for February, will bolster hawkish arguments at the BoE. On the other hand, the doves on the MPC will likely focus on Tuesday’s soft labour market numbers which showed more deterioration in payrolls and further easing in private sector pay pressures (the single-month rate fell to 2.8% Y/Y, the lowest since 2020). The headline unemployment rate fell from 5.2% to 4.9% but this reflects a rise in the inactivity rate (i.e. fewer people actively looking for work). The PMI employment gauge remains in contraction territory.

It’s certainly a mixed picture for the BoE as it contends with stagflation risks but, as noted above, we expect policymakers will err on the side of caution around second-round inflation risks.

What we’re watching next week

Euro area inflation to rise further on energy costs

There’s plenty of euro area data next week with the release of initial Q1 GDP estimates and the flash inflation numbers for April, as well as more survey evidence with the European Commission numbers.

On growth, we are tracking euro area GDP at 0.2% in Q1 with the economy carrying only limited momentum into the energy shock.

On inflation, energy effects are likely to continue to lift headline euro area inflation (we expect a headline figure of 3.0%, from 2.6% previously). Further ahead there could be some limited relief in the May numbers on the back of fiscal policy decisions such as the German government’s temporary move to cut fuel duty from 1 May to 30 June. But spot inflation numbers are unlikely to be market moving with energy costs passing through quickly and mechanically, especially through the fuel channel. Further ahead, individual components will become more important as we look for wider pass-through and unexpected inflationary sources. But from a monetary policy perspective, attention will remain firmly on second-round risks for now. Next week’s release of the ECB’s 1 and 3-year household inflation expectation gauges will garner more attention than usual, as will the price components of the European Commission’s survey.

No change from the ECB or BoE, for now

Next week will also see another ECB/BoE double-header on Thursday. Thankfully for beleaguered European economists it’s the last time that meetings fall on the same day until December. We set out our ECB views in the preview here – we do not expect any policy change for now but see 25bp hikes at both the June and July meetings. We’ve discussed the UK inflation outlook and challenges for the BoE above and will release a full preview on Monday. Again, we do not expect any policy change at this juncture but see plenty of scope for tightening further down the line.

Key data releases and events (week commencing Monday 27 April)

|

Day |

Time |

Region |

Event |

Period |

Consensus |

MUFG |

Previous |

|

Mon 27 Apr |

07:00 |

GE |

GfK Consumer Confidence |

May |

-30 |

-32 |

-28 |

|

Tue 28 Apr |

09:00 |

EC |

ECB 1 Year CPI Expectations |

Mar |

- |

- |

2.5 |

|

Wed 29 Apr |

10:00 |

EC |

Economic Confidence |

Apr |

95.8 |

94.8 |

96.6 |

|

Wed 29 Apr |

13:00 |

GE |

CPI EU Harmonized YoY |

Apr P |

3.2 |

3.1 |

2.8 |

|

Thu 30 Apr |

06:30 |

FR |

GDP QoQ |

1Q P |

0.2 |

0.1 |

0.2 |

|

Thu 30 Apr |

07:45 |

FR |

CPI EU Harmonized YoY |

Apr P |

2.3 |

2.4 |

2.0 |

|

Thu 30 Apr |

08:55 |

GE |

Unemployment Change (000's) |

Apr |

5.0k |

10.0k |

0.0k |

|

Thu 30 Apr |

09:00 |

IT |

GDP WDA QoQ |

1Q P |

0.2 |

0.2 |

0.3 |

|

Thu 30 Apr |

09:00 |

GE |

GDP SA QoQ |

1Q P |

0.2 |

0.2 |

0.3 |

|

Thu 30 Apr |

10:00 |

EC |

GDP SA QoQ |

1Q A |

0.2 |

0.2 |

0.2 |

|

Thu 30 Apr |

10:00 |

EC |

CPI YoY |

Apr P |

2.9 |

3.0 |

2.6 |

|

Thu 30 Apr |

10:00 |

EC |

CPI Core YoY |

Apr P |

2.2 |

2.3 |

2.3 |

|

Thu 30 Apr |

10:00 |

EC |

Unemployment Rate |

Mar |

6.2 |

6.3 |

6.2 |

|

Thu 30 Apr |

10:00 |

IT |

CPI EU Harmonized YoY |

Apr P |

2.2 |

2.3 |

1.6 |

|

Thu 30 Apr |

12:00 |

UK |

Bank of England Bank Rate |

30-Apr |

3.75 |

3.75 |

3.75 |

|

Thu 30 Apr |

13:15 |

EC |

ECB Deposit Facility Rate |

30-Apr |

2.00 |

2.00 |

2.00 |

Note: All times are GMT+1 (London). Source: Bloomberg, MUFG GMR