- ECB outlook: This week has seen a continued shift in ECB communication, with officials stressing data dependency and signalling a willingness to be patient. An April hike now looks unlikely, but there is plenty of inflation in the pipeline which will be hard for policymakers to ignore. In our central scenario we still expect 50bp of hikes this year, starting by June, even if the ECB is not as keen to get ahead of the curve as we initially assumed.

- UK growth: The UK economy has again started the year on a strong footing. The positive surprise in the February GDP figures has led us to raise our 2026 GDP forecast from 0.5% to 0.8%, but the good news is likely to be fleeting. Growth is set to falter over coming months as higher energy costs and tighter financial conditions weigh on activity.

- Week ahead: Next week will be busier on the data front. PMI and national surveys will likely confirm rising price pressures and weakening activity. UK CPI is set to rise further, while labour market resilience would give the BoE scope to focus on underlying inflation dynamics.

Weekly Focus - Is the ECB losing its nerve?

|

Euro area – Our latest forecasts |

|||

|

|

2025 |

2026 |

2027 |

|

GDP |

1.4 |

0.7 |

1.1 |

|

CPI |

2.1 |

3.0 |

2.3 |

Not so proactive after all: In a quiet week of data the focus has been on central bank communication with several officials speaking around the IMF meetings. The ECB’s initial messaging on the energy price shock indicated a willingness to be proactive in containing inflation risks, lifting market rate expectations considerably higher. We adjusted our call accordingly and assumed that policy would be tightened at the next policy meeting on 30 April (see here). But since then, there has been a discernible shift in tone with various officials dialling back the sense of urgency in recent public appearances. This week, Lagarde emphasised that the ECB “would need data to act”, but that it could demonstrate its “agility” once there is “enough data, enough information”. At the same time there’s been a notable lack of any discussion around the potential for an April move from the hawkish figures on the Governing Council. The minutes from the last meeting, out yesterday, also talked about maintaining a “steady hand”.

Given this, we have pushed the timing of the first move back from April to June and have less conviction that a hike then will be followed up with a back-to-back move. But we still expect the same amount of tightening this year (50bp). There is now plenty of inflation in the pipeline regardless of what happens on the geopolitical front. Higher fuel prices have already pushed headline euro area inflation up to 2.6% in March – the highest rate since July 2024. Further waves of inflationary pressures are set to follow – e.g. in jet fuel, household energy, food prices, core goods – and the headline rate looks set to exceed 3% in coming months.

The slew of survey data over coming weeks (e.g. PMIs, European Commission, national surveys) is likely to show rising price pressures, both realised and expected. There would be, we maintain, sufficient data to move this month if the ECB were minded to do so. An April hike still shouldn’t be entirely ruled out. After all, policymakers have stressed that they will be “agile”. But it seems that officials see some option value in waiting until at least June for data to confirm the initial signals. As we noted here, the relative strength of the euro may have reduced the sense of urgency as well.

Still, there won’t be any definitive evidence on second-round effects – i.e. on the pass-through to wages – for months. Whether or not it is worth getting ahead of the curve to cap medium-term inflation risks will always be a judgement call. That raises the question – does the shift in communication indicate that the ECB is losing its nerve around the need for rate hikes at all? For all the initial rhetoric around the readiness to act, there will always be concerns around making a policy mistake by tightening into a supply shock, especially without the cover of the Fed leading a global tightening cycle. But there will also be an awareness that there are credibility risks if the ECB does not follow through with tightening. As Lagarde herself put it, “the public may find it difficult to understand a reaction function that does not react”. Higher inflation is coming. To our minds, there is a clear argument for front-loading rate hikes to reduce the risk of more forceful action being required later on, and we continue to expect tightening – even if it’s not quite so front-loaded as we were initially led to believe. We will release a full ECB preview next week.

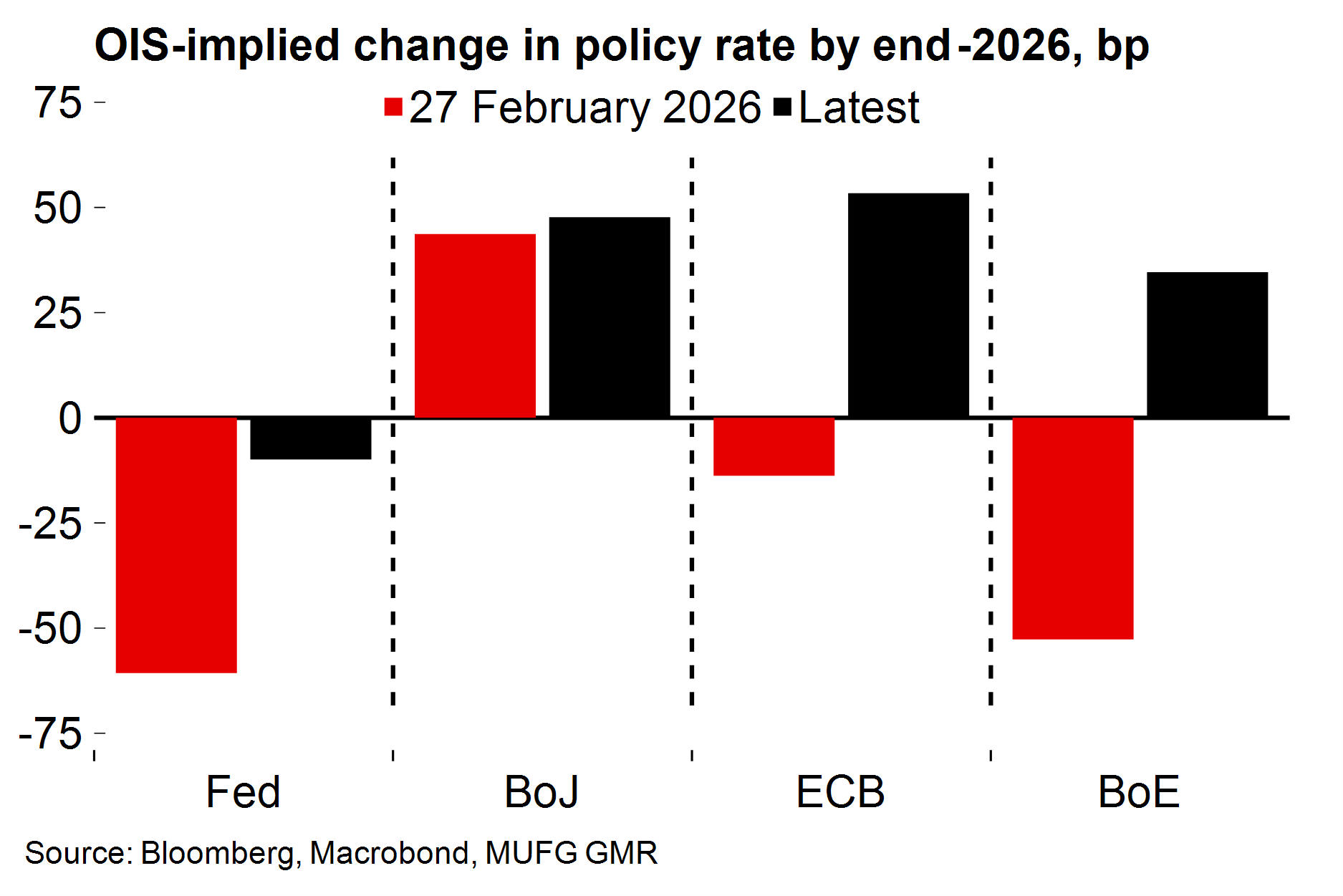

Markets continue to price in cross-Atlantic divergence

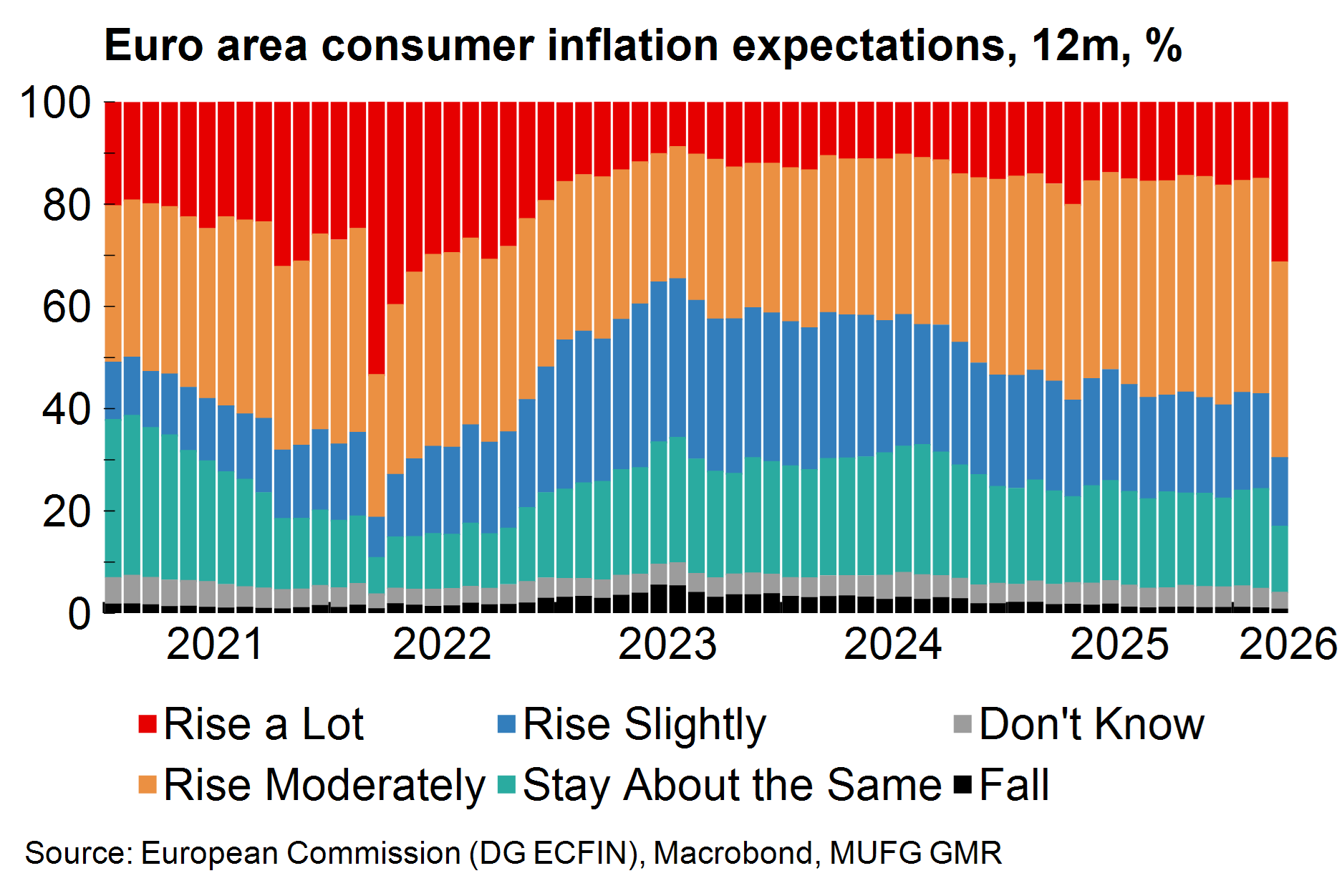

Household inflation expectations have moved higher

|

UK – Our latest forecasts |

|||

|

|

2025 |

2026 |

2027 |

|

GDP |

1.4 |

0.8 |

1.0 |

|

CPI |

3.4 |

3.6 |

2.4 |

UK growth outlook – A case of what might have been: Aside from central bank speakers around the IMF meetings, it’s been a quiet week in Europe with little to report on the data front. The most notable release was the 0.5% M/M growth in UK GDP in February, well above the consensus (0.1%). With an upward revision to the January figure, the economy started the year on a decent footing after muted growth in H2 2025. Even assuming some payback and drag on sentiment from the conflict in the March numbers, it’s now hard to see Q1 growth below 0.5% Q/Q, in the absence of revisions. This is significant for annual average GDP growth, and we have lifted our 2026 GDP assumption from 0.5% to 0.8% on the back of these numbers.

In different circumstances we would have been heralding this as a solid platform for growth, with potential for further BoE easing to support the expansion. But the good news is likely to be fleeting. Higher energy costs and the shift in monetary policy expectations (the BoE is likely to remain on hold at least, with some tightening certainly conceivable now) clearly point to growth tailing off sharply over coming quarters. Persistent domestic political risks add another element of uncertainty to the outlook.

Zooming out, the latest data does little to dispel long-standing suspicions that there’s some residual seasonality in the data with the economy yet again repeating its pattern of making a fast start to the year (Q1 growth came in at 0.7% Q/Q in 2025 and 0.8% in 2024). But we also think that there is some ‘policy seasonality’ at play here. The recent cycle of intense speculation around the need for consolidation at the Autumn Budget, followed by relief that measures are not as painful as feared has likely contributed to the UK’s bumpy GDP profile.

What we’ll be watching next week

Survey data in focus: A slew of survey data next week will provide a further steer on the impact of the conflict on activity and inflation pressures. We expect the composite PMI to slip below the breakeven mark of 50 in both the euro area and the UK. National surveys, including the German ZEW and ifo, are likely to show similar deterioration. From a monetary policy perspective, the focus will be on the pricing components in the PMIs, especially in the services sector.

UK inflation set to rise: There will also be a range of UK data out next week – inflation, labour market, public finance, and retail sales. Headline CPI is set to have risen in March on the back of rising fuel costs (MUFG: 3.4%), but we expect the core rate to remain broadly unchanged. The latest GDP data, discussed above, does not point to a sharp deterioration in the labour market. We think there could be another positive payrolls figure and an unchanged headline unemployment rate. Some stability in the labour market numbers would allow the BoE to focus on underlying inflation pressures.

Key data releases and events (week commencing Monday 20 April)

|

Day |

Time |

Region |

Event |

Period |

Consensus |

MUFG |

Previous |

|

Tue 21 Apr |

07:00 |

UK |

Average Weekly Earnings 3M/YoY |

Feb |

3.6 |

3.7 |

3.9 |

|

Tue 21 Apr |

07:00 |

UK |

ILO Unemployment Rate 3Mths |

Feb |

5.2 |

5.2 |

5.2 |

|

Tue 21 Apr |

07:00 |

UK |

Payrolled Employees Monthly Change |

Mar |

-5k |

6k |

20k |

|

Tue 21 Apr |

10:00 |

GE |

ZEW Survey Current Situation |

Apr |

-70 |

-70 |

-62.9 |

|

Wed 22 Apr |

07:00 |

UK |

CPI YoY |

Mar |

3.3 |

3.4 |

3.0 |

|

Wed 22 Apr |

15:00 |

EC |

Consumer Confidence |

Apr P |

-17.0 |

-18 |

-16.3 |

|

Thu 23 Apr |

07:00 |

UK |

Public Sector Net Borrowing |

Mar |

10.4 |

- |

14.3 |

|

Thu 23 Apr |

08:15 |

FR |

S&P Global France Composite PMI |

Apr P |

49.0 |

47.8 |

48.8 |

|

Thu 23 Apr |

08:30 |

GE |

S&P Global Germany Composite PMI |

Apr P |

51.2 |

50.6 |

51.9 |

|

Thu 23 Apr |

09:00 |

EC |

S&P Global Eurozone Composite PMI |

Apr P |

50.1 |

49.6 |

50.7 |

|

Thu 23 Apr |

09:30 |

UK |

S&P Global UK Composite PMI |

Apr P |

49.8 |

49.7 |

50.3 |

|

Fri 24 Apr |

07:00 |

UK |

Retail Sales Inc Auto Fuel MoM |

Mar |

-0.3 |

0.3 |

-0.4 |

|

Fri 24 Apr |

09:00 |

GE |

IFO Business Climate |

Apr |

85.7 |

85.4 |

86.4 |

Note: All times are GMT+1 (London). Source: Bloomberg, MUFG GMR