Talks to resume leaving US dollar vulnerable to further slide

USD: Peace hopes keeps US dollar under selling pressure

President Trump continues to manage financial market expectations with enough hope to ensure favourable market conditions. The latest efforts from Trump came in an interview with the New York Post reporting that Trump stated that talks would resume “over the next two days”. In a Fox Business interview he stated that the war was “close to over”. He also spoke of “an amazing two days ahead” so there are now high expectations in the markets that something positive will develop to justify what looks to us like incredibly optimistic pricing in the financial markets. But with the US equity markets now trading higher than the pre-conflict levels, the US dollar has understandably come under renewed US dollar selling.

This week now looks like the period when investors begin throwing in the towel on the long dollar trade that was the most obvious initial strategy after the war began. IMM positioning data indicated broad-based US dollar buying in the period following the conflict. The US dollar index non-commercial futures position has turned from net short to net long with the long dollar position in the latest data the largest since before the Liberation Day tariff announcements at the beginning of April last year. The failure of the US dollar to advance as much as we expected since the start of the conflict and the emerging signs of increased appetite for selling is an indication of the poor fundamental backdrop for the dollar ahead of the start of the conflict.

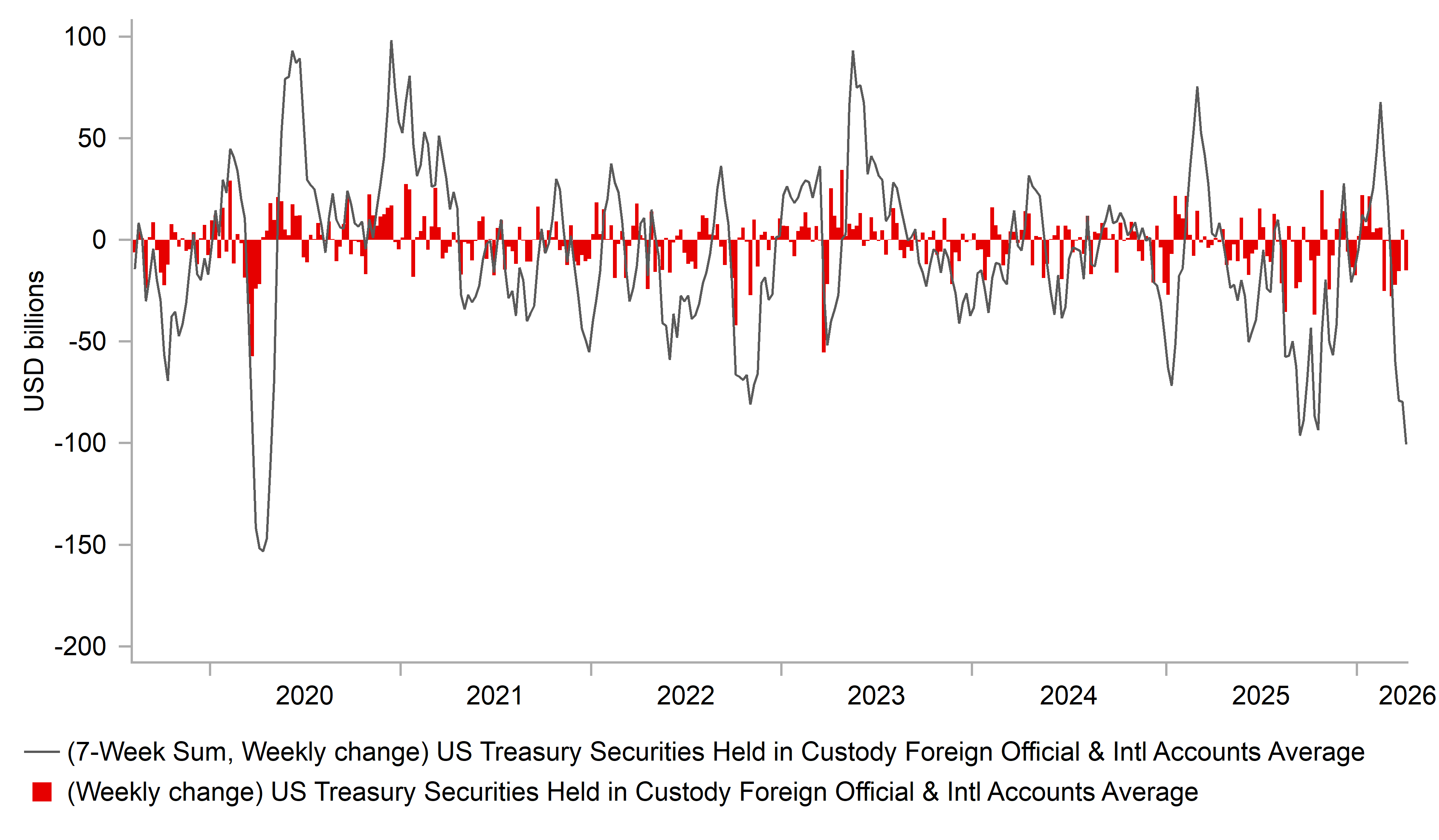

The recycling of US dollars back into the US is likely about to get severely disrupted. Middle East energy sales receipts are down sharply and hence buying of US Treasuries will likely slow notably with Middle East entities potentially set to turn sellers. The Fed custody holdings of USTs held by foreign accounts have fallen sharply. In a seven-week period holdings are down USD 101bn, the largest total since covid, which was then the largest since 2014. The US curve is yet to steepen. If the conflict drags on without a resolution soon then inflation and fiscal risks will likely start to steepen the curve – a scenario that usually coincides with a weaker dollar.

Tonight, the US Treasury will release the cross-border flow data (TIC) for the month of February and the more recent data has shown some easing demand for US Treasuries with private foreign investors selling in three of the last four months. Indeed foreign investor buying of USTs on a 6mth sum basis was the weakest in January since October 2021. Confidence in US assets continues to be tested and demand for US Treasuries was weakening even before the conflict began and a conflict that drags on will only further reinforce those increasing doubts.

FED CUSTODY HOLDINGS OF FOREIGN US TREASURIES FALLING SHARPLY

Source: Bloomberg, Macrobond & MUFG GMR

EUR: Back to pre-conflict level as Lagarde expresses surprise

If on 27th February we had been told what was about to unfold in relation to the conflict in the Middle East, the rise in energy prices and the broad-based nature of the conflict including so many countries in the region and the scale of damage to energy production and storage facilities we would not have said then that over six weeks later EUR/USD would be close to unchanged. But that’s where we are with the closing rate on 27th February 1.1812.

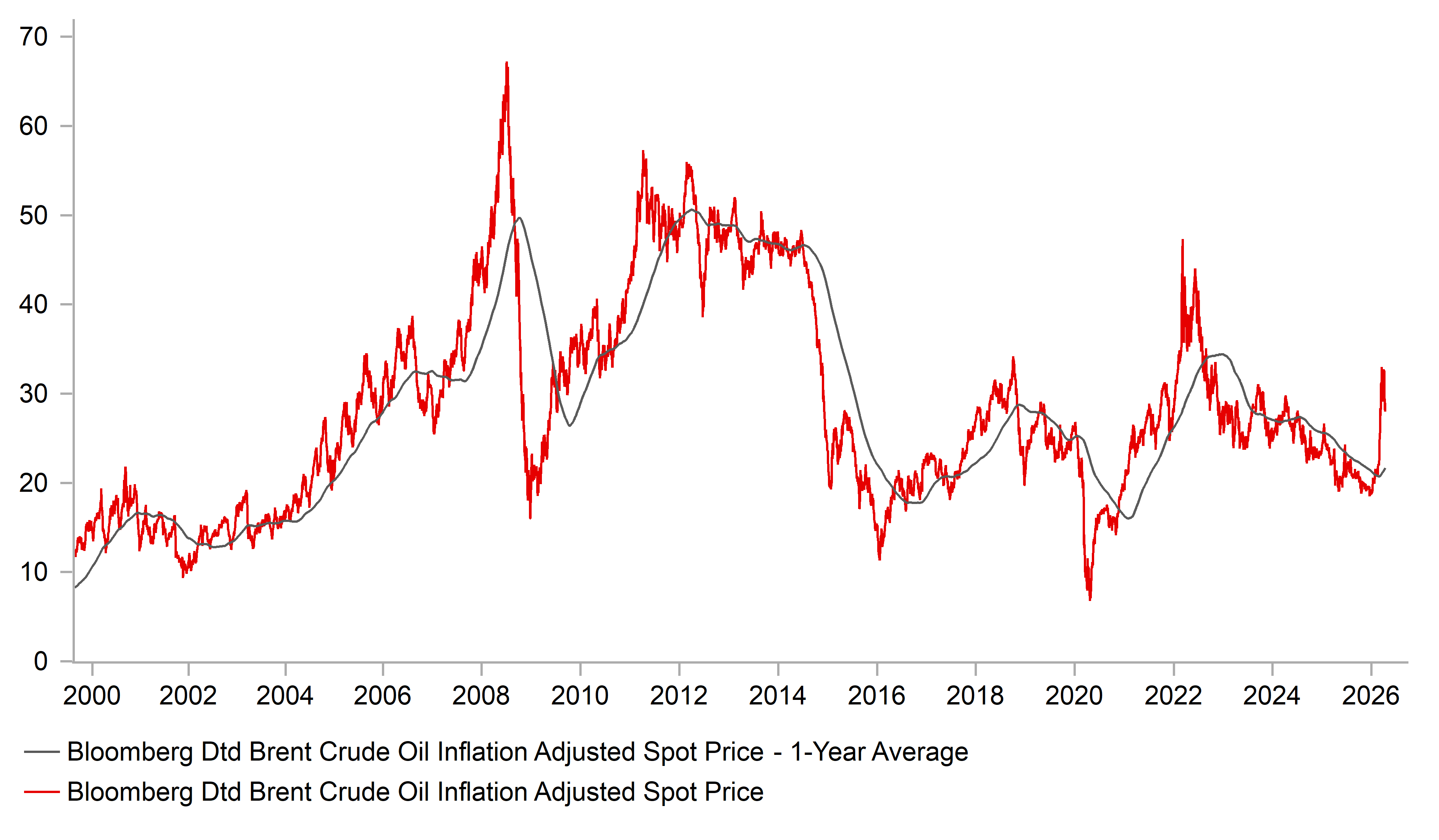

There are a number of factors that likely explain that, which we have mentioned over recent weeks. Relative FX stability is certainly a function of the stability in equities. The S&P 500 yesterday closed 1.3% above the close on 27th February! Crude oil prices just haven’t yet risen enough to raise fears over global recession that would have led to risk asset selling. In real terms, Brent crude oil is currently around 30% below the 1-year average peak in 2022. ECB President Lagarde yesterday described financial markets conditions as “a little strange” suggesting an overly optimistic take from global investors to what is the largest ever supply disruption according to the IEA.

President Lagarde yesterday certainly didn’t sound like a central banker who had an objective to steer financial market pricing in a different direction. Pricing for an April hike has been drifting lower and yesterday would have been the ideal occasion to steer market pricing ahead of a black-out period that is approaching (starting next Thursday) ahead of the meeting the following Thursday. So a hike this month does now look less likely but we’d still expect a move by June under circumstances of crude oil prices remaining around current levels or higher and equity markets remaining resilient.

President Lagarde yesterday stated that the ECB “doesn’t have a tightening bias” which is not particularly surprising. A shift in bias is something that would be done at meeting press conferences – so that’s a possibility for the April meeting. The ECB must also be “completely agile” which argues that we also should completely rule out a rate hike in April. There are survey data releases over the coming two weeks that could raise inflation concerns.

But we would argue that the ECB governing council currently find themselves with additional time scope due to the resilience of the euro that they may not have expected at the start of this conflict. EUR/USD was over 4% lower seven weeks following the Russia invasion of Ukraine and hence this time is certainly different. Lagarde hinted at that yesterday stating that Europe was not at the epicentre of the Middle East conflict. The current situation was described by Lagarde as between the ECB’s baseline and adverse scenarios (severe is the third scenario) and again in that sense the ECB will probably argue it has time before taking action. Just over two 25bp rate hikes remains priced for this year which we would certainly concur with at this juncture. Still, the strength of the euro is in part a reflection of the market’s sense of indifference to Middle East risks that makes us wary over the near-term outlook.

BRENT CRUDE OIL ADJUSTED FOR INFLATION REMAINS CONSIDERABLY BELOW PREVIOUS HIGHS

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EU |

10:00 |

Industrial Production (MoM) |

(Feb) |

0.3% |

-1.5% |

!! |

|

EU |

10:00 |

Industrial Production (YoY) |

(Feb) |

-1.4% |

-1.2% |

! |

|

US |

12:00 |

MBA Mortgage Applications (WoW) |

- |

- |

-0.8% |

! |

|

CA |

13:30 |

Wholesale Sales (MoM) |

(Feb) |

2.3% |

-1.0% |

!! |

|

US |

13:30 |

NY Empire State Manufacturing Index |

(Apr) |

0.60 |

-0.20 |

!! |

|

US |

13:30 |

Import Price Index (MoM) |

(Mar) |

2.1% |

1.3% |

!! |

|

US |

13:30 |

Export Price Index (MoM) |

(Mar) |

- |

1.5% |

!! |

|

CA |

13:30 |

Manufacturing Sales (MoM) |

(Feb) |

3.8% |

-3.0% |

! |

|

US |

15:00 |

NAHB Housing Market Index |

(Apr) |

37 |

38 |

! |

|

US |

15:30 |

Fed's Hammack speaks on CNBC |

!!! |

|||

|

GB |

16:50 |

BoE Gov Bailey Speaks |

- |

- |

- |

!!! |

|

CH |

18:00 |

SNB President Schlegel Speaks |

- |

- |

- |

! |

|

US |

18:45 |

Fed's Bowman Speaks |

- |

- |

- |

!!! |

|

GB |

19:00 |

BoE Gov Bailey Speaks |

- |

- |

- |

!!! |

|

US |

19:00 |

Beige Book |

- |

- |

- |

!! |

|

EU |

20:30 |

ECB President Lagarde Speaks |

- |

- |

- |

!!! |

|

EU |

21:00 |

ECB's Schnabel Speaks |

- |

- |

- |

!! |

Source: Bloomberg & Investing.com