The ECB is set to leave policy unchanged at next week’s meeting after dialling back the sense of urgency around the need for immediate tightening. Officials clearly judge that there is time to look for stronger evidence that the energy price shock could trigger second-round inflation pressures before adjusting rates. We expect the messaging to be relatively balanced for now, but the ECB will likely leave the door open to a hike at the June meeting. Our view is that it will become increasingly hard to ignore data showing rising inflation expectations over coming months. We continue to expect that the ECB will implement 50bp of rate hikes this year, with the first move in June.

ECB Preview – No hurry to act, for now

ECB officials have dialled back the sense of urgency – but ‘wait and see’ will become less tenable

There has been a discernible shift in tone around the need for tightening from the ECB in recent weeks. Numerous officials have dialled back the sense of urgency in recent public appearances, with even hawkish officials such as Isabel Schnabel cautioning against rushing into a move. We do not expect any policy change at next week’s meeting. The ECB struck the right tone at its March meeting to our minds (see here: ECB Review: Cool heads, for now), and will probably look for similar messaging again. The core guidance (i.e. a ‘meeting by meeting’ and ‘data-dependent’ approach) is likely to remain unchanged, but more talk along the lines of ‘vigilance’ and ‘agility’ in the press conference would leave the door wide open to a hike at the June meeting.

For now, the ECB clearly believes that it can afford to wait for more data to justify tightening. European natural gas pricing has decreased markedly since the ECB’s March meeting. Gas prices are now close to, or even slightly below, the ECB’s March baseline, which reduces the pressure to act immediately. Various national fiscal support measures, e.g. the agreement of a temporary two-month cut to fuel duty in Germany, have also bought some time to assess second-round risks.

But headline euro area HICP has already risen to 2.6% Y/Y in March and there is plenty of inflation in the pipeline. Data next week will likely show headline inflation rising to ~3% in April. Further waves of price pressures are likely to follow the immediate surge in fuel prices as the energy shock propagates through the economy, regardless of whether a peace settlement can be reached in the Middle East. There will be lagged effects on household energy bills, while jet fuel and other specific shortages (e.g. chemicals, plastics, helium) are set to increasingly show up in inflation figures over coming months. Diesel costs will likely push up core goods prices more generally, and higher fertiliser costs will gradually feed through to food prices too.

We think the ECB will find it increasingly hard to look past all this. Many of the specific price pressures mentioned above (e.g. food, energy, travel) tend to be especially salient for household inflation expectations. The next batch of ECB household survey data, released next week, will likely show there has already been an uptick in expectations in March.

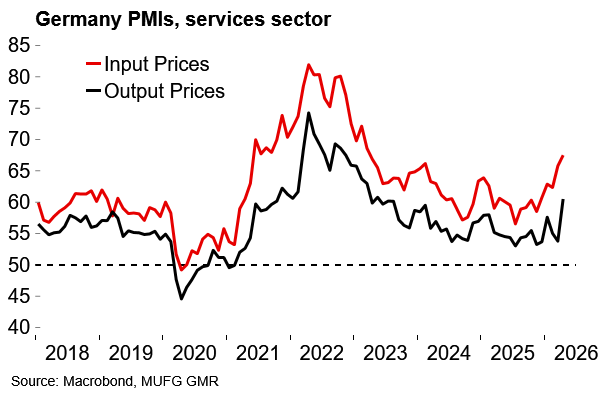

Today’s PMI data also showed a significant uptick in services sector selling price expectations, driven by Germany, which will raise hawkish concerns around second-round risks. The overall activity numbers in the PMI were on the weak side, despite a temporary front-loading boost to manufacturing as firms look to get ahead of supply-chain issues. Next week’s flash GDP report for Q1 might also disappoint. But as we’ve argued before (e.g. here: Central banks grapple with the return of stagflation risks) we think that, relative to 2022, the ECB will be more focused on inflation risks than recession risks.

All told, we expect ‘wait and see’ will become less tenable as evidence of rising inflation expectations continues to mount. It will be some time until there’s definitive evidence on second-round pass-through (i.e. higher inflation actually passing through to wage growth indicators). At some point the ECB will have to make a judgement call. Our view remains that policymakers will see greater risks of a policy error in being slow to react relative to the risks of early tightening and then calibrating lower if second-round pressures do not materialise.

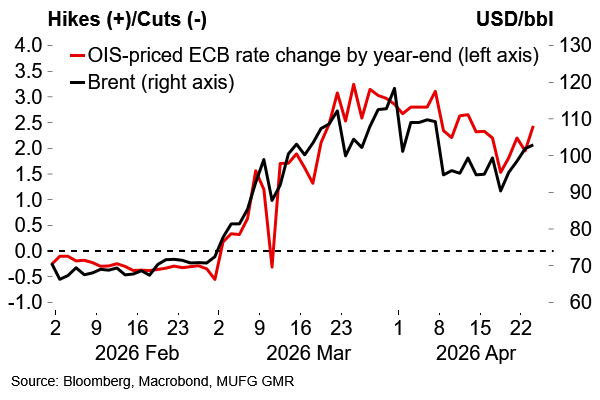

Oil prices remain elevated and two hikes are fully priced

Price pressures in the services sector will be a key focus

Outlook - we continue to expect 50bp of tightening this year

The ECB’s initial rhetoric around the inflation risks from the Iran conflict led us to expect that policymakers would take a proactive stance around containing inflationary pressures and we pencilled in back-to-back rate hikes starting in April (see here). April is no longer on the cards, but we continue to expect 50bp of tightening this year.

We have pushed the first move back to June, by when we expect it will be hard for the ECB to ignore evidence of rising inflation expectations. Despite the lack of urgency in recent communication, we see a logic in policymakers immediately following a June hike with another move in July. If the ECB feels that the threshold for tightening has been reached, then we suspect the rhetoric from officials will flip back to show a willingness to be proactive. A delay to September is certainly plausible but it would be a long gap and we expect policymakers will want to A) send a clear message about the intention to contain second-round inflation risks and B) bring policy more unambiguously into restrictive territory.