UK inflation surprised on the downside again in May, reinforcing the recent run of softer data. Core goods disinflation points to weak pricing power and the uptick in services inflation disappears when focused on underlying components. These numbers follow softer labour market numbers and limited signs of second-round risks in recent survey data.

The release further eases pressure on the BoE to act after the US-Iran deal has pushed energy pricing below even the mildest scenario set out at the last meeting in April. We expect a 7-2 vote tomorrow to leave rates unchanged. Policymakers will continue to lean on tighter financial conditions and maintain the “active hold” stance.

The MPC is not out of the woods. There remains plenty of inflation in the pipeline and officials will remain vigilant for any signs of broadening pressures beyond energy effects. But the recent run of soft data means the hawks seem to have lost the argument for ECB-style pre-emptive tightening and hence it is becoming increasingly likely that the BoE will ride out the shock without raising rates at all. We will reassess our previous call for 50bp of tightening this year after tomorrow’s meeting.

Ultimately we continue to believe that second-round effects will remain contained in the context of a soft UK labour market. But it will be some time before there is definitive evidence on broader pass-through and policymakers will be aware they are risking more forceful action later by sitting on their hands now.

Another soft CPI number adds to the string of dovish UK data

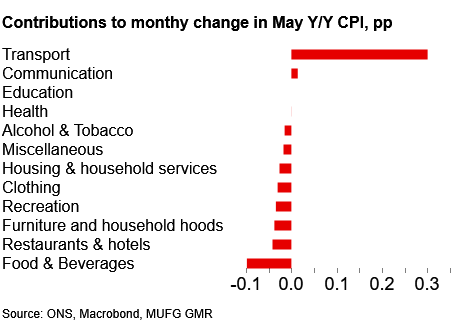

UK inflation surprised to the downside again in May with an unchanged headline rate of 2.8% (consensus/BoE: 3.0%). This miss was driven by softness in food inflation (2.2%, from 3.0% in April) and core goods (0.7%, from 1.1%), with the latter suggesting firms had limited pricing power amid weak demand. The headline services number increased from 3.2% to 3.7% but this was due to technical factors (e.g. a base effect from last year’s VED error and some Easter effects on air/sea fares). Once indexed and volatile components are removed, the picture is more stable – we estimate that services inflation was unchanged at around 3.8%.

Following the last BoE meeting (see here: BoE Review: Ready to Act), the UK data flow has been almost uniformly dovish. As well as back-to-back inflation misses to the downside, there have been more signs of a loosening labour market and business sentiment looks decidedly soft. Forward-looking survey evidence, e.g. the Decision Maker Panel, has remained broadly benign. Meanwhile, progress towards re-opening the Strait of Hormuz has seen Brent retrace to below 80 USD.

Aside from transport, almost all sectors weighed on headline inflation in May

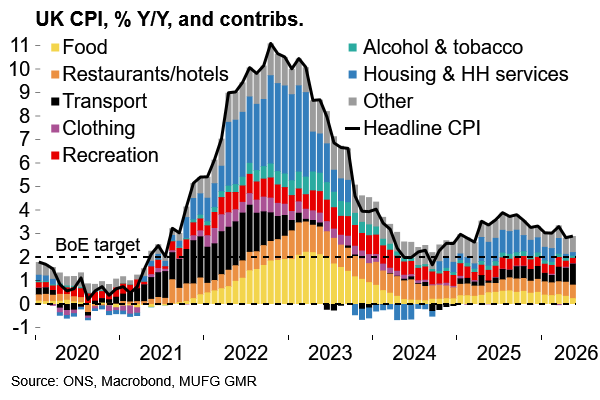

UK inflation has eased since March and remains below the 3% mark

The BoE may have been ready to act, but recent data and developments mean there is clearly no pressing need to do so. After jawboning rate expectations higher following the hawkish hold in March, BoE officials are continuing to lean on the extra breathing space afforded by tighter financial conditions relative to the pre-conflict period. The BoE has characterised its stance as an “active hold” (i.e. not cutting this year as was previously expected). Despite recent dovish developments, we think officials will want to extend this framing at tomorrow’s meeting. We expect the BoE will try to avoid significant market repricing away from current expectations for one full hike this year. As such, the tightening bias will likely be maintained (but it could be a communication challenge to ensure it seems credible).

In terms of the vote, we expect a 7-2 split with Greene still likely to join Pill in dissenting for a hike. She said in a recent speech that she considered voting for a hike in April, adding that the BoE “cannot rely on the tightening of the curve to do our work for us” and that “the risk of acting, even if inflation proves to be less persistent, is less severe than the risk of failing to act”. Her dissent is certainly not a slam dunk after today’s numbers and recent news – Greene also noted that voting for an April hike might have been “a mistake if the conflict ended immediately”. Even arch-hawk Pill could strike a softer tone in his commentary with the hawkish argument for early action certainly weakened by the data flow.

Reassessing our BoE call – the bar for hikes looks increasingly high

Our call during the conflict period has been for 50bp of front-loaded tightening this year. We will reassess that call after the communication and vote split this week.

Despite recent dovish developments, we stress that the MPC is not out of the woods. Recent geopolitical developments do not mean an instant end to inflationary pressures. The upcoming increase in the household energy price cap will add ~0.3pp to the July rate. Today’s data showed that factory gate inflation remained at 4.0% Y/Y and the indirect effects of the energy shock will continue to percolate into prices. We expect that the headline inflation rate will peak close to 4% towards year-end.

More fundamentally, headline UK CPI has averaged 3% over the last two years and policymakers will continue to fret about structural changes in wage and price-setting behaviour after another external price shock. The latest BoE/Ipsos inflation attitudes survey showed rising household expectations in Q2.

For the BoE, it may be that doing nothing is still enough. Policy is just about in restrictive territory. The UK labour market seems to have weakened further, with recent redundancy notification data looking rather ugly (see below). We suspect political uncertainty will be another headwind for hiring (and economic activity more broadly) over coming months. The Brent futures curve is now very close to the assumptions used for the BoE’s mildest scenario laid out in April. That scenario sees headline inflation falling below target in Q4 2027 and averaging 1.7% in 2028.

In short, second-round risks are likely to be contained here and we suspect that it will be hard to make a compelling case for hikes at upcoming meetings as the window for credibly pre-emptive action closes.

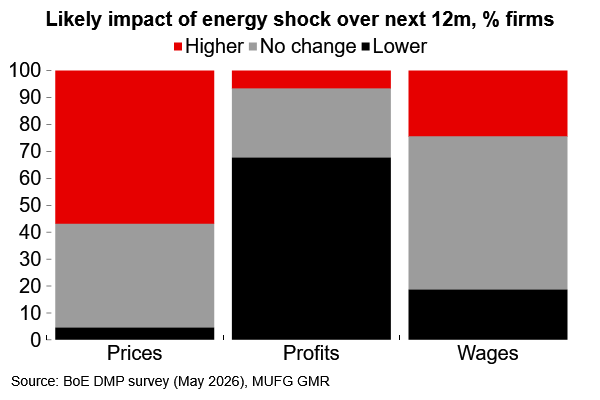

The latest DMP survey did not ring alarm bells on second-round risks

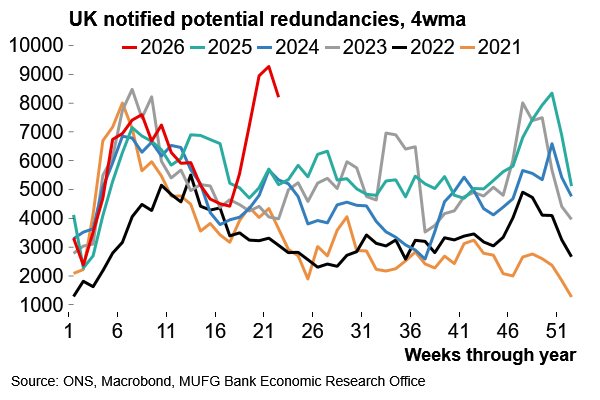

Redundancy notifications have started to look more concerning

But by sitting on its hands, the MPC will leave itself hostage to fortune. This is how Bailey put it last month: “Because interest rate changes take time to take their effect, monetary policy cannot wait for conclusive evidence of the strength of second-round effects”. It was precisely on that basis that we thought the BoE would essentially react with a degree (i.e. 50bp) of measured, front-loaded tightening – as the ECB has done (see here: ECB Review: The Hiking Begins).

Unlike the ECB, the BoE may have come into this with rates in restrictive territory, but an “active hold” is a technical thing and does not send nearly the same message to firms and households about the intention to keep a lid on inflation risks. An early hike might have been reasonably labelled as an insurance move which could be unpicked later if second-round effects do not materialise.

The bar for a July hike (current pricing: ~5bp) is obviously high after recent data, but not completely insurmountable if there is a hawkish surprise in the vote split/communication this week. There is scope for survey evidence on second-round risks to worsen over coming weeks. BoE policymakers may also see credibility risks if they do not react to rising inflationary pressures after initially signalling a willingness to do so. It is plausible too that geopolitical risks could re-emerge – US VP Vance described the deal as “very general”, with the details left to be worked out later. But right now it does seem as though the hawks have lost the case for urgency.