ECB Review: The hiking begins

Macro view: The ECB hiked rates by 25bp, as expected, in a unanimous decision. The normal guidance which leaves plenty of flexibility was retained. Lagarde’s commentary was slightly more hawkish and less cautious than we anticipated, with various comments around the broadening of inflation risks. We continue to think that a July hike is more likely than not now that the ECB has acknowledged that the threshold for tightening has been reached. But ultimately we see this as the start of a ‘measured adjustment’ of policy to lean against rising inflation risks rather than the beginning of a fully-fledged tightening cycle. As things stand, we maintain our call for 50bp of hikes in total this year on the assumption that the growth outlook will remain challenging and second-round risks will remain contained.

Markets view: Market expectations for three ECB hikes this year set a high hurdle for hawkish policy surprise today. Upside risks to inflation from the Middle East conflict would have to intensify to push euro-zone yields much higher in the near-term. The lack of a deal to end the conflict and reopen the Strait alongside the recent hawkish repricing of Fed rate hike expectations leaves risks titled to the downside for EUR/USD. The pair is currently drifting back towards the bottom of the 1.1400-1.1800 trading range that has been in place since the onset of the Middle East conflict.

Macro view: The start of a measured adjustment

A less cautious hike than expected – but we continue to see it being one of just two this year

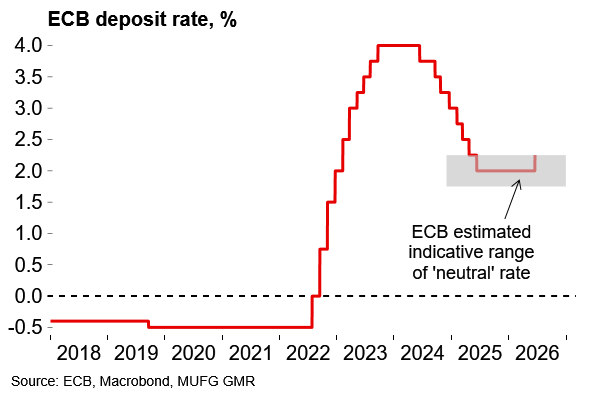

The ECB delivered the expected 25bp hike, lifting the deposit rate to 2.25%, in what was described as a unanimous decision. The core guidance (“meeting-by-meeting”, “data-dependent”, no pre-commitment) was left unchanged in the statement, with policymakers keen to retain plenty of flexibility.

Today’s move was fully priced but came in somewhat more hawkish packaging than we anticipated. Lagarde stressed that the decision was “robust” across a range of scenarios with the implication being that a hike would have been justified even if the inflation outlook was somewhat more benign. The ECB president said that the energy shock is “enduring longer than expected” and that officials are “beginning to see broadening throughout the economy”. Lagarde also highlighted the relative resilience of the economy by stressing that it is not an “environment where growth is absent or under significant threat”. There was no pushback in the statement or the Q&A against market expectations coming into the meeting for around three hikes this year.

In our preview (see ECB Preview – Securing the anchor) we suggested that officials might frame the hike as a pre-emptive insurance move which could be unpicked later if second-round risks do not materialise. Lagarde directly rejected this idea and instead stated that it was a “sensible monetary policy decision”. In that sense it was a less cautious decision than anticipated.

Unsurprisingly, there was no explicit guidance in terms of the timing of the next move, with Lagarde stressing heightened uncertainty. Almost simultaneous headlines stating that Trump intends the US to strike Iran again and ultimately take Kharg Island “at some point” rather underlined the point.

There were conflicting ‘ECB sources’ stories after the meeting with some suggesting that a July hike is less likely if energy pricing remains at current levels and other reports that a follow-up move is possible. At the time of writing, markets are pricing in a ~15bp chance of a back-to-back move, up from ~10bp ahead of the announcement. The way we see it is that the ECB has set out its stall now and has made it clear that it intends to lean against rising inflation risks. We think a July hike is more likely than not. Now the threshold for the first hike has been reached, the tone of the debate could well change over coming months.

But, while there was a hawkish slant to some of today’s communication, our assumption remains that this is the start of a measured adjustment rather than a fully-fledged tightening cycle. We believe the growth outlook will be challenging and second-round risks will ultimately remain contained. On that basis, we stick with our call for 50bp of hikes this year with the next most likely in July. Lagarde may have dismissed the idea of the ECB being “pre-emptive”, but we continue to see today’s hike as the ECB moving early to lean against risks. That said, in light of the framing today, we would consider adding another hike to the call if progress towards opening the Strait of Hormuz remains limited over coming weeks or if the June inflation data shows further signs of building momentum in services inflation.

The first hike since 2023 sees the ECB moving away from the ‘good place’

Price pressures set to broaden beyond direct energy effects

Core inflation expectations revised higher – but the growth outlook is set to darken

The new projections (based on market pricing for approaching three rate hikes this year) showed a bit less growth and a bit more inflation in the baseline, as expected. Both headline and core were revised up by 0.3pp in 2027, which reflects the longer duration of the conflict than initially expected. While headline was seen at target in 2028, it is significant that core inflation is expected to overshoot at 2.2% even under the assumption of further tightening to come.

But it’s also worth noting that the cut-off date for the market assumptions was 21 May, which would have boosted the inflation numbers. Since then, shorter-dated oil contracts have retraced following increased optimism around the potential for a US-Iran deal. The projections were also produced ahead of the downward revision to the euro area Q1 GDP estimate on the back of the sharp contraction in Irish GDP. Even if we set that aside, expectations for 0.8% growth in 2026 look optimistic to our minds (see here). We’re not so sure about the argument for resilient consumer dynamics as the ECB. We think the jobs market could start to look a bit softer over coming months with firms less inclined to hoard labour and ride out the shock. As things stand, we would expect a downward revision to growth in the ECB’s September projections and, provided a peace settlement is reached, more benign inflation numbers. This adds to our sense that the bar for hiking could seem higher after the summer.

Of course, we are all still working on the basis of scenarios rather than baseline projections while uncertainty is high. The ECB also refreshed its previous scenarios presented in March. These were produced in a hurry and a fuller reassessment was possible, but the broad profiles and peaks remain similar to the first batch with a rising degree of inflation persistence when moving across the shocks. In addition to the tweaked adverse and severe scenarios, a new ‘milder’ scenario has also been introduced – but even in this scenario, core inflation is expected to exceed target in 2028.

Markets view: Rates already well priced for measured tightening

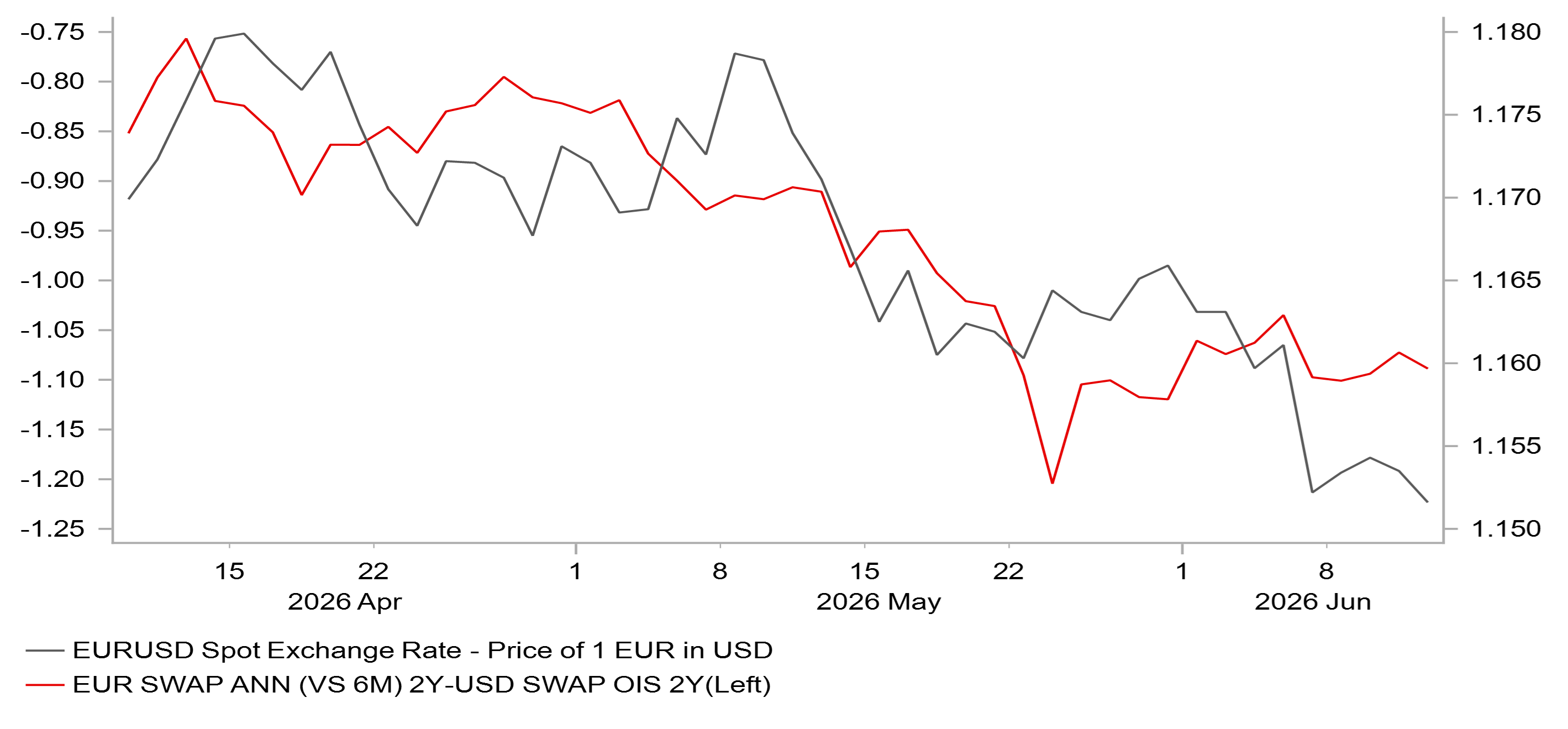

EUR/USD drifting lower in absence of Middle East deal & recent hawkish repricing of Fed rate hike expectations

The initial financial market reaction to today’s ECB policy update has been relatively muted. Short-term eurozone yields and EUR/USD are trading slightly lower than the levels recorded prior to today’s policy meeting. This subdued response reflects the fact that President Lagarde’s comments were broadly in line with market expectations for the ECB to deliver measured policy tightening.

Prior to today’s meeting, the eurozone rate market was already almost fully pricing in three 25bps hikes for this year, which set a high bar for a hawkish policy surprise. We have been pencilling in two hikes from the ECB but acknowledge the risk that even tighter policy may be required. Market expectations for multiple rate hikes were reinforced by President Lagarde’s observation of a “broadening of inflation” across the economy. The decision to raise rates today was also described as “robust across all three scenarios,” including a milder scenario, leaving the door open to further hikes.

The scale of required monetary tightening will depend heavily on how the Middle East conflict evolves. Renewed military tensions between the US and Iran this week have dampened optimism about a near-term deal to end the conflict and reopen the Strait of Hormuz, adding to upside risks for eurozone rates. The longer the Strait remains closed, the greater the risk that energy prices stay elevated, reinforcing stagflationary pressures in the eurozone economy. The ECB has signalled clearly that a more forceful response may eventually be required under a severe scenario, although this is not yet the base case. A larger negative terms-of-trade shock for European economies would also weigh more heavily on the EUR, even if the ECB is forced to hike rates further.

At the same time, the ECB refrained from providing specific guidance on the likely timing of the next rate move. The updated guidance reiterated that policy decisions will be made on a meeting-by-meeting basis, with no pre-commitment to a particular path. We continue to hold the view that a back-to-back rate hike could be delivered as soon as next month. However, the absence of clear guidance today suggests the ECB may prefer to wait slightly longer until September before tightening further.

Taking everything into account, we expect EUR/USD to continue trading on a softer footing in the near term, with the pair moving back towards the lower end of the 1.1400–1.1800 trading range that has been in place since the onset of the Middle East conflict in late February.

YIELD SPREADS HAVE BEEN MOVING AGAINST THE EURO RECENTLY

Source: Bloomberg, Macrobond & MUFG GMR