The ECB is set to deliver a 25bp hike this week. It will likely be framed as a pre-emptive ‘insurance’ move, i.e. front-loaded but reversible if inflation risks subside. Policymakers want to lean against second-round risks ahead of time but will also want to retain optionality. Credibility is also a concern – with the ECB’s inflation projections set to be revised higher there is a desire to showcase a reaction function that ‘actually reacts’.

With the hike entirely priced, the market focus will be on any signals around the timing or extent of any further tightening. We expect the ECB will leave the door open to more action but want to retain plenty of flexibility amid elevated uncertainty.

Our base case remains that there will be 50bp of tightening in total this year – i.e. a ‘measured adjustment’ rather than a fully-fledged tightening cycle. Second-round risks will likely remain contained amid a muted growth backdrop, and our view is also predicated on the assumption that the Strait of Hormuz will reopen over the summer.

In terms of timing, we believe July remains in play for the next hike. With the threshold for action now apparently met, we could see a shift in rhetoric. The same arguments for a hike this week might well prevail in July – why wait?

The ECB is set to kick off its ‘measured adjustment’ of policy

Officials want to get ahead of the curve

The ECB is fully expected to raise rates at this week’s policy meeting. Officials have laid plenty of groundwork for a move as we set out here, with influential hawk Isabel Schnabel explicitly stating that a “June hike will be needed” and that “looking through is no longer an option”. A 25bp hike is now entirely priced in. The absence of a peace settlement in the Middle East combined with the upside surprise in May core inflation (2.5% vs MUFG/consensus at 2.4%) has extinguished any lingering doubts about whether the ECB could lose its nerve this week. The latest services inflation print at 3.5%, a 50bp increase, looked especially problematic for a central bank concerned about second-round inflation risks.

Officials will hope that a ‘measured adjustment’ in policy at this relatively early stage will keep a lid on inflation expectations. The ECB is set to be the first major central bank to raise rates since the start of the US-Iran conflict and we receive plenty of questions around the risk of a policy error in response to an external price shock. So why are they hiking now? These are the most pertinent considerations, we think, for policymakers:

1) The 2022 inflation surge is still fresh in memories, which raises the risk of structural changes in wage and price-setting behaviour. While the macro backdrop is undoubtedly different today, that recent experience makes it harder to look through the current shock. Waiting until there is definitive evidence on the pass-through to underlying inflation would be too late and might require more forceful adjustment down the line. Officials clearly want to get ahead of the curve, in line with our initial post-conflict view. Looking back, the minutes of the April meeting suggest it was a “close call” for a number of voters, and so more live than assumed at the time.

2) Credibility matters. Lagarde has previously talked about the importance of showing a reaction function that actually reacts. Having jawboned rate expectations higher by signalling the possibility of rate hikes, the ECB feels compelled to actually follow through with action. Lagarde recently said that it is when “monetary policy decisions are politically fraught and economically costly that credibility is most needed”.

3) The ECB faced criticism for being slow to react to the 2022 price shock relative to other central banks. Its first hike was four months after the Fed and seven months after the BoE. While this point is less key, we suspect officials would be happy to demonstrate greater nimbleness this time around.

An insurance hike – with wriggle room to reverse

That all said, officials will be acutely aware of the risks of having to backtrack if energy prices retrace and wage growth remains in check. There are no easy options when an energy shock raises stagflation risks. The upcoming tightening will likely be framed as a pre-emptive and precautionary ‘insurance’ move. While leaving the door open for further action, the ECB is likely to leave itself space to credibly unpick rate hikes if the threat of second-round inflation risks starts to fade.

For now the market focus will be on the timing and extent of any subsequent tightening. Policymakers will want to retain plenty of flexibility and we doubt Lagarde will offer any firm guidance at the press conference. A second hike is not fully priced until September, but we maintain that there is scope for a back-to-back move in July. Once policymakers acknowledge the threshold for action has been reached this week, the tone of the debate will change. The likelihood of the same arguments prevailing next time out would increase if the ECB does characterise this week’s move as pre-emptive and reversible, thereby reducing policy error jitters. Two hikes would send a clearer signal and ‘why wait?’ becomes a valid question. Further signs of stickiness in the June core inflation figures would also add to the case, although we do suspect that some of the factors that lifted the rate in May were temporary.

Further ahead, our base case is that the upcoming hike is one of two and does not mark the start of a fully-fledged tightening cycle. We see 50bp of front-loaded ECB hikes in total this year (as we have done since March). On paper, the scope for second-round effects appears limited: the labour market is softening and growth momentum is weak. Even excluding the distortion from the 12% contraction in Ireland, Q1 GDP was relatively muted at ~0.25% Q/Q, and survey data is decidedly soft. We also work on the assumption that a US-Iran deal will allow the Strait of Hormuz to reopen this summer, prompting more distant oil price contracts to retrace towards pre-conflict baselines. All else equal, the bar for tightening should look higher by the autumn and the ECB will likely be content that it has sufficiently leant against second-round risks with its early action.

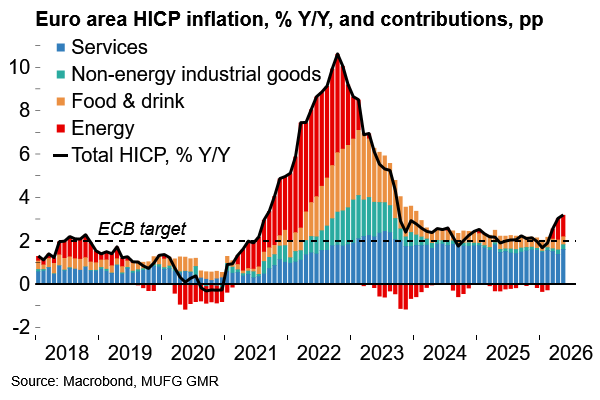

Swift energy pass-through has lifted headline inflation

The ECB is set to revise its HICP projections higher

Projections to show higher inflation and lower growth

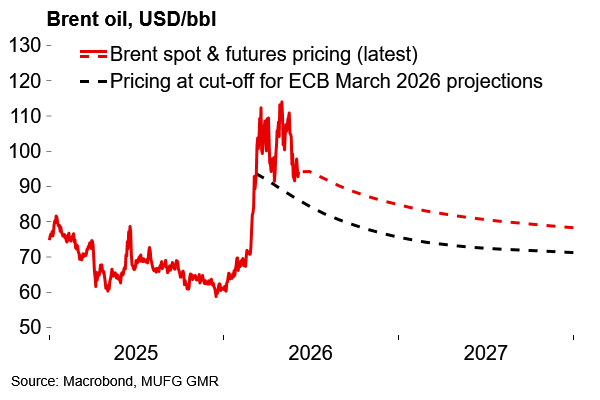

The other focus of the meeting will be on the ECB’s updated projections, which are likely to show higher inflation and lower growth relative to March. This reflects both incoming data and Brent oil futures which are around 10% above the previous assumptions. The market snapshot cut-off date introduces some uncertainty following the decline in energy prices through the latter half of May. Government policy measures (such as temporary fuel tax relief in Germany) will also offset some of the impact. However, higher wholesale energy price assumptions will ultimately leak into the core inflation projection (which will also reflect the higher spot numbers mentioned above) and support the case for tightening.

The ECB will also revisit the scenarios used in March. As Lagarde stressed at the time, these figures were prepared under considerable time pressure and so it’s possible that there will have been some re-assessment of the risks.