A pivotal UK by-election on the horizon amid still-elevated geopolitical uncertainty: The situation for UK PM Starmer quickly deteriorated this week amid fall-out from last week’s local elections. Labour party favourite and key leadership rival Andy Burnham has engineered a possible route back to Westminster – but he needs to win a pivotal by-election to clear a path, which is not a given. The stakes are high. If Burnham wins, he could be UK PM by the summer. Markets are wary of the risks around greater issuance and higher inflation under alternative Labour leadership at a time when the seemingly intractable situation in Hormuz is driving yields higher globally.

What we’re watching next week: A range of survey data will provide further evidence on the resilience of the euro area economy and clues around the extent of any inflation pass-through from higher energy prices. In the UK, we expect a temporary downshift in headline inflation and further signs of slack in the labour market.

Macro Focus: A high stakes UK by-election on the horizon

UK political risk remains squarely in focus with a pivotal election key to the outlook

Our initial take on the local election results was that, while bad, they were no worse than expected and that PM Starmer might have been able to stumble on. But a week is a long time in politics. After dozens of backbench MPs called on Starmer to step down, Wes Streeting, a leadership rival, resigned from the cabinet. That was swiftly followed by the announcement that the MP for Makerfield in the North-West of England was standing aside to allow Andy Burnham, currently the Mayor of Manchester and a popular figure within the Labour Party, a route back to Westminster.

The stakes couldn’t be much higher. A Burnham win in the upcoming by-election (we assume he will be permitted to stand) would likely clear a path for him to become PM and shift the policy conversation to the left. A loss would further weaken the governing Labour Party and add uncertainty to the leadership equation – while also boosting the credibility of Nigel Farage’s populist-right Reform party.

In terms of timing, by-elections are typically organised 6-10 weeks after the vacancy. Given the obvious risks of uncertainty and policy drift, we anticipate some desire from Labour’s NEC to hold it sooner rather than later and expect it to be held before Parliament starts the summer recess on 16 July.

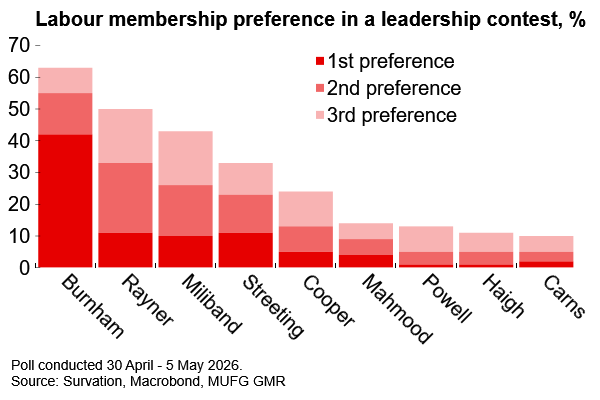

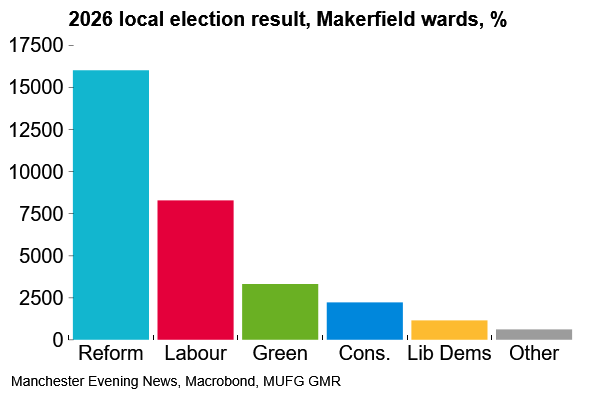

Burnham starts as the favourite – prediction markets currently imply a ~60% chance – but last week’s local election results show the scale of the challenge. Nigel Farage’s Reform party won ~50% of the vote within the constituency last week, with Labour a distant second at ~25%. A by-election is a different proposition to local elections. Burnham will hope that his strong personal brand in the region – and perhaps the opportunity for voters to register their dissatisfaction with Starmer – will support his chances. Polling after the Gorton and Denton by-election, in which Burnham was blocked from standing, indicated that he would have won the seat if allowed to stand.

It’s unlikely to be a walk in the park, but Burnham’s authority would clearly be bolstered if he does win. He would be able to say that he is the candidate that can unite the party and take on Reform at the next general election. Starmer might then see the writing on the wall and stand aside in a leadership contest, so a coronation as soon as July, before the recess, is possible. If alternative candidates stand too (e.g. Streeting, if he can secure the necessary backing) then the process would take longer, but the aim would be for a new leader to be in place by the party conference season in September.

Burnham is the clear favourite among Labour members…

…but he is no shoo-in for the by-election

Markets remain wary of leftward policy shifts at a time of elevated inflation risks

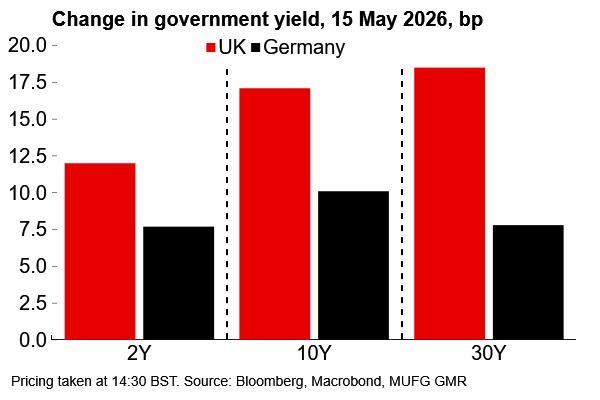

Burnham is seen as being on the left side of Starmer within the Labour Party. He has suggested that space could be carved out from the fiscal rules for borrowing to fund areas such as defence and social housing. From a market perspective, the verdict on this prospect seems clear with sterling weaker and gilts slumping this morning. At the time of writing the 10Y is up 18bp with investors wary of the scope for greater issuance and higher inflation at a time when energy risks remain elevated. Burnham’s comment that the UK should not be “in hock” to bond markets remains a strong reference for investors and points to a contrast with the deliberately market-sensitive approach from Starmer and Reeves.

Still, we continue to assume that any new leadership would heed lessons from the Liz Truss episode. Burnham is a pragmatic operator and we’d expect some messaging aimed at soothing investors’ nerves if he does get closer to Number 10. But there is a risk that market tolerance for more borrowing is misjudged and Burnham (or indeed any new PM/chancellor) would have to quickly backtrack from expansive spending pledges. The political damage from that would immediately undermine a new PM’s authority and further raise risks of policy drift and uncertainty. As we set out yesterday (see here), the UK’s macro backdrop is set to deteriorate over coming months and that will probably limit any ‘honeymoon period’ for a new PM.

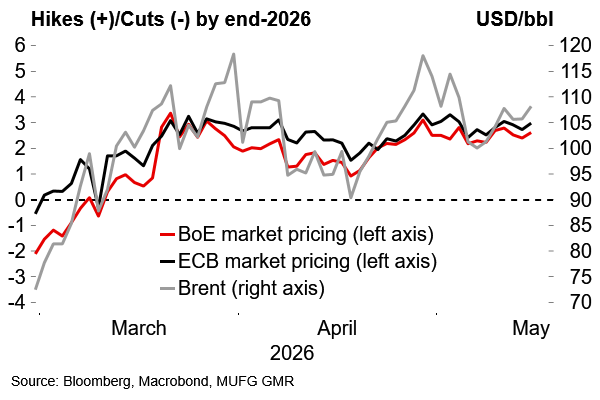

It’s also worth stressing that, for all the focus on UK political risk premiums, the underlying risk of energy-driven inflation remains the main market driver. Government yields are rising across the G7 as oil prices push higher. It is now 15 weeks since the start of the US-Iran conflict and the Strait of Hormuz problem looks no less intractable (see here) and the UK is relatively vulnerable to energy-driven inflation shocks. But in the absence of progress in the Middle East the UK 10Y yield could remain above 5%, and there is plenty of scope for political risk to amplify UK market volatility over coming weeks. Market participants will be watching for by-election polling and any comments from Burnham on policy priorities.

Energy pricing continues to drive rate expectations…

…but UK markets also reflect political developments

What we’re watching next week

How resilience is the euro area economy?

Away from UK politics it’s set to be a busy week on the data front in Europe with various surveys and UK inflation/labour market numbers in focus. The headline euro area flash PMIs for May could start to look uglier if the initial stock-building boost to manufacturing from Middle East disruption has started to reverse. The ECB will be watching closely for signs of rising price pressures, especially if charged in the services sector, as well as indications around the resilience of the labour market and the economy more broadly. The reliable German IFO survey and consumer confidence figures will also be released and we will continue to gauge whether our latest euro area GDP projection (0.7% in 2026) is on the optimistic side given the apparently limited progress towards a resolution between the US and Iran.

In the UK, beyond the continued spotlight on political developments there will also be a range of market-relevant data. Tuesday’s labour market release is likely to show a still-weak employment backdrop but limited progress on pay growth. There will be a lot of moving parts to the April inflation number with base effects and previously-announced government energy support offsetting the continued rise in fuel prices last month (~22% Y/Y). We see it all shaking out to show a small decrease in the headline rate (3.3% to 3.1%) but fully expect inflation will resume its upward march over coming months. Retail sales and public finance figures for April will also be released later in the week.

Key data releases and events (week commencing Monday 18 May)

Day | Time | Region | Event | Period | Consensus | MUFG | Previous |

Tue 19 May | 7:00 | UK | Private Earnings ex Bonus 3M/YoY | Mar | 3.1 | 3.2 | 3.2 |

Tue 19 May | 7:00 | UK | ILO Unemployment Rate 3Mths | Mar | 4.8 | 4.9 | 4.9 |

Tue 19 May | 7:00 | UK | Payrolled Employees Monthly Change | Apr | -10k | -15k | -11k |

Wed 20 May | 7:00 | UK | CPI YoY | Apr | 3.0 | 3.1 | 3.3 |

Thu 21 May | 8:15 | FR | S&P Global France Composite PMI | May P | 47.6 | 47.1 | 47.6 |

Thu 21 May | 8:30 | GE | S&P Global Germany Composite PMI | May P | 48.5 | 48.0 | 48.4 |

Thu 21 May | 9:00 | EC | S&P Global Eurozone Composite PMI | May P | 48.7 | 48.2 | 48.8 |

Thu 21 May | 9:30 | UK | S&P Global UK Composite PMI | May P | 51.6 | 50.9 | 52.6 |

Thu 21 May | 15:00 | EC | Consumer Confidence | May P | -20.8 | -30.0 | -20.6 |

Fri 22 May | 0:01 | UK | GfK Consumer Confidence | May | -28 | -28 | -25 |

Fri 22 May | 7:00 | UK | Public Sector Net Borrowing | Apr | 20.8 | 22.0 | 12.6b |

Fri 22 May | 7:00 | GE | GfK Consumer Confidence | Jun | -34.0 | -33.5 | -33.3 |

Fri 22 May | 7:00 | UK | Retail Sales Inc Auto Fuel MoM | Apr | -0.6 | -1.4 | 0.7 |

Fri 22 May | 9:00 | GE | IFO Business Climate | May | 84.3 | 83.5 | 84.4 |

Fri 22 May | 9:00 | GE | IFO Expectations | May | 83.6 | 82.3 | 83.3 |

Note: All times are GMT+1 (London). Source: Bloomberg, MUFG GMR