UK PM Starmer seems safe – for now: The UK local election results look bruising for Labour but not immediately catastrophic for Starmer. The PM’s authority will be further eroded, but the chances of an immediate challenge may have faded. Gilts rallied modestly in response to Starmer’s announcement that he does not intend to step aside. Uncertainty will remain elevated, however, and political risk could add to market volatility which is still driven primarily by energy pricing and Middle East developments.

The week that was: Away from UK politics and US-Iran developments it has been a quiet week in Europe. Weak German industrial production data raises concerns about a lack of growth momentum coming into this energy shock period. Tariff risks also re-emerged with the US threatening to raise tariffs on autos if last year’s trade agreement is not ratified, but the July deadline gives some breathing space.

What we’re watching next week: Fallout from the UK elections (especially any comments from cabinet members) will be the focus next week. It’s a light schedule on the data front in Europe again but UK Q1 GDP is set to show that the economy has repeated its pattern of making a strong start to the year.

Macro Focus: Starmer seems safe – for now at least

The Labour party suffered a bruising defeat in local UK elections, as expected, but the initial reaction suggests the PM will continue in his position

Yesterday’s UK local elections have long been circled as a potential flashpoint for embattled PM Starmer. A bruising result for his Labour party was expected and priced in by market participants. It will still be a while before we get the full picture from the patchwork of local elections around the country. At the time of writing the results for Labour seem in line with expectations, if not quite as bad as feared. Labour was defending around half of the contested 5,000 council seats. The party looks on course to lose over 1,000 of these but the losses, while heavy, will likely fall well short of credible ‘worst case’ scenarios of seat losses approaching 2,000.

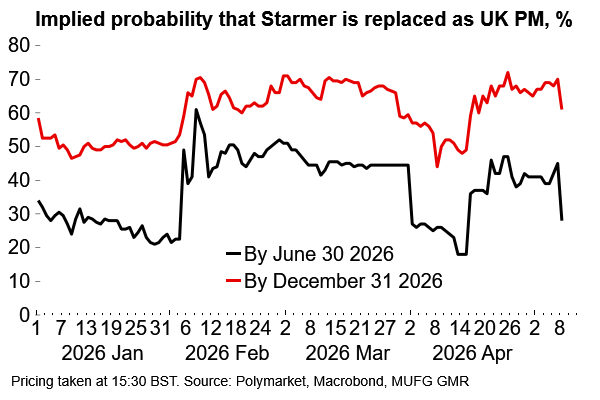

Starmer’s initial comments indicate that he has no intention of stepping down, saying he will “not walk away”. The implied probability that Starmer is replaced as PM this year fell from 70% to around 60% on prediction markets. The probability of a departure by end-June is now below 30% (see chart below). This feels about right to us.

The PM’s personal approval ratings are dire and Labour’s national polling is hovering around 20% (from 34% vote share at the 2024 general election). But a rival would need to muster the support of 81 Labour MPs (i.e. 20%) and at least two trade unions to trigger a leadership contest. The procedural bar is quite high and the PM continues to benefit from the absence of an obvious candidate to replace him. The current frontrunner in betting markets, Burnham, is not a sitting MP and would need to engineer a route back to parliament first. Based on the results this week we’re not convinced it would be a given that he would win a by-election – even if a sympathetic MP were to stand aside and Labour allows Burnham to stand in the ensuing contest. Meanwhile, there have been some stories that Rayner, who is seen as the next most likely alternative, would struggle to secure the backing of trade unions.

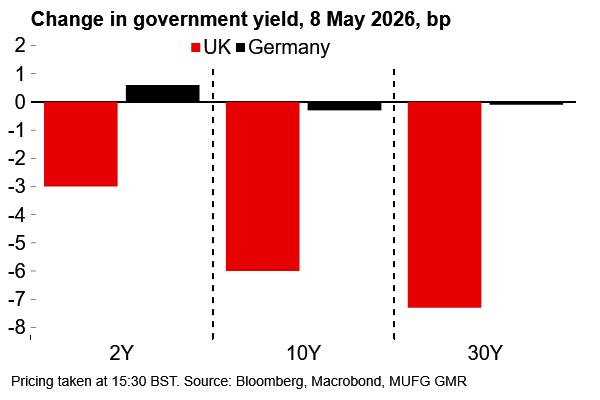

Gilts rallied after Starmer indicated that he does not intend to step down after the local election results

Prediction markets still imply that Starmer is more likely than not to be ousted this year (but may be safe for now...)

The dust will continue to settle on the result and there is still uncertainty around how Labour MPs will react now the sizeable losses are laid bare. The focus now will be on the weekend media round and any critical comments or signs of manoeuvring from cabinet ministers, in particular. Our initial sense is that, while the result is a bad loss for Labour, it is not as bad as feared, and not bad enough for MPs to panic and coalesce support around a single alternative candidate immediately.

Still, the results will further contribute to the erosion of Starmer’s authority. On balance, we just about agree with the consensus view that it’s more likely than not that Starmer will be ousted this year. In terms of timings, there’s a case for a move to be made by July to give time for a contest and a bedding-in period before the Labour Conference (27-30 September). That would be seen as a good time to formally launch a new leadership. But if Starmer is still leading the party at the time of the Conference, attention would turn to the Autumn Budget and potentially difficult fiscal decisions once again – and hence leadership speculation may fade until 2027.

In the meantime, we doubt there will be any knee-jerk fiscal reaction from Starmer. We continue to expect any policy support in response to rising energy costs will be targeted and relatively limited compared to the 2022 shock. Blatant fiscal giveaways to shore up public support would trigger a negative market reaction. Indeed, Starmer and Reeves might well lean into the narrative that alternative leaders would push up UK borrowing costs.

There is some truth in that. Gilts rallied following Starmer’s comments that he would not step down, especially at the longer end of the curve with 30y yields down ~8bp. It looks like a UK-specific move (see chart above). While it has certainly not been plain sailing for this government, Reeves has been consistent and credible in sticking to the fiscal rules and there are valid concerns around the possibility of a less market-sensitive UK administration.

There’s still plenty of scope for political risk to amplify UK market volatility over coming weeks and months. If a clear front-runner emerges to replace Starmer then markets could give a clearer signal around the specific fiscal risks. But it’s still worth stressing that, for all the political noise, it is energy pricing and the monetary policy outlook which remain the primary concern for investors. This was laid bare mid-week when gilts rallied on reports of a potential US-Iran agreement which pushed oil prices lower.

The week that was

Tariff threats and weak German industrial production

Away from UK politics there were further developments on the US-EU tariff front. Following last Friday’s threat to raise tariffs on EU automobiles to 25%, Trump announced that the EU has until 4 July to ratify last July’s trade deal or US tariffs will be increased. European Commission president Von der Leyen said that “good progress” is being made, but it is plausible that tariff tensions could rise again at a time when the European economy is facing a range of other external headwinds.

On the data front, German industrial production disappointed at -0.7% M/M in March with a downward revision to the previous number too. So much for a front-loading boost amid fears of deterioration in the Middle East situation. On a quarterly basis, industrial production fell by 1.2% Q/Q in Q1, which looks somewhat at odds with the initial estimate of GDP at 0.3%. A downward revision to that seems plausible which would weaken the narrative that the German (and euro area) economy was carrying a degree of momentum into the Iran conflict period.

What we’re watching next week

Never write off UK growth prospects (in Q1, at least)

It’s a relatively light data calendar next week. The first estimate of UK Q1 growth is probably the highlight. The monthly numbers up to February surpassed expectations and led us to raise our 2026 average growth forecast up to 0.8% (see here). In Q1 we look for a figure of 0.6% Q/Q. In the absence of revisions, it would take a huge contraction in the March monthly number to get anything below a respectable 0.5% for the Q/Q.

The lesson is clear: never write off UK growth prospects at the start of the year, with the pattern of strong Q1 growth well-established now. This may have initially been a residual seasonality problem following pandemic-related behaviour shifts, but we think increasingly reflects what we call ‘policy seasonality’. The recent cycle of intense speculation around the need for consolidation at the Autumn Budget (followed by relief that measures are not as bad as feared) has likely contributed to the UK’s bumpy GDP profile. Looking ahead, we fully expect another slowdown in activity through the year, but there are signs of resilience in the initial survey data following the start of the US-Iran conflict which suggest that activity in Q2, at least, might hold up better than expected. Resilient growth would build the case for BoE tightening, but the focus will be mostly on energy prices and the pass-through to pay. Policymakers will be closely watching the KPMG/REC report on jobs next week for any signs of rising wage pressures.

Key data releases and events (week commencing Monday 11 May)

Day | Time | Region | Event | Period | Cons. | MUFG | Previous |

Mon 11 May | 0:01 | UK | KPMG & REC UK Report on Jobs | - | - | - | - |

Tue 12 May | 10:00 | GE | ZEW Survey Expectations | May | -18.8 | -18.0 | -17.2 |

Tue 12 May | 10:00 | GE | ZEW Survey Current Situation | May | -78.0 | -75.4 | -73.7 |

Wed 13 May | 10:00 | EC | Industrial Production SA MoM | Mar | 0.3 | 0.1 | 0.4 |

Thu 14 May | 7:00 | UK | GDP QoQ | 1Q P | 0.6 | 0.6 | 0.1 |

Note: All times are GMT+1 (London). Source: Bloomberg, MUFG GMR