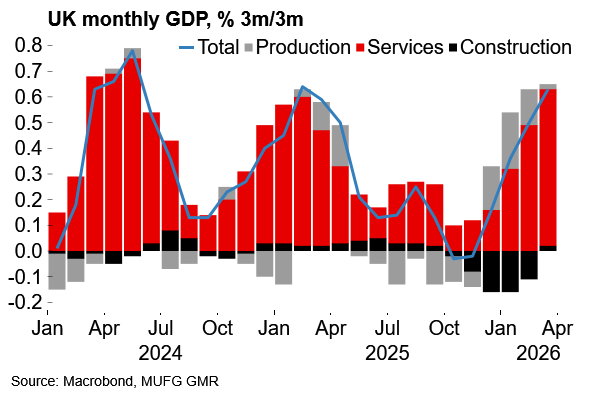

• The UK economy has again started the year with solid growth momentum. Q1 GDP at 0.6% Q/Q was in line with expectations but the monthly figure for March (0.3% M/M) was a notable upside surprise and suggests a degree of initial resilience to developments in the Middle East. Together, the data supports upward revisions to Q2 and 2026 annual average growth numbers. But quarterly growth is still set to fizzle out as effects from the Iran conflict percolate through the economy. The combination of a renewed real income squeeze, tighter financial conditions and softer external demand is likely to weigh on activity in coming quarters.

• The rise in domestic political uncertainty and associated tightening in financial conditions could amplify these headwinds to growth. The prospect of a potentially disruptive leadership transition and yet another challenging fiscal backdrop heading into the autumn is likely to weigh on sentiment. We see the balance of risks to the UK outlook as firmly skewed to the downside.

UK growth set to fizzle out after a strong start to the year

UK Q1 GDP data shows the economy was carrying good momentum coming into the Iran conflict period and heightened political uncertainty. The UK economy expanded by 0.6% Q/Q in Q1, in line with our expectations and the consensus. Concerns around lingering seasonal adjustment issues will remain (see e.g. here) but post-Budget clarity likely supported yet another strong start to the year with consumer spending contributing 0.3pp to the figure. Q4 growth was also revised higher (from 0.1% to 0.2% Q/Q). To us, the most eye-catching part of the release was the monthly GDP estimate for March, which came in at 0.3% M/M, well above expectations. That is the first bit of hard data on activity since the start of the Iran conflict and suggests a good degree of initial resilience. We will always caution against reading too much into the monthly numbers given their propensity for revision, but it is certainly encouraging.

Assuming an unchanged profile through April-June (i.e. no monthly growth), the latest data would be consistent with Q2 growth printing at 0.3% Q/Q. We had previously pencilled in a figure of 0.0% and the BoE looked for 0.1%. Combined with the upward revision to Q4 GDP it means that 1%+ annual average growth in 2026 suddenly looks plausible (our current forecast is for 0.8%). It is a good platform coming into what is set to be a challenging period for the economy. There have been encouraging signs of improving productivity growth in recent data – and AI investment and adoption could provide further support.

But it’s a case of what might have been. We fully expect growth will fizzle out over coming months as the inflationary consequences of the Iran conflict percolate through the economy. The real income squeeze, tighter financial conditions and weaker external demand are likely to increasingly weigh on activity, yet we still see the BoE being forced into at least two rate hikes this year. The UK is now also facing another bout of political instability, which we expect will also be a headwind to growth, at least at the margin, through delayed investment plans and amplified market volatility. In short, the economy may have carried good momentum at the start of the year, but the balance of risks remains firmly skewed to the downside.

Yet another fast start to the year for the UK economy

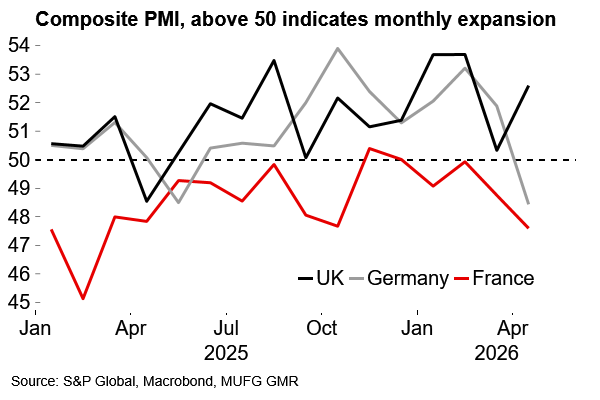

UK business sentiment was relatively resilient in April

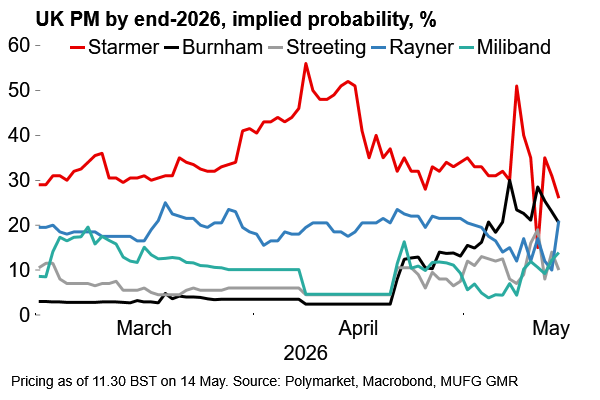

Political uncertainty adds to the downside risks

Our initial take on the local election results was that, while bad, they were no worse than expected and that PM Starmer might have been able to stumble on. But for Labour MPs there is a difference between expecting a bad result and actually seeing the numbers laid bare. The steady drip of criticism from backbenchers and junior minister resignations suggests that Starmer has lost authority within his party and, although he is digging in, it looks like a tough ask for the PM to turn things around from here.

It’s been clear that Starmer has been on thin ice for some time (see e.g. Political uncertainty remains the key UK risk theme). But there is no standout candidate to replace him and there’s an impossible trinity feel to the challenge of finding someone with the support of markets, MPs and the public. Streeting, from the right of the party, would be perceived as market-friendly but could struggle to secure the backing of the party. The relatively popular frontrunner, Burnham, still needs to engineer a route back to parliament. If a contest is forced in his absence by Streeting then other soft-left candidates (e.g. Miliband, Rayner) could push themselves forward. At that point the contest might open further with wild-card candidates putting themselves forward (e.g. Al Carns, a junior defence minister who is ambitious but has limited political experience). The situation is fluid but there is clear risk for a destabilising leadership contest rather than a smooth transition.

If Starmer is indeed on his way out, we assume there would be an aim to install a new leader by the time of the Labour conference (27-30 September). We doubt there would be much of a honeymoon period. A new leader would inherit exactly the same problems. Inflation looks on course to rise above 4% in H2, and growth is set to fade. The need for difficult fiscal decisions in the autumn looks likely yet again. The OBR estimated fiscal headroom at GBP 23.6bn in March. On current conditions we guess that this could be reduced by ~15bn in the autumn on the back of BoE re-pricing, higher borrowing costs and a weaker growth outlook. That is before higher spending demands – e.g. defence and household energy support measures – are considered.

Starmer/Reeves have been relatively market-sensitive and have managed to at least stabilise the UK’s fiscal situation, albeit with tax-to-GDP rising to a post-war high of 38%+ per the OBR’s projections. But there is little to address structural issues. There has been clear can-kicking on difficult decisions – the plans rely on a degree of ‘fiscal fiction’ with much of the consolidation back-loaded in nature (see UK Budget review: Relief for now but fiscal doubts remain). Dare we suggest that alternative leadership would be more effective, have better political instincts, and could plausibly sell the need for difficult trade-offs to the electorate – at least if justified by a macroeconomic shock? That would be the optimistic take on any transition.

On possible spending plans, the lesson from the Liz Truss episode is that gilt markets remain a powerful disciplining force. We assume that any new leadership will heed some lessons from that, and we’d expect messaging aimed at soothing investors’ nerves. There is also an obvious legitimacy gap if policies stray too far from the manifesto. But there is still a risk that market tolerance is misjudged and a new PM/chancellor would have to quickly backtrack from expansive spending pledges. The political damage from that would immediately undermine a new PM’s authority and further raise risks of policy drift and uncertainty.

The big picture here is that the UK has already had six PMs in the last decade. So much for hopes of relative stability under this government. The revolving door of leadership is plainly bad for investor sentiment. It has been a period marked by Brexit, overlapping external shocks and a tight fiscal backdrop. But some fundamental shifts – e.g. a weakening of the political centre and move into an era of multi-party politics – look likely to remain relevant. Under the FPTP electoral system shallow majorities and leaders with thin authority could increasingly become the new norm. In that environment we suspect that UK assets will continue to reflect a relatively high political risk premium.

The UK leadership outlook is highly uncertain

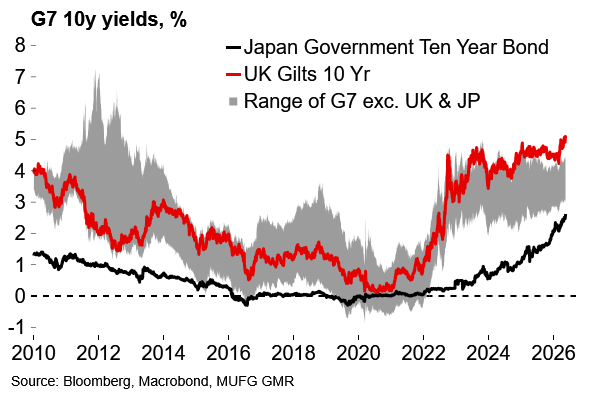

UK borrowing costs have diverged from G7 peers