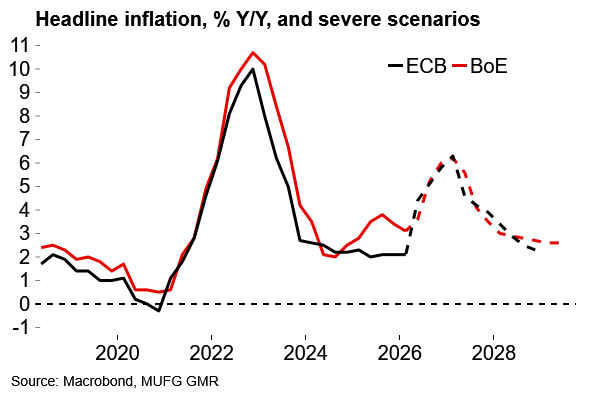

- Energy prices continue to steer the monetary policy outlook: The ECB and BoE held rates this week, as expected, but the argument for patience will become less tenable unless energy costs retrace quickly. Both central banks are grappling with the same problem and see similar peaks in inflation (~6%) in their respective severe scenarios. The BoE comes into this crisis with rates above neutral but the UK’s recent experience of higher inflation raises second-round risks. We expect both the ECB and the BoE will raise rates by 50bp this year.

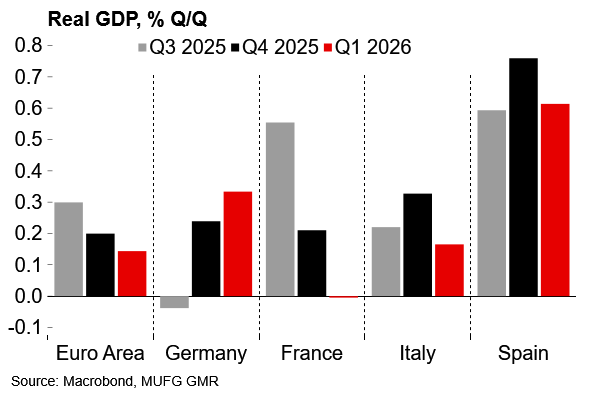

- Data already underscores the stagflation challenges ahead: Euro area GDP fell short of expectations in Q1 at 0.1% Q/Q, dragged down by a sharp contraction in Ireland. Some of the other national figures were better but overall growth momentum is clearly weak. There is already a clear whiff of stagflation around with euro area inflation pushing higher to 3.0% in April and headline rates set to move above 4% by year-end on our estimates.

- What we’re watching next week: A flurry of ECB & BoE speakers may shed some further light on reaction functions after this week’s meetings. In the UK, next week’s local elections will be the key focus. Heavy losses for the governing Labour party are expected but a particularly bruising result would further raise speculation around the future of PM Starmer.

Macro Focus: Energy prices continue to steer the monetary policy outlook

Still waiting for credibly durable de-escalation

The ECB and BoE both left rates unchanged yesterday as expected. Our initial take can be found here and here. The bottom line is that energy pricing remains the pertinent factor for policymakers. Unless there is a rapid decrease in energy prices over coming weeks, we think the case for patience will start to wear thin and we see both central banks raising rates at the next meeting in June.

Uncertainty is high and both central banks are working on the basis of scenarios now. To underline the similarity of the challenge, the ECB and the BoE both see inflation peaking north of 6% in their respective severe scenarios.

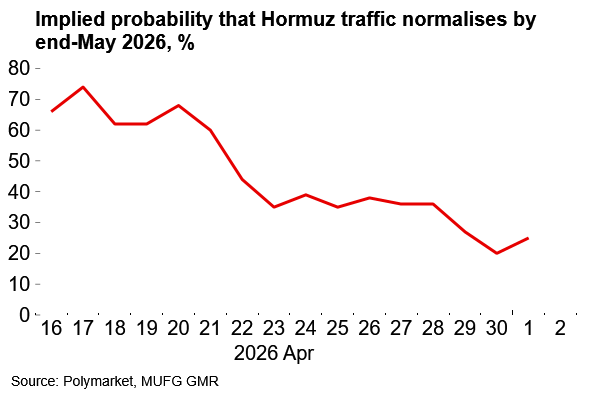

In terms of geopolitical assumptions, credibly durable de-escalation in the Middle East looks somewhat out of reach over the short-term. It quickly became clear that the ceasefire did not mean safe passage when Iran re-imposed “strict control” over the Strait. But, as time passes, it doesn’t seem like there’s a good platform for a negotiated outcome either, with limited sign of willingness from either side to make concessions so far. At the time of writing, prediction markets imply around 20% probability that shipping through the Strait of Hormuz will have normalised by end-May. Even if there is progress, markets will want to see a pattern of sustained safe transit through the Strait. It’s clear that reversing any reopening is a relatively low-cost form of re-escalation for Iran and that points to some persistent volatility and elevated risk premia in shipping and energy costs.

Expectations for de-escalation in the Middle East have faded

Both the BoE and ECB are working on the basis of scenarios - and have similar bad-case inflation profiles

We assume that both the ECB and the BoE will hike in June:

22bp of ECB hikes and 15bp of BoE hikes are priced for June at the time of writing. For now, central banks can point to the fact that financial conditions have tightened without any policy move following the market repricing of policy expectations. That may buy some time, but the ‘advance effect’ will need to eventually be validated by policy action if the energy shock persists.

If energy costs remain high at the time of the next policy meetings (11 June for the ECB, 18 June for the BoE) we would expect both central banks to hike. Yesterday the ECB continued its core messaging from the March meeting but provided clear signals that June is a live meeting. Lagarde said “I think directionally, I know where we’re heading”. Post-meeting reports from ‘ECB sources’ then emphasised that policymakers are leaning towards a hike in June.

There is more doubt about whether the BoE would move in June. As we stressed yesterday, we think that the BoE was trying to convey a sense of relative patience and composure after the surprisingly hawkish messaging at the March meeting. But the central guidance – that the MPC stands ready to act as necessary – remains unchanged. This was an “active hold” which left little doubt that future tightening is on the cards. Setting the common energy backdrop to one side, we also think that there could be some relevant peer effects, at least at the margin, if the ECB were to raise rates the week before the BoE’s next meeting.

The argument for proactive tightening will get stronger: Bailey said yesterday that “it would be a mistake to wait to see second round effects before acting because then it would be too late”. That certainly applies to the ECB too and we continue to expect both central banks will try to get ahead of the curve. We see a logic in policymakers immediately following a June hike with another move in July if energy prices remain elevated. Once officials feel that the threshold for initial tightening has been reached then we’d expect clearer rhetoric around the willingness to be proactive. A delay to September is certainly plausible but would risk diluting the message around the intention to contain second-round risks.

Unlike the ECB (which has rates at neutral) the BoE comes into this crisis with policy already in mildly restrictive territory. But the BoE has more reason to fret about second-round risks to wage- and price-setting behaviour with UK inflation averaging 5.5% since 2022 – which is 1pp more than the euro area average. We currently expect 50bp of tightening from both the ECB and the BoE this year.

The week that was

Ireland giveth, Ireland taketh away

It’s also been a busy week on the data front in the euro area. The first estimate of euro area GDP growth in Q1 came in at 0.1% Q/Q, below both our and the consensus expectations (0.2%). A sharp fall in the always-volatile Irish GDP numbers (-2.0% Q/Q) subtracted 0.1pp from the aggregate growth figure. It’s no surprise to see some more mean reversion after Ireland boosted euro area growth numbers significantly around the turn of 2024/25. Setting that distortion aside, growth was reasonably firm in Germany (0.3% Q/Q) with the release noting growth in household and government consumption. Italian growth (0.2% Q/Q) would likely have looked weaker without the Winter Olympics boost. Spain (0.6% Q/Q) remains the euro area’s star performer, while France was the main disappointment at the start of the year with no growth on the quarter. All told, it’s not a great platform for growth coming into the conflict period even accounting for the Ireland distortion. Data at the start of Q2 continues to look weak. There are plenty of signs of slack in the latest German labour market numbers for April, while the European Commission’s survey reinforced the weak signals shown in last week’s PMI data for the euro area.

Aggregate euro area growth is fading…

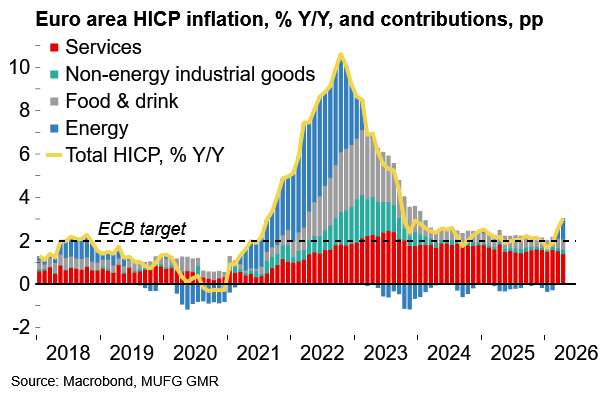

…and the period of well-behaved inflation is over

Euro area inflation will continue to rise

The flash euro area inflation figure for April matched our expectations at 3.0% (+0.4pp on March, +1.1pp on February) but was close to rounding up to 3.1%. It is the highest rate since September 2023, unsurprisingly driven by energy (10.9%). There were a few signs of continued disinflation in underlying components with core down 0.1pp to 2.2% and services down 0.2pp to 3.0%. As we discussed last week, rising spot inflation data is obviously not a surprise with the mechanical energy pass-through and any impact on core components set to be lagged. But combined with the weak growth numbers set out above there is more than a whiff of stagflation in the air already – and conditions will continue to worsen as the Middle East shock percolates through the economy. We expect headline euro area inflation will rise above 4% by year-end.

What we’re watching next week

Central bank speakers and UK local elections in focus

It’s a relatively light data calendar next week but we’ll be watching for the ECB’s latest wage tracker data and the German industrial numbers. There will also be the final PMIs for April (with initial estimates for Italy and Spain) as well as the Sentix survey which will provide a first look at sentiment in May.

Away from the data flow, a post-meeting flurry of ECB and BoE speakers could provide some further clues about reaction functions. We will also be closely watching the UK local elections and subsequent fallout with the governing Labour party on course for heavy losses. A particularly bruising result would further increase the pressure on PM Starmer – prediction markets currently imply around a 2/3 probability that he is ousted by year-end. Political uncertainty is set to remain a key UK risk theme (see here).

Key data releases and events (week commencing Monday 4 May)

|

Day |

Time |

Region |

Event |

Period |

Consensus |

MUFG |

Previous |

|

Mon 4 May |

09:30 |

EC |

Sentix Investor Confidence |

May |

-21 |

-23 |

-19.2 |

|

Wed 6 May |

07:45 |

FR |

Industrial Production MoM |

Mar |

0.5 |

0.2 |

-0.7 |

|

Wed 6 May |

09:00 |

EC |

ECB Wage Tracker |

|

- |

- |

|

|

Thu 7 May |

07:00 |

GE |

Factory Orders MoM |

Mar |

1.0 |

1.4 |

0.9 |

|

Fri 8 May |

07:00 |

GE |

Industrial Production SA MoM |

Mar |

0.7 |

0.4 |

-0.3 |

Note: All times are GMT+1 (London). Source: Bloomberg, MUFG GMR