ECB Review: Time is running out to look through energy price shock

- Macro view: The ECB left its policy rates unchanged at today’s meeting. The ECB highlighted that upside risks to inflation and downside risks to growth have intensified. However, the ECB did not judge that it warranted an immediate rate hike and preferred to take more time to assess the impact on the euro-zone economy from the energy price shock. President Lagarde indicated that the euro-zone economy is moving away from their baseline scenario but did not go as far as saying that the adverse scenario was now the most likely outcome. It leaves the door open for measured rate hikes beginning at the next policy meeting in June.

- Markets view: The market response both for euro-zone rates and the EUR was only modest highlighting that there were no major policy surprises from today’s meeting. The euro-zone rate market is already pricing in multiple ECB rate hikes which remains plausible while the Strait of Hormuz is effectively closed. At the same time, the EUR remains resilient to the energy price shock. The ECB is still on course to hike rates ahead of the Fed narrowing yield spreads and offering support for EUR/USD.

Macro view: ECB acknowledges economy is moving away from baseline scenario

Need for “measured” policy tightening is increasing

The ECB decided to leave rates on hold at today’s policy meeting but acknowledged that upside risks to inflation and downside risks to growth have “intensified” as a result of the energy price shock. The ECB noted that the war in the Middle East has led to sharp increase in energy prices which have pushed up inflation and weighed on economic sentiment. The decision to leave rates on hold today allows the ECB more time to assess implications of the war for medium-term inflation and economic activity. The longer the war continues and the Strait of Hormuz remains effectively closed, the stronger the likely impact on broader inflation and the economy.

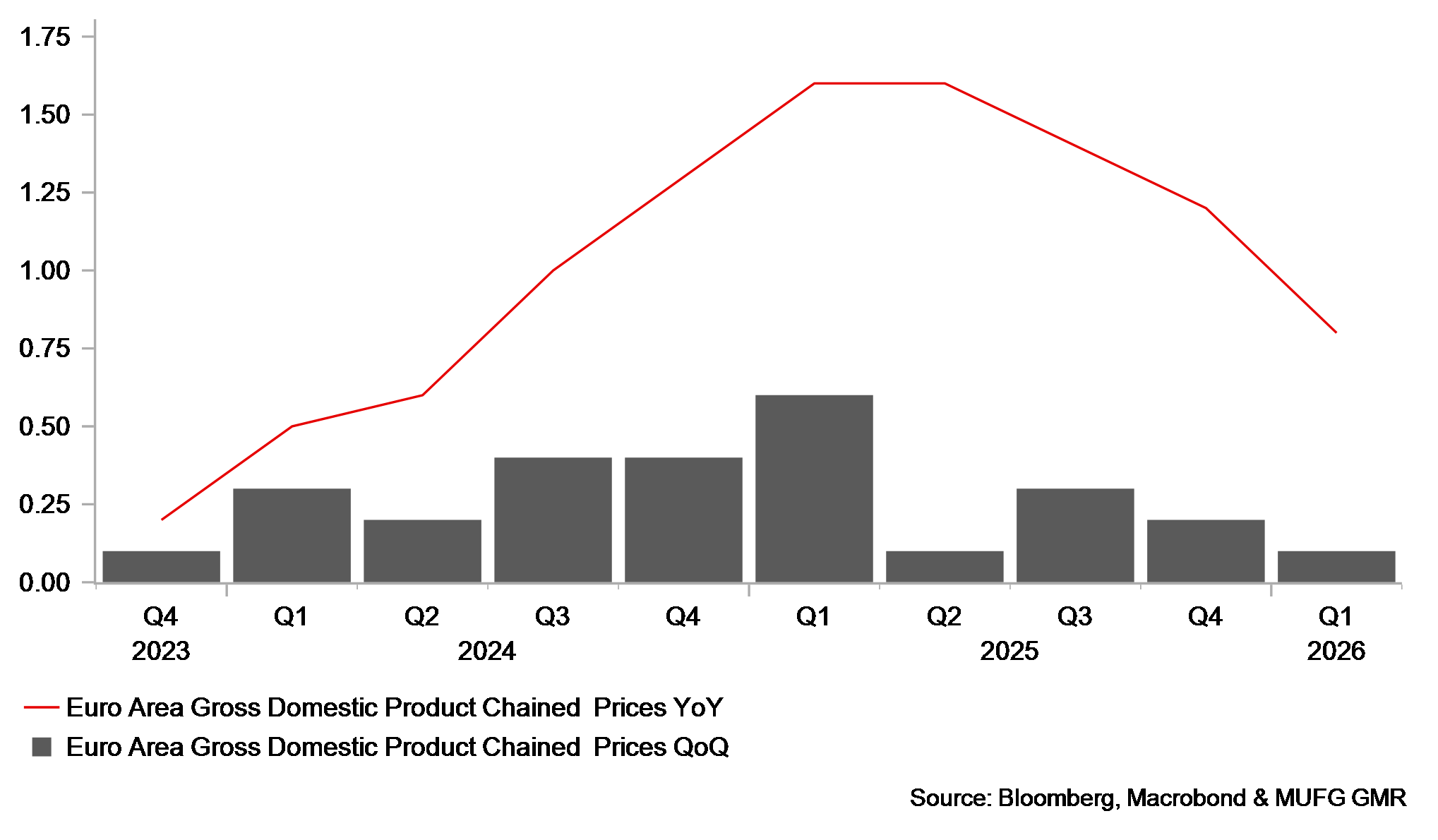

One positive factor for the ECB is that they continue to judge that they remain well positioned to navigate the current uncertainty. The ECB highlighted that inflation had already fallen back to around the ECB’s target prior to the energy price shock, and the euro-zone economy had shown resilience over recent quarters. However, this morning’s release of the latest GDP report for Q1 revealed slowing growth momentum as the euro-zone economy expanded by only 0.1%. It was the weakest quarter of growth since Q2 of last year. The loss of growth momentum was primarily driven by France where the economy stalled in Q1. In contrast, growth surprised modestly to the upside in Germany (0.3%), Italy (0.2%) and Spain (0.6%).

In the accompanying press conference, President Lagarde emphasized that the economic outlook is highly uncertain with the conflict weighing on economic activity while supply chains are coming under pressure from the ongoing closure of the Strait of Hormuz. The unfavourable developments in the Middle East are “certainly moving” the euro-zone economy “away from their baseline scenario” which assumes the inflationary effects from the energy price shock are temporary and fade quickly which would allow the ECB to look through higher inflation and leave rates on hold. However, she was reluctant to clarity whether the euro-zone economy is closer to the baseline or adverse scenario. In the adverse scenario, the energy price shock gives rise to a large but not-too-persistent overshoot of their inflation target. The ECB forecasts that annual inflation could rise almost one percentage point higher this year than in the baseline scenario, and could warrant “some measured adjustment of policy”.

With the economy judged to be somewhere between the baseline and adverse scenarios, the ECB debated various policy options today including hiking rates. The decision to ultimately leave rates on hold was unanimous. President Lagarde did appear to tee up a rate hike as soon as the next policy meeting in June by stating that the next six weeks will be “crucial” to make an informed decision. If there is no outcome to the Middle East conflict by then, it would be “significant”. At the June policy meeting, the ECB will also revise and update its scenarios for the euro-zone economy which could be used to justify taking policy action. By then it will have a better view on second-round effects from higher energy prices.

Overall, the updated policy guidance was broadly in line with recent communication from ECB officials including President Lagarde ahead of today’s meeting. We remain comfortable with our forecast for “measured” policy tightening and continue to forecast 50bps of hikes for this year. The first hike could be delivered at the next policy meeting in June unless there is a deal soon between the US and Iran to re-open the Strait of Hormuz. More front-loaded hikes would reduce the risk of the ECB falling behind the curve and then having to play catch up by delivering more forceful hikes further down the line.

Euro-zone growth slowed more than expected in Q1 prior to energy price shock

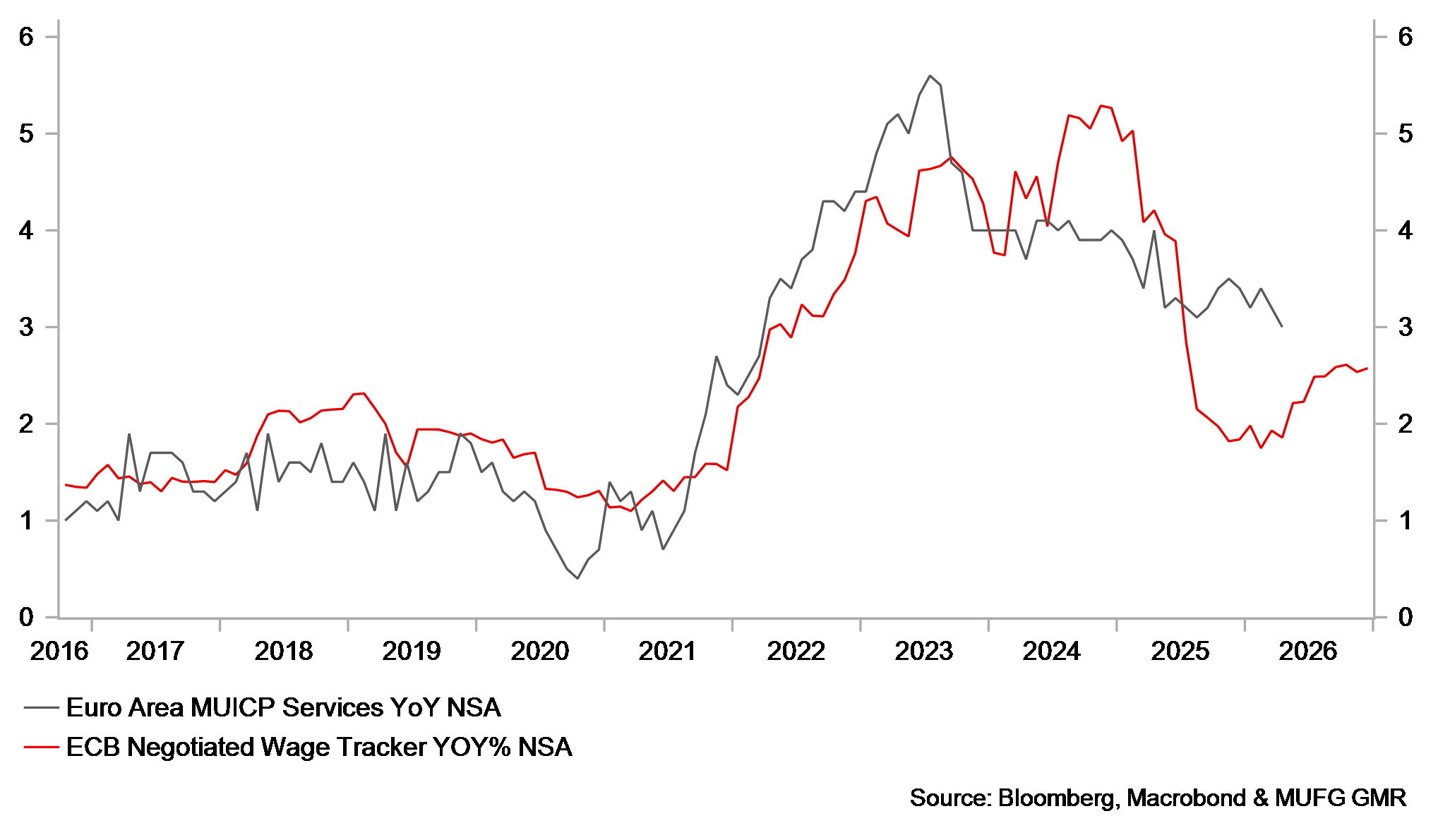

ECB is wary of second round effects from higher energy prices but still too early to call for hike

Markets view: Muted market reaction as ECB sticks to script

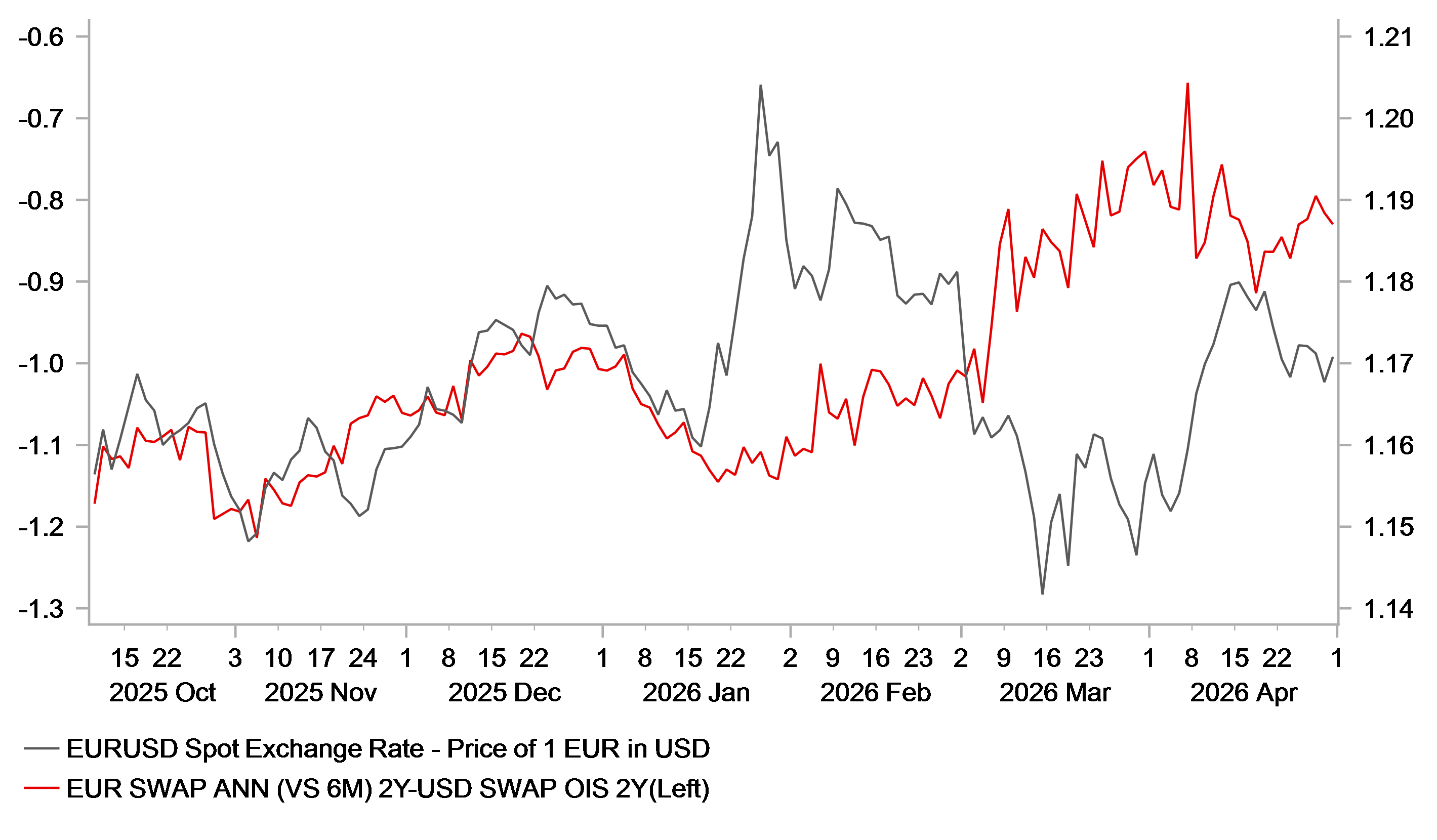

EUR & EZ rates are already expecting multiple ECB hikes

Today’s ECB policy update has had only a modest impact on the performance of the EUR. Prior to the policy announcement, EUR/USD was trading at closer to 1.1720 but then dropped back to a low of 1.1687. Similarly, EUR/GBP has fallen from around 0.8660 to a low of 0.8640. At the same time, the euro-zone rate market has moved to modestly scale back ECB rate hike expectations. The implied yield on the December 2026 three-month ESTR futures contract has declined by around 3bps. The muted market reaction highlights that there were no major policy surprises. The ECB’s recent clear policy guidance is helping to dampen interest rate volatility amidst heightened uncertainty stemming from the unprecedented energy price shock. The euro-zone rate market is still pricing in around 75ps of ECB hikes. While we are forecasting only 50bps of hikes, it is reasonable for the market to price in some risk of more forceful tightening under the “severe” scenario while the Strait of Hormuz remains effectively closed.

The EUR continues to prove more resilient than we had initially expected in response to the energy price shock. The price of Brent crude oil has increased by around 60% since the conflict started but EUR/USD has only declined by around 1.0%. After initially attempting and failing to break below support at the 1.1400-level, the pair has since settled between 1.1400 and 1.1900. The longer the Strait of Hormuz remains shut, the higher the risk that EUR/USD could retest the bottom of that range by triggering a bigger stagflationary shock for European economies. In the interim, the combination of resilient global investor risk sentiment and the ECB’s relatively hawkish policy stance are helping to provide support for the EUR. The ECB still appears on track to hike rates ahead of the Fed and to narrow yield spreads between the euro-zone and US.

RELATIONSHIP BETWEEN EUR/USD & YIELD SPREADS HAS BROKEN DOWN THIS YEAR

Source: Bloomberg, Macrobond & MUFG GMR