Headline UK inflation eased from 3.3% to 2.8% in April. There were a lot of moving parts to the release but the picture on underlying, domestically generated inflation looks better than expected. The rise in fuel prices remains the only obvious impact of the Iran conflict on CPI so far. But the good news is likely to be fleeting. Household energy prices will rise in July and PPI data make it clear that there are plenty of broader price pressures in the pipeline. We expect UK inflation to rise to 4% by year-end. For now, the combination of these numbers and yesterday’s soft labour market release may give the BoE a bit of breathing space, but we continue to expect 50bp of tightening this year.

Plenty of price pressures in the pipeline, despite good news on domestically generated inflation

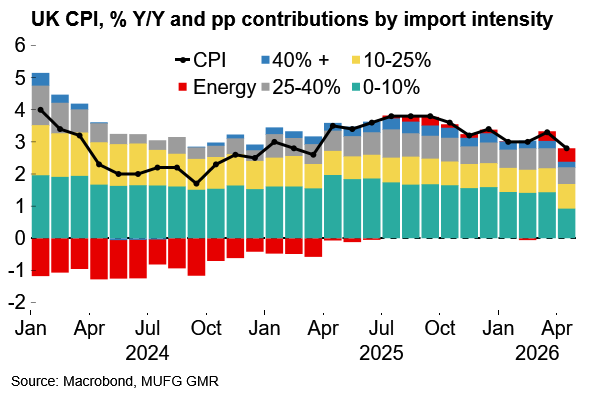

UK CPI was 2.8% in April, down from 3.3% in March and below the consensus and BoE expectation (3.0%). There were a lot of moving parts to the April number, and a forecast miss is no great surprise. The two main reasons for the decrease in the headline rate were: 1) favourable base effects after the jump in regulated/indexed services prices last year, and 2) lower household energy costs, largely driven by pre-Iran government policy decisions. The volatile airfares and package holiday components also weighed on headline inflation, and food inflation was softer than we expected. All of this more than offset the impact of higher fuel prices (23% Y/Y), which remains the only obvious impact of the Iran conflict on the CPI so far.

That will change. Regardless of any positive geopolitical developments, there is plenty of inflation in the pipeline with consequences of Hormuz disruption set to cascade through the economy. Producer input prices increased by 7.7% Y/Y in April. Factory gate prices rose by 4.0%. The decrease in household energy costs will also prove fleeting in the absence of any government support measures. The price cap is likely to be increased by 10-15% from July. The downward effect on the April inflation number from airfares/travel may well reverse next month as well. Looking ahead, we expect headline UK inflation to reach 4% by year-end, with more gradual pass-through to components such as food.

But the combination of these CPI numbers and yesterday’s labour market data (see here) reduce the pressure on the BoE to act immediately. Setting aside noise from base effects, energy policy and travel, today’s data shows that domestically generated inflation fell in April. There was some progress on underlying services inflation, which has eased below 4% to the lowest mark since early 2022. The benign food inflation number (3.0%, from 3.6%) will help ease some concerns around risks of higher household inflation expectations.

This week’s data gives the BoE a little more breathing space – but we still expect 50bp of tightening this year

However, the key point stands that it will be a long while before there is definitive evidence of second-round inflation effects, for example in 2027 annual pay settlements. Given that, we continue to expect that the BoE will raise rates by 50bp this year on a proactive/pre-emptive basis. That said, we had thought that a rate hike at the next meeting in June was possible (see here) but the combination of today’s data and heightened political uncertainty supports the case for patience. The projection meeting in July now looks the most likely juncture for the first move.

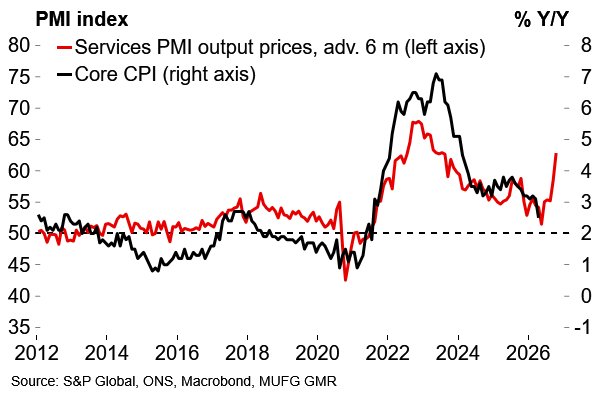

Looking back, we can’t help but consider what the macro landscape would have looked like without the Iran energy price shock. Take away the impact of higher fuel prices, and 1) UK inflation would have been very close to the 2% target, 2) labour market slack would likely support further BoE easing (i.e. our pre-Iran view), and 3) strong UK Q1 growth would be seen as a platform for the year ahead rather than a brief boost. But it’s a different world now, and policymakers will have to grapple with the challenge of stagflation ahead. That’s likely to be underscored in tomorrow’s flash PMI data for May. Further increases in the output price components would support the case for monetary tightening after what has been a week of dovish-looking data so far.

Domestically-generated inflation eased in April…

…but there are obvious risks ahead