Today’s UK labour market data reinforces the narrative of gradual cooling, but significant volatility (most notably in payrolls) complicates interpretation. The sharp drop in employment is very likely to be revised upward in subsequent releases, but other indicators, such as falling vacancies, still suggest plenty of slack. The BoE will likely downplay employment and pay data and instead focus on risks of second-round inflation effects in forward-looking indicators. We continue to expect 50bp of tightening this year. However, today’s numbers are on the dovish side and, combined with elevated political uncertainty, reduce the likelihood of a June hike.

Don’t take payrolls at face value – but the cooling labour market trend remains

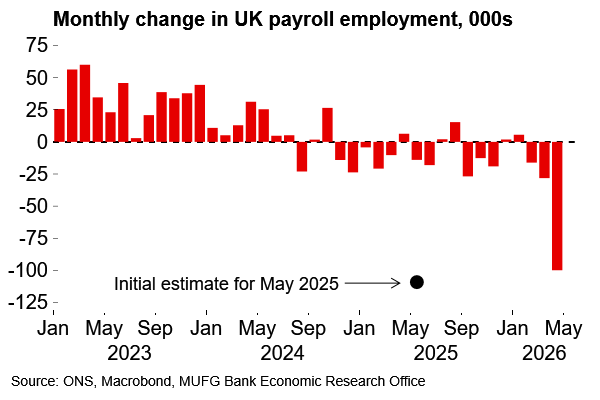

Today’s UK labour market data adds to the evidence of a gradual cooling in conditions, even if measurement issues require that some of the figures should be treated with caution. At first glance the most eye-catching element was the plunge in payroll employment. The first estimate showed that employment decreased by 100k in April relative to March (cons.: -11k, MUFG: -15k), the sharpest fall since May 2020. There are plenty of caveats, however. These payroll numbers are volatile and prone to revision at the best of times – but especially so early in the fiscal year. The ONS noted that: “Early months in the tax year typically carry a greater degree of uncertainty in their initial estimates, and such estimates in recent years have received larger-than-average upward revision.” For reference, the first print for April 2025 (-33k) has since been revised up to +6k. Perhaps even more relevant is the initial estimate for May last year which showed payroll employment falling by a huge 109k. That has since been revised up to just -14k (see chart below). Clearly, today’s number should be taken with a large dose of salt and the assumption should be that there will be sizeable upward revision down the line.

Setting payrolls aside, the rest of the release is still consistent with a stuttering UK labour market. The previous payrolls figure was revised lower (-11k to -28k). The headline unemployment rate increased from 4.9 to 5.0% with the single-month rate up to 5.5%. There are persistent issues here with sampling in the ONS Labour Force Survey which introduce volatility – but the general trend in the UK unemployment rate remains upward. Meanwhile, vacancies decreased by 7.1% Y/Y to the lowest level since early 2021.

In terms of risks, it’s worth stressing that the employment PMI in April was slightly better, and redundancy notification data, while moving higher in recent weeks, is not overly alarming at this stage. The UK economy also seems to be carrying a good degree of growth momentum (see here). But uncertainty is high and today’s heavily-caveated labour market numbers won’t help. Concerns that persistent labour market slack could evolve into something more alarming may rise in coming months. The flash PMI for May will be released on Thursday and we’ll be paying more attention to the employment components than usual. It’s certainly hard to see scope for the UK labour market to improve over the short-term. The Iran conflict is in its third month with the Strait of Hormuz issue looking no less intractable, and UK political uncertainty (see here) might also weigh on hiring sentiment..

Dovish jobs data but focus will remain on inflation risks

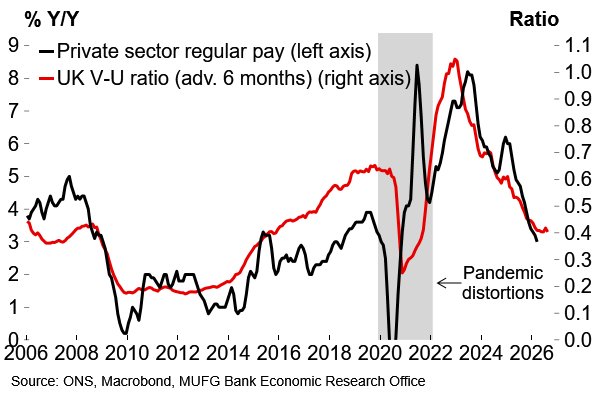

In terms of the BoE outlook, we cast our minds back to our pre-Iran view (e.g. here) that labour market slack would support further easing. Today’s numbers, which mostly reflect pre-Iran trends, would have been supportive of that. Private sector pay growth eased from 3.2% Y/Y to 3.0% Y/Y, slightly below the consensus and the BoE’s latest estimate.

But it’s a different world and spot pay data is less relevant now. Policymakers are firmly on the hunt for any sign of second-round effects on wages from energy-driven inflation. It will take time before that would show in these numbers and so the focus will remain on more forward-looking survey estimates. We continue to believe that these will provide sufficient cover for some pre-emptive tightening and expect 50bp of hikes this year. For now, dovish labour market data alongside heightened political uncertainty will support the case for patience. We had thought that a June rate hike was possible (see here) but July now looks the most likely juncture for the first move. Attention now turns to tomorrow’s inflation figure. There are a lot of moving parts in the April print but we expect these will shake out to show a small decrease in the headline figure (MUFG: 3.1%).

UK payroll employment plunged – but watch for revisions

Clear labour market slack and cooling pay growth