Tit-for-tat strikes fail to disrupt current market trends including stronger USD

USD: Building expectations for policy divergence driving stronger US dollar

The major foreign exchange rates have remained relatively stable overnight with the dollar index continuing to trade just below year to-date highs. Last week was the second consecutive week of gains for the US dollar after the Fed’s hawkish policy update although it did lose some upward momentum at the end of the week. Evidence of soft US consumption in Q1 and comments from New York Fed President Williams who indicated that he was comfortable with the Fed’s current policy stance have both helped to trigger a reversal of Fed rate hike expectations in the near-term. After hitting a high of 4.23% on 22nd June, the 2-year US Treasury yield has since dropped back by around 12bps.

In our latest FX Weekly report on Friday (click here) we highlighted how widening expectations for monetary policy divergence between the Fed and other major central banks particularly in Europe have triggered a bullish break out for the US dollar. We see two main scenarios for EUR/USD over the remainder of the year. In our base case, where the Fed does not follow through with rate hikes, we expect EUR/USD to move back up into the 1.1400–1.1800 range that has prevailed over the past year. Alternatively, if the Fed delivers multiple rate hikes, EUR/USD could fall further below 1.1000. Evidence of slowing US inflation and/or a less hawkish Fed reaction function would support a weaker USD, and vice versa in the months ahead. For now, we maintain our long USD/NOK trade recommendation (click here) until the recent hawkish repricing of Fed rate expectations is convincingly challenged. Looking ahead, this week’s ECB annual policy forum in Sintra should provide further insight into the extent to which monetary policy paths in Europe and the US are likely to diverge. ECB President Lagarde, new Fed Chair Warsh, BoE Governor Bailey and BoC Governor Macklem are all scheduled to take part in a policy panel discussion on Wednesday.

The sharp correction lower for energy prices has encouraged expectations that European central banks will be more cautious over tightening policy further given that upside risks to inflation have eased. European rate markets are now pricing in less than one rate hike by the end of this year for both the BoE and ECB. The recent US-Iran deal to reopen the Strait of Hormuz has contributed to the price of oil returning back to pre-conflict levels sooner than most people including major central banks would have expected. However, developments over the weekend in the Middle East have delivered a timely reminder that the risk of further energy supply disruption and upside risks have not completely gone away. The US and Iran engaged in tit-for-tat strikes at the end of last week after Iran struck a container ship. Iran also launched missiles and drones at a US air base in Kuwait and US naval base in Bahrain after the US hit military sites in Iran. However, the US and Iran have since agreed to stop attacking each other before peace talks resume this week. The latest military strikes provide highlight that the current ceasefire remains fragile yet there has been little impact on the oil market with prices continuing to trade closer to recent lows limiting any spillovers into the FX market.

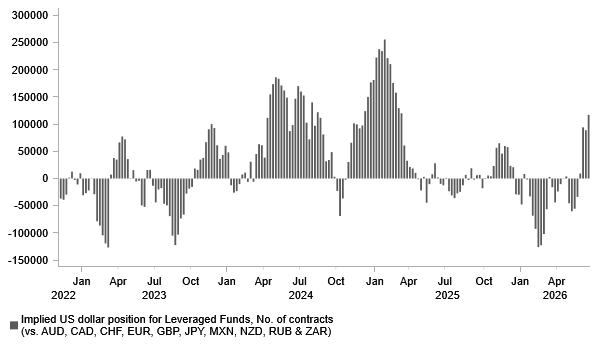

LEVERAGED FUNDS ADDING TO LONG USD POSITIONS

Source: Bloomberg, Macrobond & MUFG Research

GBP: Keynote speech rom Andy Burnham is likely to attract market attention

The pound is continuing to trade at close to recent lows against the US dollar at just above the 1.3200-level. On the other hand, the pound has remained more stable against the euro with EUR/GBP trading towards the bottom of the recent trading range between 0.8600 and 0.8700 where it has been for most of this year. The relative stability of the pound against the euro highlights that UK political risks have not yet significantly continued to a weaker pound this month. The move lower in cable has been driven more by the stronger US dollar leg.

Andy Burnham who is the next Prime Minister in waiting is set to make a keynote speech today laying out some of his views on economic and fiscal policy. It has been reported over the weekend that he will pledge the biggest devolution of powers in modern times to help “lift Britain back up” by handing more decision-making powers to local authorities, overhauling public procurement to boost British jobs and talking youth unemployment. It includes plans for more work placements and apprenticeships. He hopes to boost regional growth by giving local decision makers more power. He also reportedly wants to create a “No.10 North” to drive devolution and 10-year mission to raise living standards through industrialization, housing, infrastructure and reform of essential utilities.

So far market participants have not been unnerved by potential policy changes under his leadership. The 30-year gilt yield has fallen by around 40bps from last month’s high at 5.86% driven mainly by the paring back of inflation expectations and BoE rate hike expectations. Andy Burnahm’s pledge to stick to the government’s current fiscal rules curtailing room to loosen fiscal polices have also played a role. We are not expecting today’s speech from Andy Burham to change recent price action in the gilt market which limit spillovers. Market participants are waiting eagerly to see who Andy Burham will choose to be the chancellor after he is confirmed as the next Prime Minister.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 09:00 | M3 Money Supply | (May) | - | 17,433.9B | ! |

GB | 09:30 | M3 Money Supply | (May) | - | 3,272.0B | ! |

EU | 10:00 | Business Climate | (Jun) | - | -0.26 | ! |

AU | 12:30 | RBA Assist Gov Kent Speaks | - | - | - | !! |

US | 15:30 | Dallas Fed Mfg Business Index | (Jun) | - | 0.4 | ! |

EU | 18:30 | ECB President Lagarde Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com