To read the full report, please download PDF.

Fed opens door to stronger USD

FX View:

It has been an eventful week in the FX market, initially driven by the US–Iran deal and then quickly followed by a hawkish market reaction to the Fed’s policy update. The USD initially weakened in response to lower energy prices but swiftly reversed those losses after the Fed signalled increased concern about higher inflation. While we do not expect the Fed to raise rates given inflation risks are likely to ease in the coming months, US yields and the USD can continue to move higher in the near term after forward guidance was watered down. This is creating a more challenging backdrop for Japanese policymakers, as USD/JPY moves further above 160.00. The BoJ’s latest rate hike and updated forward guidance have not been sufficient to prevent further JPY weakness. Pressure will build on Japan to intervene again if the pace of depreciation accelerates. In contrast to the BoJ and the Fed, the BoE is not in a rush to tighten policy. We no longer expect the BoE to hike rates this year, leaving scope for UK yields and the GBP to continue adjusting lower.

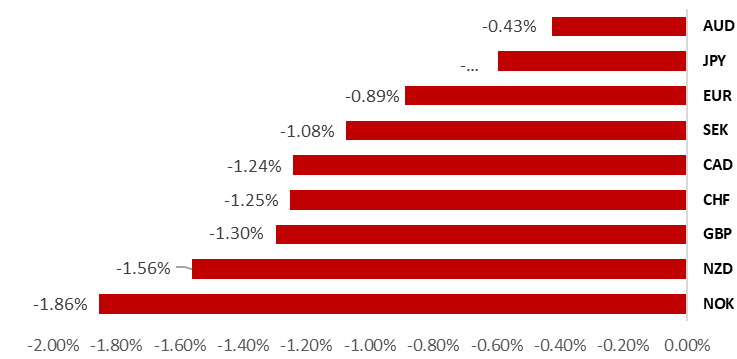

BROAD-BASED USD STRENGTH AFTER FOMC MEETING

Source: Bloomberg, close on 19th June 2026 (Weekly % Change vs. USD)

Trade Ideas:

We are recommending a new long USD/NOK trade idea to reflect lower energy prices and higher US rates.

JPY Portfolio Flows:

After a relatively subdued month for cross-border flows by Japanese investors in April, there was a notable pick-up in May. Japanese investors bought JPY 3,086bn worth of foreign bonds, the largest since July 2025.

AI Overview of BoE MPC Communication:

Our sentiment analysis points to a clear shift by the BoE into a high uncertainty hold phase, moving away from signalling proactive tightening.

FX Views

USD/JPY: Fed shift complicates MoF resistance to JPY depreciation

The US dollar buying momentum following the notable hawkish shift from the FOMC on Wednesday resulted in USD/JPY getting close to the 2024 high (161.95) but failed at 161.81 as fears over intervention prompted a pull-back. But USD/JPY looks very likely to test this high once again and the MoF will struggle to contain a move higher if the broader dollar sentiment remains positive. We already knew that the record one-month intervention total of JPY 11.7trn would likely fail to prompt a sustain move lower in USD/JPY given the fundamental backdrop. The hawkish shift from the Fed makes this even less likely and doubts over persisting with intervention are likely to grow.

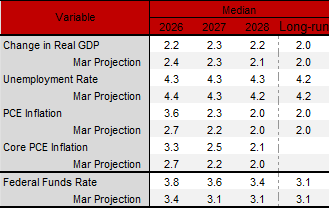

The shift in the dots profile relative to the last profile in March revealed on Wednesday was the largest ever since introduced in 2012. The nine FOMC members signalling at least one rate hike this year was in sharp contrast to none in March. Twelve FOMC members expected a rate cut compared to just one now. A hawkish shift in the dots profile was always likely given the Middle East conflict had been ongoing for most of the time since the March meeting and the labour market had shown greater strength than expected. However, the scale of the shift is surprising. Crude oil prices were falling sharply by the time of the dots being finalised (FOMC members would have finalised by end of last week) although oil prices have fallen nearly a further 10% since. The jobs numbers have been stronger but as the FOMC statement pointed out, the jobs growth has “kept pace with the workforce” and hence the unemployment rate was stable. Did the change in leadership at the FOMC in some way influence the scale of shift in the dots profile? That is certainly possible and, in any case, given Chair Warsh did not contribute his own dot and supports less forward guidance in principle, it seems likely that the median dots will soon be scrapped. We should probably give the dots less focus in that context than in the past.

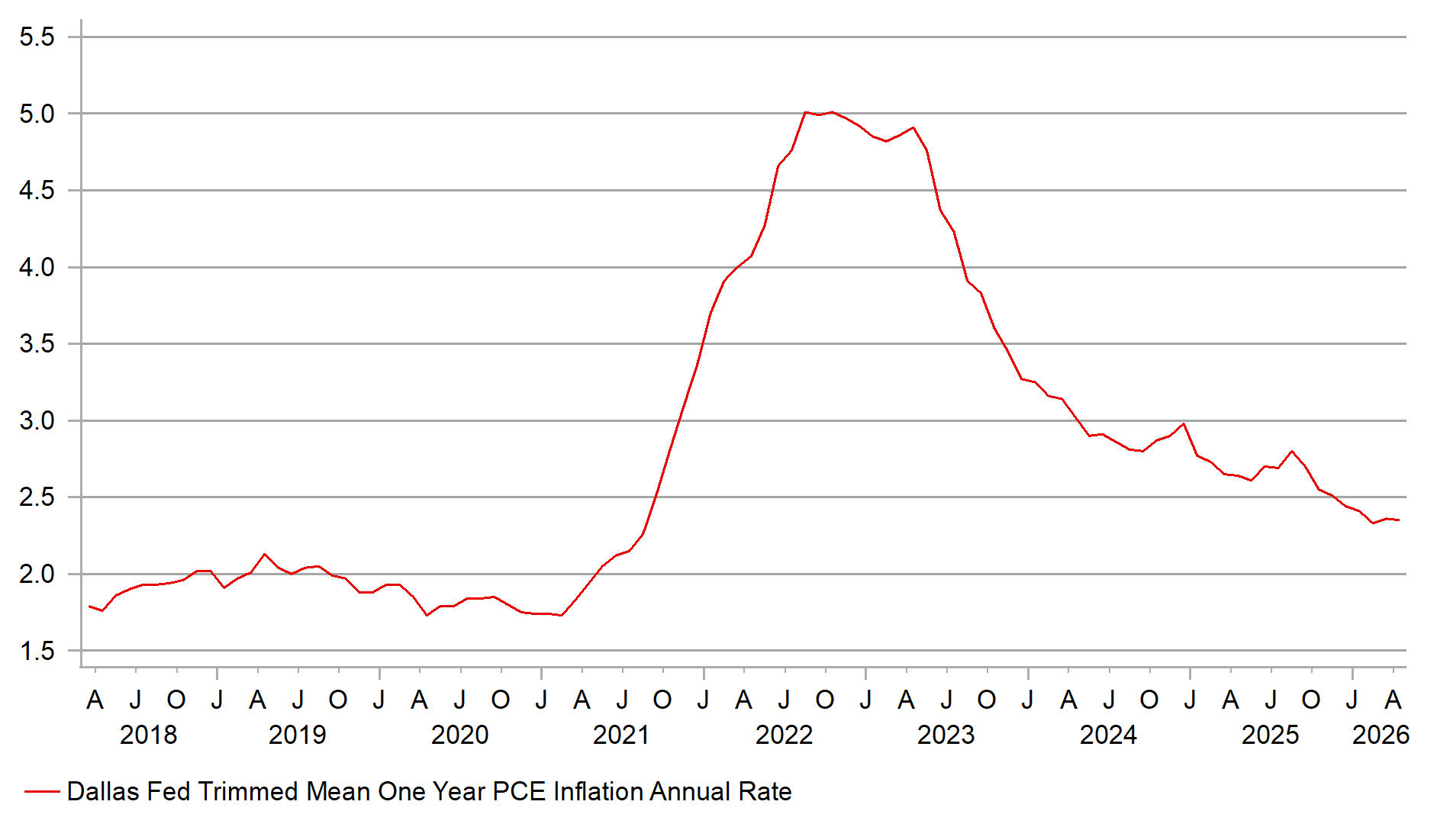

MUFG’s projections for annual inflation ahead points to the current annual inflation rate as being at or close to the peak. The trend going forward is one of disinflation. This is especially now the case given the scale of decline in crude oil prices. An OER/rents quirk in the inflation data due to a lack of collection during a previous government shutdown lifted inflation but is now reversing and has further to run. In addition, the lift to inflation last year due to tariffs implemented is now falling out of the annual calculations and that too has a little further to run and when combined to the energy disinflation, the annual inflation rate should turn notably lower. The Fed on Wednesday estimated YoY core PCE at 2.5% next year, down from 3.3% this year. There is scope for this to undershoot. The trimmed mean Dallas PCE YoY rate has remained stable at just 2.3%/2.4% over the last three months.

FED FORECASTS HIGH CORE PCE THROUGH 2027

Source: Federal Reserve SEPs June 2026 & MUFG

UNDERLYING US INFLATION IS STABLE

Source: Bloomberg, Macrobond & MUFG GMR

The BoJ action this week failed to alter the momentum for the yen although we would certainly argue that the overall tone of the communications from the BoJ was more hawkish than expected. There were more explicit references to upside inflation risks and there was no doubt that the message from the BoJ was that there would be further rate hikes ahead. However, another 25bp rate hike was nearly fully priced ahead of the meeting this week and the pricing now following the 25bp hike is roughly the same – so there was no sense from investors of any increased urgency to hike and the current pace of a hike every six months has failed to remove the concerns over the BoJ being behind the curve. Deputy Governor Himono spoke today and repeated what Deputy Governor Uchida stated this week that there was a risk that inflation could overshoot the 2% target. But bond market performance suggests investors are less concerned over that risk. The 2s10, 2s30s, and 2s40s curves have all flattened over the last month roughly in line with the decline in crude oil prices which are down by about 30% over the same period. Yields jumped today on Himino’s comments and given the modest bounce in crude oil prices given the refusal of Iran to sign the MoU. Core nationwide CPI YoY rate remained at 1.4% in data released today further reinforcing reduced fears over inflation risks.

Despite the renewed yen weakness that suggests investors remain concerned over the BoJ being behind the curve, the monetary policy setting has now reached the bottom of the R* range (-1.0% to +0.5%) at -1.0% (1.0% BoJ & 2.0% inflation target) and if we look at forward pricing the OIS market is indicating a policy rate of 1.50% implying an R* level of -0.5%. We doubt the BoJ is going to consider a faster pace of monetary tightening. The macro backdrop is broadly favourable – equity markets have been strong at record highs, bank stocks are also at record highs, inflation has receded from global inflation shock highs, wage growth has strengthened and debt-to-GDP is falling (the 5-year average YoY nominal GDP growth rate is the strongest since 1995). So there is little incentive for the BoJ to accelerate the pace of tightening and a break higher in USD/JPY (becoming much more likely) will have to be dealt with via MoF intervention rather than via a more hawkish BoJ.

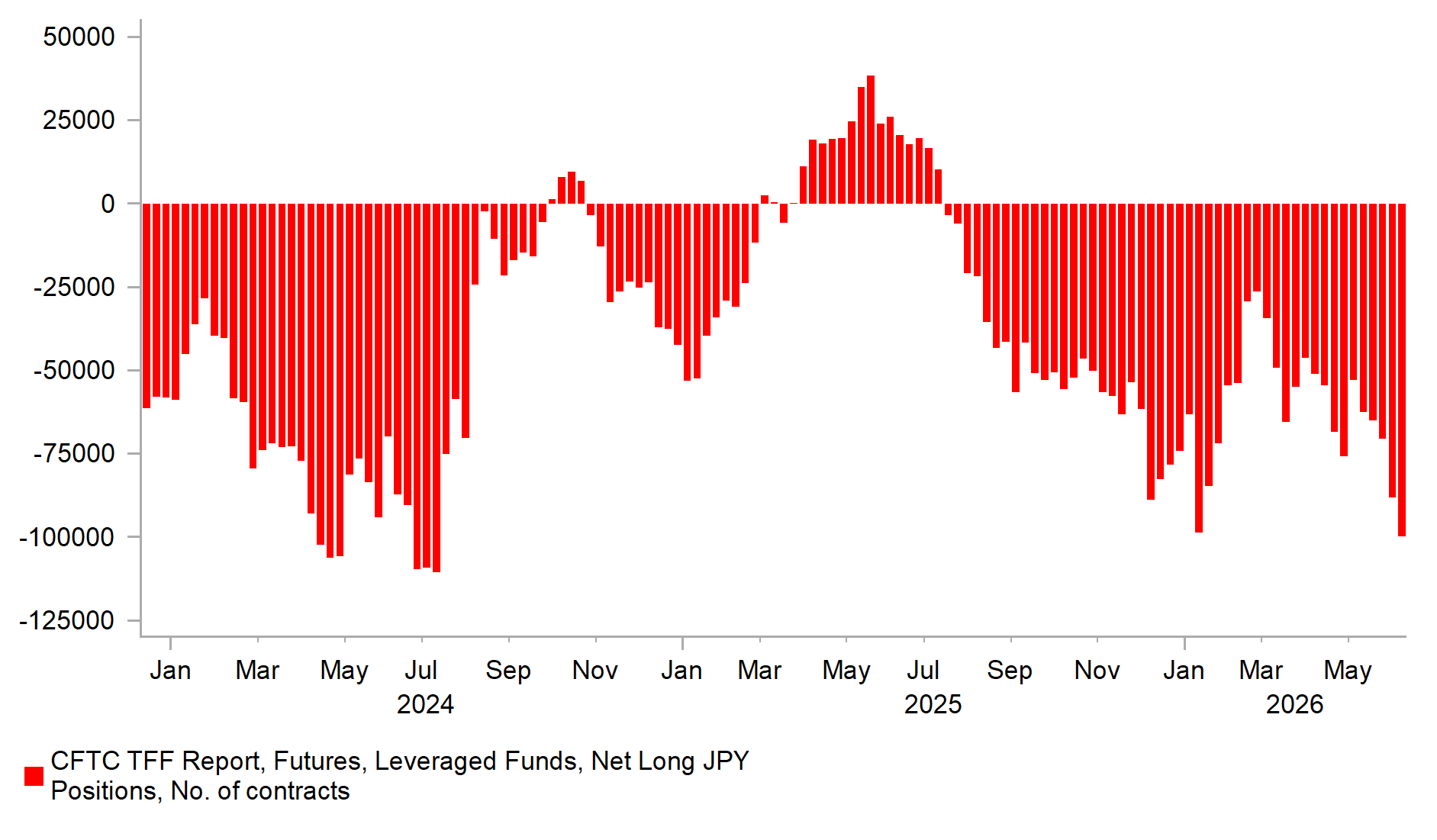

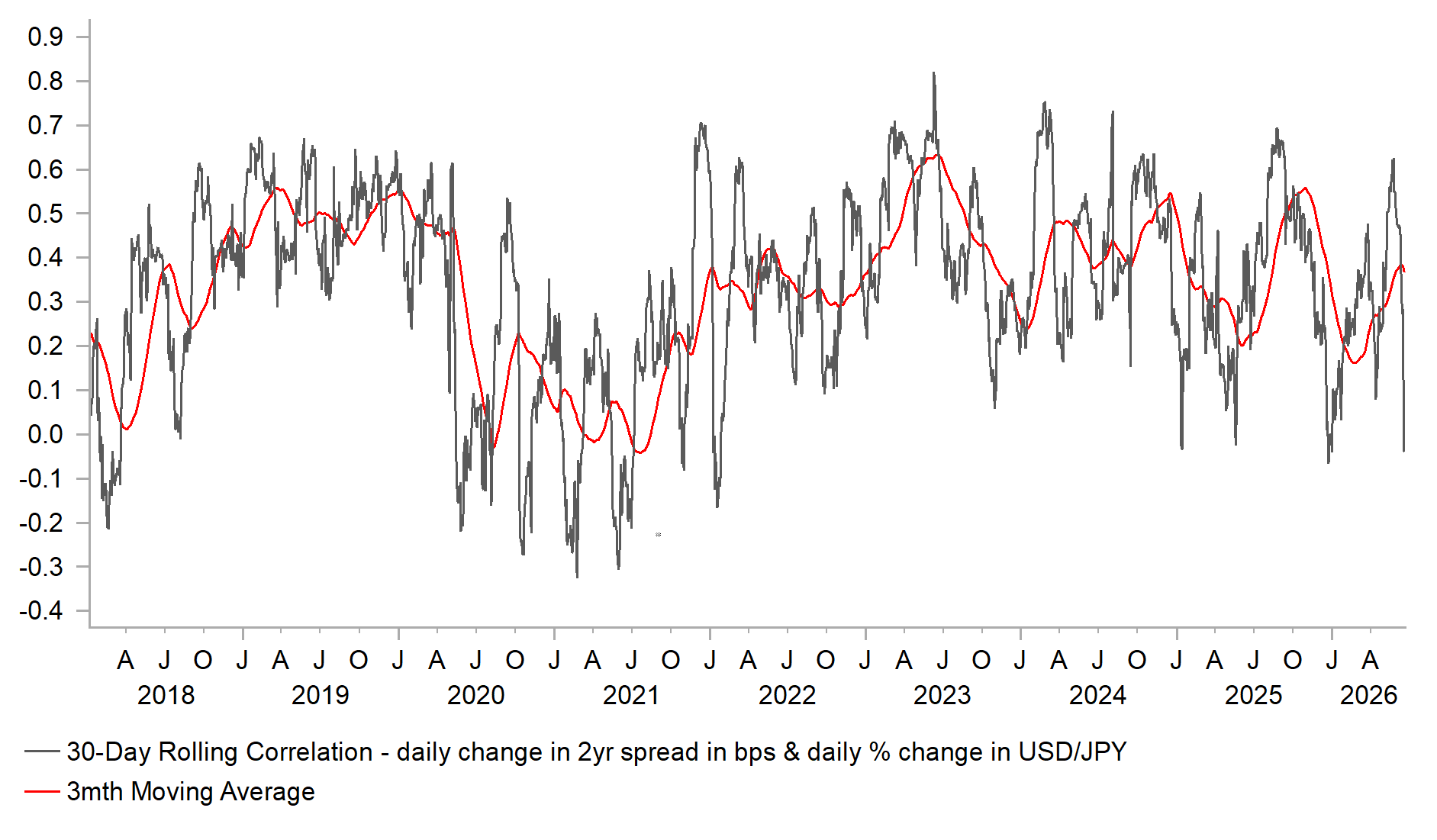

The MoF in April/May cited speculative selling of the yen as a factor in justifying yen buying intervention. That argument is stronger now, with short positions amongst Leveraged Funds back at the 2024 levels when USD/JPY last traded here. As can be seen below, those positions were liquidated abruptly after intervention although it coincided with a big equity correction and a drop in US yields. That fundamental backdrop looks different now and front-end yields in the US could drift further higher. The MoF is unlikely to abandon intervention, but it may accept new USD/JPY and intervention at higher levels around 165-170 – that’s the biggest risk now.

LEVERAGED FUNDS’ JPY SHORTS BACK AT 2024 LEVELS

Source: Bloomberg, Macrobond & MUFG GMR

INTERVENTION WEAKENED FX / RATES CORRELATION

Source: Bloomberg, Macrobond & MUFG GMR

GBP: Room for UK yields & GBP to continue adjusting lower

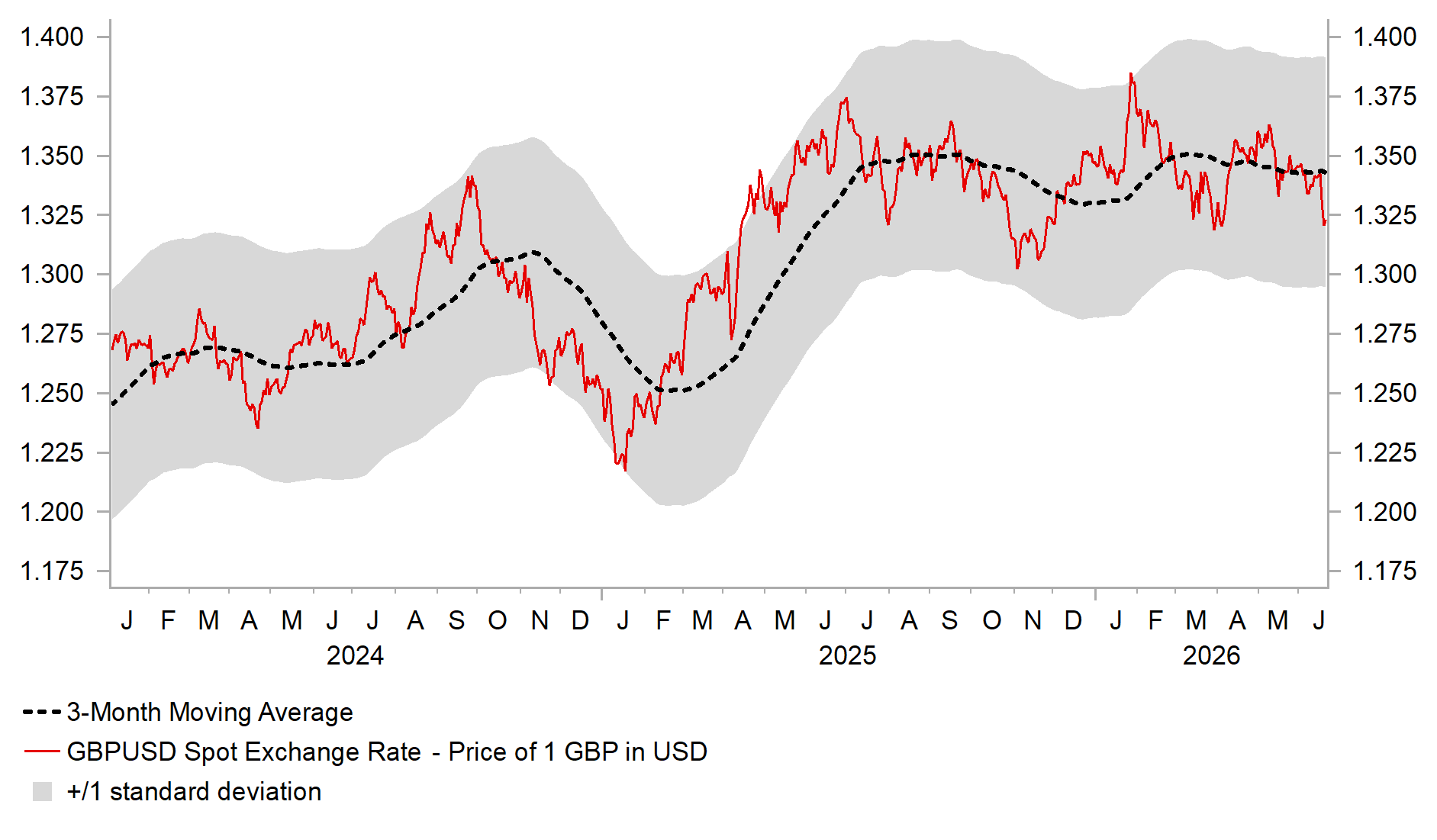

The GBP has underperformed over the past week, with cable falling back below support at the 1.3200 level and EUR/GBP rising towards the 0.8700-level. This follows a recent failure to break below the bottom of the current narrow trading range between 0.8600 and 0.8800. The US–Iran deal has initially contributed to a weaker GBP by lowering energy prices and UK yields. After failing to hold above resistance at 4.60%, the two-year gilt yield has declined towards support at 4.20%, reflecting a scaling back of BoE rate hike expectations. UK rate market participants are now less confident that the BoE will deliver multiple rate hikes and have pushed back the expected timing of a hike to later this year, likely in September or November. Alongside lower energy prices, evidence of softer inflation in May and a still-weak labour market are allowing the BoE more time to assess the impact of the energy price shock on the UK economy.

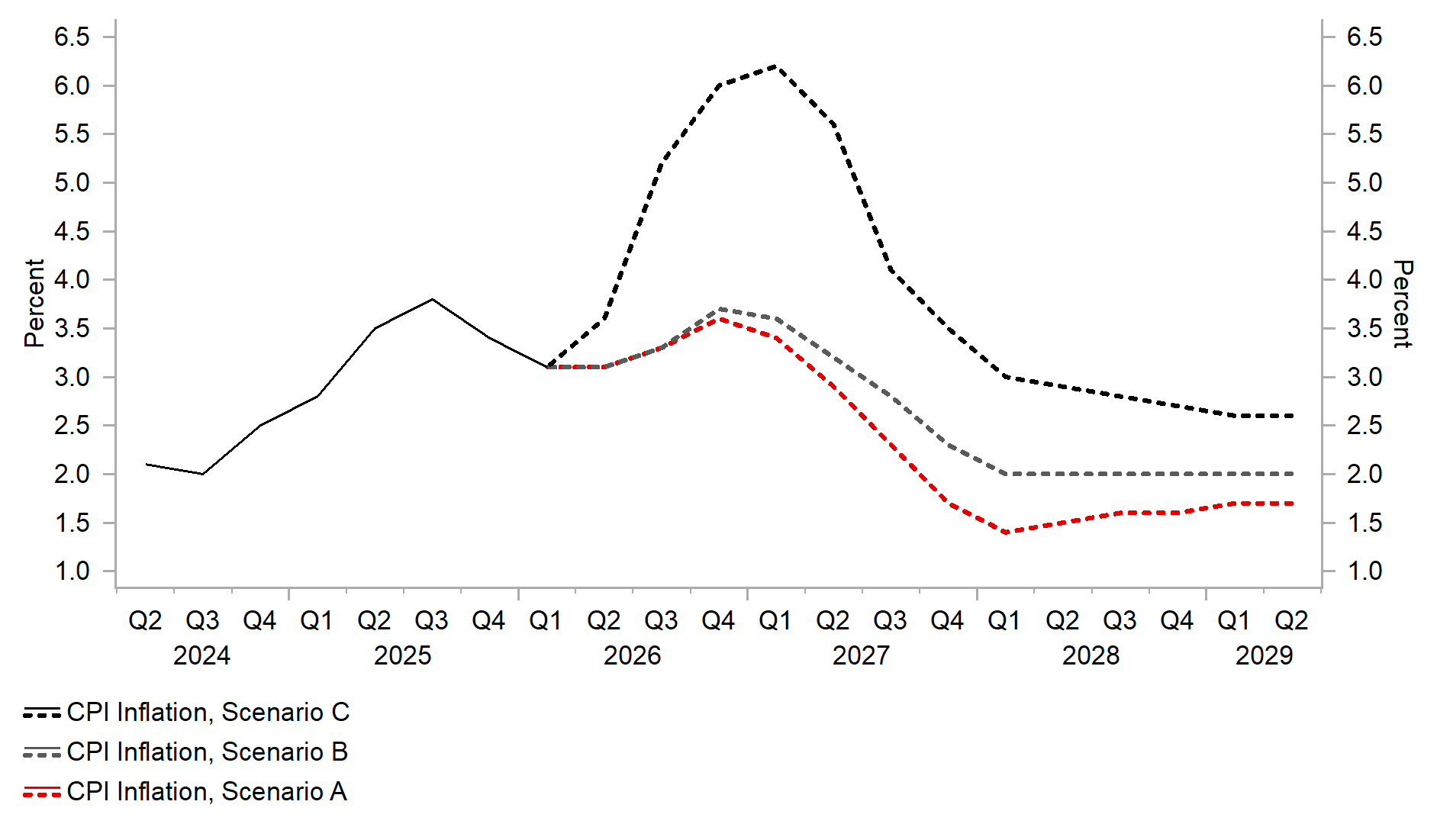

At this week’s MPC meeting (click here), the BoE indicated that it now expects inflation to rise less this year to just above 3.25% in Q4. This is even lower than the BoE’s best-case scenario (Scenario A) outlined in April, when inflation was projected to reach 3.6% in Q4. Under Scenario A, the energy price shock was expected to be short-lived, with weak demand helping to offset inflationary pressures and there are no meaningful second-round effects. It would allow the BoE to continue to judge that the tightening in financial conditions, driven by higher market rates since the onset of the Middle East conflict, provides sufficient monetary restraint without the need for additional rate hikes. Reduced concern over upside risks to inflation was also evident among the majority of MPC members, who voted to keep rates on hold this week. The higher bar for further tightening has led us to revise our outlook: we have dropped our forecast for two rate hikes this year and now expect the BoE to leave rates on hold, unless second-round effects such as stronger wage growth begin to emerge.

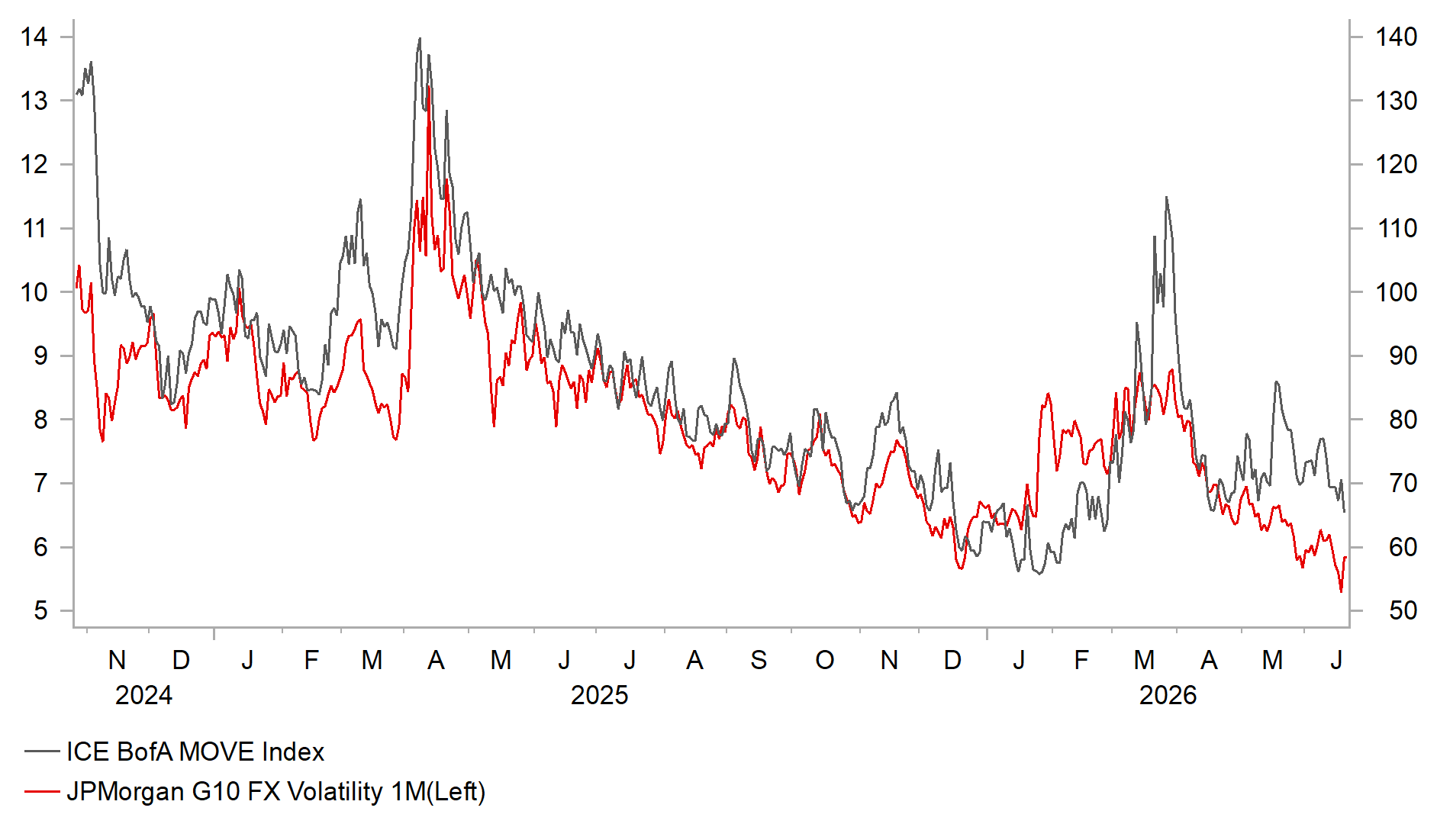

This leaves room for UK yields to continue adjusting lower, putting further downward pressure on GBP performance particularly against the USD, as US yields are currently moving higher to price in additional Fed rate hikes. At the same time, recent communication from ECB policymakers continues to signal readiness to deliver at least one more rate hike. Chief Economist Philip Lane made a timely intervention this week, noting that their estimate of the neutral policy rate has “crept up from 2.25% to 2.50%.” It highlights that the ECB believes it has scope to deliver one further hike without pushing policy into restrictive territory for the eurozone economy. This supports our decision to maintain our forecast for a final hike to 2.50% in September, despite the backdrop of lower energy prices. Recent developments have contributed to yield spreads moving against GBP, reinforcing our view that EUR/GBP will rise towards the upper end of its current trading range between 0.8600 and 0.8800. Furthermore, the Fed’s shift away from forward guidance has injected more volatility into financial markets, making the risk-reward profile for FX carry trades relative less attractive although volatility is still low. The GBP may also receive less support from carry-related demand if volatility picks up further.

CABLE IS TESTING RECENT LOWS AROUND 1.3200

Source: Bloomberg, Macrobond & MUFG GMR

UK INFLATION IS UNDERSHOOTING BOE SCENARIOS

Source: Bloomberg, Macrobond & MUFG GMR

Heightened political uncertainty in the UK could provide an additional near-term headwind for GBP, although we expect any initial negative impact from political change to be modest. Andy Burnham’s by-election victory in Makerfield at the end of this week is likely to pave the way for him to be installed soon as the next leader of the Labour Party and Prime Minister. It now appears to be only a matter of time before Keir Starmer is replaced. According to media reports, Burnham is hoping that Starmer will step down voluntarily to allow for an orderly transition of power. However, Starmer has publicly stated that he does not intend to resign. This stance is likely to increase pressure on Labour MPs to formally trigger a leadership challenge, which requires the support of 81 MPs. A threshold that should be readily met. If a challenge is initiated, the final decision over the next leader of the Labour Party will rest with party members. Burnham is by far the most popular potential candidate among members, and his standing has likely been strengthened further by his decisive victory over right-wing Reform and Restore candidates in the Makerfield by-election. As a result, Burnham is widely seen as the leader-in-waiting, and we expect him to be in place ahead of the Labour Party’s annual conference in September.

In the recent past, the prospect of Andy Burnham becoming Prime Minister would have triggered a more pronounced sell-off in gilts and the GBP. The relatively muted market reaction to the Makerfield by-election result suggests that market participants have become more comfortable with the potential policy changes under his leadership. Recent rhetoric appears designed to help stabilise the gilt market. Burnham has pledged to adhere to the government’s fiscal rules, limiting the scope for significant fiscal loosening. At the same time, it has been reported that he is expanding his team of economic advisers to strengthen the credibility of his policy platform. He has reportedly sought advice from former BoE Chief Economist Andy Haldane, former OBR Chair Richard Hughes, and former Goldman Sachs Chief Economist Jim O’Neill who are highly regarded by financial market participants. This helps to further ease concerns about the risk of a more disruptive shift to the left in policymaking. On the other hand, if Burnham proves overly cautious and avoids implementing more substantial policy changes, he may struggle to reverse the Labour Party’s declining public support. It leaves market participants waiting eagerly to see how fiscal policy evolves in the UK, with the Autumn Budget likely to be even more significant than usual.

REMOVAL OF FED GUIDANCE TO TRIGGER VOL PICK-UP?

Source: Bloomberg, Macrobond & MUFG GMR

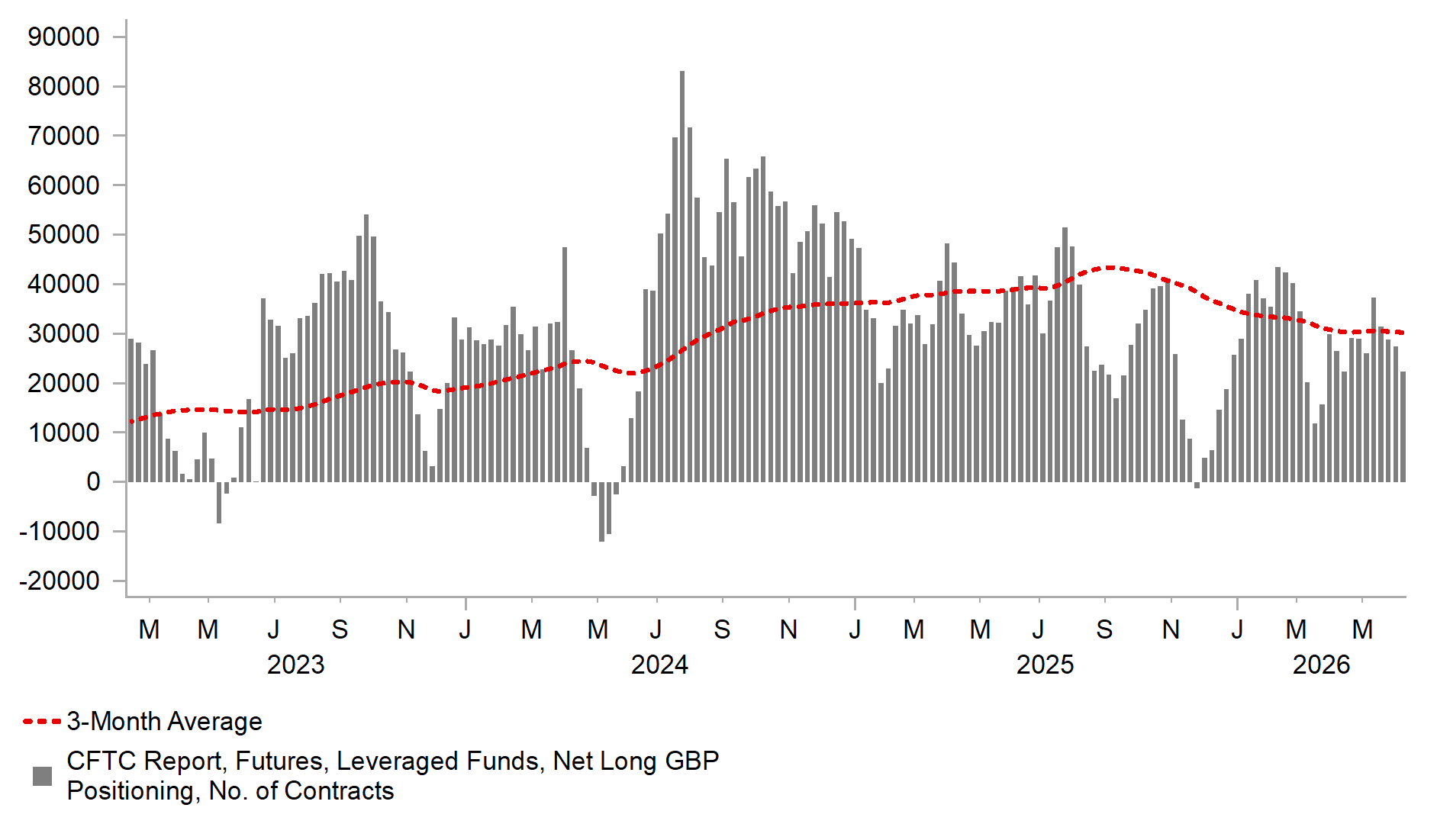

SCALING BACK OF LONG GBP POSITIONS

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

Ccy | Date | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

SZ | 22/06/2026 | 09:00 | Total Sight Deposits CHF | -- | 468.5b | ! | |

EC | 22/06/2026 | 13:30 | ECB's Lagarde Speaks in EU Parliament | !!! | |||

CA | 22/06/2026 | 13:30 | CPI YoY | May | 3.0% | 2.8% | !!! |

EC | 23/06/2026 | 09:00 | S&P Global Eurozone Manufacturing PMI | Jun P | -- | 51.6 | !!! |

EC | 23/06/2026 | 09:00 | S&P Global Eurozone Services PMI | Jun P | -- | 47.7 | !!! |

EC | 23/06/2026 | 09:30 | ECB's Lane Speaks in EU Parliament | !! | |||

UK | 23/06/2026 | 09:30 | S&P Global UK Services PMI | Jun P | -- | 49.3 | !!! |

UK | 23/06/2026 | 09:30 | S&P Global UK Manufacturing PMI | Jun P | -- | 53.9 | !!! |

CA | 23/06/2026 | 14:00 | BoC Governor Tiff Macklem Speaks | !!! | |||

US | 23/06/2026 | 14:45 | S&P Global US Composite PMI | Jun P | -- | 51.5 | !! |

UK | 23/06/2026 | 16:00 | BoE's Dhingra Speaks | !! | |||

AU | 24/06/2026 | 02:30 | CPI YoY | May | -- | 4.2% | !!! |

SW | 24/06/2026 | 08:30 | Riksbank Publishes Minutes | !! | |||

GE | 24/06/2026 | 09:00 | IFO Business Climate | Jun | -- | 84.9 | !!! |

UK | 24/06/2026 | 12:20 | BoE's Breeden Speaks | !! | |||

US | 24/06/2026 | 15:00 | New Home Sales | May | 640k | 622k | !! |

CA | 24/06/2026 | 18:30 | Bank of Canada Summary of Deliberations | !! | |||

AU | 25/06/2026 | 02:30 | Employment Change | May | -- | -18.6k | !!! |

AU | 25/06/2026 | 02:30 | Household Spending MoM | May | -- | -1.1% | !! |

EC | 25/06/2026 | 09:00 | ECB Publishes Economic Bulletin | !! | |||

US | 25/06/2026 | 13:30 | Core PCE Price Index MoM | May | 0.3% | 0.2% | !!! |

US | 25/06/2026 | 13:30 | Durable Goods Orders | May P | -6.0% | 8.0% | !! |

US | 25/06/2026 | 13:30 | Initial Jobless Claims | -- | -- | !! | |

US | 25/06/2026 | 13:30 | GDP Annualized QoQ | 1Q T | 1.6% | 1.6% | !! |

US | 25/06/2026 | 20:40 | Fed's Williams Gives Keynote Remarks | !!! | |||

JN | 26/06/2026 | 00:30 | Tokyo CPI YoY | Jun | 1.6% | 1.4% | !! |

US | 26/06/2026 | 13:30 | Advance Goods Trade Balance | May | -$83.3b | -$83.0b | !! |

EC | 26/06/2026 | 14:45 | ECB's Schnabel Speaks in Germany | !! | |||

US | 26/06/2026 | 15:00 | U. of Mich. Sentiment | Jun F | -- | 48.9 | !! |

Source: Bloomberg & MUFG GMR

Key Events:

The main economic data release in the week ahead will be the latest US PCE deflator report for May. The report is likely to attract even more attention following the Fed’s hawkish policy update. New Chair Kevin Warsh has repeatedly emphasized the importance of meeting the Fed’s price stability mandate. The Fed’s preferred measure of inflation, the core PCE deflator, has picked up at the start of this year, increasing at an annualised rate of just over 4.0% between January and April, compared with around 2.8% in the second half of last year. Further evidence of stronger inflation in May would reinforce expectations that the Fed may respond by hiking rates. Fed Vice Chair Williams is also scheduled to speak next Thursday, which may offer additional insight into the likelihood of further rate hikes.

The main economic data releases in Europe will be the latest PMI surveys for the euro area and the UK for June. Business confidence may receive some support from the recent announcement of a US‑Iran agreement to end the conflict and reopen the Strait of Hormuz, although the timing of the announcement means this is more likely to be reflected in the July surveys. If sustained, lower energy prices should help to dampen stagflation risks for European economies and ease pressure on the BoE and ECB to tighten policy. However, the ECB’s recent rate hike may weigh on business confidence in the euro area. ECB officials have indicated over the past week that further tightening could still be required, even as energy prices continue to ease

The political fallout from the UK by-election is likely to remain in focus in the week ahead. Andy Burnham has secured a seat in Parliament and is expected to begin putting pressure on Prime Minister Keir Starmer to step aside. So far, Starmer has indicated that he intends to remain in office. The situation may encourage Burnham to launch a formal leadership challenge in the week ahead. He reportedly has strong support among Labour Party members and is well placed to win a leadership contest if one is triggered.