To read the full report, please download PDF.

Bullish break out for USD in anticipation of monetary policy divergence

FX View:

The USD is on course to strengthen for a second consecutive week. The bullish breakout was triggered by the Fed’s hawkish policy update, which alongside the sharp correction lower in energy prices, has reinforced expectations of monetary policy divergence. While the Fed is now seen as potentially hiking rates just as energy‑driven inflation peaks, European central banks are becoming more cautious about further tightening. The ECB’s annual policy forum in Sintra next week should provide additional insight into the policy outlook among European central banks and the Fed. A smaller and shorter‑lived energy price shock would be a positive development for the global economy, particularly for Asia and Europe, whose economies have been more heavily affected. The potential for improving cyclical momentum outside of the US later this year, combined with the Fed remaining on hold, underpins our expectation that the USD’s strength will not hold up beyond the near term. However, if we are wrong and the Fed delivers multiple rate hikes to reinforce its inflation fighting credibility, then the USD could strengthen by a further 3–5%.

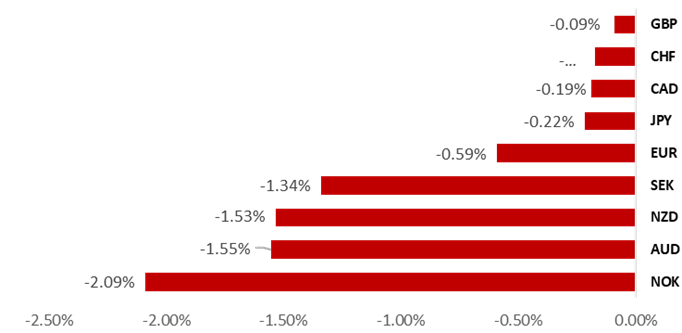

COMMODITY CURRENCIES CONTINUE TO UNDERPERFORM

Source: Bloomberg, close on 26th June 2026 (Weekly % Change vs. USD)

Trade Ideas:

We are maintaining a long USD/NOK trade idea to reflect lower energy prices and higher US rates.

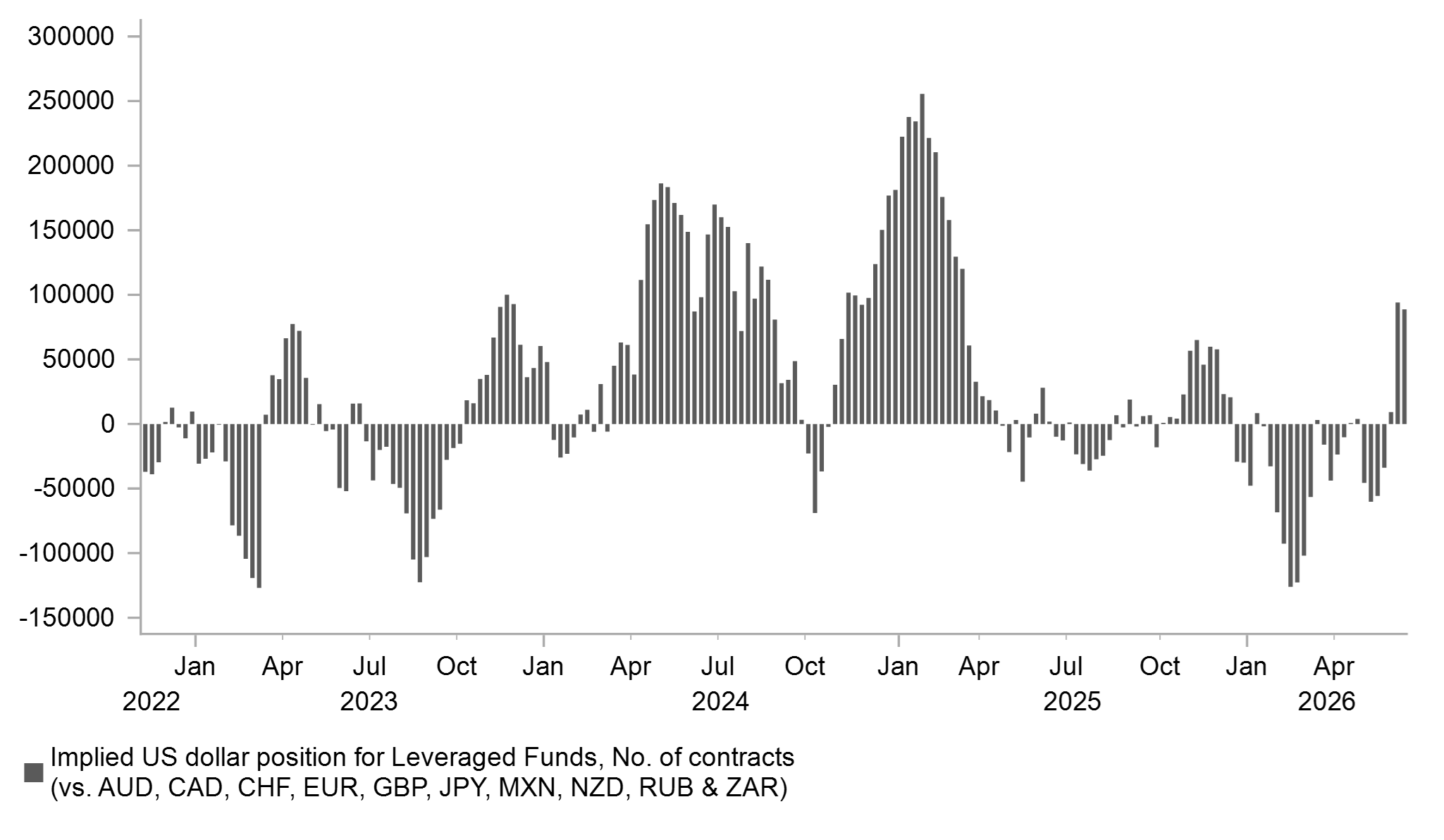

IMM FX Positioning:

Overall, total long USD positions are still less than half the levels recorded at the start of this year, leaving scope for a further build-up in the near term following the Fed’s hawkish policy update.

FX Options Flows

Our analysis of daily FX options flow data reveals a stronger conviction for further USD upside against the EUR compared to the JPY.

FX Views

USD: Diverging monetary policy expectations trigger bullish break out

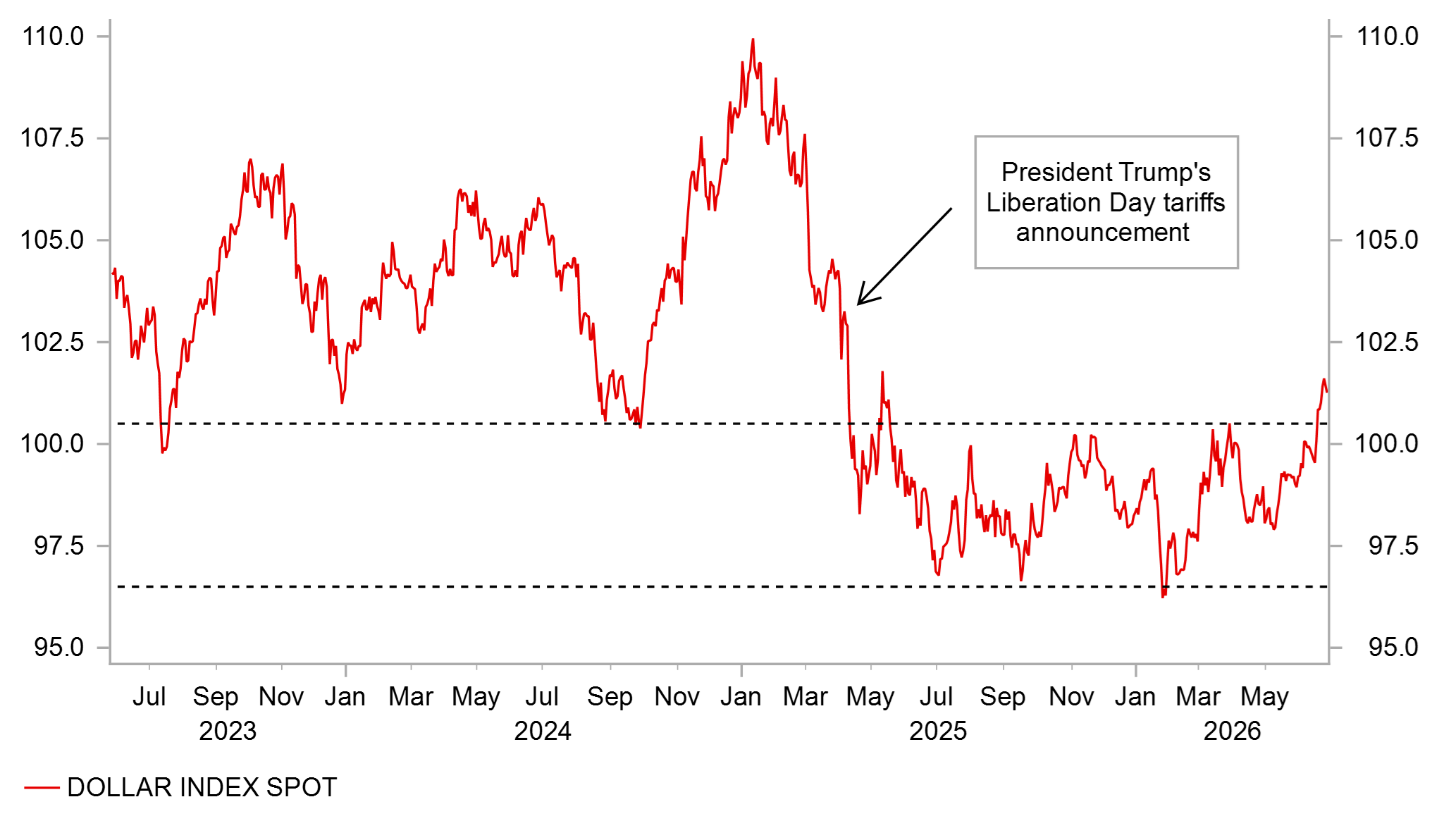

The USD is on track to record a second consecutive week of gains following last week’s hawkish Fed policy surprise. Its upward momentum has accelerated after the dollar index broke above the top of its year‑long trading range. As a result, the dollar index has moved back toward levels last seen prior to the “Liberation Day” tariffs announced by President Trump in early April 2025, around 103.00. The “Liberation Day” tariffs announcement triggered the last significant leg lower for the USD. A full reversal of those losses would suggest that the US policy uncertainty risk premium previously priced into the USD has largely been unwound. New Fed Chair Kevin Warsh’s tough stance on inflation at his first FOMC meeting has helped ease investor concerns about potential threats to the Fed’s monetary policy independence.

At the same time, Kevin Warsh’s tough rhetoric on inflation has fuelled expectations that the Fed will respond to upside risks with multiple rate hikes. This has contributed to higher US yields in recent weeks, even as energy prices have fallen sharply following the US‑Iran agreement to reopen the Strait of Hormuz. Brent crude has now fully reversed all of the gains recorded during the conflict. The scale and speed of the sell‑off have taken us and many others by surprise. If lower energy prices are sustained, the energy price shock to the global economy is likely to be smaller and shorter‑lived than previously feared. This would be a positive development in particular for Asian and European economies, which have been hit harder by the shock during the first half of the year. The prospect of improving cyclical growth momentum outside the US is one reason we continue to expect the USD to weaken heading into year‑end.

The main risk to our view is that the Fed follows through on its tough rhetoric on inflation with concrete policy action. If the Fed is serious about returning inflation to target more quickly, it would really need to deliver a series of rate hikes to restore its inflation‑fighting credibility. The PCE deflator is currently running at roughly double the Fed’s 2.0% target and has remained above target for more than five years. A tightening cycle would support a significantly stronger USD, with the dollar index potentially rising by a further 3–5%. However, we remain unconvinced that the Fed will ultimately pursue such an aggressive policy path. US inflation appears close to peaking and should moderate through the remainder of the year thereby easing pressure on the Fed to respond forcefully. We expect disinflationary pressures to build from lower energy prices and the fading effects of last year’s tariff increases. This view was echoed yesterday by New York Fed President John Williams, who stated that “the current stance of monetary policy is well positioned” to return inflation to the Fed’s 2% longer‑run target on a sustained basis. That said, he acknowledged that inflation remains “unquestionably elevated,” driven by tariffs, the energy shock stemming from the Iran conflict, and strong investment linked to the AI boom. He also noted the risk that AI‑related investment could push prices higher than expected, while ongoing supply disruptions from the Middle East conflict continue to pose risks to both growth and inflation. Williams expects inflation to ease to around 3.5% by year‑end before gradually declining toward 2.0%, reaching target in 2028. His relatively steady policy outlook contrasts with new Fed Chair Kevin Warsh’s reluctance to provide forward guidance, making it more difficult to assess the Fed’s evolving reaction function. This added uncertainty could inject greater volatility into US rates and the USD.

BULLISH BREAK OUT FOR USD

Source: Bloomberg, Macrobond & MUFG

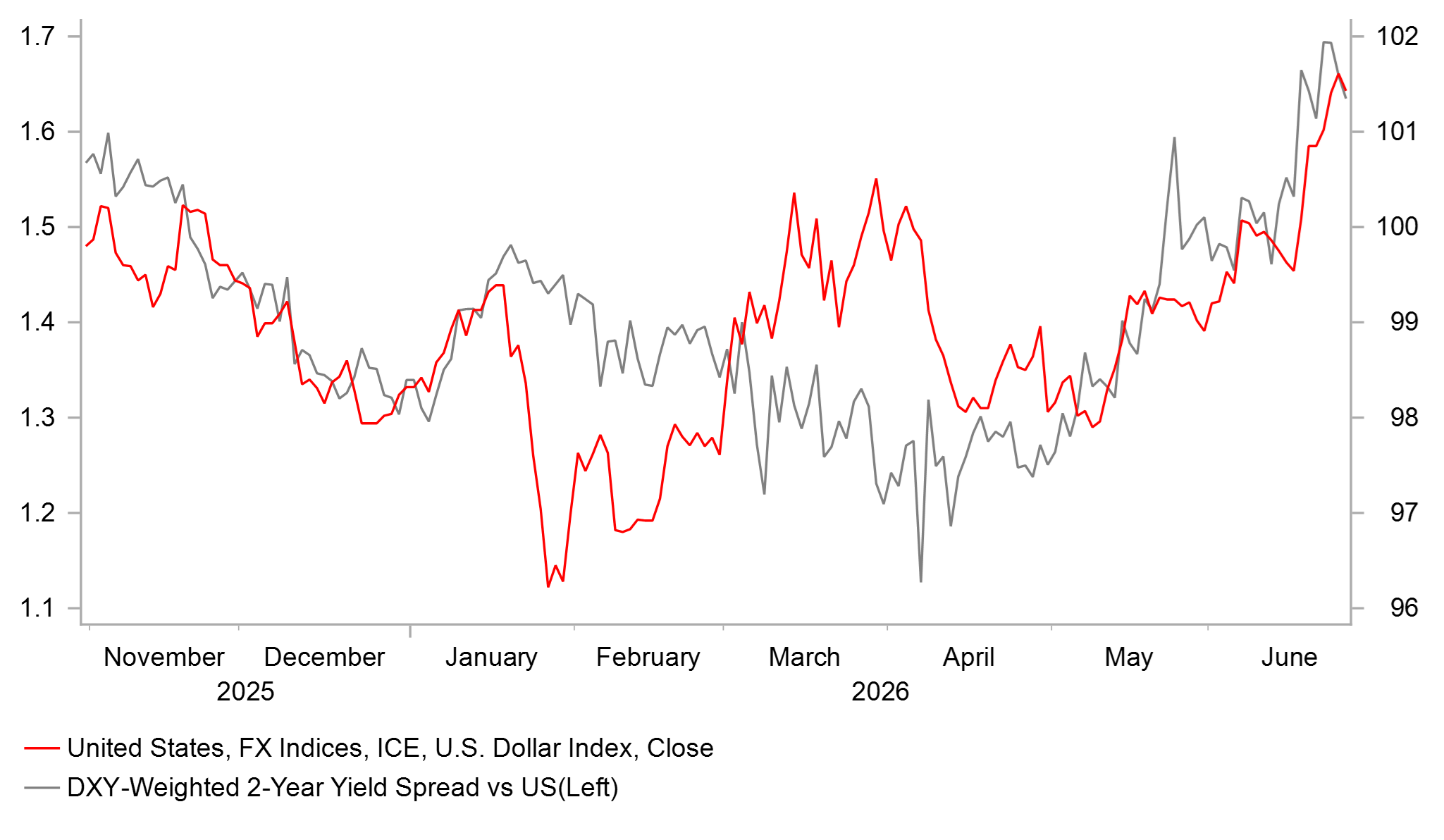

USD IS MORE TIGHTLY LINKED TO YIELD SPREADS

Source: Bloomberg, Macrobond & MUFG GMR

The USD’s upward momentum has been reinforced by diverging central bank expectations outside the US. In contrast to the recent rise in US yields, European rates have declined as markets have scaled back expectations for further monetary tightening in response to lower energy prices. A smaller and shorter‑lived energy shock is more consistent with the ECB’s milder economic scenario, reducing the need for an additional rate hike. That said, ECB officials, including Chief Economist Philip Lane, have indicated that a final 25bp hike remains on the table. He noted that the upper end of the ECB’s estimated neutral rate range has risen by 25bp to 2.50%, leaving scope for further tightening. He also highlighted that “a range of forward‑looking indicators points to continued inflationary pressures in the coming months.” For now, we maintain our forecast for a September hike, while acknowledging the growing risk that the ECB opts to keep rates on hold, which would add to near‑term headwinds for the EUR. On balance, however, we expect the positive impact of a smaller and shorter‑lived energy shock on Europe’s economy to outweigh the drag from the ECB nearing the end of its tightening cycle.

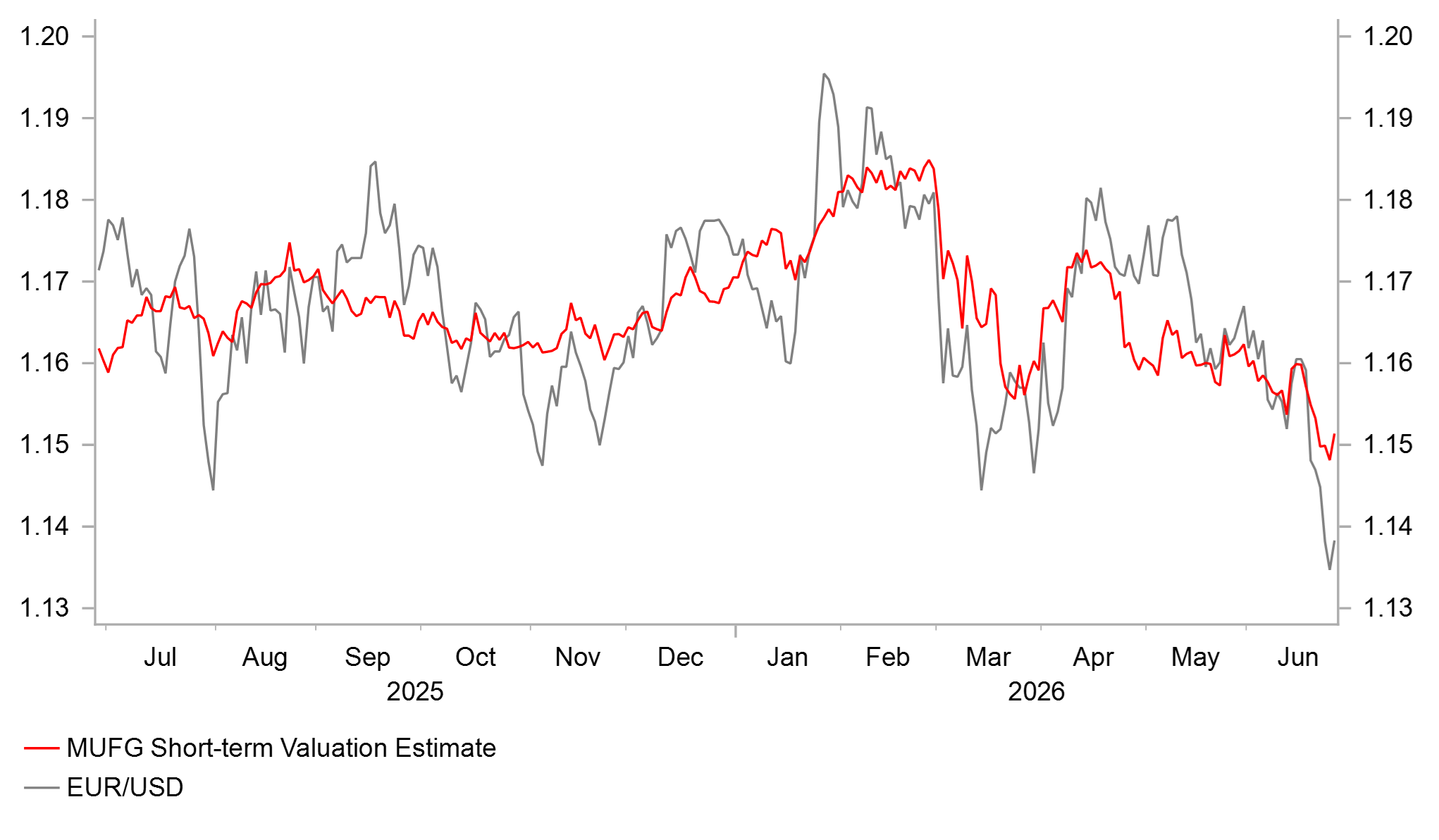

Taking all of these factors into account, we see two main scenarios for EUR/USD over the remainder of the year. In our base case, where the Fed does not follow through with rate hikes, we expect EUR/USD to move back up into the 1.1400–1.1800 range that has prevailed over the past year. Alternatively, if the Fed delivers multiple rate hikes, EUR/USD could fall further below 1.1000. Evidence of slowing US inflation and/or a less hawkish Fed reaction function would support a weaker USD, and vice versa in the months ahead. For now, we maintain our long USD/NOK trade recommendation (click here) until the recent hawkish repricing of Fed rate expectations is convincingly challenged. Looking ahead, next week’s ECB annual policy forum in Sintra should provide further insight into the extent to which monetary policy paths in Europe and the US are likely to diverge.

IS USD STRENGTH GETTING AHEAD OF ITSELF?

Source: Bloomberg, Macrobond & MUFG GMR

ROOM FOR USD LONGS TO INCREASE FURTHER

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

Ccy | Date | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

AUD | 28/06/2026 | 13:15 | RBA's Bullock Remarks | !! | |||

JPY | 29/06/2026 | 00:50 | Retail Sales MoM | May | -0.7% | 2.1% | !! |

EUR | 29/06/2026 | 18:30 | ECB's Lagarde Speaks in Sintra | !!! | |||

JPY | 30/06/2026 | 00:50 | Industrial Production MoM | May P | -0.3% | 0.5% | !! |

AUD | 30/06/2026 | 02:30 | RBA Minutes of June Policy Meeting | !! | |||

GBP | 30/06/2026 | 07:00 | GDP QoQ | 1Q F | 0.6% | 0.6% | !! |

CHF | 30/06/2026 | 08:00 | KOF Leading Indicator | Jun | -- | 98.0 | !! |

EUR | 30/06/2026 | 08:55 | Germany Unemployment Rate SA | Jun | -- | 6.3% | !! |

EUR | 30/06/2026 | 13:00 | Germany CPI YoY | Jun P | -- | 2.6% | !!! |

CAD | 30/06/2026 | 13:30 | GDP MoM | Apr | -- | -0.1% | !! |

USD | 30/06/2026 | 14:00 | S&P Cotality CS 20-City MoM SA | Apr | -- | -0.2% | !! |

USD | 30/06/2026 | 15:00 | Conf. Board Consumer Confidence | Jun | 94.2 | 93.1 | !! |

USD | 30/06/2026 | 15:00 | JOLTS Job Openings | May | 7360k | 7618k | !! |

JPY | 01/07/2026 | 00:50 | Tankan Large Mfg Index | 2Q | 16.0 | 17.0 | !! |

EUR | 01/07/2026 | 09:00 | S&P Eurozone Manufacturing PMI | Jun F | -- | 51.3 | !! |

GBP | 01/07/2026 | 09:30 | S&P UK Manufacturing PMI | Jun F | -- | 53.1 | !! |

EUR | 01/07/2026 | 10:00 | CPI Estimate YoY | Jun P | -- | 3.2% | !!! |

USD | 01/07/2026 | 13:15 | ADP Employment Change | Jun | 110k | 122k | !! |

EUR | 01/07/2026 | 14:30 | Fed's Warsh Speaks | !!! | |||

USD | 01/07/2026 | 15:00 | ISM Manufacturing | Jun | 53.8 | 54.0 | !! |

CHF | 02/07/2026 | 07:30 | CPI YoY | Jun | 0.2% | 0.6% | !! |

GBP | 02/07/2026 | 09:30 | BoE Credit Conditions Survey | !! | |||

EUR | 02/07/2026 | 10:00 | Unemployment Rate | May | -- | 6.3% | !! |

USD | 02/07/2026 | 13:30 | Change in Nonfarm Payrolls | Jun | 130k | 172k | !!! |

USD | 02/07/2026 | 13:30 | Unemployment Rate | Jun | 4.3% | 4.3% | !!! |

USD | 02/07/2026 | 15:00 | Durable Goods Orders | May F | -- | -- | !! |

EUR | 03/07/2026 | 09:00 | S&P Global Eurozone Services PMI | Jun F | -- | 48.9 | !! |

GBP | 03/07/2026 | 09:30 | S&P Global UK Services PMI | Jun F | -- | 48.7 | !! |

Source: Bloomberg & MUFG GMR

Key Events:

There is a busy schedule of central bank speakers in the week ahead. The ECB will hold its annual policy conference in Sintra, Portugal, under the theme “Shaping Europe’s future: innovation, growth and stability.” Policy sessions and panel discussions will focus on growth and productivity in Europe, including the impact of AI. The programme will feature a panel discussion on Wednesday involving ECB President Lagarde, Fed Chair Warsh, BoE Governor Bailey, and BoC Governor Macklem. Comments from Fed Chair Warsh will be scrutinised closely for any further insights into his views on monetary policy, although he is expected to avoid providing forward guidance. He has previously expressed optimism that the adoption of AI will boost productivity growth and generate disinflationary pressures in the US economy.

The main economic data release in the week ahead will be the latest US nonfarm payrolls report for June. Employment growth has picked up strongly in recent months, expanding by an average of 188k per month in the three months to May. This follows average job losses of 8k per month in the second half of last year. The sharp turnaround in hiring has helped to ease concerns over downside risks to the US labour market, although recent monthly readings likely overstate the underlying trend, with employment growth expected to slow to around 130k in May. At the same time, the unemployment rate has remained steady and earnings growth has slowed, providing reassurance that labour market conditions are not tightening significantly or requiring further Fed rate hikes.

In the UK, Prime Minister-in-waiting Andy Burnham is expected to make an important speech in the week ahead outlining his views on economic and fiscal policy. The exact date and timing of the speech have not yet been confirmed, so it has not been included in the calendar above. The speech should provide greater clarity on the policy changes he is likely to pursue if he becomes the next leader of the Labour Party. He is expected to reiterate his intention to adhere to the government’s fiscal rules, limiting the scope for a shift towards looser fiscal policy. However, there may still be efforts to boost defence spending and long-term capital investment by adjusting the fiscal framework, for example by separating capital expenditure from day-to-day spending.