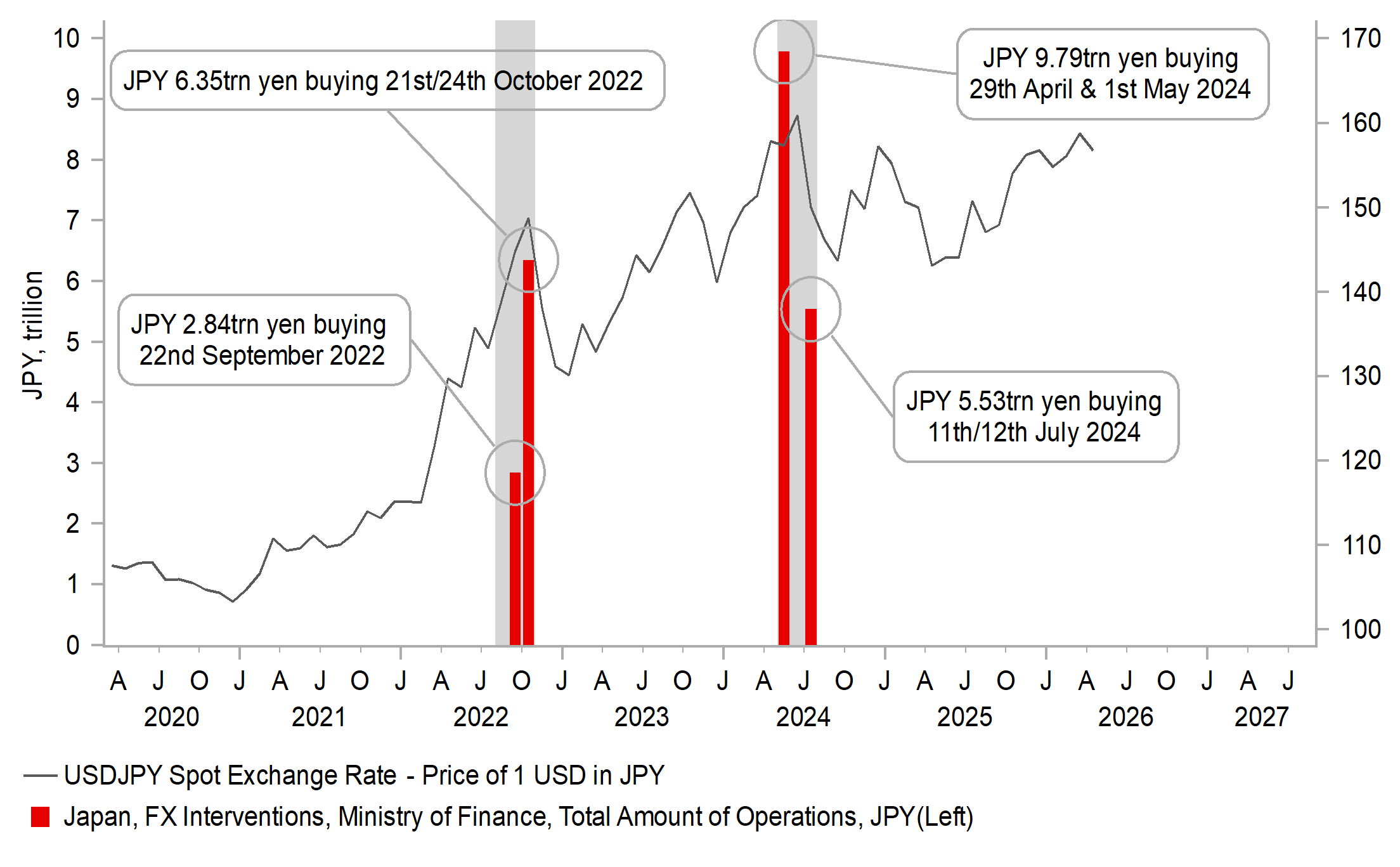

Intervention underlines tolerance threshold for yen weakness unchanged

JPY: JPY downside limited for now – action buys time

Yesterday we had the most explicit and strongest warning from the Vice Finance Minister for International Affairs, Atsushi Mimura, who gave a “final warning” over yen selling and the sudden and sharp drop in USD/JPY that followed was certainly indicative of intervention by the BoJ on behalf of the MoF. The five-big figure drop in USD/JPY is far too big a move on just rhetoric and the report from the Nikkei that intervention took place points strongly to intervention.

Mimura cited signs of speculative selling of the yen in his warnings yesterday and will no doubt be cited as the justification for intervention. He has warned today that speculative selling is still being seen. Under the G20 remit agreed, a divergence in FX from fundamentals is a justification for intervention and hence speculative selling can be cited as a justifiable excuse. But there is no getting away from the obvious point that the action coincided with a move above the 160-level to a high that was last recorded in July 2024 when the MoF last intervened. So protecting the 160-level looks a much more plausible trigger for the action than speculative selling. This action does at least buy the BoJ some time and is helpful politically for the government to be seen curtailing yen depreciation given the increased Japanese household concerns over the cost of living. The timing was also convenient in coming at month-end and hence the details, like the size of intervention, will not be known until the MoF at the end of May reports its intervention activities to the markets. Vice Finance Minister Mimura today refused to confirm whether intervention took place.

Is the mention of speculative yen selling as a factor backed up by any data? There is certainly some evidence, but the evidence is not as compelling as when intervention last took place in July 2024. OTC margin retail FX positioning is monthly data but there was a pick-up in selling in March. The short yen position across all currencies increased to the largest size since July 2024 when intervention last took place. However, yen shorts versus the US dollar did not change – it was versus the Australian dollar and pound. Secondly, IMM data does show a pick-up across Asset Managers, Institutional Investors and Leveraged Funds combined but the current size is less than halve the total from July 2024.

What this intervention does is provide some time for the BoJ to assess the uncertainties related to the conflict in the Middle East. There was an understandable reluctance to hike this week due to the lack of clarity and that reluctance coupled with the Fed being more hawkish opened up scope for a de-stabilising yen sell-off, possibly next week when Japan will be on vacation for Golden Week – Monday through Wednesday next week is a Japan holiday. But with yen shorts not as extensive as in past intervention episodes there is a danger that this action does not have a lasting impact. An escalation in the conflict and/or a further rise in energy prices could see USD/JPY rebound quickly. MoF yen-buying intervention in Oct 2022 and July 2024 were successful for a period as the action coincided with or was soon followed by a decline in US yields. At the time of the intervention in Apr/May 2024 US yields did not decline and intervention was required again by July. There is a risk that this intervention could be like the Apr/May 2024 episode given global yields are currently moving higher.

JPY BUYING INTERVENTION HAS FAILED TO TURN JPY STRONGER

Source: Bloomberg, Macrobond & MUFG GMR

EUR & GBP: Rate hikes are coming

Yesterday we released two FX focuses on the BoE and ECB policy meetings (here & here) and it was clear to us that without a dramatic reversal in energy prices between now and the June meetings, both the BoE and the ECB will be hiking rates. Yields in Europe and the UK declined yesterday in part reflecting the fact that market pricing had nearly fully captured rate hikes ahead. Crude oil prices declined modestly yesterday, and US yields were lower also. There may have been some relief in the UK that the vote for a hike was only 8-1 – there could easily have been a larger number looking for a hike. Nonetheless, the scenarios laid out by the BoE all included lifting the key policy rate that underlines the increasing prospect of action.

The lone dissenter – Huw Pill, the Chief Economist – will speak today at 12:15 BST and will no doubt lay out the reason why he thinks action is necessary given the risk stemming from second-round effects. Pill sees upside inflation risks in all three scenarios laid out by the BoE yesterday and argues for a hike to reduce the “re-emergence of intrinsic inflation persistence”. Between two and three rate hikes are now priced for the UK which feels about right to us – we have raised our forecast for this year from one hike to two following yesterday’s BoE meeting. Pricing remains somewhat short for June – with only a little over a 50% chance of a hike priced. The lower probability likely reflects the fact that only Pill voted for a hike yesterday and there was no explicit hint of an imminent hike. Nearly all MPC members gave greatest probability to Scenario B that would not require much tightening and indeed Bailey yesterday suggested a lot of tightening has already taken place given the rates market has moved from pricing cuts to now pricing hikes. However, we still see scope for the required shift in numbers voting for a hike in June if energy prices remain elevated.

An ECB hike in June is much more priced and that reflects the more explicit guidance suggesting a move. President Lagarde confirmed that the Governing Council “debated at length, and in depth” a decision to hike in June and Lagarde added that six weeks would be the right amount of time “in order to make an informed decision”. The BoE is already running a restrictive monetary stance while the ECB is at around neutral and in that regard, it is understandable to expect the ECB to be more willing to act. There was little yesterday to suggest much in the way of policy divergence between the ECB and the BoE and hence, EUR/GBP range trading looks set to continue. The risk though would be scope for EUR/GBP to drift higher with ECB’s signalling of a near-term rate hike that bit stronger.

THE STOCK OF CRUDE OIL ON WATER IS DIMINISHING INDICATING INCREASED RISKS OF PRICE SURGE

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

UK |

09:30 |

Manufacturing PMI |

(Apr) |

53.6 |

51.0 |

!!! |

|

UK |

09:30 |

Mortgage Approvals |

(Mar) |

60.00K |

62.58K |

! |

|

UK |

09:30 |

BoE Consumer Credit |

(Mar) |

1.800B |

1.935B |

! |

|

UK |

09:30 |

Mortgage Lending |

(Mar) |

4.20B |

4.84B |

! |

|

UK |

09:30 |

M4 Money Supply (MoM) |

(Mar) |

0.5% |

0.6% |

! |

|

UK |

12:15 |

BoE MPC Member Pill Speaks |

- |

- |

- |

!!!! |

|

CA |

14:30 |

Manufacturing PMI |

(Apr) |

- |

50.0 |

! |

|

US |

14:45 |

Manufacturing PMI |

(Apr) |

54.0 |

54.0 |

!! |

|

US |

15:00 |

ISM Manufacturing PMI |

(Apr) |

53.1 |

52.7 |

!!! |

|

US |

15:00 |

ISM Manufacturing Employment |

(Apr) |

49.0 |

48.7 |

!! |

|

US |

15:00 |

ISM Manufacturing Prices |

(Apr) |

80.0 |

78.3 |

!!! |

Source: Bloomberg & Investing.com