The ECB is set to leave rates unchanged next week, with officials showing little urgency for a back-to-back hike. The statement is likely to retain the usual emphasis on flexibility, but Lagarde may feel more comfortable hinting that further tightening is on the cards after the collapse of the US-Iran deal and the renewed rise in energy prices. The June meeting account already pointed to an implicit tightening bias, with additional rate hikes embedded in the ECB’s baseline projections.

Our base case remains one further 25bp hike in September, supported by fresh staff projections, which would take the deposit rate to 2.50%. Beyond that, the bar for additional tightening looks higher. Policymakers will likely require clearer signs of second-round inflation pass-through, which have been in limited supply thus far. On that basis, we continue to expect a ‘measured adjustment’ rather than a fully-fledged tightening cycle.

The ECB appears content to defer the decision on further tightening until September

Renewed energy risks strengthen the case for further tightening later this year

The ECB is set to leave rates unchanged at its July meeting with markets pricing only a few basis points of tightening next week. Despite the re-escalation in the Middle East and the subsequent rise in crude oil prices, even the hawks have stopped short of making a case that this is a live policy meeting. Joachim Nagel, president of the Bundesbank, said yesterday that rates are currently at an “appropriate” level.

Indeed, there is some sense of balance coming into this meeting. The US-Iran deal was signed soon after the ECB’s June hike and prompted a retracement in energy prices. That was followed by a soft euro area inflation print for June with the headline rate slowing from 3.2% to 2.8%, leaving the Q2 average 0.2pp below the ECB’s projection. These developments put the hawks on the back foot. But any reservations about the justification for the June hike have likely diminished considerably now after the US-Iran deal has effectively collapsed and energy prices rebounded. It is hard to argue that the decision was a mistake.

This all means that officials are likely to be more comfortable striking a somewhat more hawkish tone than would have been the case a few weeks ago. The statement will likely retain the usual flexibility (“data-dependent and meeting-by-meeting”), but we expect Lagarde will provide some hints that some further tightening is on the cards if energy pricing remains elevated. There is already an implicit tightening bias – the account of the ECB’s June meeting stated that “continued vigilance was vital, and it was important to acknowledge that further rate hikes were embedded in the baseline projections”.

In terms of the immediate decision, the case for a back-to-back move might have been stronger if the ECB had framed June as a pre-emptive hike which could be unpicked later if risks start to fade. Instead Lagarde has directly pushed back on suggestions that it was an insurance hike and stressed that it was “a good monetary policy interest rate decision” which was “robust” across all the ECB’s scenarios. Policymakers will see value in waiting for the next batch of those projections in September to validate any further tightening on the same basis.

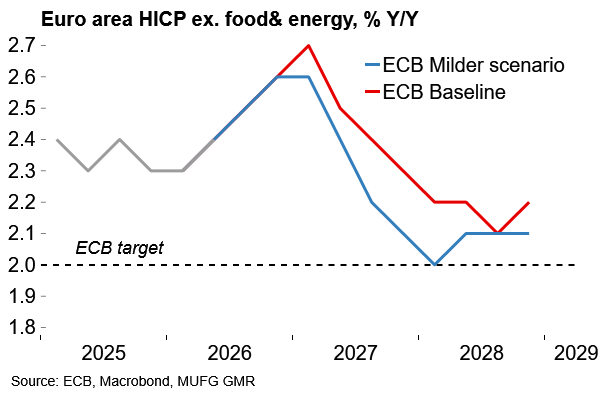

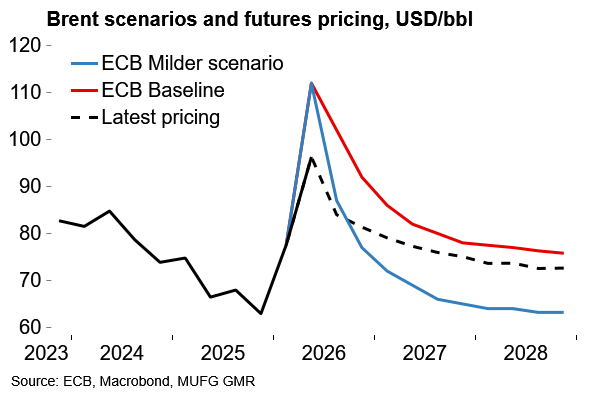

Brent is currently trading somewhere between the ECB’s Milder and Baseline scenarios from June (see chart below). Both of those scenarios showed a small but persistent overshoot in core inflation. We assume that would remain the case in the next batch of numbers. While headline inflation undershot the ECB’s June projections, the services and broader core measures were in line with expectations.

We continue to expect a hike in September, justified by persistent underlying inflation in the updated projections. That would lift the deposit rate to 2.50%, which is the upper end of the ECB’s estimated neutral range (see here). All else equal, officials would likely see that as sufficient to lean against inflation risks and would feel well-positioned to react to adverse developments. The bar for tightening beyond that mark will feel higher. We believe that policymakers will require clearer signs of second-round inflation pass-through, which has thus far been in scant supply. We continue to see the ECB undertaking a ‘measured adjustment’ with 50bp of hikes in total this year rather than a fully-fledged tightening cycle.

Energy pricing is now somewhere between the ECB’s baseline and milder scenarios from June….

…both of which showed a persistent overshoot in underlying inflation