The Philippines central bank raised its key policy rate by 25bps during its June 2026 monetary policy meeting, bringing it to 4.75% from 4.50%.

The policy statement and the comments by the BSP Governor during the press conference were modestly hawkish in our view, highlighting among other things that it stands ready to take monetary actions to guide CPI back to target, inflationary pressures remain strong, and measured policy action will complement fiscal actions.

From a policy rate perspective, we continue to see BSP hiking rates twice more this year for a total of 50bps, with the rate at 5.25% by end-2026.

Just as importantly for FX and rates markets, we are forecasting BSP to reverse its rate hikes in 2027 starting 1Q2027 once we get greater confidence on a moderation in year-on-year headline inflation, with the policy rate likely to end 2027 at 4.50%. These forecasts assume oil prices remain contained, and the US-Iran deal holds through 2027.

From an FX perspective, we are opting to keep our current baseline forecast for USD/PHP to trade between the 60.00 to 61.50 range for now. Net-net, we expect USD/PHP to move lower towards 60.00 by 2Q2027 after weighing the balance of risks of different factors.

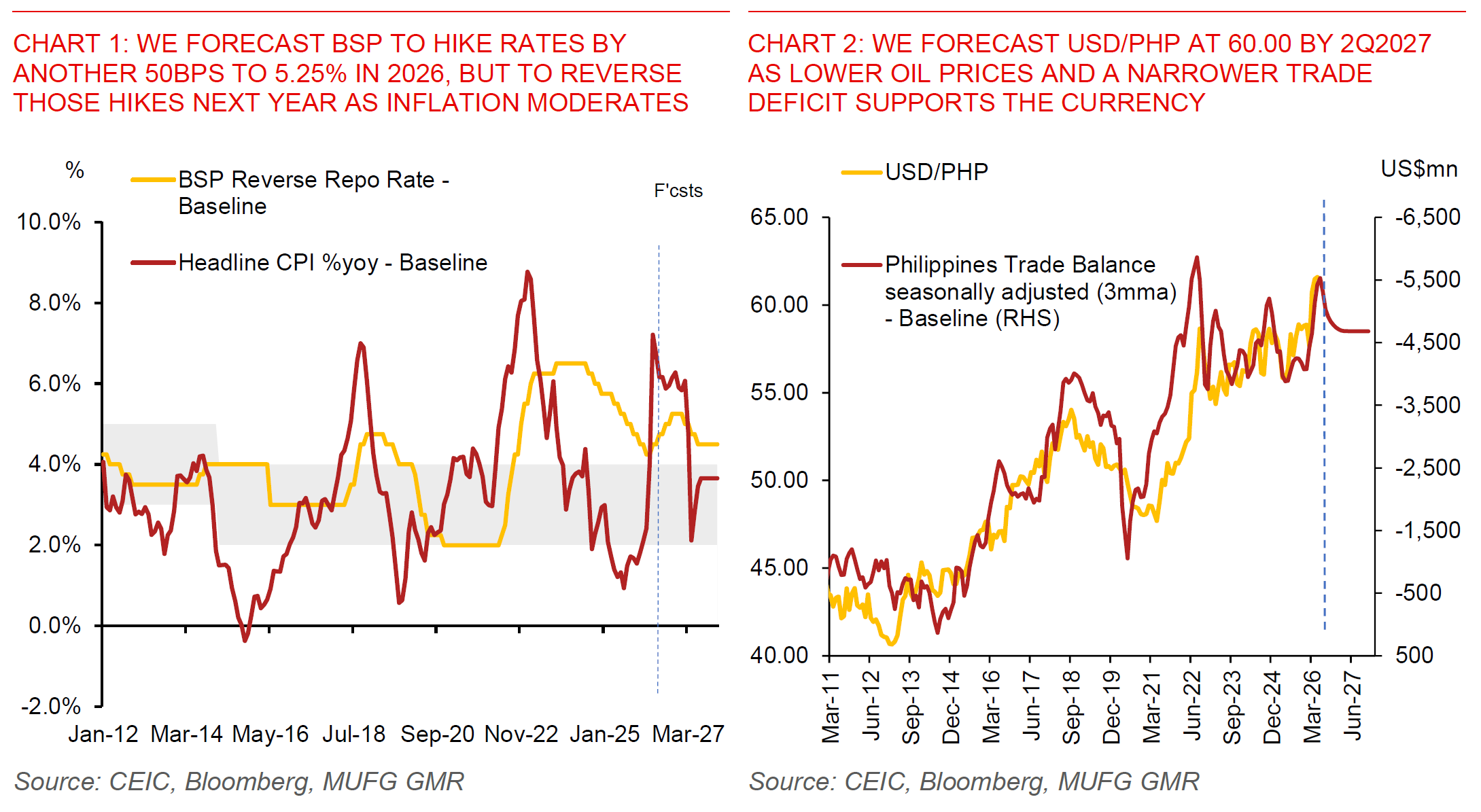

From a rates perspective, we see some value starting to emerge in Philippines local currency bonds given how much PH yields have already spiked and how much the curve has already bear flattened. We are forecasting PH 10-year local bond yields to move gradually lower towards the 6.70% levels by 2Q2027 from current 7.00%, but bigger moves in the PH rates market would likely need more clarity on the path of inflation, how the El Nino effect and food prices will pan out this year, and also clarity on the path of US Treasury yields.

More details:

Overall, we think the Philippines Peso should be supported by a narrower trade deficit given lower oil prices and the US-Iran deal, the hawkishness from the BSP and our expectation for further BSP rate hikes, coupled with the nascent pick-up in Philippines government spending over the past few months which if continued should help boost sentiment.

There are however two major sources of uncertainty moving forward which make us hesitant to chase USD/PHP lower given current levels, even as it still makes sense to expect PHP to strengthen against the Dollar over time after weighing the balance of factors and risks.

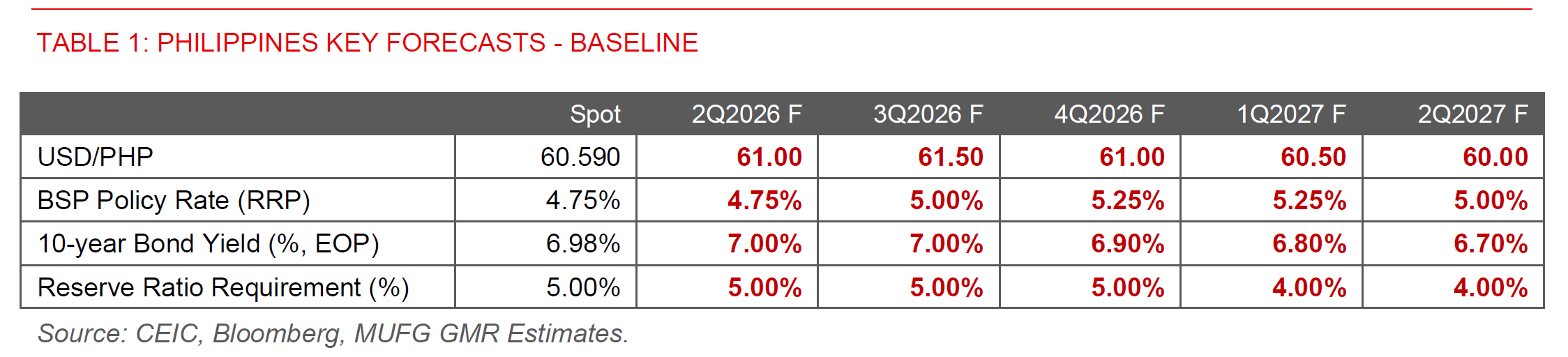

The first key uncertainty is to what extent the Fed will turn more hawkish through 2026 under new Fed Chair Kevin Warsh, the Fed’s possible rethinking of its balance sheet policy, and what these collectively imply for US short-end rates and US 10-year Treasury yields.

In our model of USD/PHP, interbank rate differentials between the US and the Philippines and US 10-year yields are key drivers of the FX pair, together with other factors such as the trade deficit, sovereign CDS spreads, domestic rice prices and government spending (see Philippines - Strait of Hormuz: Impact of higher oil prices). In particular, our model estimates that every 25bps increase in PH-US interbank rate differentials strengthens the Philippines peso by 1.2% and every 10bps increase in US 10-year yields weakens PHP by 0.1%. For PHP given how salient changes in US rate expectations can be, USD/PHP may be affected more so than other Asia and G10 FX pairs by these shifts.

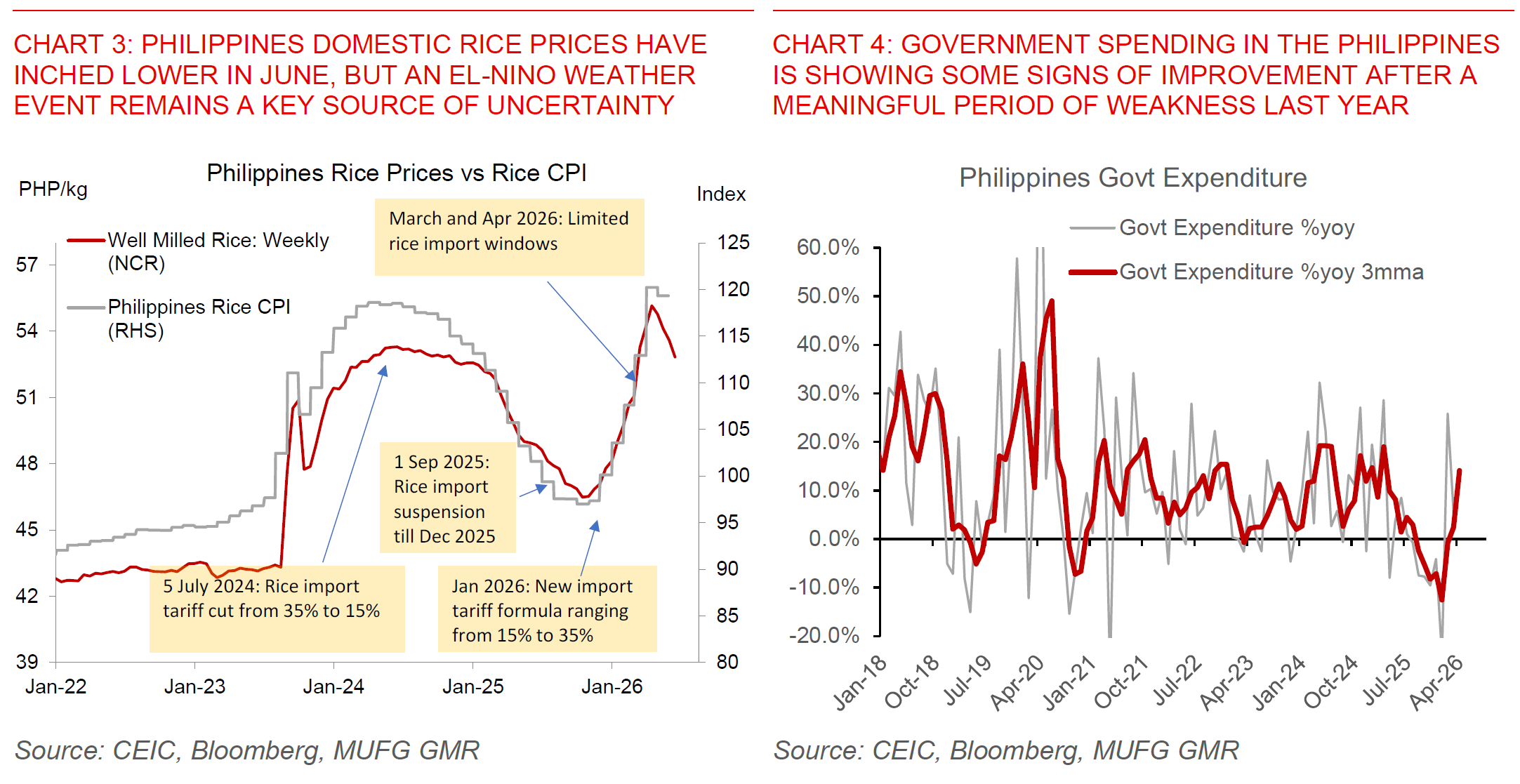

The second key source of uncertainty is a possible “Super-El Nino” event and what that could imply for domestic food prices including rice. It looks quite likely that we will have an El-Nino event this year, with the key question being the strength of the weather phenomenon. Domestic rice prices have inched lower in June based on latest numbers, but there are upside risks to global rice prices given the current weakness in India’s Southwest Monsoon. The good news is that food inventory buffers including in India are still quite high, but this is not to say that things will not change if global weather patterns turn for the worse over the next few months.

Overall, we forecast USD/PHP moving towards the 60.000 levels by 2Q2027 in our baseline expectations after weighing the balance of risks.