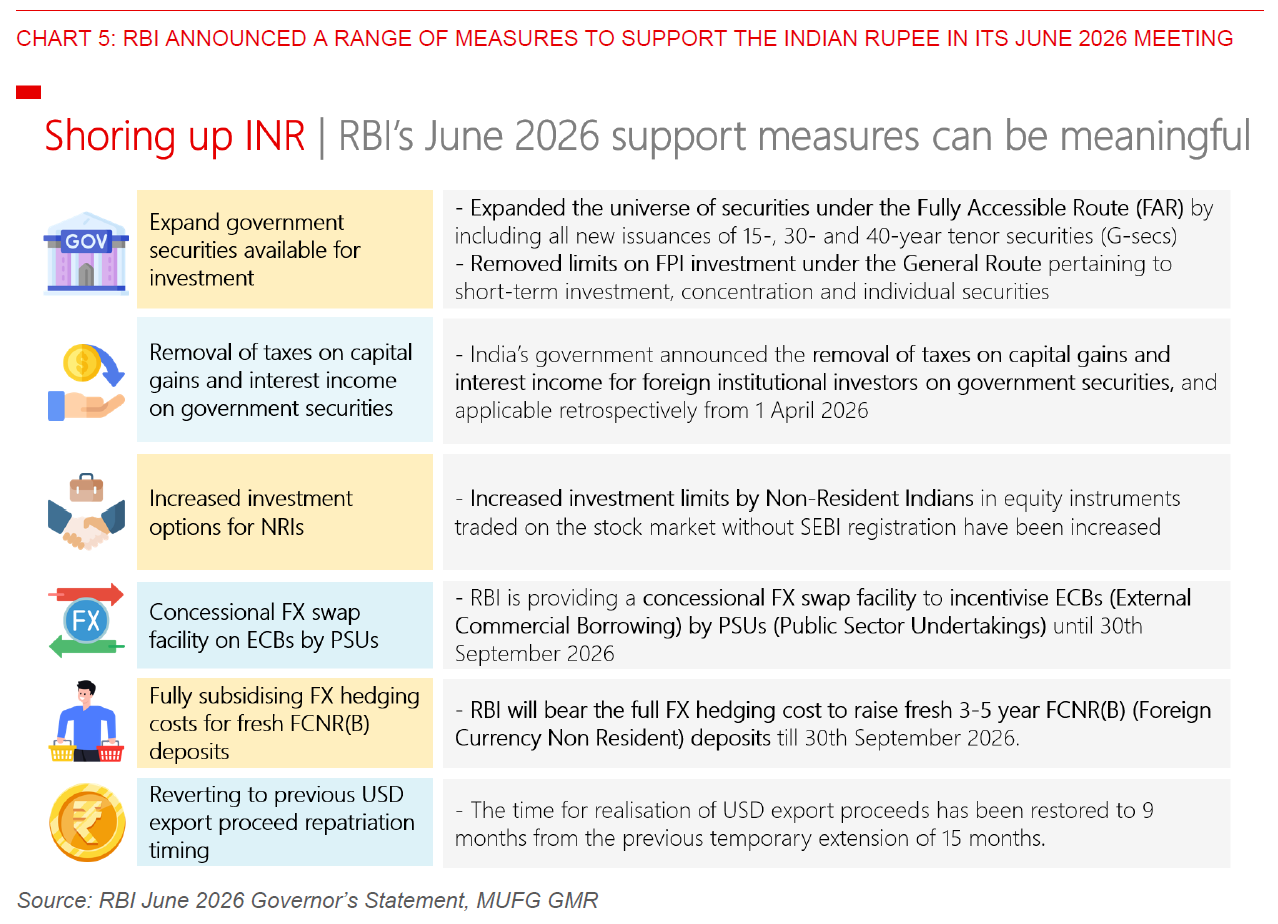

RBI announced a slew of measures to help shore up the Indian Rupee during its 5 June 2026 monetary policy meeting. These policies include RBI fully subsidising the FX hedging costs of banks raising fresh 3-5 year FCNR(B) deposits and a concessional FX swap facility to incentivise the raising of ECBs by state-owned enterprises (PSUs). In addition, the government has removed taxes on capital gains and interest on government securities for foreign investors, applied retrospectively from 1 April 2026, while expanding the list of government securities available for investment (more details in full report).

While we were already expecting some of these policies to be announced, in totality they were more than we were building into our INR FX and rates forecasts (see India – A Perfect Storm?).

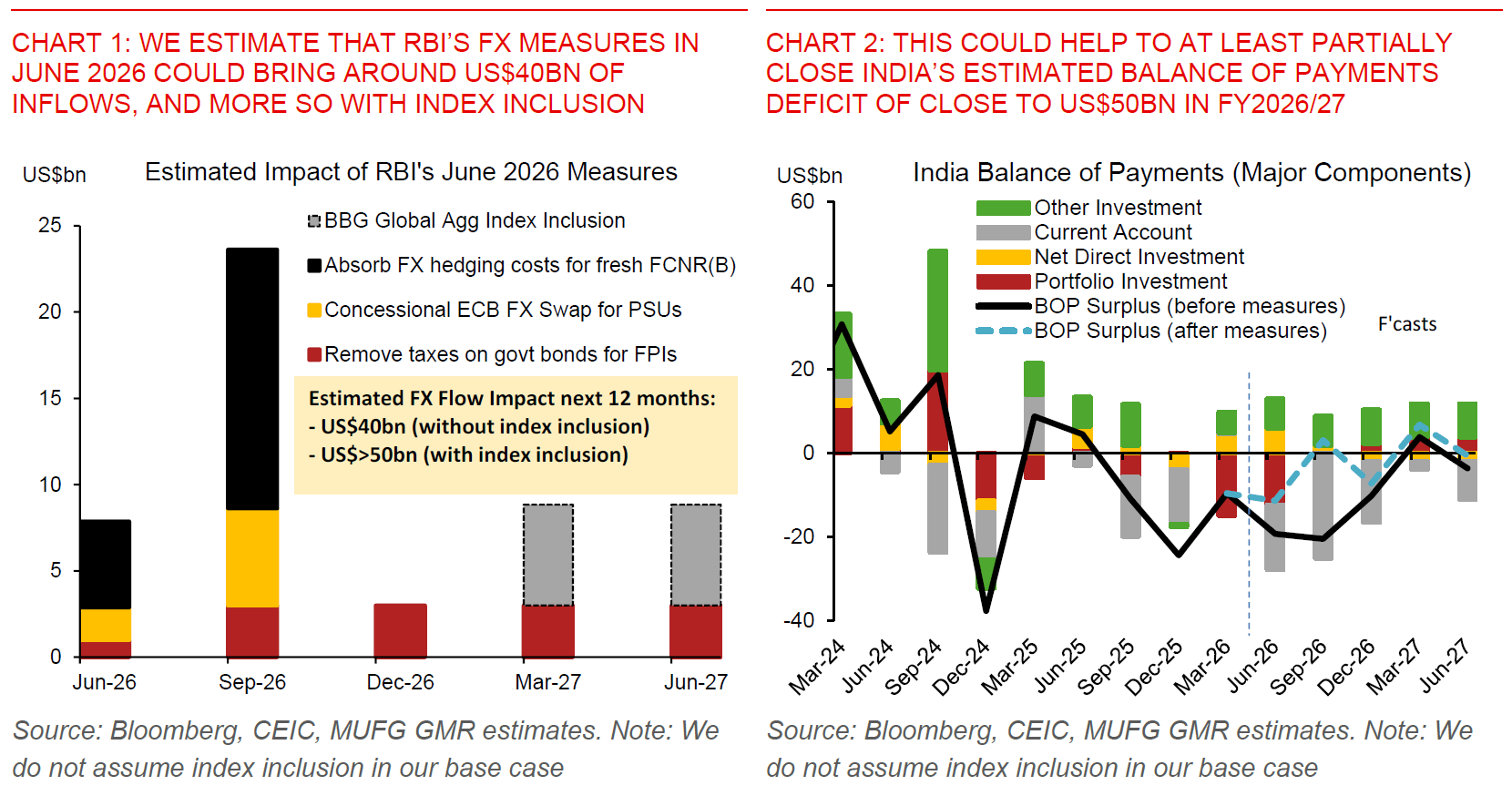

Net-net our preliminary estimates suggest that there could be around US$40bn of inflows from these policies, and more so if India were to be included in the Bloomberg Global Agg Index as an indirect result.

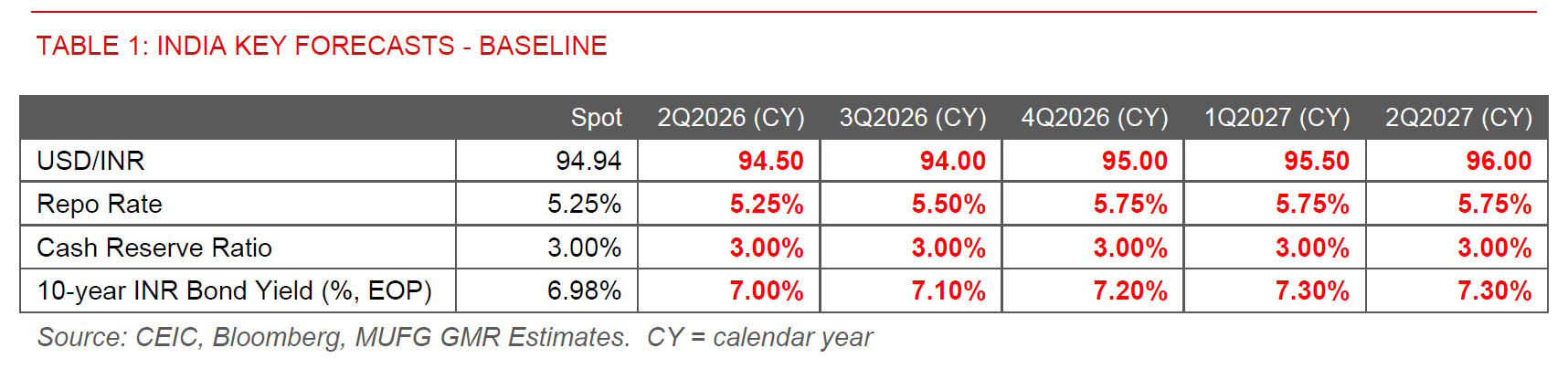

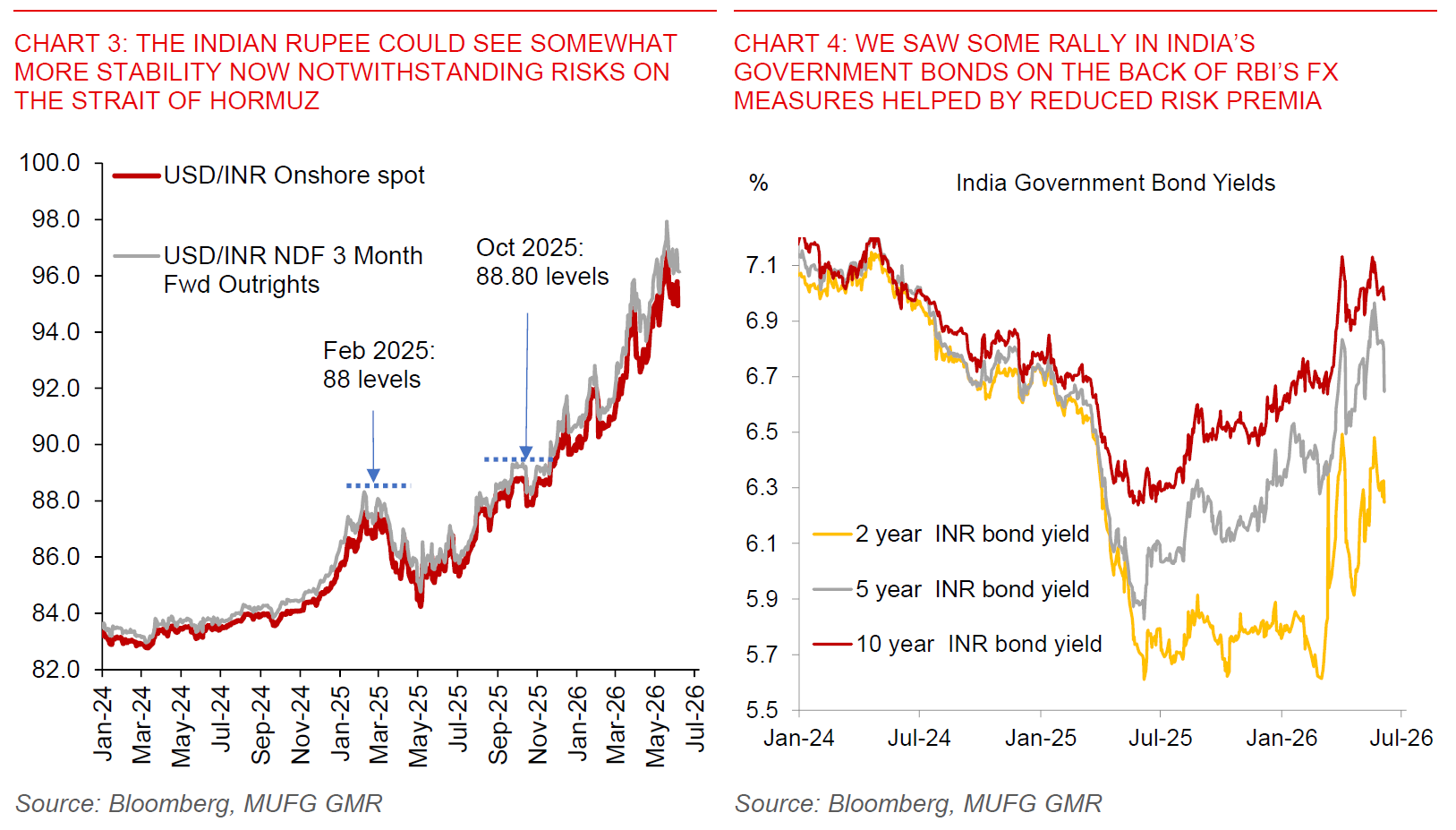

We tentatively adjust our forecasts for INR stronger near-term and see USD/INR at 94.00 by the September quarter before rebounding towards the 96.00 handle in the next calendar year.

From a rates perspective, we continue to see 50bps of hikes by RBI as our base case, bringing the repo rate to 5.75% from 5.25% currently.

We think the broader macro environment still implies yields in India heading higher rather than lower over time, even as these measures should help reduce some risk premia embedded in the broader interest rate structure. Net-net we forecast 10-year INR yields rising towards 7.30% from 6.98%.

From a strategy perspective, we prefer more relative value FX plays rather than USD/INR outright at this time, both because of the uncertainty around the US rates trend right now and also the impact of these INR FX measures.

Going long CNH/INR (or long SGD/INR) on dips should still work given our constructive view on the Chinese Renminbi and CNY’s greater resilience against US yields in today’s environment. On the flipside going long INR against currencies more vulnerable to higher US yields such as IDR may also work – while accounting for common influences if US yields were to decline.

On rates perspective, we are biased to pay INR rates on dips and don’t quite want to chase any declines in INR rates, in part because of the current uncertainty around US yields. We think some modest bear flattening in the INR 2s10s yield curve should make sense given our view that the RBI will deliver rate hikes with terminal rates closer to 5.75% from 5.25% currently.

Shoring up the Indian Rupee

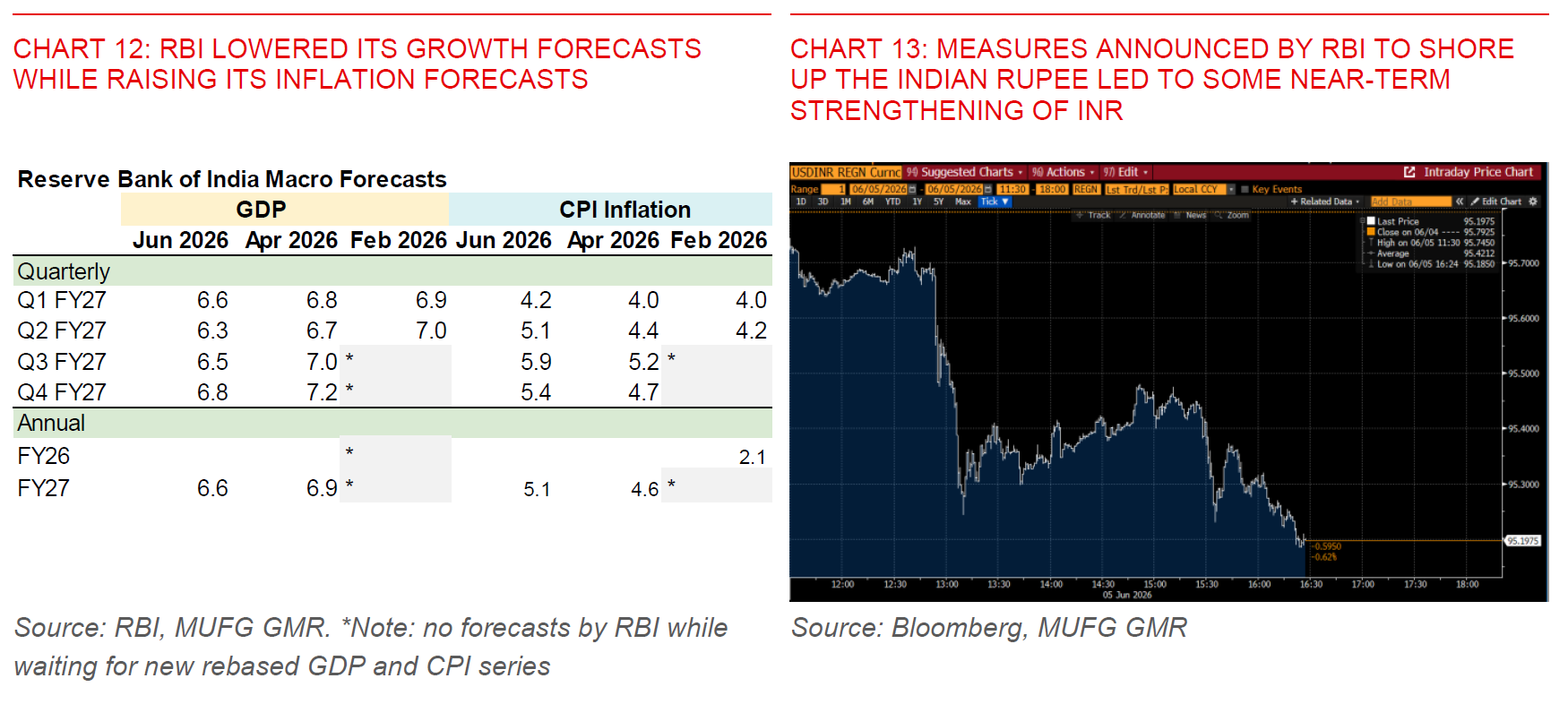

The Reserve Bank of India kept its key repo rate on hold at 5.25% in its 5th June 2026 meeting, and kept a neutral stance on monetary policy. This was in line with the consensus, but was against our view for a 25bps rate hike.

More importantly, RBI announced a slew of measures to help shore up the Indian Rupee, and the timing also seemed to be coordinated together with the government (see Chart 5 below):

First, RBI expanded the universe of securities under the Fully Accessible Route (FAR) by including all new issuances of 15-, 30- and 40-year tenor G-secs. At the same time, India’s government also announced the removal of capital gains and interest income taxes for foreign institutional investors, and retrospectively from 1 April 2026.

Second, investment limits by Non-Resident Indians in equity instruments traded on the stock market without SEBI registration have been increased.

Third, the RBI is providing a concessional FX swap facility until 30th September 2026 to incentivize External Commercial Borrowings (ECBs) by Public Sector Undertakings (PSUs).

Fourth, the RBI will bear the full FX hedging cost for authorised banks to raise fresh 3-5 year FCNR (B) deposits till 30th September 2026.

Fifth, the time for realisation of USD export proceeds has been restored to nine months from the previous temporary extension of 15 months.

In particular, we see the measures to fully subsidise FX hedging costs for FCNR(B) deposits, and importantly the removal of taxes on government bonds for FPIs as having the greatest potential impact for the Indian Rupee.

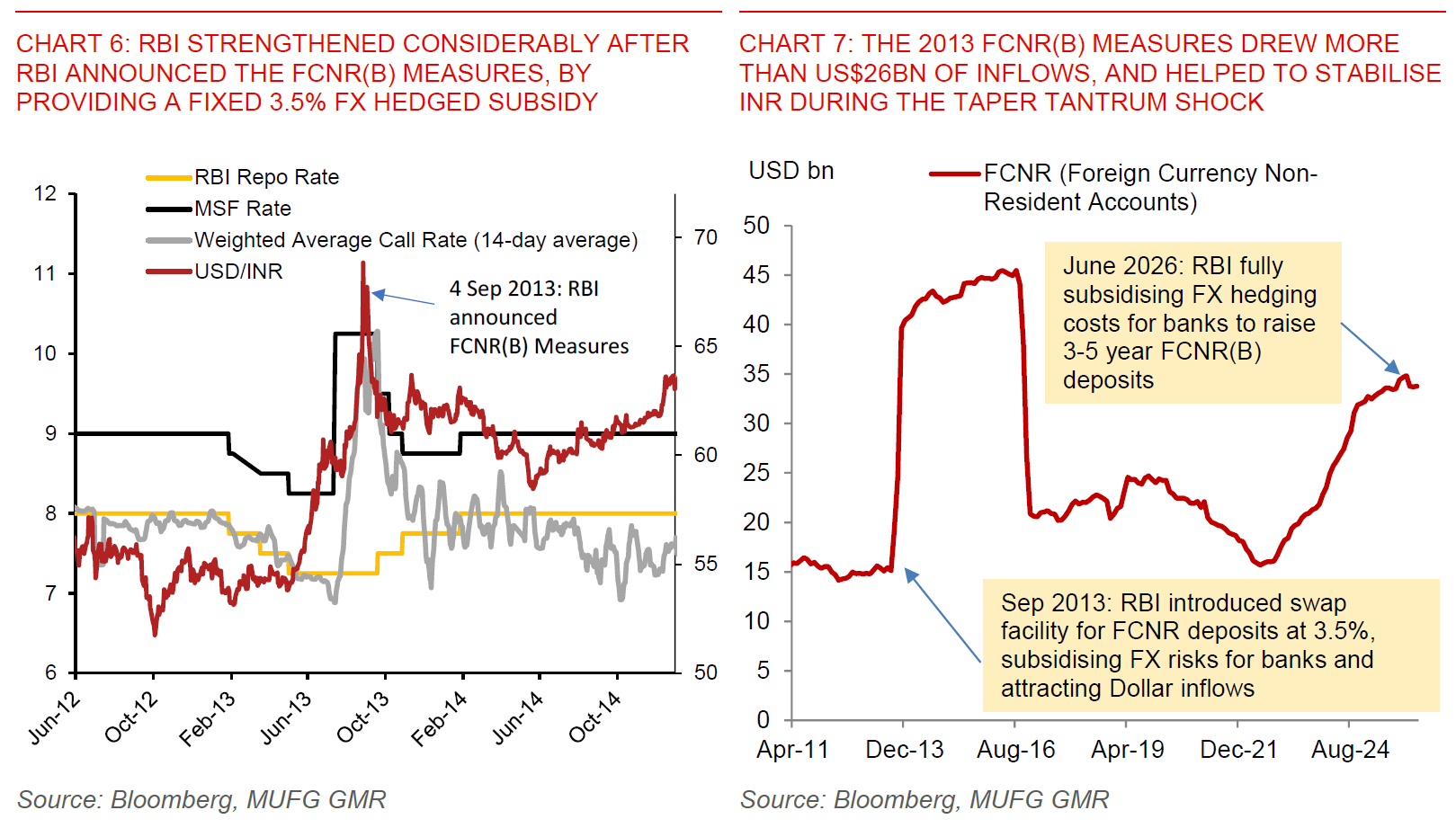

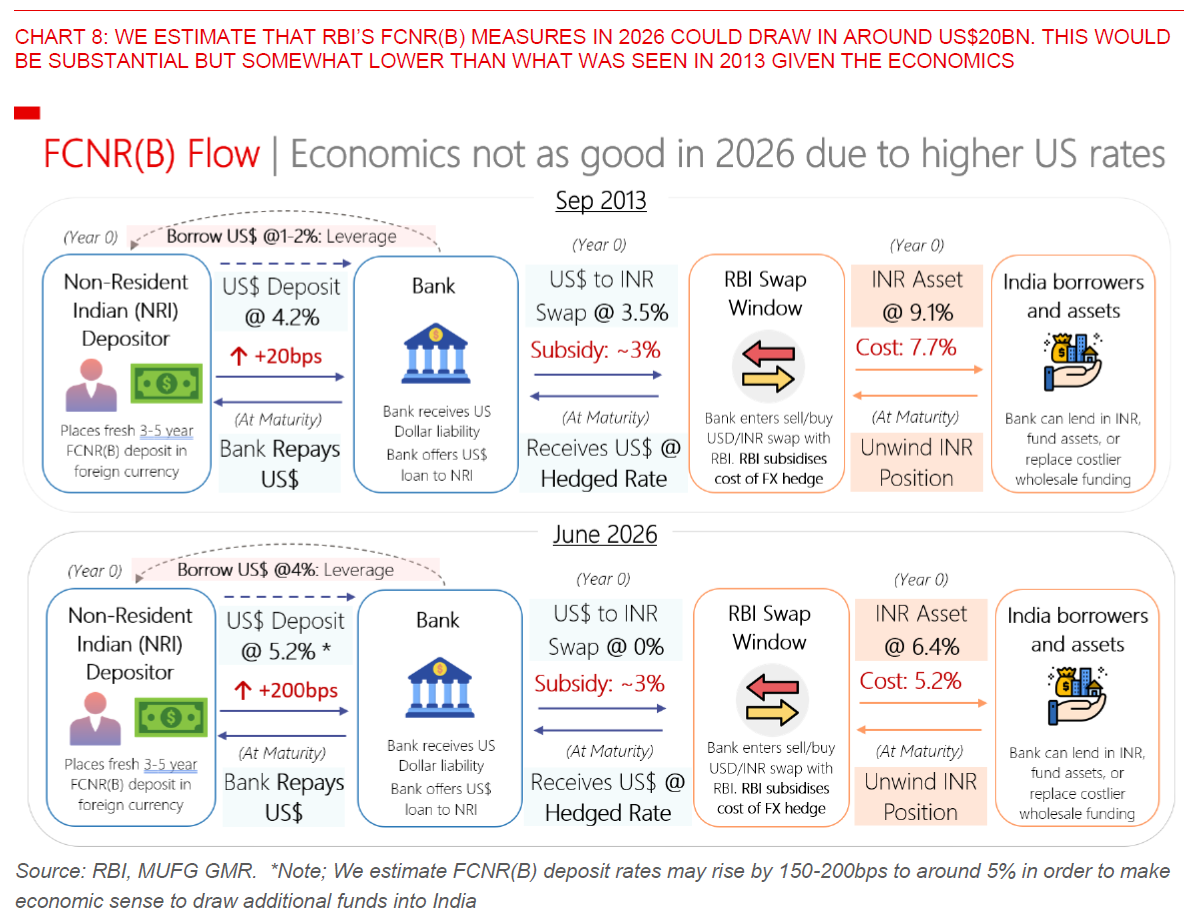

For context, the FCNR(B) measure was a key measure that was announced under RBI on 4 Sep 2013, under then new RBI Governor Raghuram Rajan. This policy subsidised FX hedging costs for banks to raise fresh Foreign Currency Non-Resident funds, drawing in US$26bn from this policy alone, and close to US$34bn from a combination of other measures as well (see Charts 6 and 7).

This measure worked very well back in 2013 due to two key factors. 1st, RBI’s FX hedge subsidy at 3.5% fixed (around 3% discount to prevailing market rates) significantly increased the incentives for banks to raise US Dollar funds from Non-Resident Indians, while investing domestically to earn a spread. 2nd Low US short-end interest rates in 2013 (~1-2%), and relatively high India yields (~9%) increased the incentives for banks and NRIs to borrow to leverage up to benefit from this spread, while importantly taking no FX risks due to RBI’s subsidy.

In today’s context, RBI has now offered to fully subsidise the FX hedging costs for fresh 3-5 year FCNR(B) deposits till 30 September 2026. This implies around a 3% discount to prevailing FX swap rates of 2.8% to 3.3% for the 3-5 year tenor.

With no FX hedge cost, we think the incentive for banks and NRIs to bring in additional US$ funds makes sense today for the FCNR(B).

Nonetheless, with short-end US rates much higher today (~4%) and longer-end INR yields relatively lower (~6.4% for 5-year), we think the economics is less attractive relative to 2013. This is both because FCNR(B) rates have to rise sufficiently to compensate for higher US dollar deposit rates, and also because borrowing to leverage up makes less sense given the higher cost of funds both for banks and for NRIs (see Chart 8 for an illustration).

As a base case, we are pencilling in US$20bn of funds coming in through this route. While this is substantial, the eventual quantum of funds may be lower than what we saw in 2013 in our view based on our preliminary assessment.

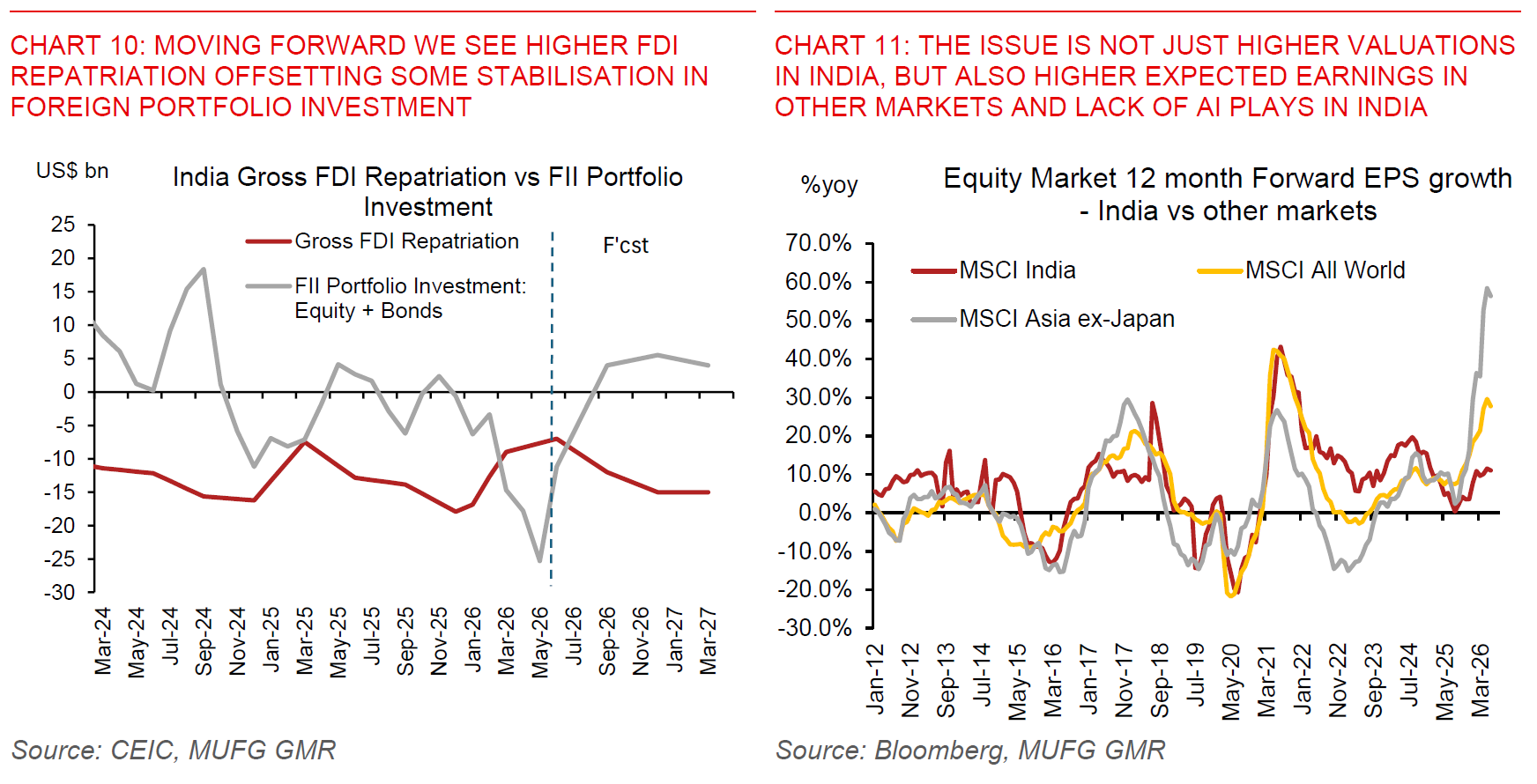

The removal of taxes on capital gains and interest income on government bonds for foreign investors is also meaningful in our view as a long-term reform measure, and will go a long way to help ease the burden of investing in India’s government bond market which has been a perennial issue. This is crucial not just because of the direct impact to flows, but also through the potential indirect impact were India to be included in the Bloomberg Global Aggregate Index. We estimate that additional flows of around US$15-20bn are quite likely with inclusion depending on the eventual weighting for index inclusion, but timing wise we think it’ll likely be 1H2027 at the earliest notwithstanding some front-running by active funds.

With the combined impact of these measures from RBI’s policy meeting, we are now somewhat less negative on the Indian Rupee than we were before, and are less confident that INR will underperform moving forward (see India – A Perfect Storm?)

These policies may bring around US$40bn of inflows in totality in FY2026/27, and more than US$50bn of flows expected if India were to be included in the BBG Global Agg Index as an indirect result.

The inflows could as such help to at least partially close the estimated balance of payments deficit of around US$50bn for FY2026/27.

INR remains under pressure from FDI repatriation and capital outflows

While India’s FX measures can help plug India’s balance of payments deficit for the time being and buy some time, we continue to think that the Indian Rupee remains under pressure given a meaningful change in the underlying FX flows.

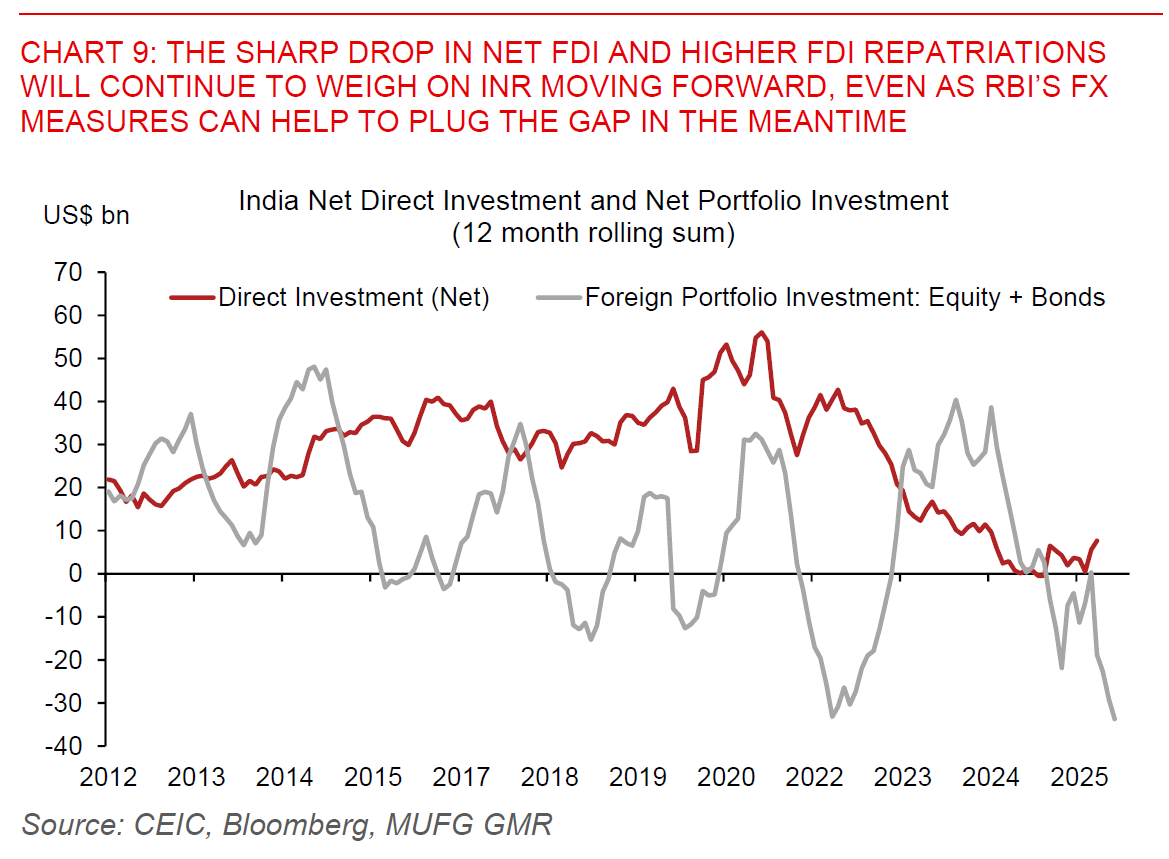

As we wrote about in our flagship thematic report published earlier this year, the sharp decline in India’s net FDI from +US$40bn a few years ago to close to zero right now implies a sizeable hole in India’s balance of payments that needs to be filled by other means (see India: Flows before growth – this time is different for INR).

The details suggest that high gross FDI repatriation is one key driver behind these elevated outflows and more than offsetting gross inward FDI, and reflecting PE/VC funds taking profits on existing investments given they had invested previously at much lower valuations.

This in turn is driven fundamentally by: 1) high valuations in India vis-à-vis other countries, 2) far higher relative earnings expectations in other markets, and 3) lack of AI plays in India and with some arguing that AI is a marginal net-negative for the whole economy given the possible impact to IT services.

With a strong pipeline of IPOs continuing we see gross FDI repatriation outflows from India remaining high moving forward (see India: Flows before growth – this time is different for INR). While we have seen a near-term slowdown in FDI repatriation given the more uncertain market environment, portfolio investors have significantly pared down their exposure into India’s equity market. Our expectation moving forward is that although we may see some stabilisation in the equity market and with that portfolio inflows, FDI repatriation will pick-up speed moving forward and continue to be an important drag on the Indian Rupee.