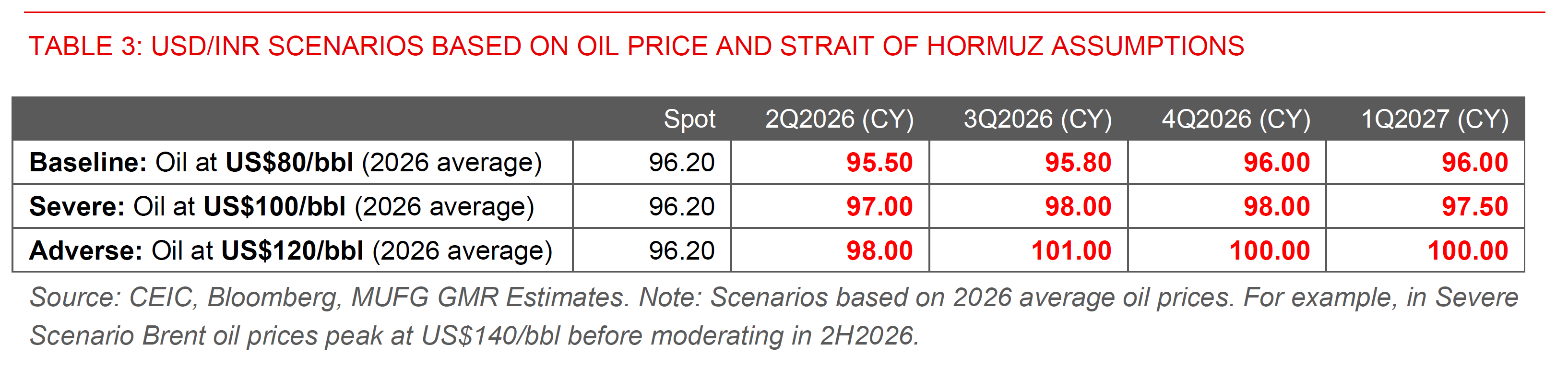

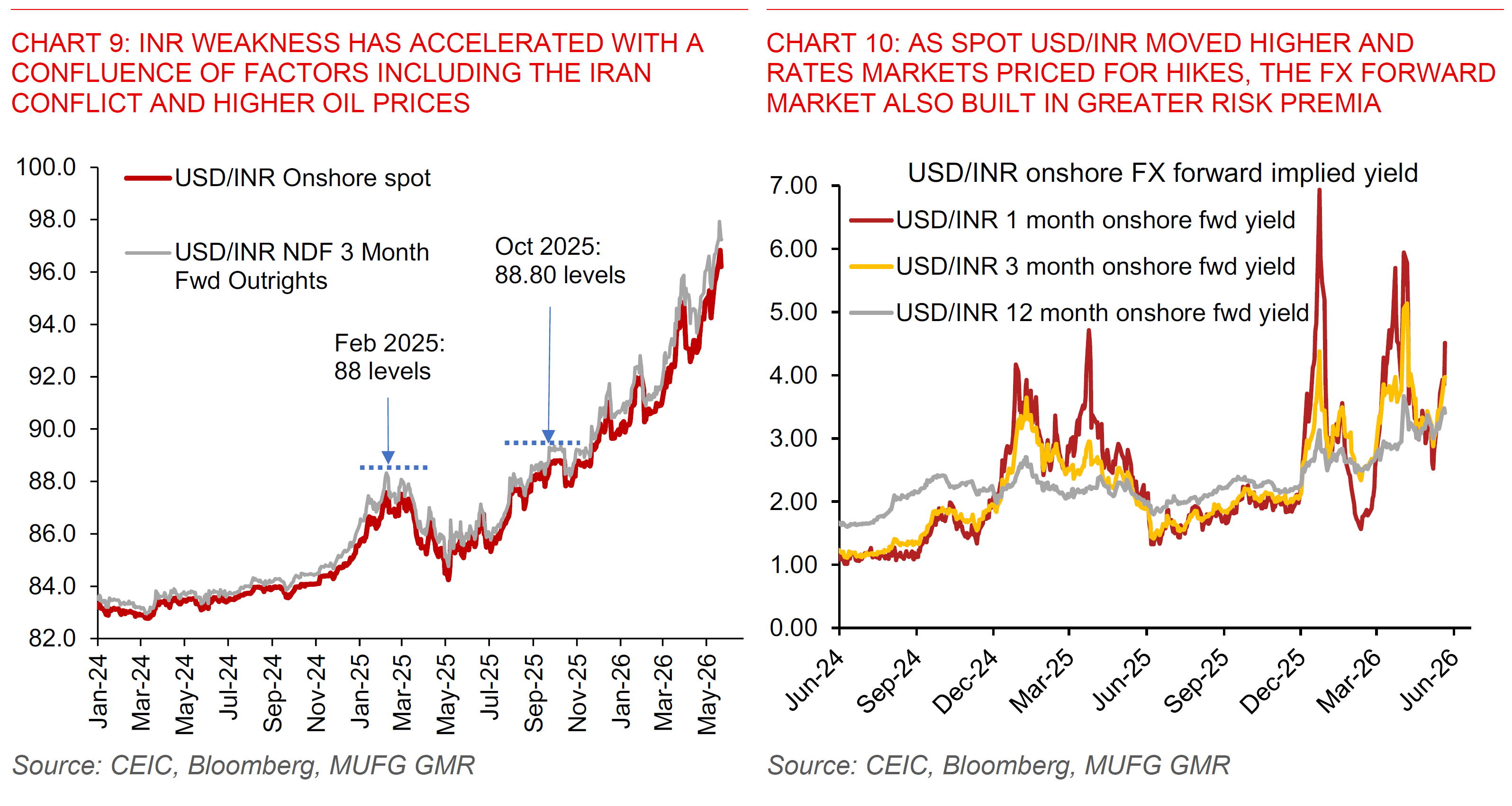

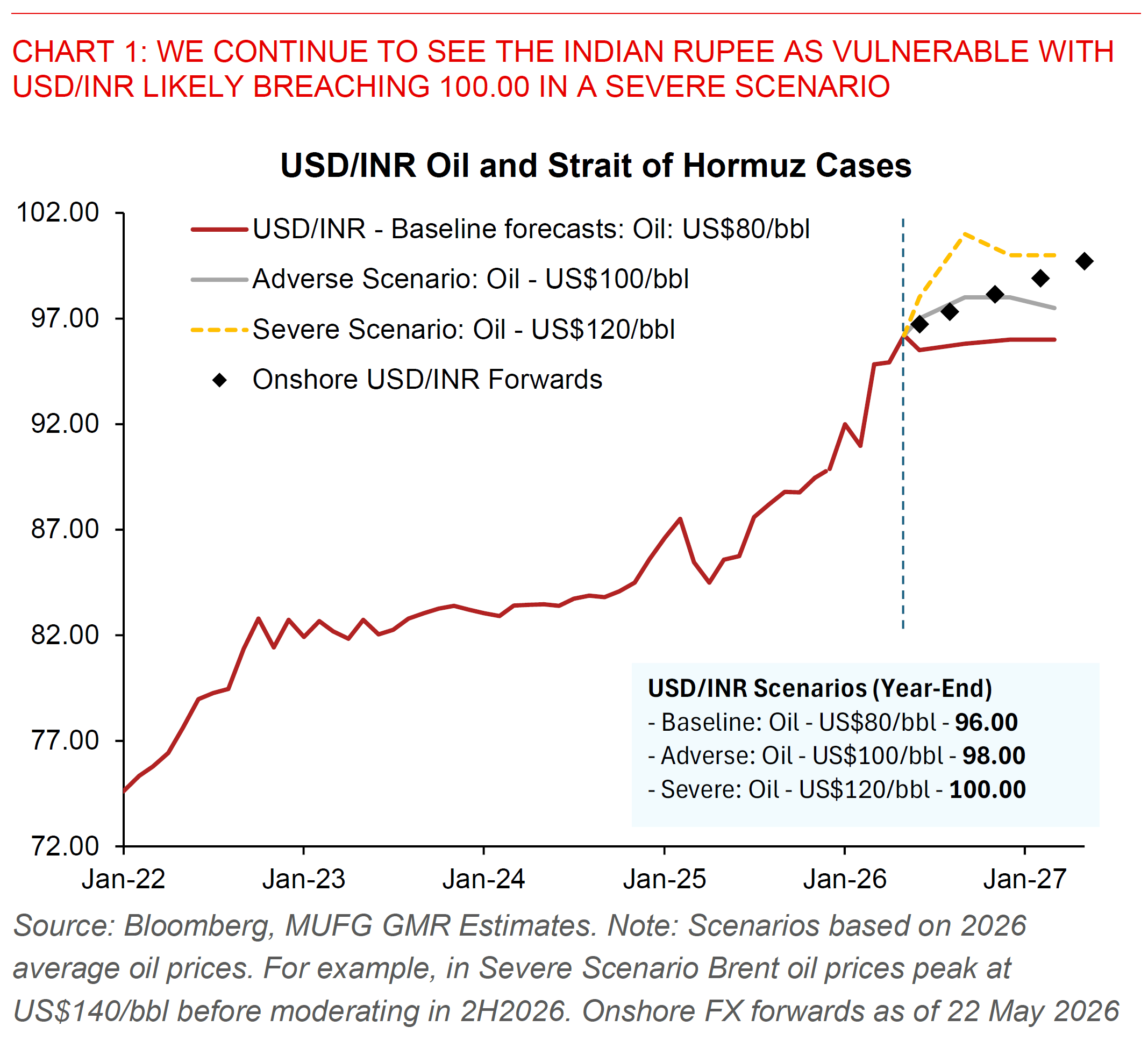

We continue to view the Indian Rupee as vulnerable across a range of scenarios on the Strait of Hormuz, with USD/INR likely moving towards 98.00 levels and even 100.00 is in sight if the conflict prolongs or escalates.

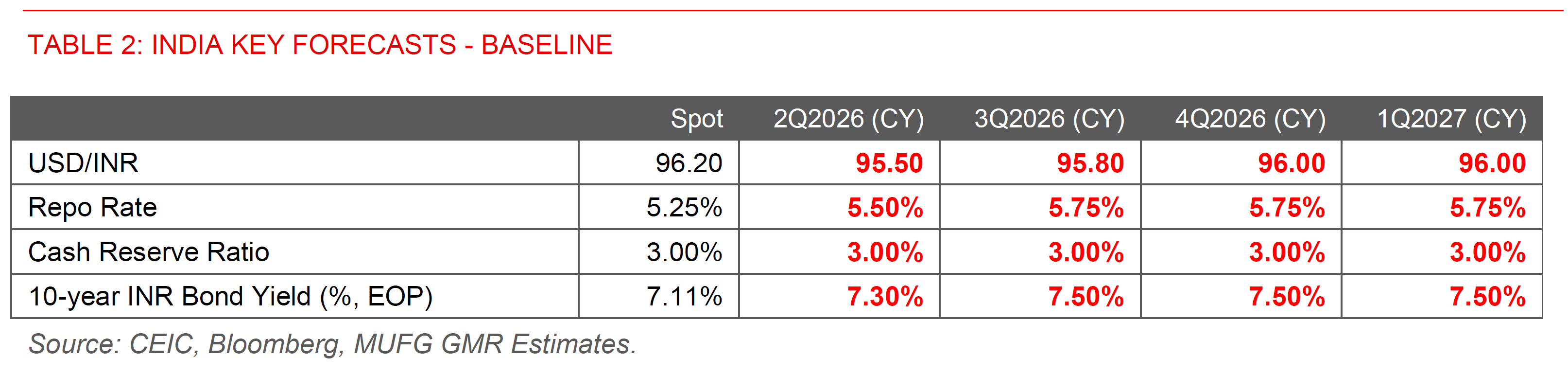

Our expectation assumes a de-escalation and over here our baseline forecasts for USD/INR to trade between 95.00 to 96.00 implies INR weakening further against Asia and G10 FX including EUR, JPY and CNH.

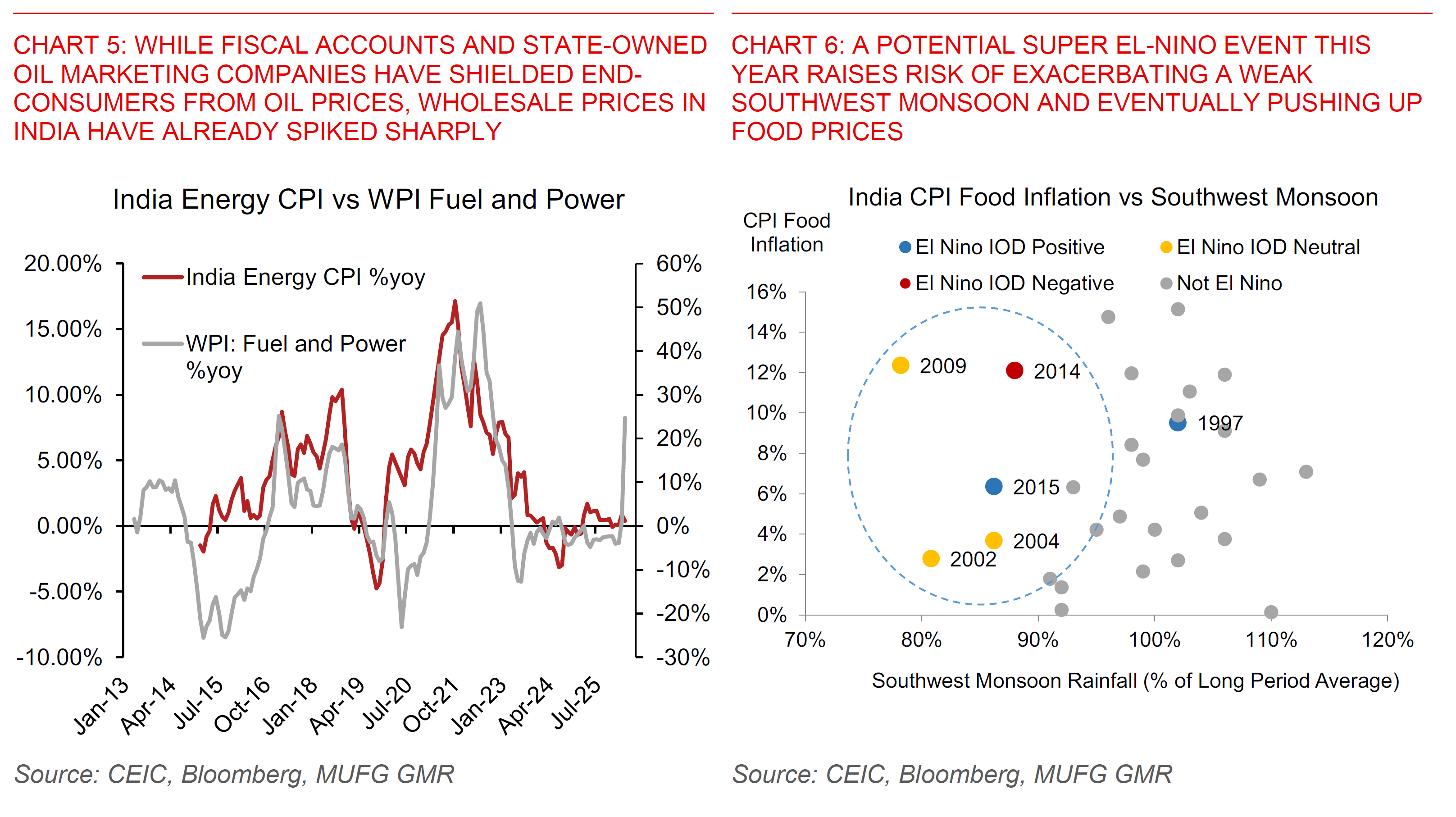

Overall, our forecast for INR underperformance is driven by a combination of weak capital inflows, a wider current account deficit with higher oil prices, and potential energy supply disruption from a prolonged conflict (see India – Strait of Hormuz closure: Not just about oil prices). Risks from a possible weak Southwest Monsoon and a "Super El-Nino", coupled with uncertainty around further increases in US yields also introduce meaningful left tail risks for INR.

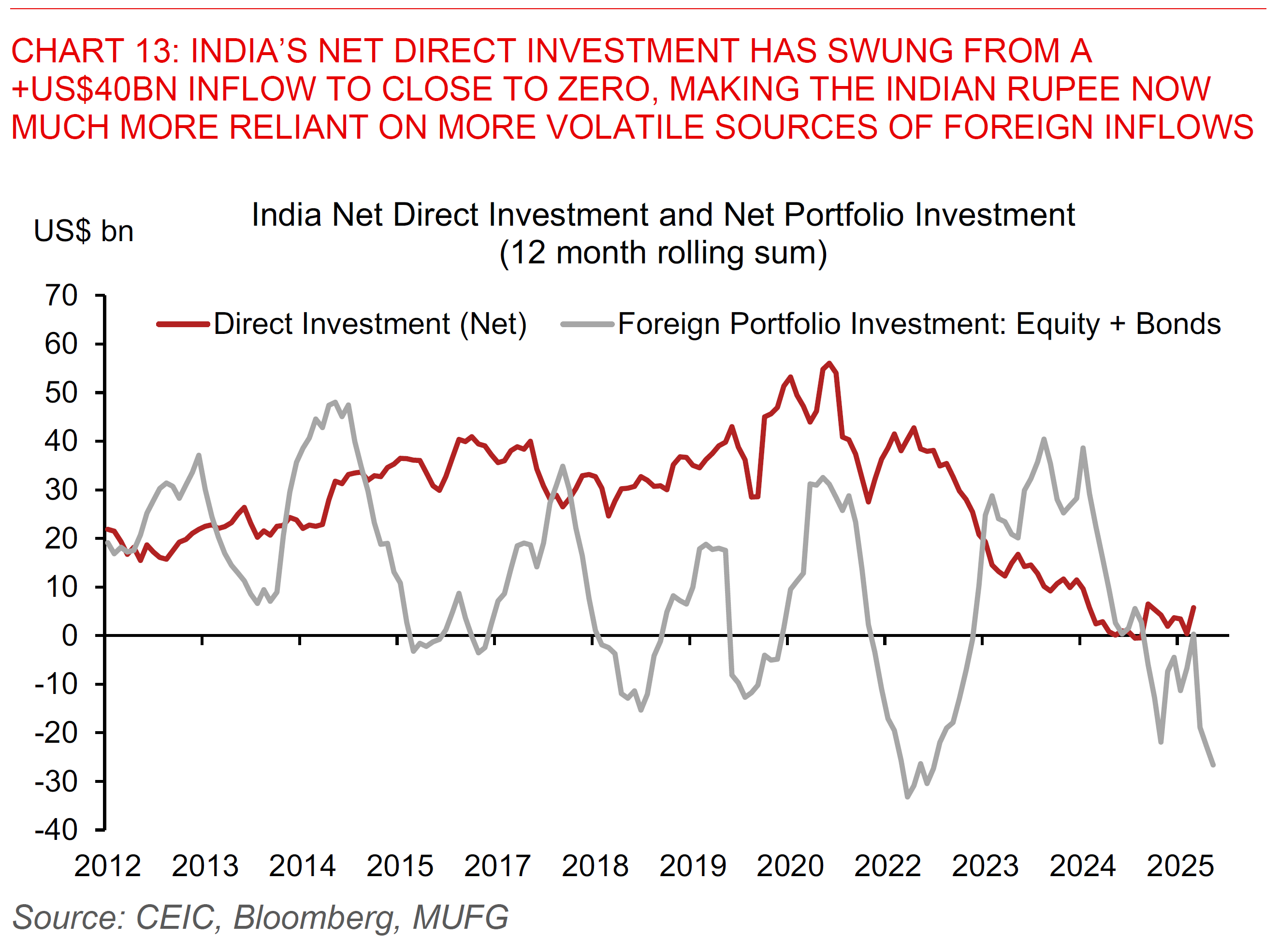

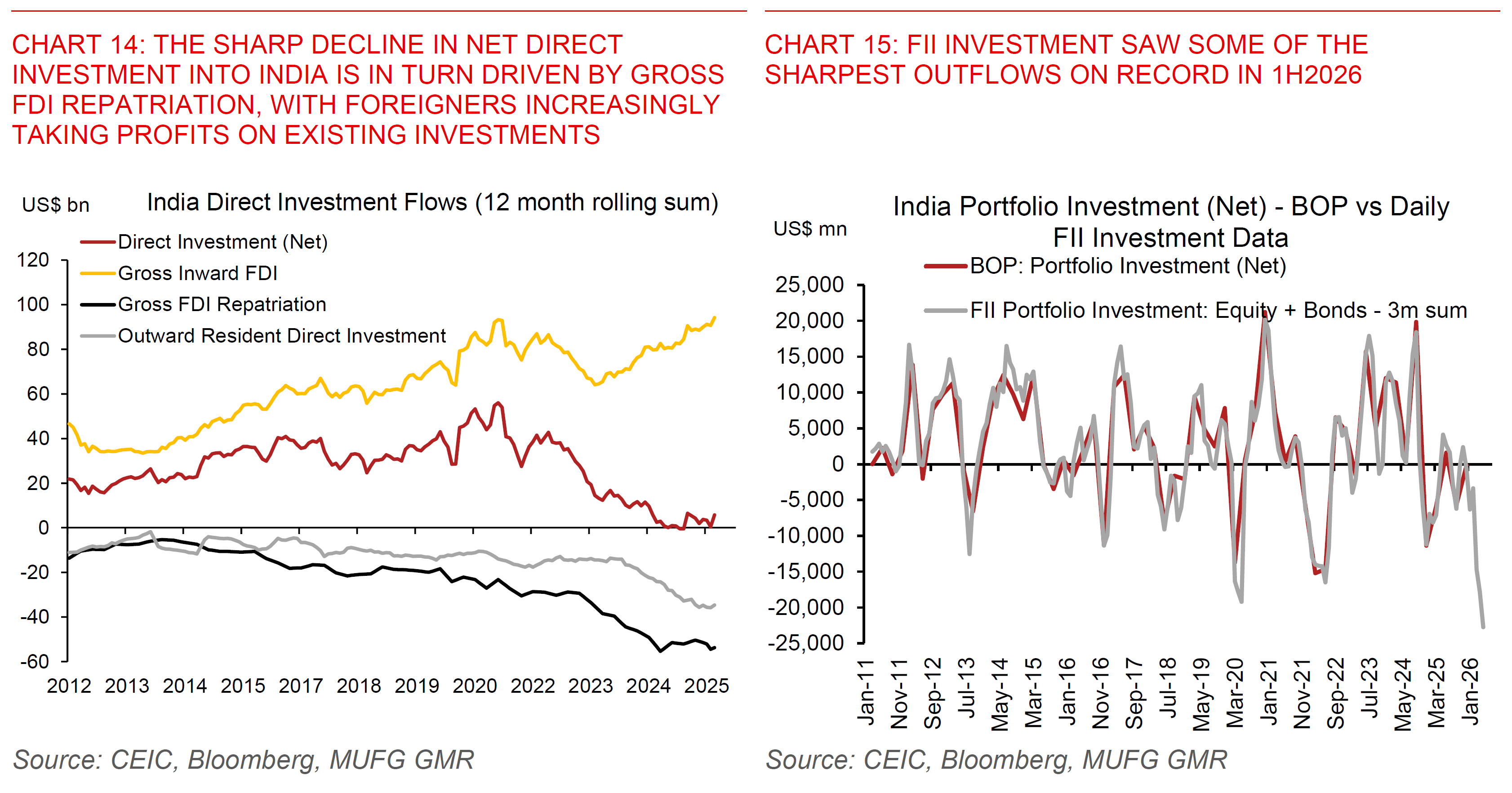

Crucially this problem of weak capital inflows into India predates the Iran conflict, and is likely to as such continue even with de-escalation. We have highlighted these drivers in past reports (see India: Flows before Growth – this time is different for INR), and while this was earlier underappreciated we think more market participants including the RBI and the government are realising the extent of underlying changes in India's balance of payments.

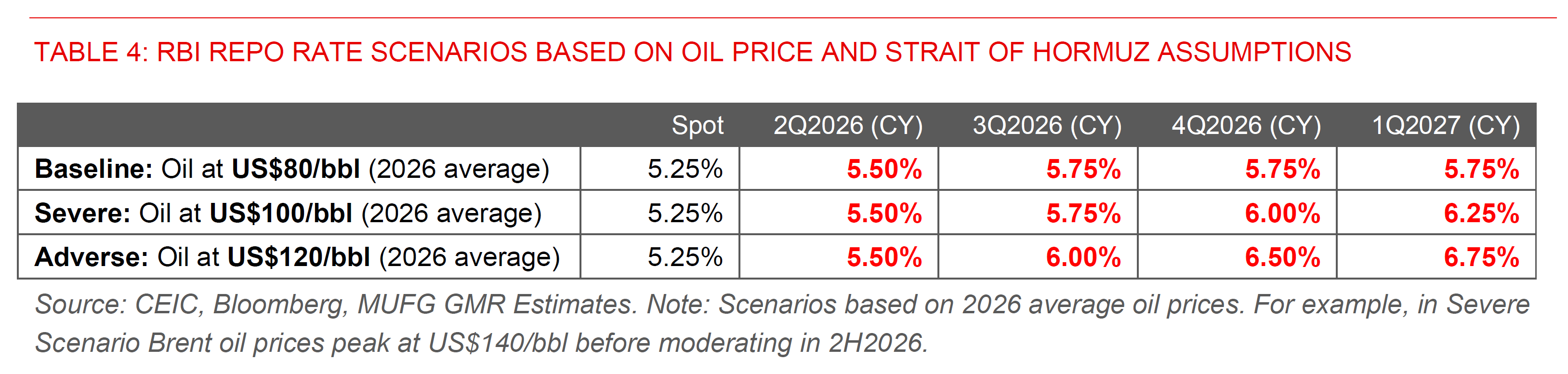

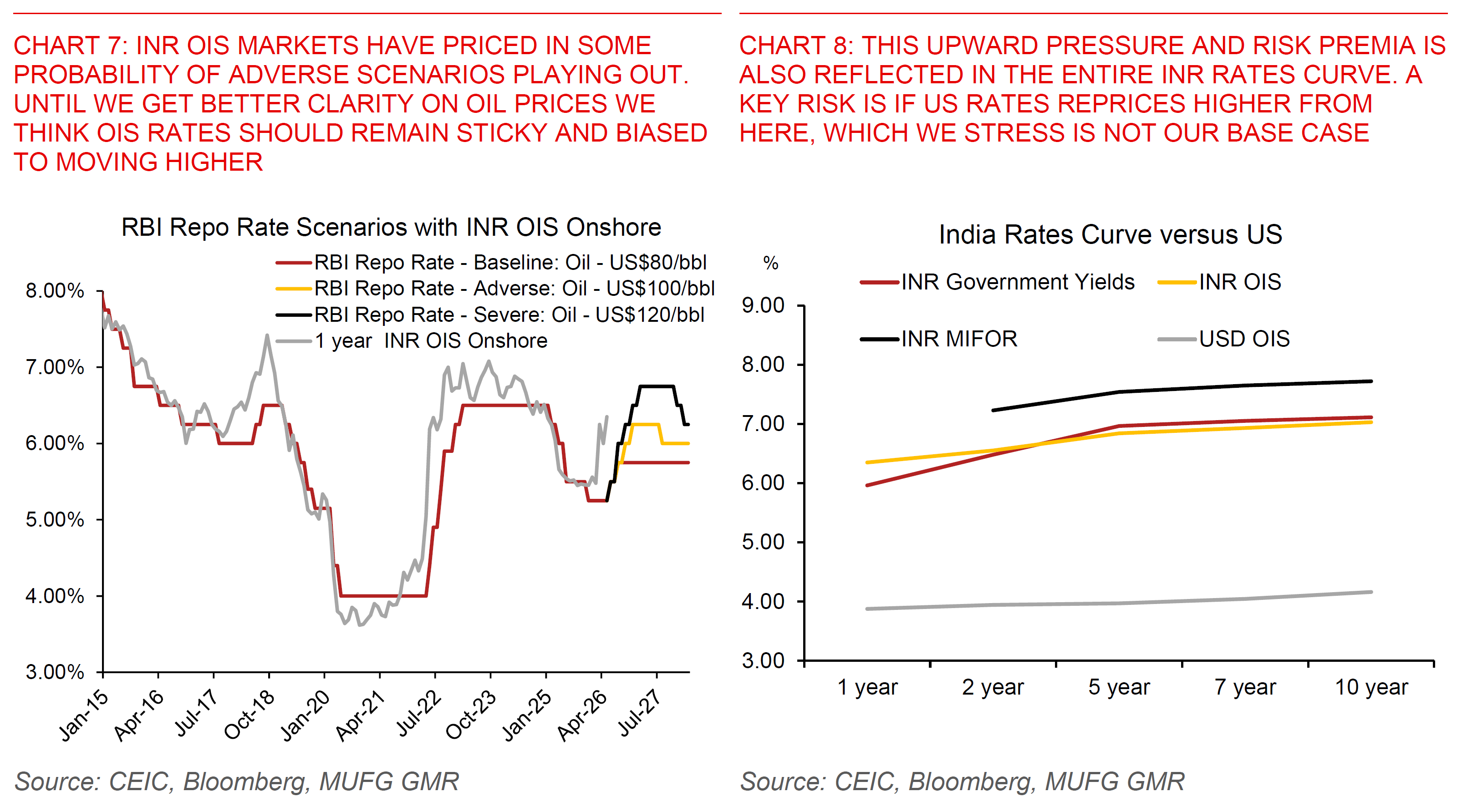

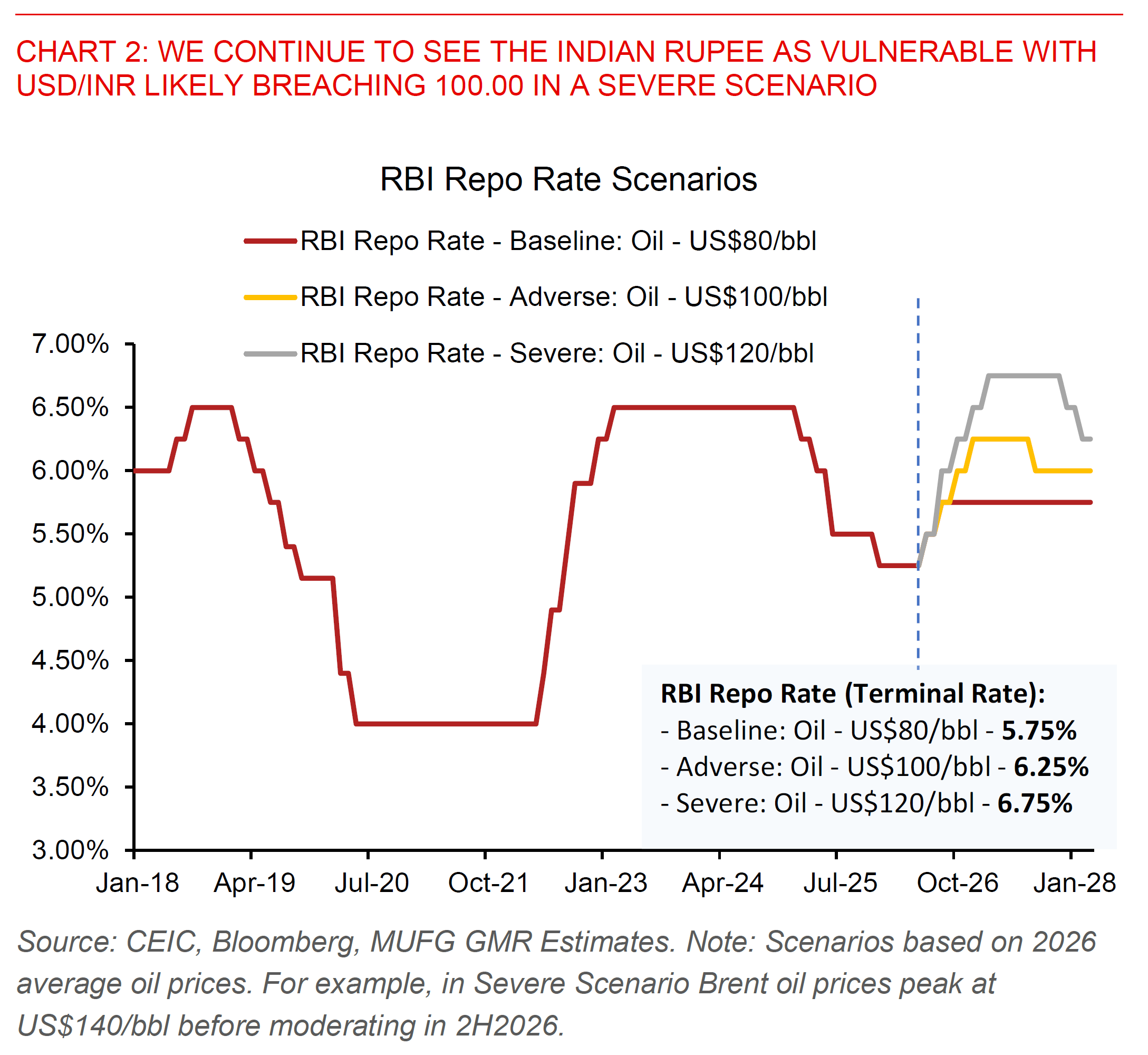

We now forecast RBI hiking rates by at least 50bps this fiscal year, bringing the terminal repo rate to 5.75%, and against the backdrop of INR weakness and a challenging capital inflow picture. This is in part a measure to shore up INR by raising domestic and relative rates of returns while managing inflation expectations. We see these rate hikes as happening sooner rather than later and we pencil them in the June and August meetings.

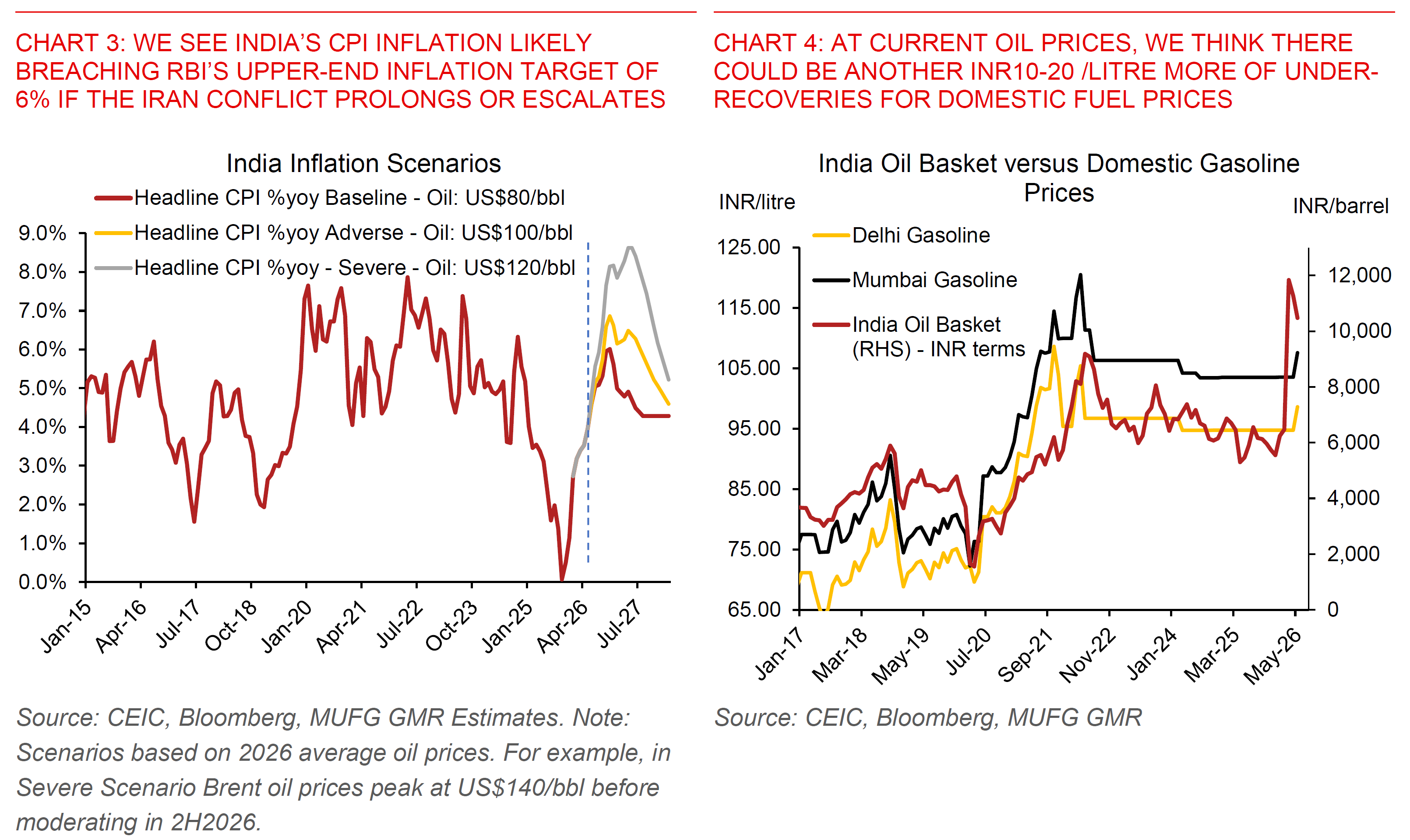

In risk scenarios we think RBI may bring terminal rates up to between 6.25% to 6.75%, with some reversal in rate hikes subsequently in FY2027/28 once RBI sees year-on-year inflation moderating more durably.

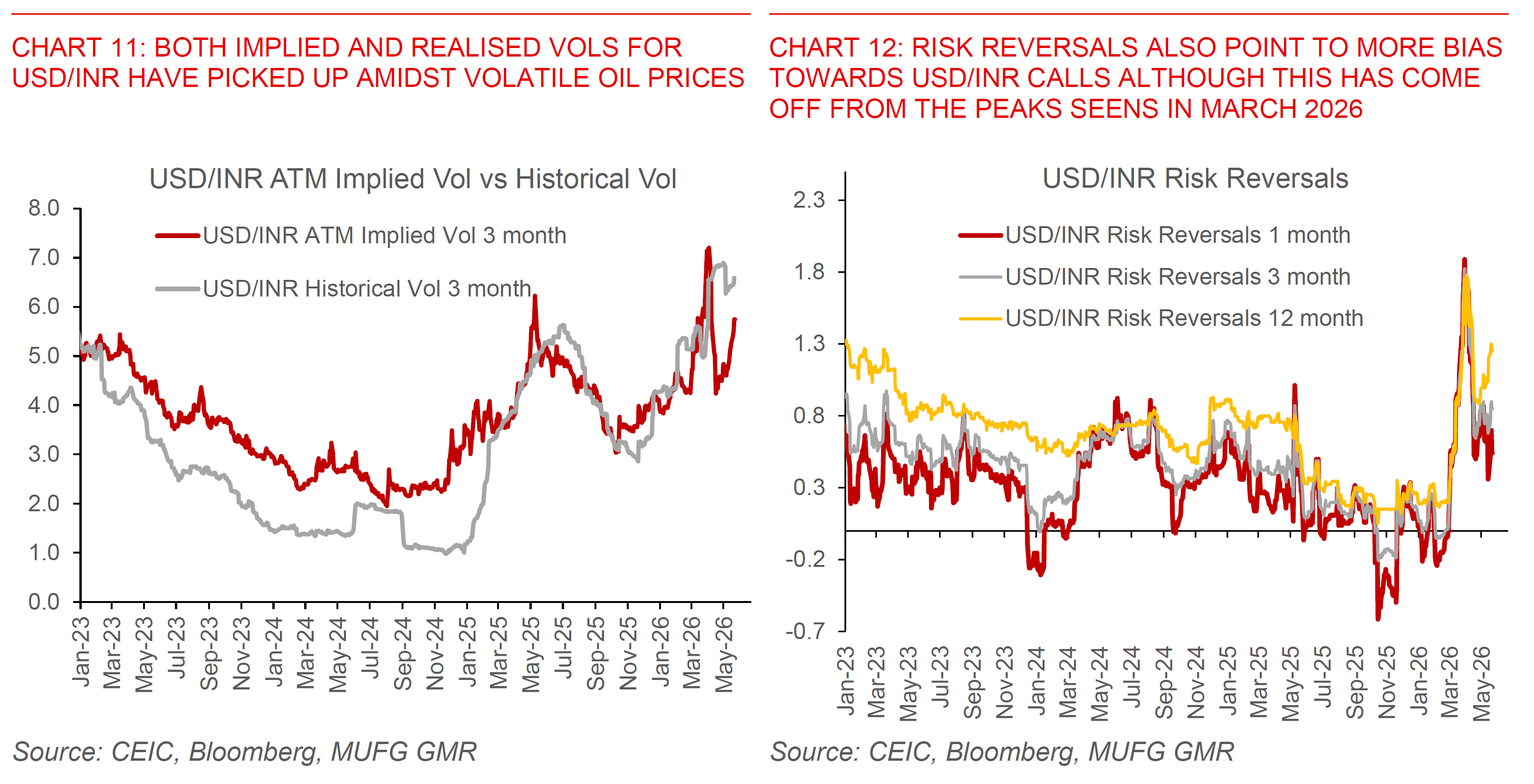

From a markets perspective we note that both the onshore INR OIS curve and FX forwards are already pricing in a fair amount of risk-premia. For instance, there is already more than 125bps of RBI rate hikes priced over the next 12 months, while 12-month USD/INR FX forwards are a touch below 100 at the time of writing. Nonetheless, until we get better clarity on oil prices and the Strait of Hormuz we think the current environment still favours buying on dips for USD/INR and paying on dips for INR rates in the near-term. Given current pricing we would recommend staying patient rather than chasing levels excessively.

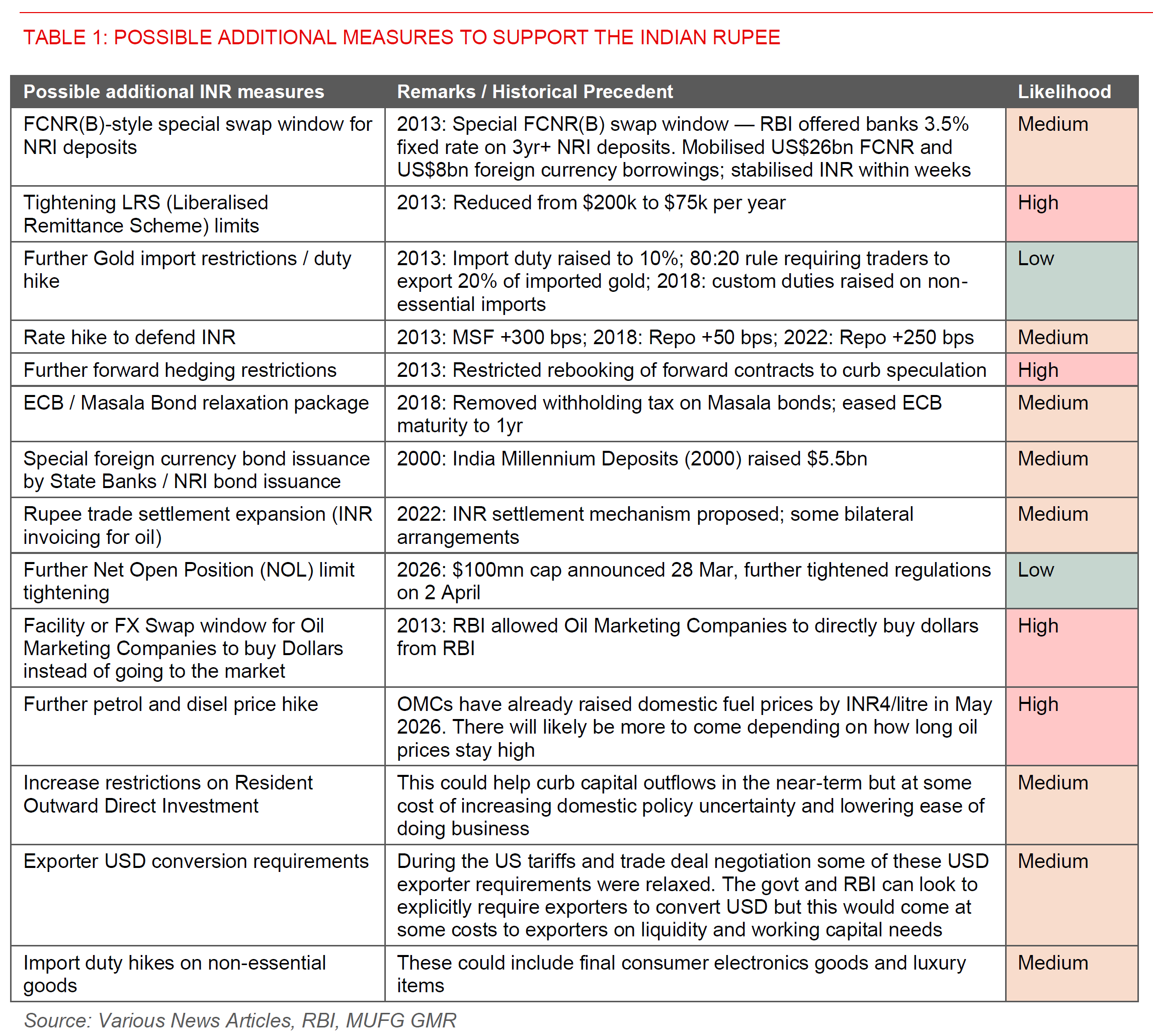

One additional reason to stay patient is that we expect RBI and the India government to take further measures to try to support the Indian Rupee, by shoring up capital inflows, managing capital outflows, while controlling imports needs such as through fuel conservation measures. Authorities have already taken steps including gradually raising domestic fuel prices, increasing import duties on gold, restricting silver imports, introducing some work from home measures, and also increasing scrutiny and restrictions on the INR NDF market. Of course there is no free lunch in life and some policies such as the NDF restrictions arguably had some unintended negative spillover effects to foreign bond investor sentiment as hedging costs spiked (see India: RBI limits on onshore INR positions – Can’t stop this train and India: RBI further tightens NDF restrictions – Driving a Wedge). Moving forward, we think policies including further domestic fuel hikes, tightening of the Liberalised Remittance Scheme, lower caps on India companies’ Direct Investment outflows, coupled with issuance of foreign currency bonds to tap Non-Resident Indian funds among others are likely to be announced moving forward.

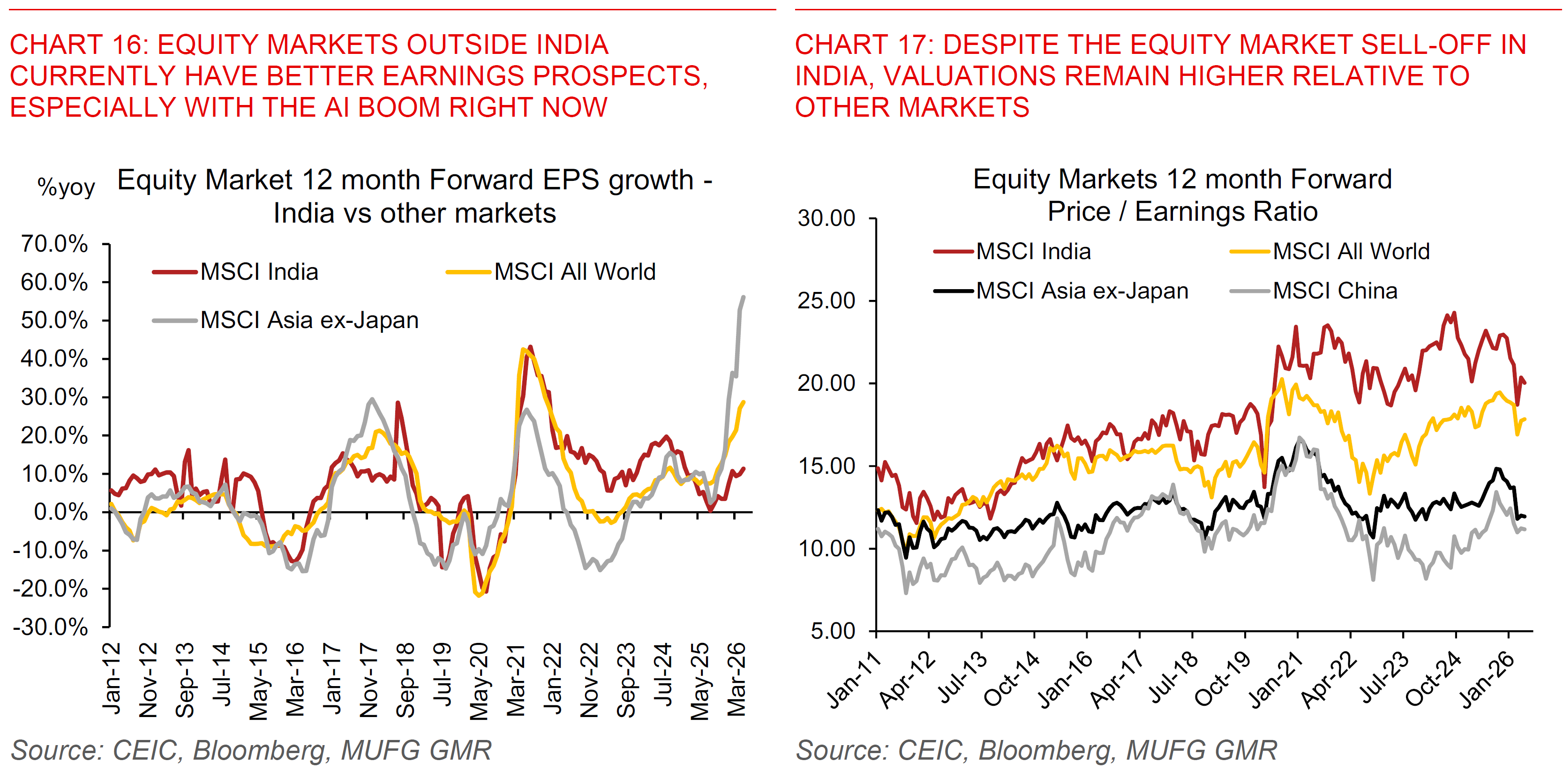

Overall, we think for these measures to have a durable impact on supporting INR they would need to improve the ease of doing business in India and ultimately improve long-term earnings prospects in India relative to other markets.