To read the full report, please download PDF.

Central banks set to highlight inflation risks

FX View:

The G10 FX moves last week were mostly within +/-0.5% underlining the recent relative stability as the Middle East ceasefire holds. Risk appetite remains robust with the Nasdaq advancing 1.5% last week – from the low toward the end of March, the Nasdaq has advanced over 19% helped by renewed AI optimism. With risk appetite resilient, the scope for US dollar appreciation is relatively modest. However, the longer the Strait of Hormuz remains closed the greater the risk of economic disruption and a turn in investor sentiment. One source of potential disruption to the positive sentiment is higher rates due to rising inflation risks. This week will be a busy week for central bank meeting with five G10 central banks meeting – the BoJ tomorrow; the BoC and the Fed on Wednesday; and the BoE and the ECB on Thursday. Greater inflation risks and the potential need for monetary tightening is likely to be one common message that could see higher yields potentially disrupting the positive investor sentiment.

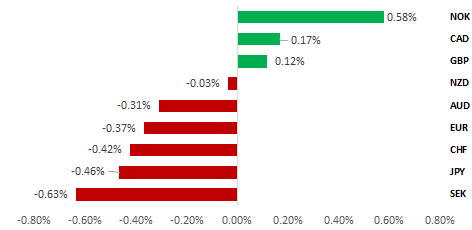

NOK OUTPERFORMED LAST WEEK AS CRUDE OIL SURGED OVER 16%

Source: Bloomberg, close on 24th April 2026 (Weekly % Change vs. USD)

Trade Ideas:

We are maintain a short GBP/CHF trade idea to reflect heightened global stagflation risks and domestic political risks in the UK.

JPY Flows:

The higher frequency flow data from the MoF has seen Japanese investor selling of foreign bonds on rising inflation risks but also a strong rebound in foreign investor buying of Japanese equities.

Short Term Regression Modelling:

According to our BEER fair value model, EUR/USD is trading above its equilibrium, suggesting the pair is expensive relative to fundamentals. In contrast, USD/JPY is trading below fair value, indicating a modest undervaluation versus model fundamentals.

FX Views

USD: Middle East uncertainty & central bank clarity on inflation risks

The price of Brent crude oil closed last week 16.5% higher as concerns grew over the lack of progress in reaching a deal to re-open the Strait of Hormuz. Crude oil has gained further on the open this week following the failure to convene another round of negotiations in Pakistan. The Iranian delegation departed Islamabad prior to the US negotiation team arriving, resulting in President Trump cancelling. US Central Command reported an Iranian tanker was intercepted on Saturday with a total of 37 vessels now having been redirected since the US blockade began. While the ceasefire holds, there remains hope of de-escalation that is curtailing financial market volatility. The hope of some degree of de-escalation coincides with five G10 central banks meeting this week, starting with the BoJ tomorrow, the BoC and the Fed on Wednesday and then BoE and ECB on Thursday. The OIS curve for the US continues to point to investor expectations of the Fed taking a more relaxed approach to energy-related inflation risks with market pricing still showing a modest risk of rate cuts this year. All the other central banks meeting this week are expected to hike at some stage over the coming months. In a scenario of de-escalation in the Middle East, that pricing is likely to encourage renewed US dollar selling.

The key central bank meeting of the week will be the FOMC meeting on Wednesday. The statement from the FOMC could reveal some upgrade to the description of the labour market given the stronger payrolls data (+178k) published at the start of April. The statement will likely repeat that the implications of the conflict in the Middle East are “uncertain” although given the six weeks that will have passed since the last meeting, there could be some emphasis on the greater risks of a broader energy-price pass-through by explicitly referencing a growing upside risk to its inflation mandate. If the statement itself does not reference increased inflation risks, we would expect Fed Chair Powell to be more hawkish in the press conference. Powell will find it difficult to continue to ignore the reality that upside inflation risks are rising given the conflict will this week be in its ninth week. At the March FOMC, Powell stated that he wouldn’t say “one mandate risk is bigger than the other” which is very unlikely to be repeated. Energy price rises and fertiliser price rises will quickly translate to higher food prices that will then start to show up in core CPI as services inflation picks up.

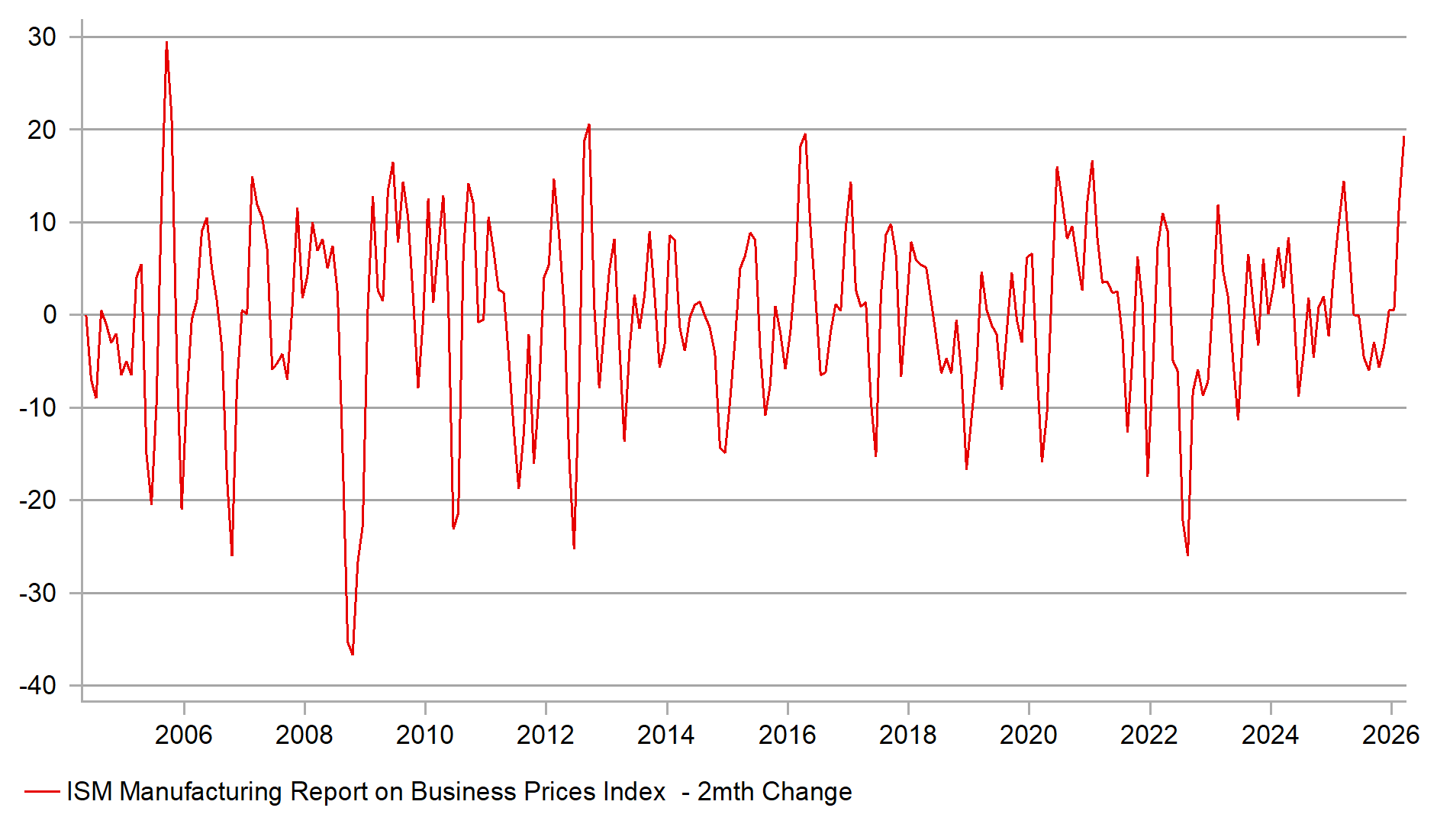

When the data provides evidence of increased risks it is much more difficult for the Fed to ignore it. The ISM manufacturing prices paid index jumped to 78.3 in March. The two-month increase over Feb/Mar totalled 19.3ppt, the biggest increase since April 2016. With gasoline pump prices up over 30% since the conflict began, there are plenty of examples of the immediate inflationary impact. The Fed on Wednesday will need to emphasise that it is seeing the inflationary risks rise and will be willing to respond if the conflict persists. There is also a risk that Steve Miran drops his vote to cut rates – on 16th April he indicated that he was “reconsidering his rate cut outlook” acknowledging that the inflation outlook had become more complicated. Overall, the tone of the FOMC meeting next week appears more likely to turn hawkish.

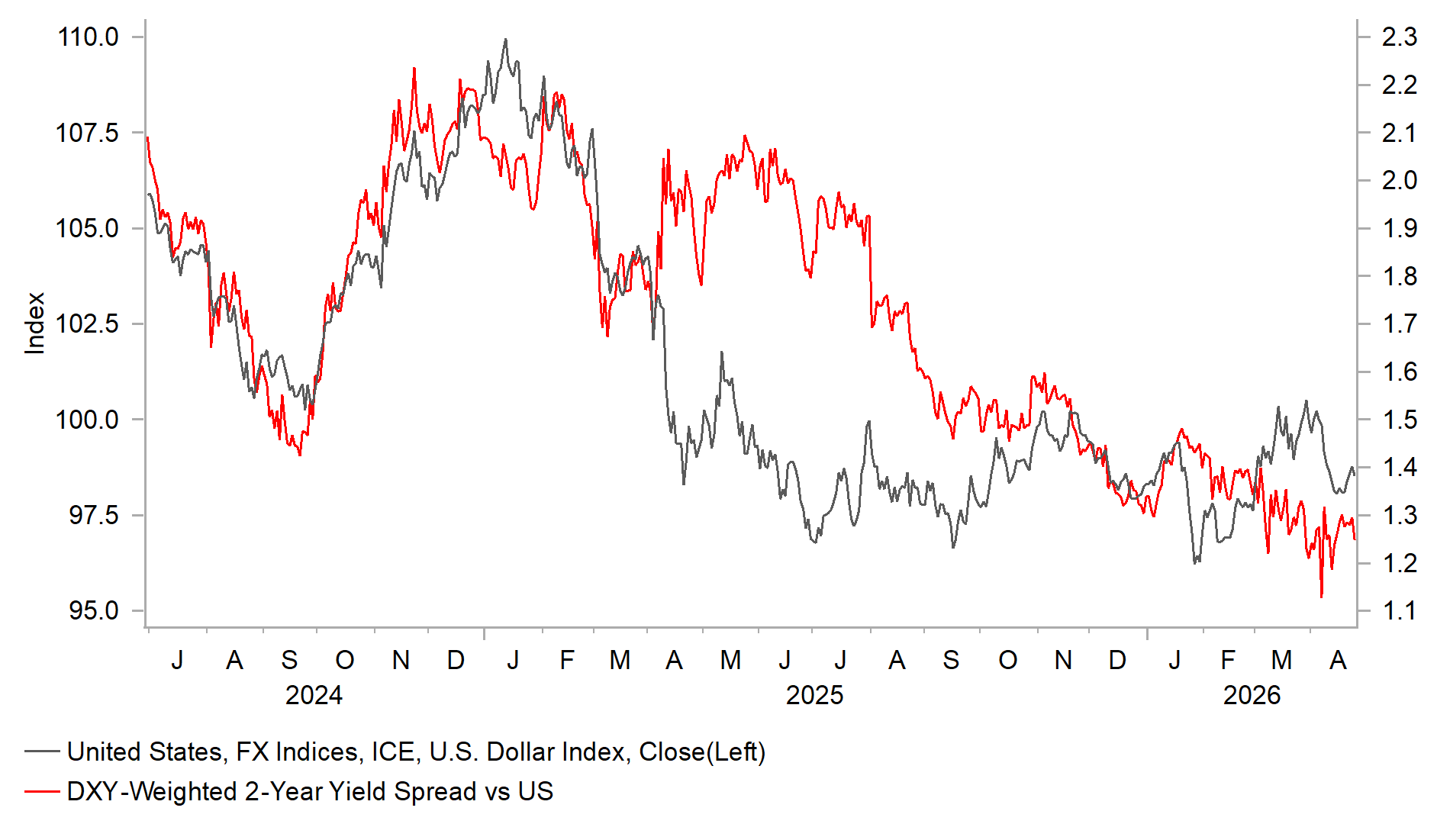

YIELD SPREADS KEEP USD GAINS IN CHECK

Source: Bloomberg, Macrobond & MUFG GMR

2MTH CHANGE IN PRICES PAID BIGGEST SINCE 2016

Source: Bloomberg, Macrobond & MUFG GMR

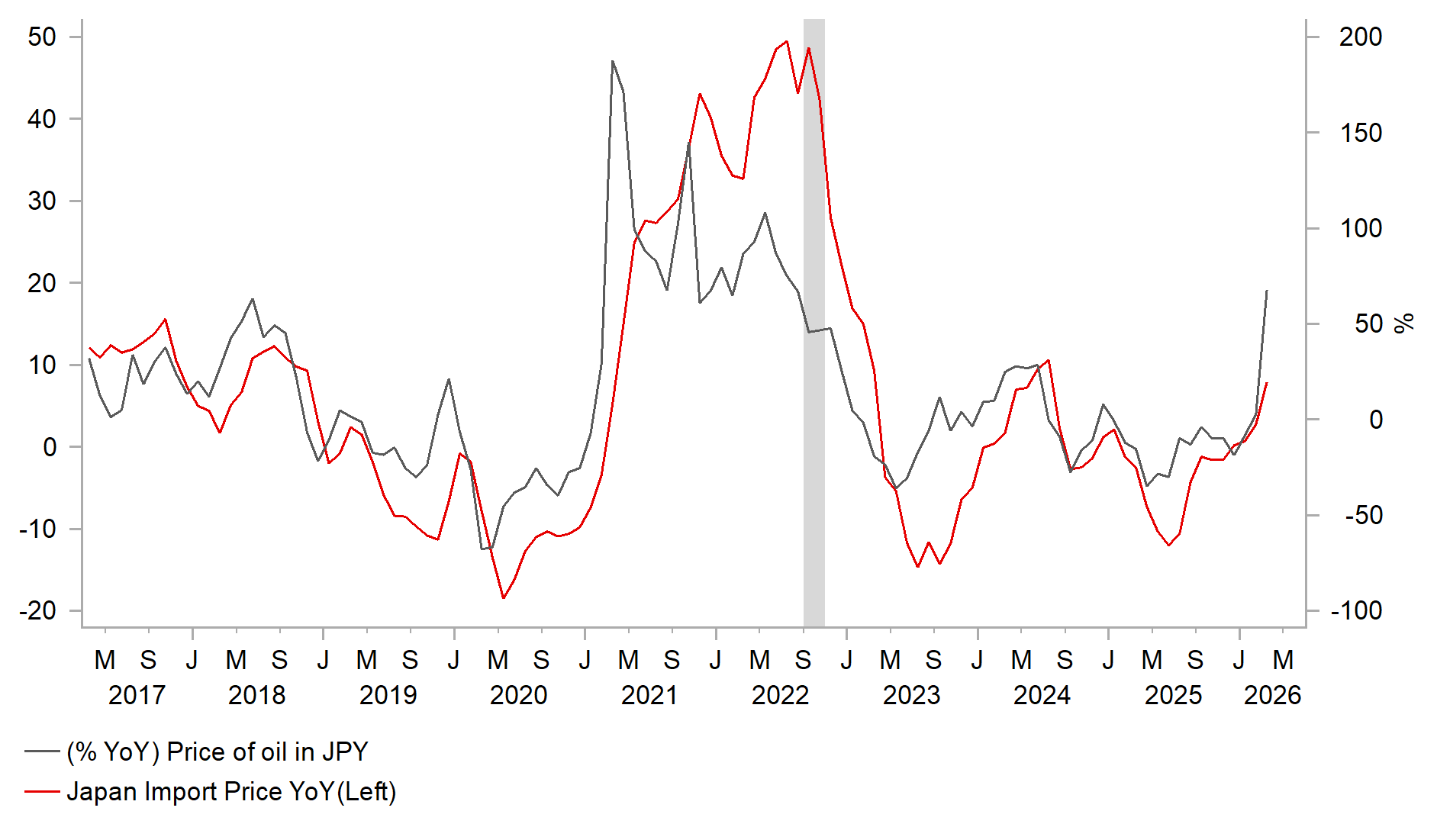

Ahead of the FOMC meeting, the BoJ will meet tomorrow with expectations of a rate hike having come down notably. At the beginning of April about 18bps of tightening was priced but that is now close to zero. The BoJ have drip-fed information to the market suggesting caution was warranted at the April meeting due to the conflict in the Middle East. But Governor Ueda will have to thread a fine line between emphasising the current uncertainty as reason for caution and signalling that the BoJ will act to limit upside inflation risks. The monetary stance remains loose and rising inflation will only reinforce the still deeply negative policy rate in real terms. Nationwide CPI data on Friday for March revealed upside surprises for the headline and core rates. Services PPI also jumped more than expected, from 2.7% to 3.1%, the biggest jump since 2024.

A more dovish communication from the BoJ and the potential for the Fed being more hawkish is a recipe for renewed upside momentum in USD/JPY through the 160-level. That would likely coincide with renewed instability in the JGB market as fears over the BoJ being behind the curve return. A more dovish communication would also reinforce the impression that PM Takaichi is dictating the overall monetary stance that would further reinforce Japan selling risks. The BoJ therefore needs to limit this risk and convey a more hawkish message on the outlook for policy. The BoJ tomorrow will also publish updated forecasts, and it is likely we will see inflation projections above the 2.0% target given in January the FY26 projection was 1.9% for core nationwide CPI and 2.0% in FY27. We expect the BoJ to provide a message that signals a likelihood of a hike at the next meeting and we currently assume a 25bp hike to 1.00% in June.

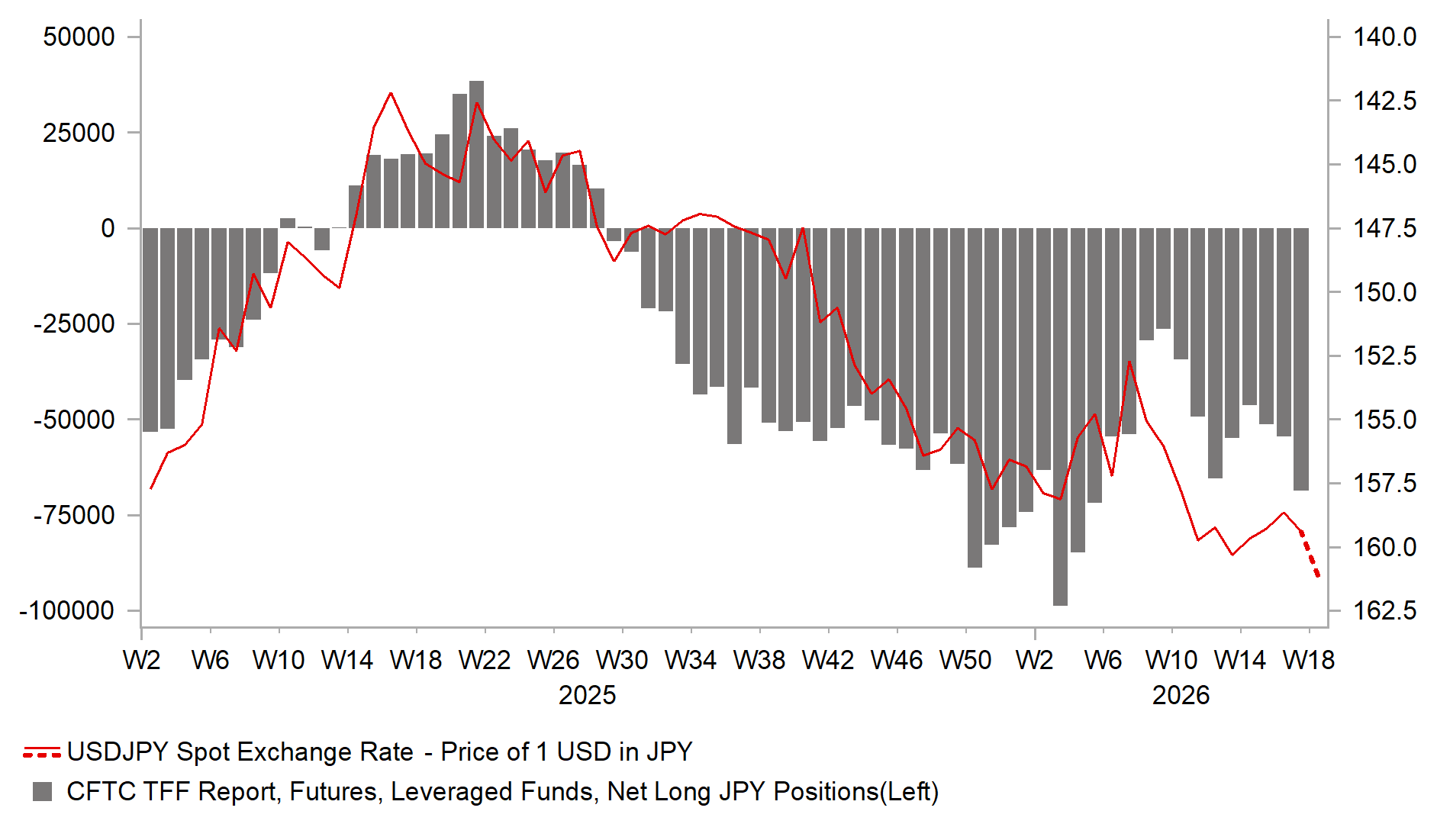

The threat of intervention was once again communicated last week by FM Katayama and this messaging and the fact that the Fed checked rates in USD/JPY in January have helped limit appetite for yen selling above the 160-level. Since the conflict began USD/JPY has breached 160 three times and has traded within 20 pips of that level another ten times and this week could be the week in which we see a more meaningful break higher. Abrupt moves have not yet taken place although the latest IMM speculative positioning data did reveal a pick-up in yen selling that could be an indication of increased expectations of a move higher in USD/JPY. The BoJ’s communication tomorrow will be key for avoiding a bigger move higher in USD/JPY.

IMPORT PRICES IN JAPAN SET TO PICK UP

Source: Bloomberg, Macrobond & MUFG GMR

EVIDENCE OF INCREASED SPECULATIVE SELLING

Source: Bloomberg, Macrobond & MUFG GMR

EUR/GBP: European FX majors lose upward momentum ahead of BoE & ECB policy updates

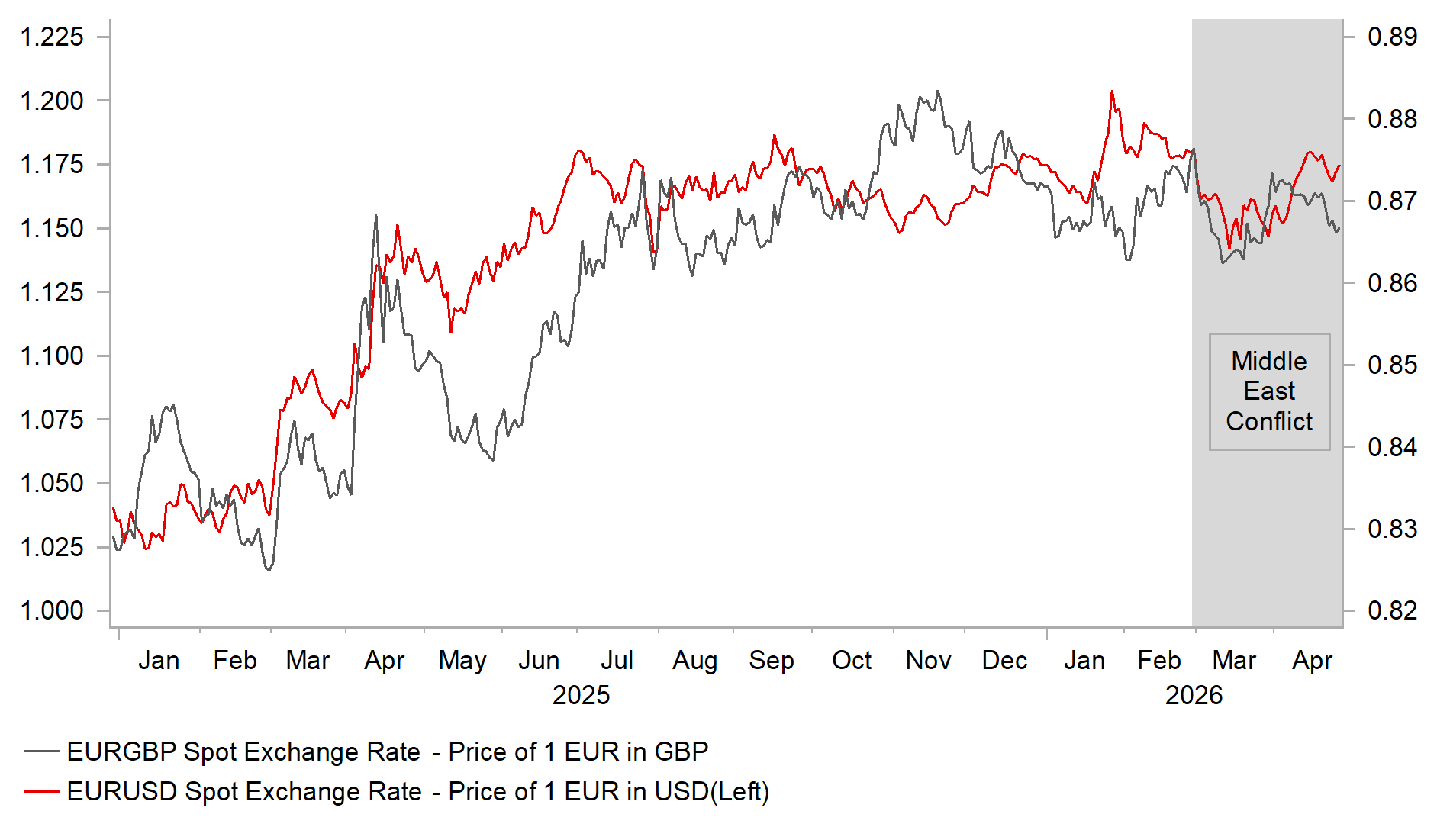

The EUR has lost upward momentum over the past week, with both EUR/USD and EUR/GBP falling below 1.1700 and 0.8700, respectively. The pullback in EUR/USD follows a strong rally that fully reversed the initial losses seen at the start of the Middle East conflict, with the pair peaking at 1.1849 on 17th April. As a result, EUR/USD has slipped back toward the middle of the 1.1400–1.2000 trading range that has been in place since June last year. The recent correction in the EUR appears to have been driven by a combination of factors, including disappointment over the lack of progress in US–Iran talks aimed at reopening the Strait of Hormuz and emerging evidence of the initial negative impact of the energy price shock on the euro‑zone economy. The longer the Strait of Hormuz remains closed, the more disruptive the energy price shock is likely to be for the euro‑zone economy, reinforcing headwinds for the EUR.

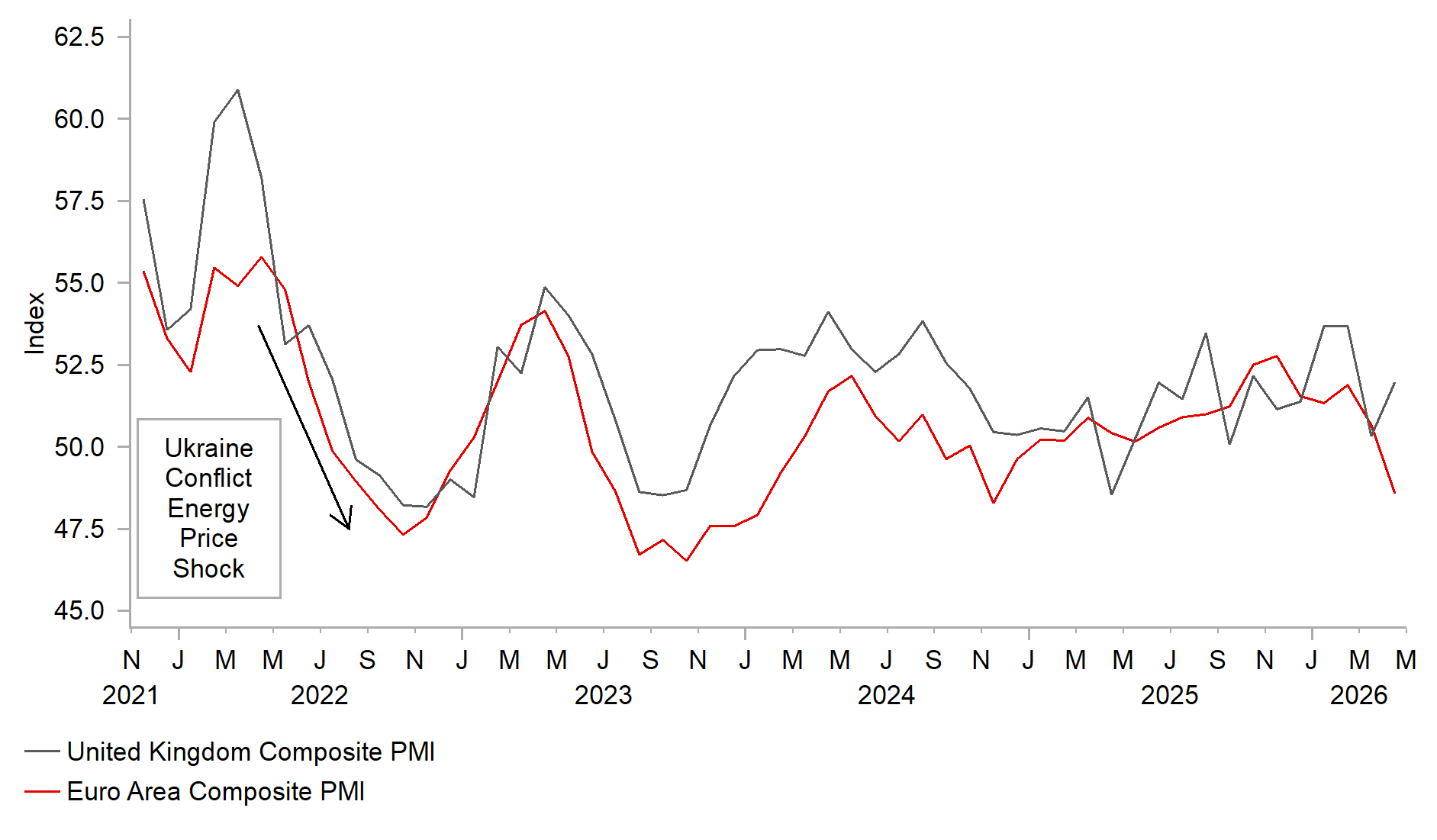

The initial negative impact of the energy price shock on the euro‑zone economy was evident in the latest PMI surveys for April. The surveys showed that business confidence fell sharply in the services sector, while holding up better among manufacturers. The euro‑zone services PMI declined by 2.8 points to 47.4 in April, whereas the manufacturing PMI rose by 0.6 points to 52.2. For the euro‑zone economy as a whole, the composite PMI dropped by 2.1 points to 48.6, marking its weakest level since November 2024. The index has now fallen by 3.3 points since February, prior to the Middle East conflict. Business confidence has deteriorated more quickly than during the previous energy price shock triggered by Russia’s invasion of Ukraine in early 2022 and is already at much weaker levels. On that occasion, the composite PMI fell by 8.5 points between April and October 2022. The current level of the composite PMI is already signalling that economic growth may stagnate at the start of Q2. Stagflation risks were further underscored by a sharp rise in both the input and output price sub‑components, which each increased by just over three points.

The ECB has clearly outlined three main scenarios for the euro‑zone economy in response to the energy price shock: baseline, adverse, and severe. In a recent speech, President Lagarde stated that she currently judges the euro‑zone economy to be positioned between the baseline and adverse scenarios. She noted that energy prices have not yet risen “far enough to push us squarely into our adverse scenario”, while European natural gas prices remain “below our baseline”. President Lagarde also expressed optimism that, should the conflict be resolved quickly, the energy price shock could prove to be at the lower end of expectations, allowing the economic impact to remain contained. However, the longer the Strait of Hormuz remains closed, the more the euro‑zone economy risks remaining on a trajectory toward the adverse

scenario. Under the baseline scenario, the ECB has indicated that it would keep policy rates on hold, while the adverse scenario would require a more measured policy response. Ahead of this week’s policy meeting, the ECB has signalled that it is not in a hurry to begin raising rates and prefers to take more time to assess the economic impact of the energy price shock. This approach reflects a desire to better gauge the risks of second‑round effects and the potential for inflation expectations to become unanchored. We continue to expect the ECB to deliver a cumulative 50bp of rate hikes (click here), although the timing of the first increase is likely to be delayed until June. This creates scope for near‑term policy divergence between the ECB and the Fed, as the Fed appears more comfortable looking through the energy price shock on this occasion. Narrowing yield spreads have helped support the EUR and have softened USD strength in response to the energy price shock.

EUROPEAN FX MAJORS REMAIN IN TIGHT RANGES

Source: Bloomberg, Macrobond & MUFG GMR

BUSINESS CONFIDENCE IN EURO-ZONE HIT HARDER

Source: Bloomberg, Macrobond & MUFG GMR

The GBP has held up better than the EUR over the past week, placing modest downward pressure on EUR/GBP, although the pair has remained within a relatively tight 0.8600–0.8800 range since the conflict began. The GBP has been supported by further evidence that the UK economy started the year with more underlying momentum than previously expected, while the initial negative impact of the energy price shock has so far appeared limited. Prior to the energy shock, the UK economy expanded solidly by 0.5% in February and remains on track to grow by around 0.6% in Q1. This compares favourably with earlier Bank of England staff estimates that had pointed to underlying growth of just 0.1%–0.2% in Q1. In contrast to the euro‑zone, the latest UK PMI surveys also showed an improvement in business confidence in April, although this followed a sharp decline in March.

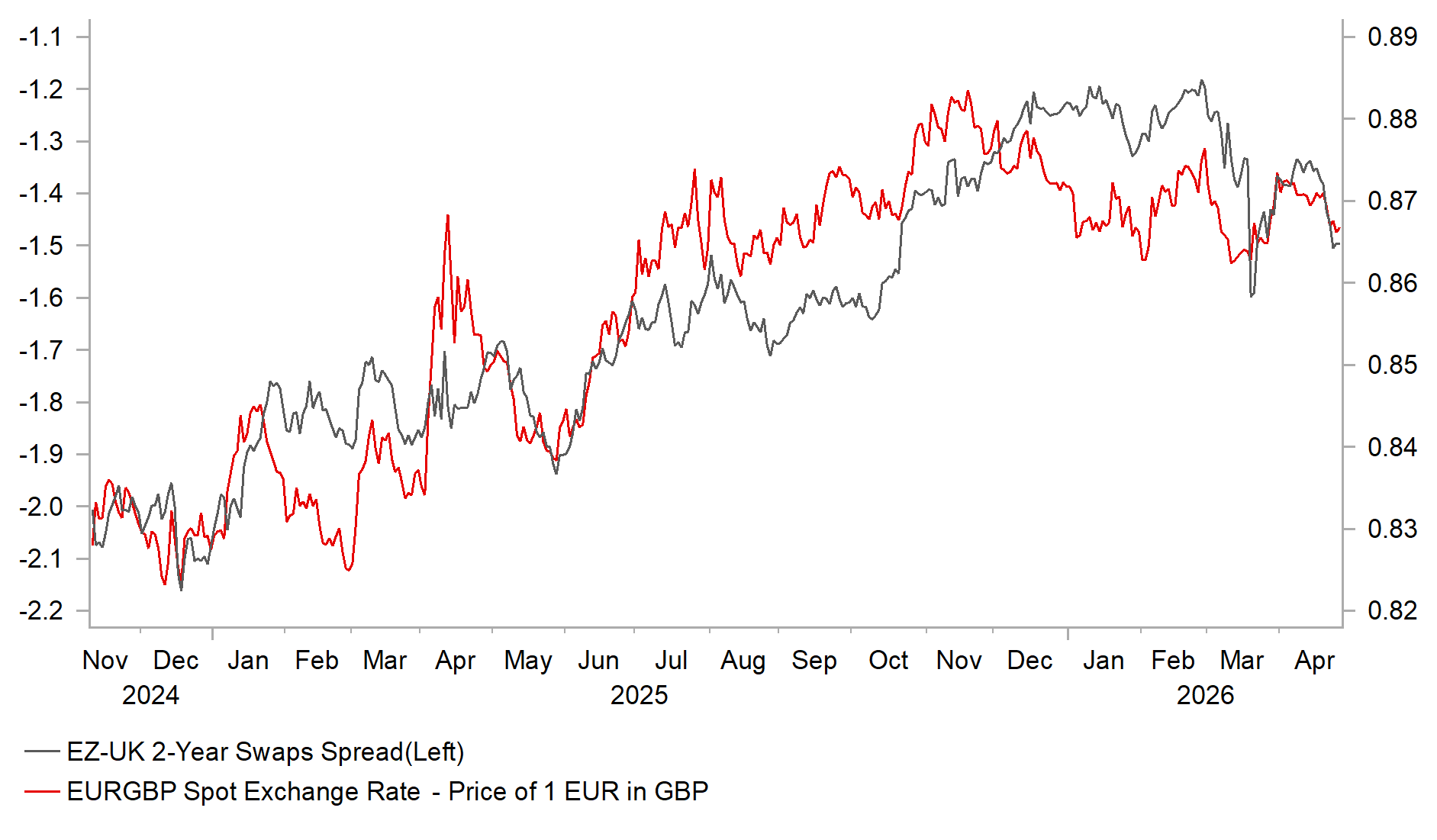

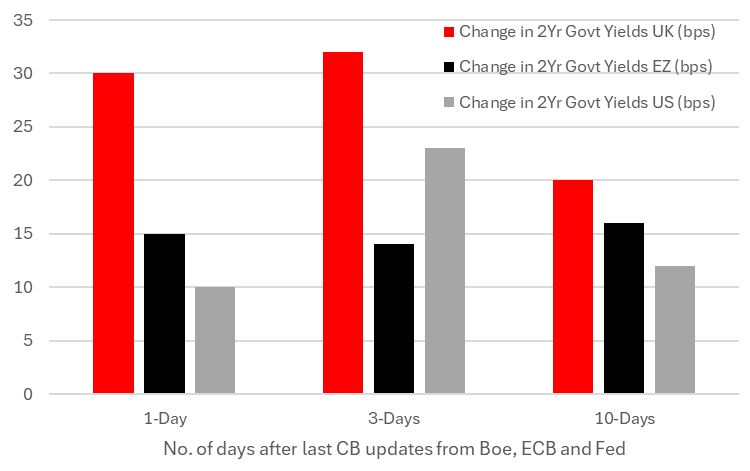

Stronger growth momentum has increased the risk of a hawkish policy update from the BoE this week. The UK rate market has moved to price back in more tightening from the BoE, and the uplift for UK yields has provided more support for the GBP. The 2-year government bond yield in the UK has increased by around 30bps from the recent low compared to around 20bps in the euro-zone and just over 10bps in the US. At the same time, the latest UK CPI report for March continued to reveal that underlying inflation pressures remain uncomfortably high at the start of the energy price shock curtailing the BoE’s ability to look through the inflation shock. While the BoE will be wary of triggering another outsized hawkish market reaction similar to after the last MPC meeting in March, it will be hard to avoid presenting a hawkish policy signal. There is a good chance several MPC members including Chief Economist Pill and MPC member Mann will vote for a hike this week. After the last MPC meeting in March, the 2-year government yield from the UK increased by around 50bps in the following days. Another hawkish message that keeps alive expectations for at least a couple of BoE rate hikes will continue to support the GBP.

YIELD SPREADS HAVE MOVED IN FAVOUR OF GBP

Source: Bloomberg, Macrobond & MUFG GMR

OUTSIZED REACTION TO LAST MPC MEETING

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

|

Date |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

|

JN |

28/04/2026 |

00:30 |

Jobless Rate |

Mar |

2.6% |

2.6% |

!! |

|

JN |

28/04/2026 |

Tbc |

BOJ Target Rate |

0.75% |

0.75% |

!!! |

|

|

EC |

28/04/2026 |

09:00 |

ECB Bank Lending Survey |

!! |

|||

|

US |

28/04/2026 |

14:00 |

S&P Cotality CS 20-City MoM SA |

Feb |

-- |

0.2% |

!! |

|

US |

28/04/2026 |

15:00 |

Conf. Board Consumer Confidence |

Apr |

90.0 |

91.8 |

!! |

|

AU |

29/04/2026 |

02:30 |

CPI YoY |

Mar |

4.8% |

3.7% |

!!! |

|

SW |

29/04/2026 |

07:00 |

GDP Indicator SA QoQ |

1Q |

-- |

0.2% |

!! |

|

EC |

29/04/2026 |

09:00 |

M3 Money Supply YoY |

Mar |

-- |

3.0% |

!! |

|

GE |

29/04/2026 |

13:00 |

CPI YoY |

Apr P |

-- |

2.7% |

!!! |

|

US |

29/04/2026 |

13:30 |

Advance Goods Trade Balance |

Mar |

-$86.9b |

-$98.5b |

!! |

|

US |

29/04/2026 |

13:30 |

Housing Starts |

Mar |

1410k |

1487k |

!! |

|

US |

29/04/2026 |

13:30 |

Durable Goods Orders |

Mar P |

0.5% |

-1.3% |

!! |

|

CA |

29/04/2026 |

14:45 |

Bank of Canada Rate Decision |

2.25% |

2.25% |

!!! |

|

|

US |

29/04/2026 |

19:00 |

FOMC Rate Decision (Upper Bound) |

3.75% |

3.75% |

!!! |

|

|

US |

29/04/2026 |

19:30 |

Fed Holds Press Conference |

!!! |

|||

|

JN |

30/04/2026 |

00:50 |

Industrial Production MoM |

Mar P |

1.0% |

-2.0% |

!! |

|

FR |

30/04/2026 |

07:45 |

CPI YoY |

Apr P |

-- |

1.7% |

!! |

|

GE |

30/04/2026 |

08:55 |

Unemployment Change (000's) |

Apr |

-- |

0.0k |

!! |

|

EC |

30/04/2026 |

10:00 |

GDP SA QoQ |

1Q A |

0.2% |

0.2% |

!! |

|

EC |

30/04/2026 |

10:00 |

CPI Estimate YoY |

Apr P |

2.9% |

2.6% |

!!! |

|

UK |

30/04/2026 |

12:00 |

Bank of England Bank Rate |

3.75% |

3.75% |

!!! |

|

|

EC |

30/04/2026 |

13:15 |

ECB Deposit Facility Rate |

2.00% |

2.00% |

!!! |

|

|

CA |

30/04/2026 |

13:30 |

GDP MoM |

Feb |

0.3% |

0.1% |

!! |

|

US |

30/04/2026 |

13:30 |

Core PCE Price Index YoY |

Mar |

3.2% |

3.0% |

!! |

|

US |

30/04/2026 |

13:30 |

Initial Jobless Claims |

-- |

-- |

!! |

|

|

US |

30/04/2026 |

13:30 |

Employment Cost Index |

1Q |

0.8% |

0.7% |

!! |

|

US |

30/04/2026 |

13:30 |

GDP Annualized QoQ |

1Q A |

1.4% |

0.5% |

!! |

|

EC |

30/04/2026 |

13:45 |

ECB Press Conference |

!!! |

|||

|

JN |

01/05/2026 |

00:30 |

Tokyo CPI YoY |

Apr |

1.6% |

1.4% |

!! |

|

US |

01/05/2026 |

15:00 |

ISM Manufacturing |

Apr |

52.6 |

52.7 |

!! |

Source: Bloomberg & MUFG GMR

Key Events:

- There is a heavy schedule of central bank policy updates in the week ahead, including the BoJ (Tuesday), BoC (Wednesday), Fed (Wednesday), BoE (Thursday), and ECB (Thursday). Market participants will be watching closely to assess how central banks are responding to the recent energy price shock. The lack of fresh talks between the US and Iran over the past week has increased the risk of a more prolonged disruption to energy supplies from the Middle East, which could result in greater strain on the global economy.

- The BoJ is expected to deliver a hawkish hold this week, leaving the policy rate unchanged at 0.75%. Heightened uncertainty related to the Middle East conflict has prompted caution over further rate hikes in the near term. However, updated guidance is expected to signal that another hike could be delivered as early as the June meeting, supported by upward revisions to inflation forecasts.

- Fed officials have indicated they are comfortable leaving rates on hold in the near term, allowing more time to assess the potential economic fallout from the Middle East conflict. We expect the Fed to stick closely to this script in the week ahead.

- In contrast to the Fed, the European central banks of the BoE and the ECB have signalled that they are considering tightening policy in response to the energy price shock. However, neither central bank appears in a rush to raise rates as soon as this week and both prefer to take additional time to evaluate the economic impact. Updated communication from the BoE has the potential to generate greater market volatility given differing views among MPC members, although the overall tone is unlikely to trigger such a hawkish reaction as seen after the March meeting. One or two MPC members could vote for a hike this week. For the ECB, we expect President Lagarde to reiterate that measured tightening may be required should risks of an adverse scenario continue to build.