To read the full report, please download PDF.

Optimism elevated but FX response muted

FX View:

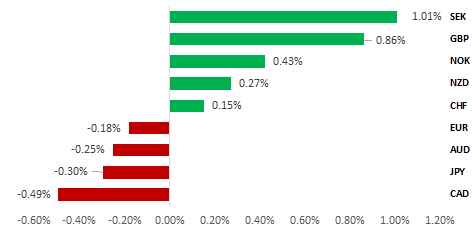

The US dollar performance last week was mixed and this week with optimism elevated over the potential for a peace deal in the Middle East, the US dollar performance remains somewhat muted. SEK and AUD are the biggest movers but the response to the 7% drop in crude oil prices yesterday has been limited. The US attacks on Iranian ships in the region have increased uncertainty over whether a deal can be achieved. A retracement of the optimism is a risk and higher volatility would add further support for the dollar over the short-term. We focus on the performance of AUD this week and see signs that the strong performance may be coming to an end. For sure, a deal being announced will provide further support but a lot of good news is priced at this stage and we see more limited scope for continued AUD outperformance. AUD has been the second best performing G10 currency since the conflict began. The RBA has been much more proactive than other central banks and that could see pricing for another hike pushed back further given the RBA’s wait-and-see capacity is greater than elsewhere. We also provide an updated outlook on the Turkish lira.

G10 FX LAST WEEK HIGHLIGHTS MIXED USD PERFORMANCE

Source: Bloomberg, close on 22nd May 2026 (Weekly % Change vs. USD)

Trade Ideas:

We have closed our long AUD/SEK trade idea but are maintaining our short GBP/CHF trade idea.

JPY Flows:

The monthly Balance of Payments data for March was released earlier this month and for FY25 the investment income surplus are larger than the current account surplus highlighting its growing dominance.

G10 FX Reactions to US CPI:

US CPI impact has shifted from volatile, persistent 2022 moves to muted post‑2023 pricing, with 2026 showing renewed USD‑driven, but less persistent, reactions.

FX Views

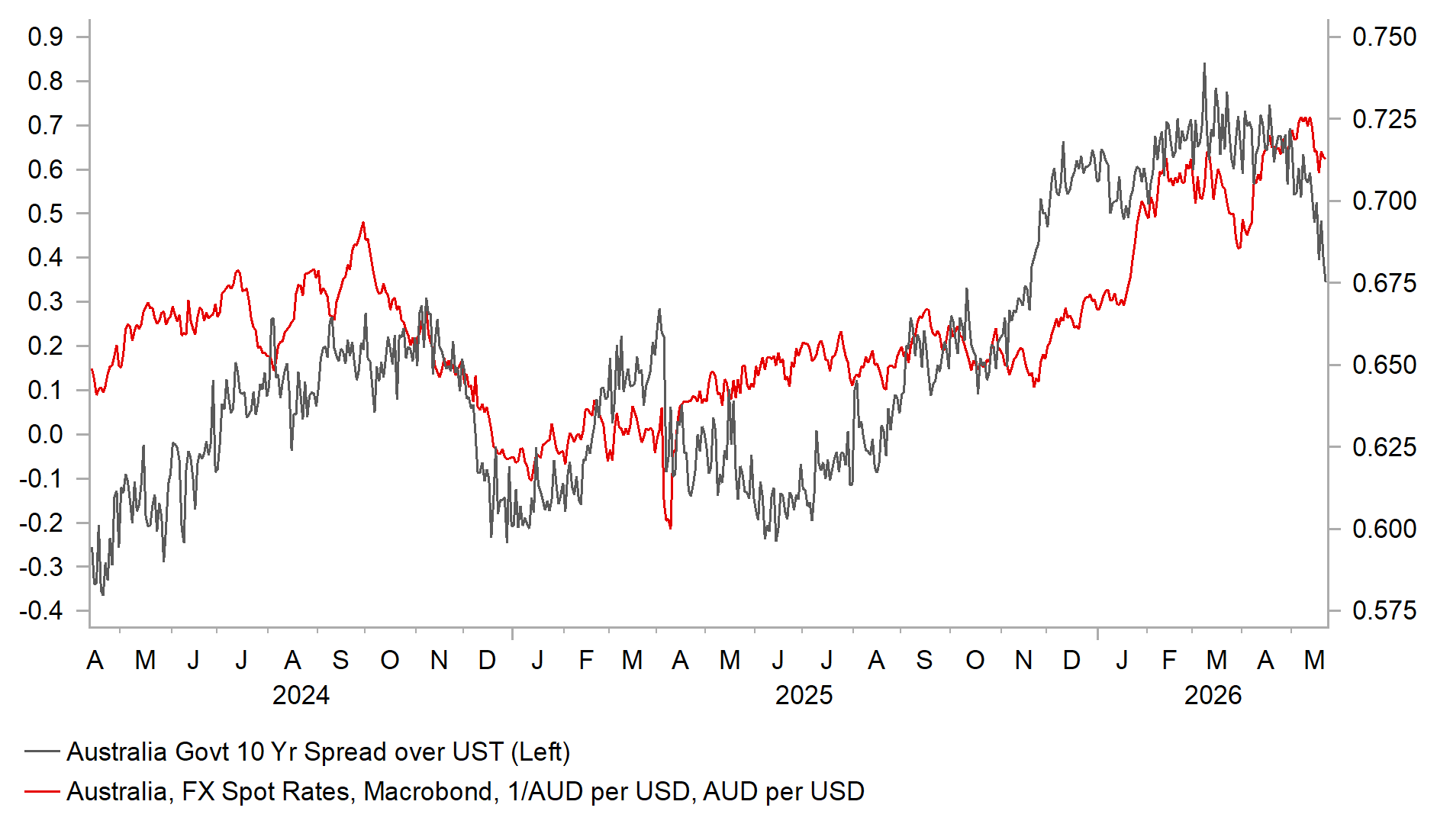

AUD: Advance could be running out of steam

The Australian dollar remains the second best performing G10 currency since the US-Iran conflict began at the end of February and price action and macro developments certainly suggest to us that the upside for AUD/USD from here is limited and the risks are now starting to skew more to the downside. The RBA has been the standout central bank taking a pro-active approach to tightening policy and had already hiked once before the conflict began but was not deterred in hiking two further times since. The remarkable period of strong risk appetite driven by stronger than expected corporate earnings in the tech sector due to AI could have run its course – that’s not to say we assume a downturn, just more that the scale of positive momentum is likely to ease considerably. That will likely leave the pro-cyclical global growth currencies, like AUD, more vulnerable to other macro and market developments.

We expect financial market participants to be more responsive to news and/or data suggesting the RBA has time to assess the policy stance. The pro-active approach from the RBA has afforded time and the minutes from the May meeting, released last week, revealed that “members agreed that the decision (to hike) would give the Board space” to assess the impact of the conflict on households and companies. Like elsewhere business and consumer confidence have plunged but the weakness in the labour market will certainly be most impactful on RBA decision making. The 18.6k decline in employment that lifted the unemployment rate to 4.5% (the highest since 2021) will ease RBA concerns given the minutes believed labour market conditions in aggregate “were still a little tight relative to full employment”. The RBA projects the unemployment rate at 4.7% by mid-2028, which could easily be too low considering the projection is now only 0.2ppt higher than the current level.

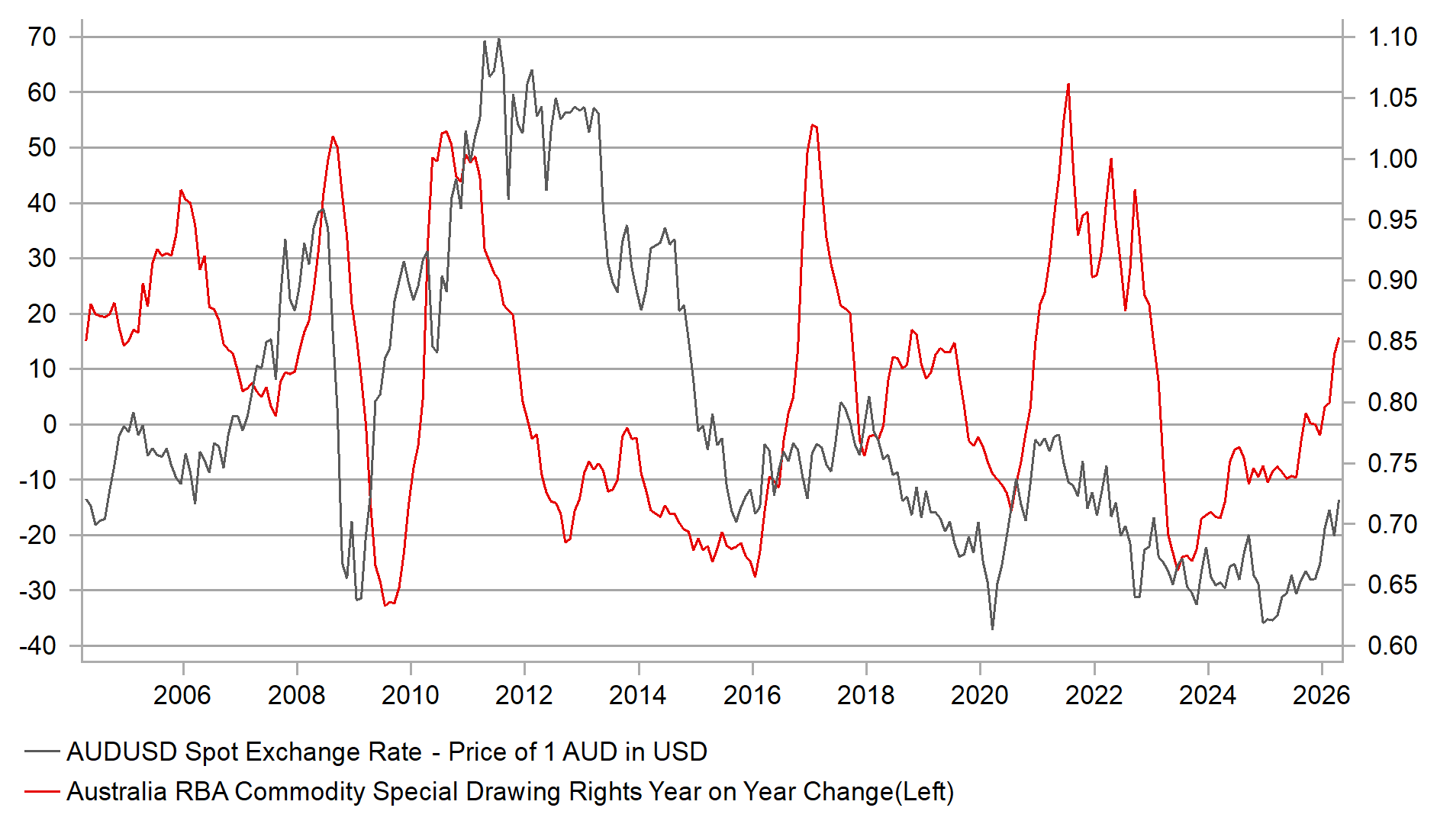

The importance of China for Australia’s external demand is well known and in 2025 Australia exported a little over USD 100bn worth of goods to China, equating to around 30% of total exports. China looks to be now slowing more notably even though export growth has held up. If global growth is weakening due to geopolitical uncertainties (seems likely from data available) then a further weakening of China GDP is probable. Data last week revealed YoY retail sales growth of just 0.2%, way below the post-covid period (since mid-2021) average of 3.6%. Industrial production growth was weaker than expected and fixed asset investment growth (ex-rural) contracted on a year-to-date basis (here). Any terms of trade benefit from the rise in natural gas prices for Australia could well be offset by weaker global growth, in particular in China. PMI data in Europe and the UK certainly point to weakening global growth conditions.

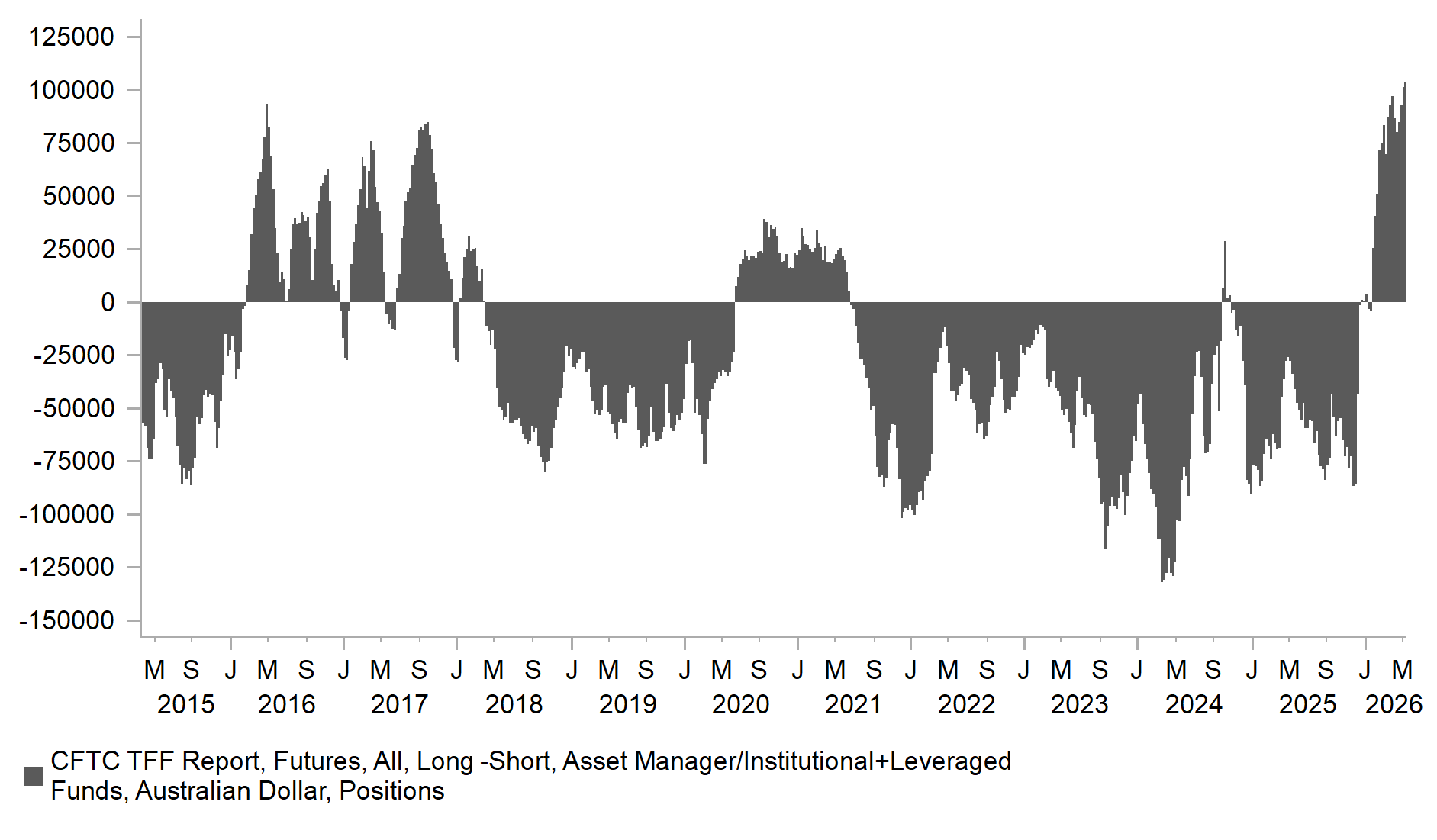

AUD LONG POSITIONS AT A RECORD HIGH

Source: Bloomberg, Macrobond & MUFG GMR

RBA COMMODITY PRICE INDEX YOY VS AUD/USD

Source: Bloomberg, Macrobond & MUFG GMR

The 2-year yield in the US hit a new high on Friday, closing at 4.12%, a 25bp move higher just in May to date and the highest level since February 2025. The move since the start of the conflict is big – approaching 80bps and hence we have certainly seen the bulk of a move higher. But the OIS market has a hike fully priced only by December now and we still see dangers of market pricing drifting further forward. A hike of course may not ultimately be delivered, depending on how Middle East developments play out but FOMC members could certainly turn more hawkish. A continued rise in YoY CPI is not necessarily required, merely the fact that inflation is not moving back lower would be the concern. Fed Governor Waller spoke on Friday and he now shares the view that an easing bias is no longer appropriate and that he would consider a rate hike if inflation “doesn’t abate soon”. He also suggested balance sheet shrinkage to the tune of USD 300-500bn was feasible. The US rates market has scope to move further higher.

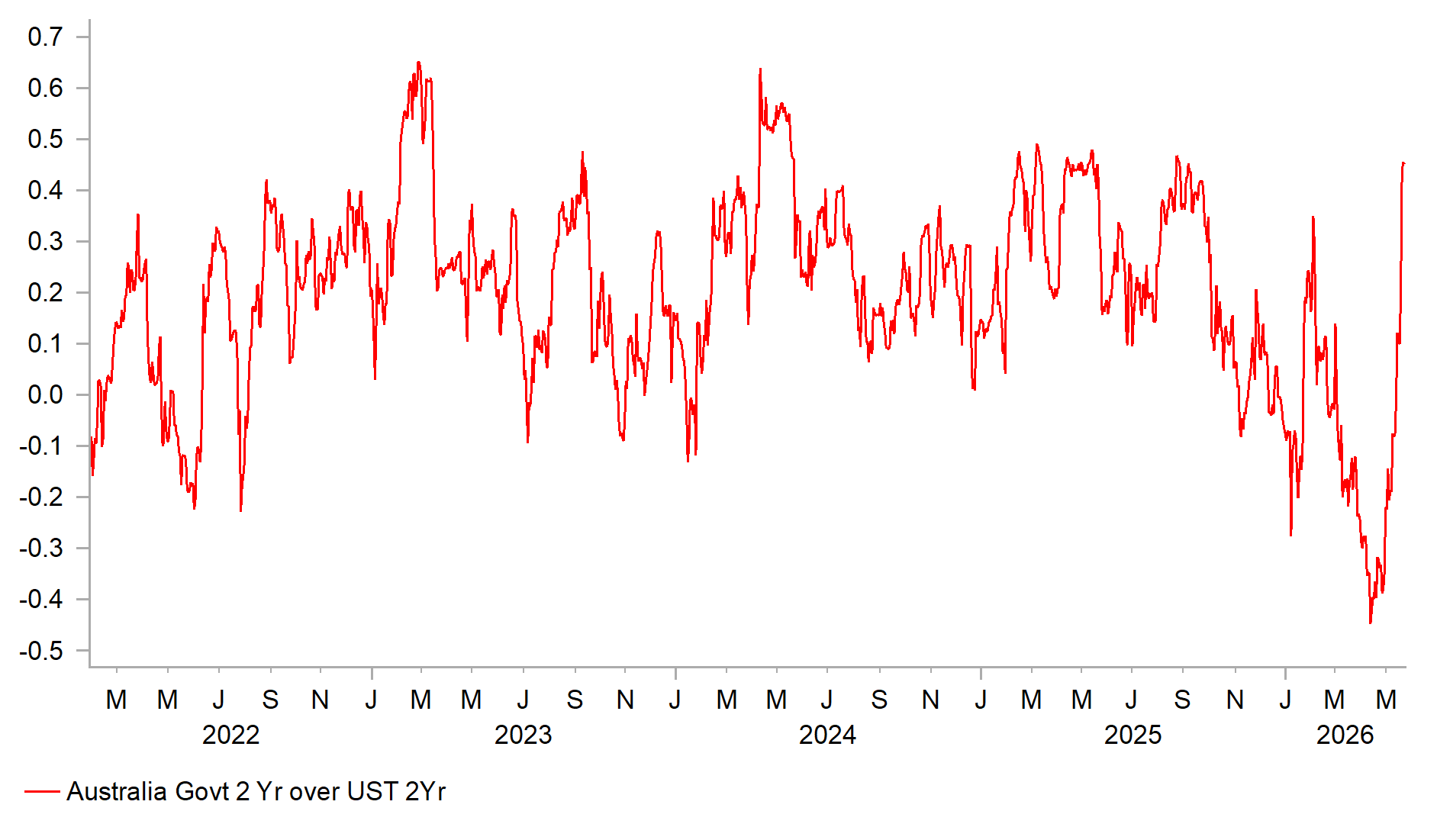

Over last week, the probability of a 25bp hike in September from the RBA dropped from 130% to around 80% while the probability of a Fed rate hike in the same month increased from 20% to around 55%. As we have highlighted recently, FX dynamics are changing and this is evident in AUD FX as well. During the initial stages of the Middle East conflict rate spreads were not the prominent driver of FX as risk and terms of trade dynamics were more prominent. Now through, in part due to rising US yields specifically, but also due to positive equity market momentum fading, the focus is shifting back to rate differentials. The daily correlation between AUD/USD and the AU-US 2-year spread has strengthened sharply and an extension of higher rates in the US as the RBA takes a backseat is going to increasingly weigh on AUD/USD. The move favouring the US dollar is further out the curve too with the 10-year AU-US yield spread now consistent with an AUD/USD move back toward the 0.68-level. Positioning risks also point to the potential to add to downside risks. The IMM position combined for AM/II and Leveraged Funds hit a new high of 103k in the week ending 12th May – that total is in fact a record in the series going back to 2006. Our z-score measure of stretched positions is also the biggest across currencies covered.

The prospects of a peace deal have increased significantly over the weekend and that may well see the AUD/USD rate move further higher from here as optimism picks up and some of the current pricing of a rate hike by the Fed is reversed. However, the RBA rate hike pricing could get pushed back as well and that will likely limit any dramatic change in relative short-term yield spreads. It is certainly too soon to make any strong calls on the inflation outlook. The risks of problematic inflation have come down but even if this deal is done and the Strait of Hormuz reopens, inflation pressures look set to continue through the second half of the year. A lot of the good news looks priced to us in AUD with upside scope still limited from here.

AUDUSD / YIELD 2YR SPREAD CORRELATION STRONGER

Source: Bloomberg, Macrobond & MUFG GMR

10YR AU-US YIELD SPREAD POINTS TO LOWER AUD/$

Source: Bloomberg, Macrobond & MUFG GMR

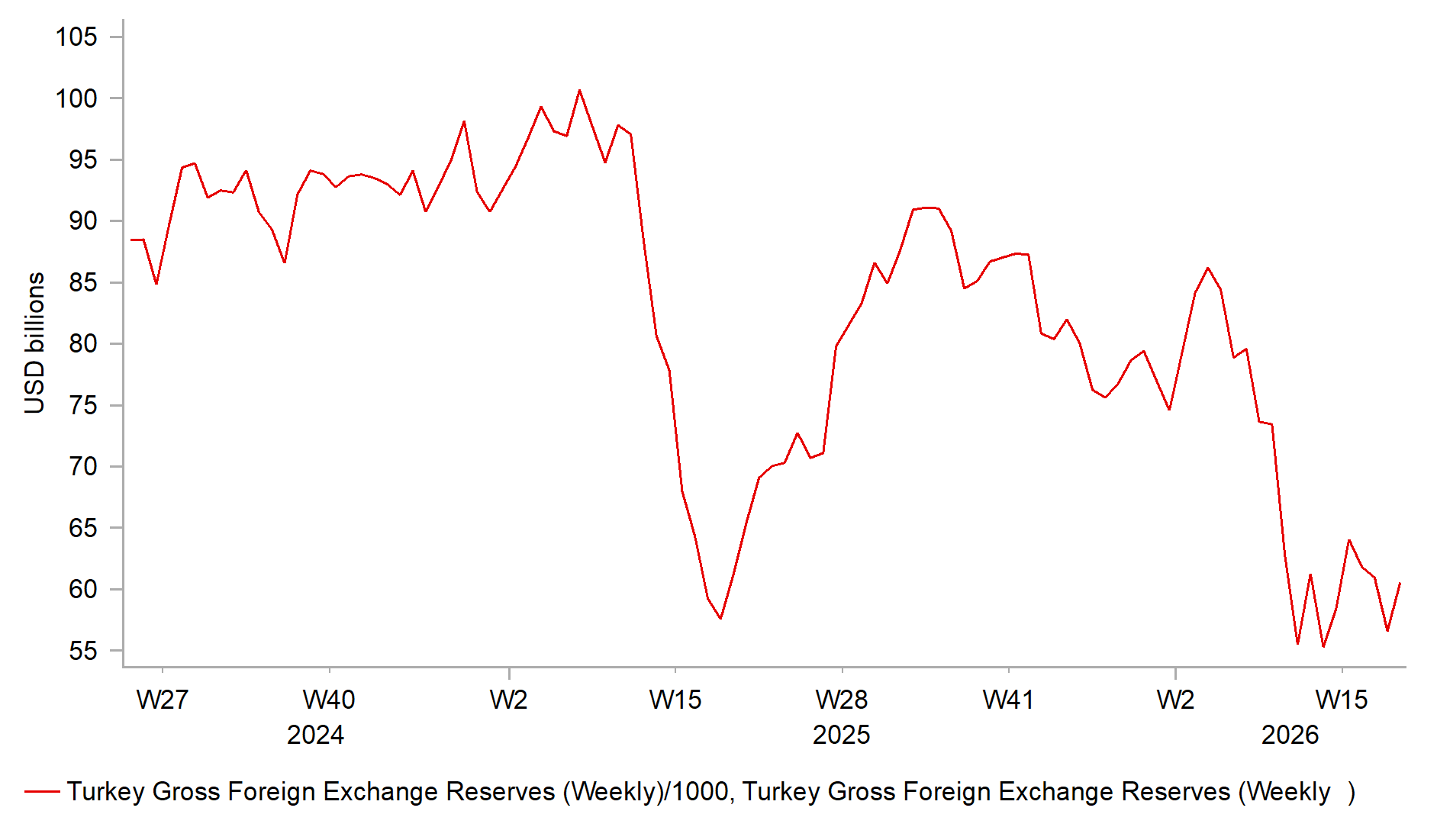

TRY: Domestic political adds to downside risks for TRY from energy shock

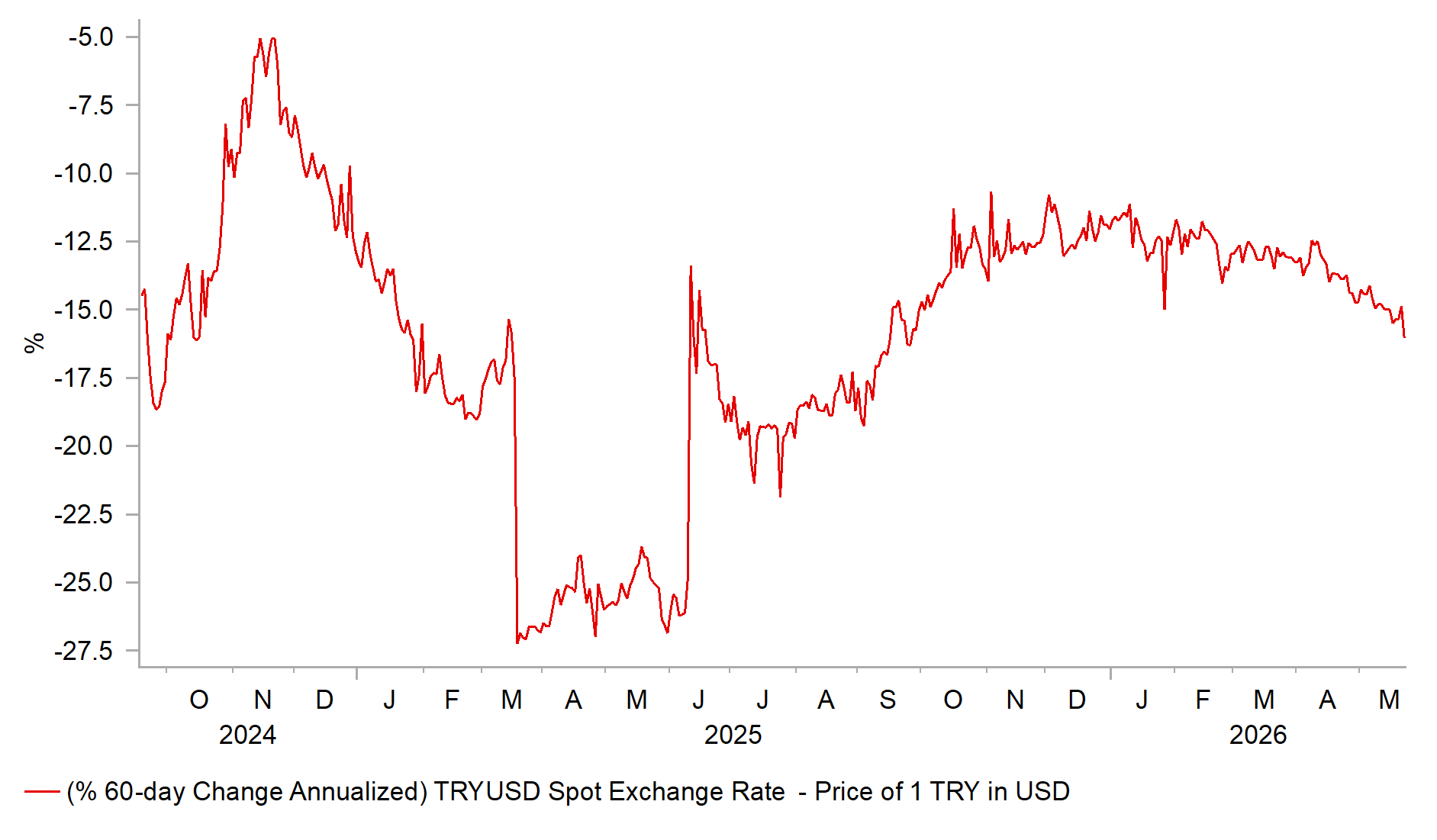

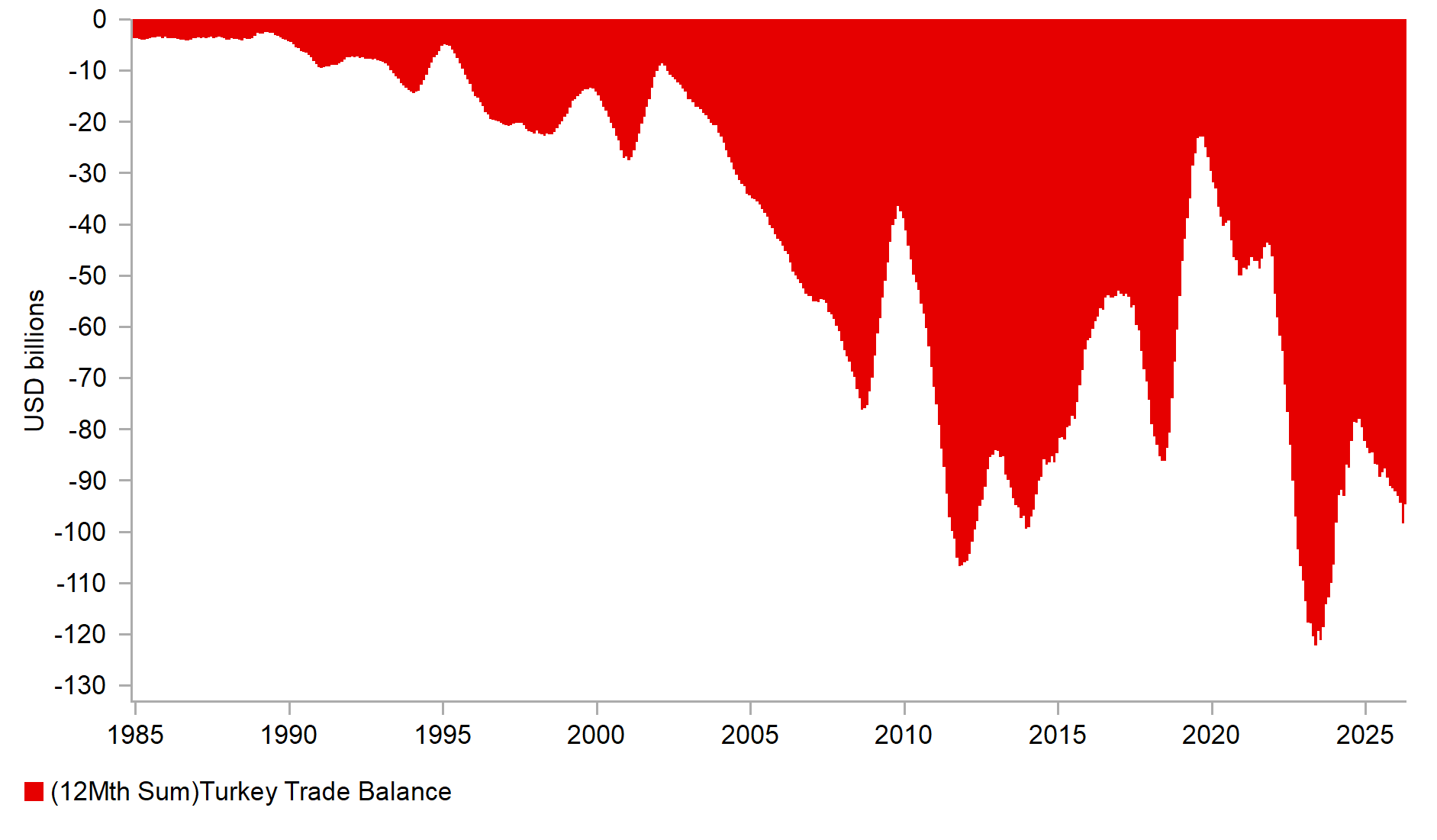

The pace of TRY depreciation has accelerated in recent months following the outbreak of military conflict between Iran and the US in late February. In the first three months of this year, the TRY depreciated at an annualised rate of just over 13% against the USD. Since the end of March, the pace of depreciation has picked up further, reaching an annualised rate of around 18% against the USD. Turkish policymakers have allowed the TRY to weaken as the Middle East conflict delivers a negative shock to the economy. Higher energy prices are generating an adverse terms of trade shock, while regional instability risks undermining tourism revenues. Reflecting these pressures, Turkey’s trade deficit widened to a cumulative total of just under USD 20 billion in March and April.

When the Middle East conflict first began, Turkey intervened aggressively to prevent a sharper sell-off in the TRY. According to Bloomberg, Turkey’s official reserves declined by around USD 43 billion in March. This included a reduction in gold holdings of approximately 58 tonnes, equivalent to about USD 8 billion at prevailing prices, with more than half utilised in swap transactions alongside outright sales. The drawdown in reserves also involved Turkey liquidating almost all of its US Treasury holdings. Treasury holdings fell to just USD 1.8 billion at the end of March, down from USD 16 billion in the previous month. Alongside FX intervention to support the TRY, the CBRT also tightened monetary policy modestly via the back door by shifting liquidity provision to the overnight lending rate of 40.00%. As a result, the weighted-average cost of CBRT funding increased by around 300 basis points.

After the sharp drawdown in March, reserves had stabilised over the past month until the latest adverse political developments in Turkey last week. An Ankara appeals court annulled the results of the Republican People’s Party’s (CHP) 2023 congress, voiding the election of Özgür Özel as party leader. The ruling reinstates the CHP’s previous leadership, including former party head Kemal Kılıçdaroğlu, and invalidates all decisions taken by the party since the 2023 congress. Özel had revitalised the main opposition party and delivered a significant setback to President Erdoğan’s ruling AK Party in the 2024 municipal elections. By contrast, under Kılıçdaroğlu’s leadership, the CHP lost the presidential election to Erdoğan in 2023. The CHP has indicated that it plans to appeal the ruling to a higher court. The decision is likely to further weaken the opposition and follows last year’s move to imprison Istanbul Mayor Ekrem İmamoğlu, the CHP’s presidential candidate. He was detained on 19th March 2025, triggering substantial capital outflows and prompting intervention by the CBRT to support the TRY. Bloomberg estimates that Turkey spent around USD 53 billion from net reserves at that time. In comparison, Bloomberg reports that Turkey initially spent around USD 6 billion to support the TRY following the latest court ruling against the CHP.

PACE OF TRY DEPRECIATION PICKS UP

Source: Bloomberg, Macrobond & MUFG GMR

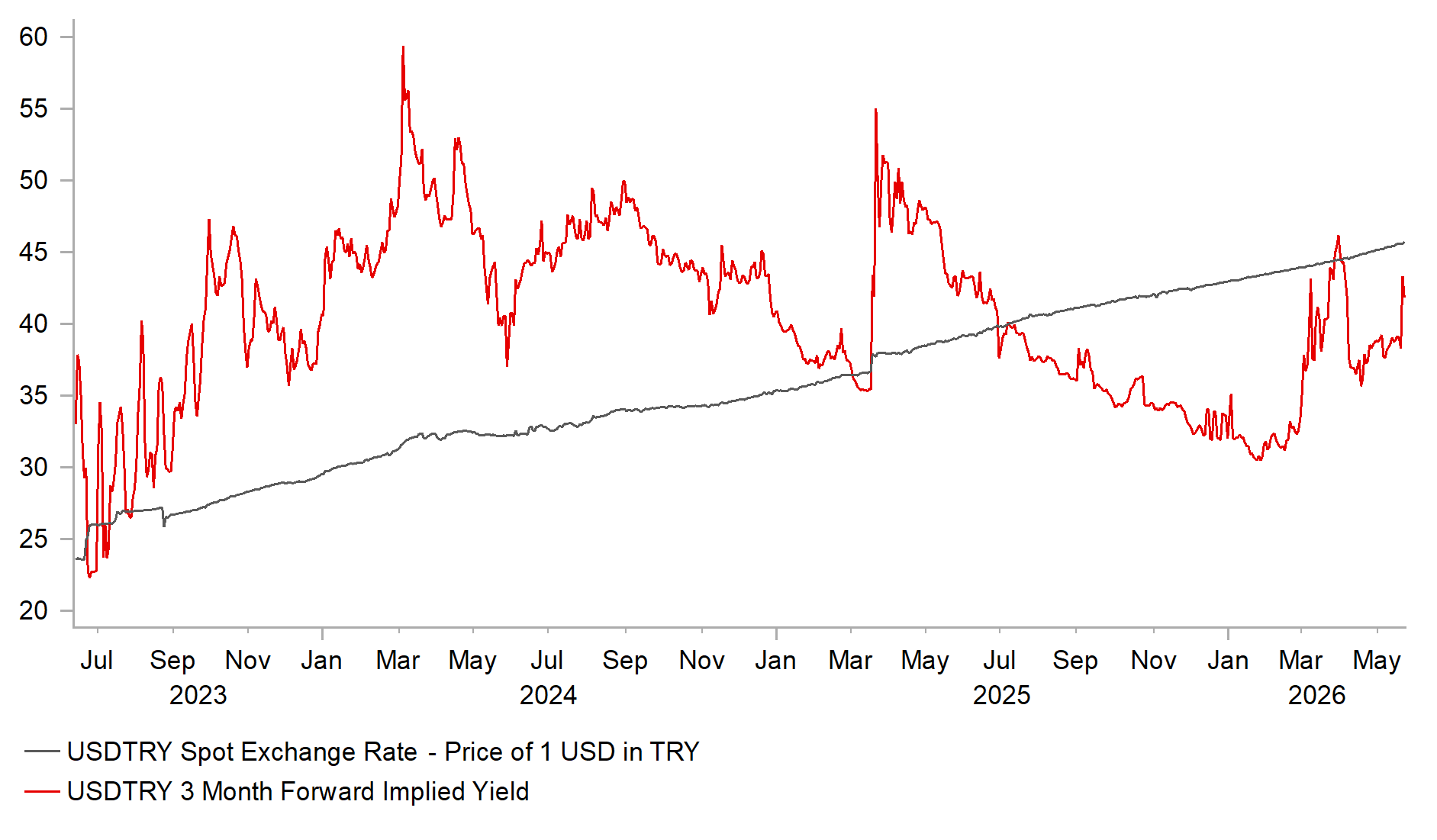

TRY CARRY TRADES BECOMING HIGHER RISK

Source: Bloomberg, Macrobond & MUFG GMR

The CBRT has less ammunition to support the TRY through reserves on this occasion. Bloomberg estimates that net reserves, excluding swaps, total just under USD 30 billion. Turkey has rebuilt its gold reserves, which have increased to around USD 110 billion and could be drawn upon further to support the currency. If pressure on the TRY continues to build driven by a combination of adverse domestic political developments and the risk of an intensifying Middle East conflict and energy price shock, it could trigger a sharper sell-off as Turkey’s reserves are depleted. Policymakers may therefore choose to allow greater currency weakness rather than continue attempting to smooth the pace of depreciation at the cost of further reserve losses. At the same time, a lower level of reserves could place additional pressure on the CBRT to tighten monetary policy to support the TRY, through a combination of rate hikes and macroprudential measures aimed at making the currency more attractive to domestic investors.

In light of these developments, we judge that upside risks have increased to our current forecasts for USD/TRY (click here) to rise up to 50.500 by year end. Our current forecast implied an annualized pace of depreciation of around -15% against the USD through the rest of this year. In our latest monthly FX Outlook report released at the start of next month, we plan to raise the USD/TRY forecasts to show annualized depreciation of closer to 20.0%. We also can’t exclude the risk of a bigger one-off devaluation for the TRY if the Middle East conflict/energy price shock moves into a more severe scenario for the global economy and Turkey’s economy. During the last energy price shock in 2022, the TRY fell by closer to 30% against the USD in the calendar year.

TURKEY’S WIDENING TRADE DEFICIT

Source: Bloomberg, Macrobond & MUFG GMR

FX RESERVE DRAWDOWN ADDS TO DOWNSIDE RISKS

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

Ccy | Date | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

GBP | 26/05/2026 | 11:00 | CBI Retailing Reported Sales | May | -- | - 68.0 | !! |

USD | 26/05/2026 | 14:00 | House Price Purchase Index QoQ | 1Q | -- | 0.8% | !! |

USD | 26/05/2026 | 15:00 | Conf. Board Consumer Confidence | May | 92.5 | 92.80 | !! |

AUD | 27/05/2026 | 02:30 | CPI YoY | Apr | -- | 4.6% | !!! |

NZD | 27/05/2026 | 03:00 | RBNZ Official Cash Rate | 2.25% | 2.25% | !!! | |

EUR | 28/05/2026 | 01:00 | ECB's Lane Speaks | !!! | |||

AUD | 28/05/2026 | 02:30 | Private Capital Expenditure | 1Q | -- | 0.4% | !! |

NOK | 28/05/2026 | 07:00 | GDP Mainland QoQ | 1Q | -- | 0.4% | !! |

EUR | 28/05/2026 | 10:00 | Economic Confidence | May | 92.5 | 93.0 | !! |

EUR | 28/05/2026 | 12:30 | ECB Account of April Rate Decision | !! | |||

CAD | 28/05/2026 | 13:30 | Current Account Balance | 1Q | -- | -$0.71b | !! |

USD | 28/05/2026 | 13:30 | Personal Spending | Apr | 0.5% | 0.9% | !! |

USD | 28/05/2026 | 13:30 | Core PCE Price Index MoM | Apr | 0.3% | 0.3% | !!! |

USD | 28/05/2026 | 13:30 | Durable Goods Orders | Apr P | 2.5% | 0.8% | !! |

USD | 28/05/2026 | 13:30 | Initial Jobless Claims | -- | 209k | !! | |

USD | 28/05/2026 | 13:30 | GDP Annualized QoQ | 1Q S | 2.0% | 2.0% | !!! |

USD | 28/05/2026 | 13:55 | Fed's Williams Speaks | !!! | |||

CAD | 28/05/2026 | 15:00 | BoC Releases Financial Stability Report | !! | |||

USD | 28/05/2026 | 15:00 | New Home Sales | Apr | 660k | 682k | !! |

CAD | 28/05/2026 | 16:00 | BoC's Macklem and Rogers Speak | !!! | |||

JPY | 29/05/2026 | 00:30 | Tokyo CPI YoY | May | 1.6% | 1.5% | !! |

JPY | 29/05/2026 | 00:50 | Retail Sales MoM | Apr | 0.4% | 1.3% | !! |

SEK | 29/05/2026 | 07:00 | GDP QoQ | 1Q | -- | 0.5% | !! |

EUR | 29/05/2026 | 07:45 | France CPI YoY | May P | -- | 2.2% | !! |

EUR | 29/05/2026 | 07:45 | France GDP QoQ | 1Q F | -- | - | !! |

EUR | 29/05/2026 | 08:55 | Germany Unemployment Change (000's) | May | -- | 20.0k | !! |

EUR | 29/05/2026 | 13:00 | Germany CPI YoY | May P | -- | 2.9% | !!! |

CAD | 29/05/2026 | 13:30 | Quarterly GDP Annualized | 1Q | -- | -0.6% | !!! |

USD | 29/05/2026 | 13:30 | Advance Goods Trade Balance | Apr | -$88.2b | -$87.9b | !! |

CAD | 29/05/2026 | 13:30 | GDP MoM | Mar | -- | 0.2% | !! |

Source: Bloomberg & MUFG GMR

Key Events:

The RBNZ is expected to leave its policy rate unchanged in the week ahead. Market participants will be watching closely to see whether it provides a strong signal on the potential for a rate hike as soon as the following meeting in July. New Zealand rate market participants are pricing in a high probability (around 16bps) of a hike at the July policy meeting and are nearly fully pricing in three hikes by the end of this year. Governor Breman has previously stated that the RBNZ is ready to act decisively and in a timely manner if there are signs that short-term inflation is feeding into more persistent pressures, in order to ensure inflation settles sustainably at 2% over the medium term. At the last policy meeting in April, the RBNZ signalled that if medium-term inflation pressures do not subside, then “decisive and timely increases in the OCR would be required.”

The main economic data release from the US in the week ahead will be the latest PCE deflator report for April. Evidence of a pickup in inflation in April from the latest CPI, PPI, and import price reports has encouraged US rate market participants to price in a higher probability of the Fed delivering multiple rate hikes. While the Fed has indicated that it is moving closer to dropping its easing bias, its communication does not fully support the recent hawkish repricing in the US rates market. A speech by New York Fed President Williams will also be closely scrutinised for any shifts in policy views among the more dovish members of the Fed leadership.

In Europe, we believe the ECB remains on track to raise rates as soon as next month despite evidence of slowing growth momentum in response to the energy price shock. ECB officials have indicated that a June hike is likely to address upside inflation risks. Chief Economist Lane is scheduled to speak in the week ahead, which could provide further insight into whether the ECB judges that the euro area economy is moving closer to the adverse scenario that would warrant only measured policy tightening. The release of the latest CPI reports from France and Germany for May will also offer further insight into the initial inflationary impact of the energy price shock.