Please download PDF from above for the following currencies.

Australian dollar // New Zealand dollar //Canadian dollar // Norwegian krone // Swedish Krona // Swiss franc // Czech koruna // Hungarian forint //Polish zloty // Romanian leu // Russian rouble // South African rand // Turkish lira // Indian rupee // Indonesian rupiah // Malaysian ringgit // Philippine peso //Singapore dollar // South Korean won // Taiwan dollar // Thai baht // Vietnamese dong // Argentine peso // Brazilian real // Chilean peso // Mexican peso // Saudi riyal // Egyptian pound

Monthly Foreign Exchange Outlook

DEREK HALPENNY

Head of Research, Global Markets EMEA and International Securities

Global Markets Research

Global Markets Division for EMEA

E: derek.halpenny@uk.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

E: lee.hardman@uk.mufg.jp

LIN LI

Head of Global Markets Research Asia

Global Markets Research

Global Markets Division for Asia

E: lin_li@hk.mufg.jp

KHANG SEK LEE

Associate

Global Markets Research

Global Markets Division for Asia

E: khangsek_lee@hk.mufg.jp

MICHAEL WAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for Asia

E: michael_wan@sg.mufg.jp

LLOYD CHAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for Asia

E: lloyd_chan@sg.mufg.jp

SOOJIN KIM

Analyst, ESG and Emerging Markets Research – EMEA

DIFC Branch – Dubai

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

May 2026

KEY EVENTS IN THE MONTH AHEAD

1) ON BLOCKADE WATCH

The Strait of Hormuz remains closed and crude oil prices advanced by 15% in April but this failed to disrupt risk appetite with the S&P 500 advancing by more than 10%. As a result, the US dollar fell by close to 2.0%. We view it as quite unlikely that we would get a repetition of that type of price action in equities if the Strait of Hormuz is still closed at the end of May and crude oil prices have had another large jump. Strong corporate earnings results have helped insulate equities from the rise in energy prices and from the rising risk that refined fuel shortages could start to disrupt economic activity over the coming months. At the time of writing there appears to be little impetus toward the blockade ending or appetite for the resumption of peace negotiations. That points to a rising probability of further energy price rises and a re-escalation of military conflict. We therefore maintain our forecast of near-term US dollar strength on a further rise in energy prices over the coming months before de-escalation is achieved and energy prices gradually decline in the second half of the year. The risk to that assumption is that the closure of the Strait of Hormuz drags on for longer and energy prices are higher still, resulting in a bigger risk-off at some point that sees the US dollar stronger than we expect. However the US-Iran stand-off plays out, we ultimately expect negative US dollar fundamentals to reassert themselves resulting in a weaker US dollar by the end of the year.

2) CENTRAL BANK WATCH

May will be quieter than April for central bank meetings with four G10 central banks meeting – the RBA (5th); the Norges Bank and the Riksbank (7th) and the RBNZ (27th) will meet with OIS pricing indicating that the RBA is most likely to hike followed by Norges Bank. A change in Fed leadership will also take place in May with Fed Chair Powell’s term ending on 15th with Kevin Warsh then set to assume the role. Warsh’s first FOMC meeting as Fed Chair will be 16th-17th June. There will also be some focus on the BoJ following the probable intervention on 30th April on behalf of the MoF. The MoF has not confirmed or denied the intervention and we may have to wait until 31st May when the MoF will release details of intervention activities settled in the month of May that would capture action on 30th April.

3) WILL THE XI-TRUMP MEETING PUT GUARDRAILS ON RIVALRY?

Markets are expecting the Xi–Trump meeting to happen on 14th-15th May. For FX markets, it presents asymmetric risks: the tail winds may be that both parties reaffirm a dialogue mechanism and cooperative channels, increase collaboration on global issues like climate change and fentanyl control. Marginal easing on tariff, relaxed trade restrictions on key products on both sides, and China to increase purchases of US goods could be tail winds too. The tail risks are there too—adverse signals on Taiwan, secondary sanctions tied to Iran, tighter AI/tech restrictions could quickly reprice geopolitical risk premia. We expect overall risk skews modestly to a slight improvement in sentiment, providing mild support for a stronger CNY and high beta regional currencies.

Forecast rates against the US dollar - End-Q2 2026 to End-Q1 2027

| Spot close | Q2 2026 | Q3 2026 | Q4 2026 | Q1 2027 |

DXY | 98.166 | 99.990 | 97.810 | 96.360 | 96.210 |

JPY | 156.66 | 158.00 | 156.00 | 154.00 | 152.00 |

EUR | 1.1728 | 1.1500 | 1.1800 | 1.2000 | 1.2000 |

GBP | 1.3578 | 1.3140 | 1.3410 | 1.3560 | 1.3480 |

CNY | 6.8277 | 6.8500 | 6.8300 | 6.8000 | 6.7800 |

AUD | 0.7183 | 0.7100 | 0.7150 | 0.7200 | 0.7300 |

NZD | 0.5890 | 0.5800 | 0.5900 | 0.6000 | 0.6050 |

CAD | 1.3611 | 1.3700 | 1.3600 | 1.3500 | 1.3400 |

NOK | 9.2924 | 9.4780 | 9.3220 | 9.2500 | 9.3330 |

SEK | 9.2492 | 9.4780 | 9.1530 | 8.9170 | 8.9170 |

CHF | 0.7824 | 0.7910 | 0.7710 | 0.7630 | 0.7670 |

|

|

|

|

|

|

CZK | 20.798 | 21.300 | 20.680 | 20.170 | 20.080 |

HUF | 310.84 | 317.40 | 309.30 | 300.00 | 300.00 |

PLN | 3.6309 | 3.7220 | 3.6100 | 3.5330 | 3.5170 |

RON | 4.4257 | 4.4780 | 4.3900 | 4.3330 | 4.3500 |

RUB | 74.675 | 75.880 | 75.860 | 77.060 | 79.820 |

ZAR | 16.706 | 17.000 | 16.700 | 16.300 | 16.000 |

TRY | 45.182 | 46.500 | 48.500 | 50.500 | 52.000 |

|

|

|

|

|

|

INR | 94.908 | 95.500 | 95.800 | 96.000 | 96.000 |

IDR | 17339 | 17000 | 16850 | 16700 | 16600 |

MYR | 3.9690 | 3.9000 | 3.8500 | 3.7500 | 3.7000 |

PHP | 61.463 | 62.000 | 61.500 | 61.000 | 60.500 |

SGD | 1.2740 | 1.2750 | 1.2600 | 1.2600 | 1.2500 |

KRW | 1478.0 | 1480.0 | 1470.0 | 1460.0 | 1450.0 |

TWD | 31.648 | 31.800 | 31.500 | 31.300 | 31.100 |

THB | 32.525 | 33.400 | 33.000 | 32.500 | 32.000 |

VND | 26348 | 26400 | 26500 | 26600 | 26700 |

|

|

|

|

|

|

ARS | 1378.6 | 1450.0 | 1500.0 | 1550.0 | 1650.0 |

BRL | 4.9793 | 5.0000 | 5.1000 | 4.9000 | 4.8000 |

CLP | 902.04 | 920.00 | 900.00 | 880.00 | 860.00 |

MXN | 17.519 | 17.750 | 17.750 | 17.500 | 17.500 |

|

|

|

|

|

|

SAR | 3.7502 | 3.7500 | 3.7500 | 3.7500 | 3.7500 |

EGP | 53.570 | 49.000 | 49.500 | 50.500 | 52.500 |

Notes: All FX rates are expressed as units of currency per US dollar bar EUR, GBP, AUD and NZD which are expressed as dollars per unit of currency. Data source spot close; Bloomberg closing rate as of 5:00pm London time, except VND which is local onshore closing rate. All consensus forecasts are Bloomberg sourced.

US dollar

Spot close 30.04.26 | Q2 2026 | Q3 2026 | Q4 2026 | Q1 2027 | |

USD/JPY | 156.66 | 158.00 | 156.00 | 154.00 | 152.00 |

EUR/USD | 1.1728 | 1.1500 | 1.1800 | 1.2000 | 1.2000 |

Consensus | Consensus | Consensus | Consensus | ||

USD/JPY | 157.00 | 155.00 | 153.00 | 152.00 | |

EUR/USD | 1.1700 | 1.1900 | 1.2000 | 1.2000 |

MARKET UPDATE

In April the US dollar weakened against the euro in terms of London closing rates, from 1.1524 to 1.1728. In addition, the dollar weakened against the yen, from 159.00 to 156.66. The FOMC at its meeting in April kept the range for the federal funds unchanged at 3.75%-4.00%. The FOMC confirmed the end of QT effective December last year with the Fed no longer reducing UST bond holdings. MBS holdings continue to decline but will be offset by buying of US T-bills, now estimated to be running at around USD 25bn per month.

OUTLOOK

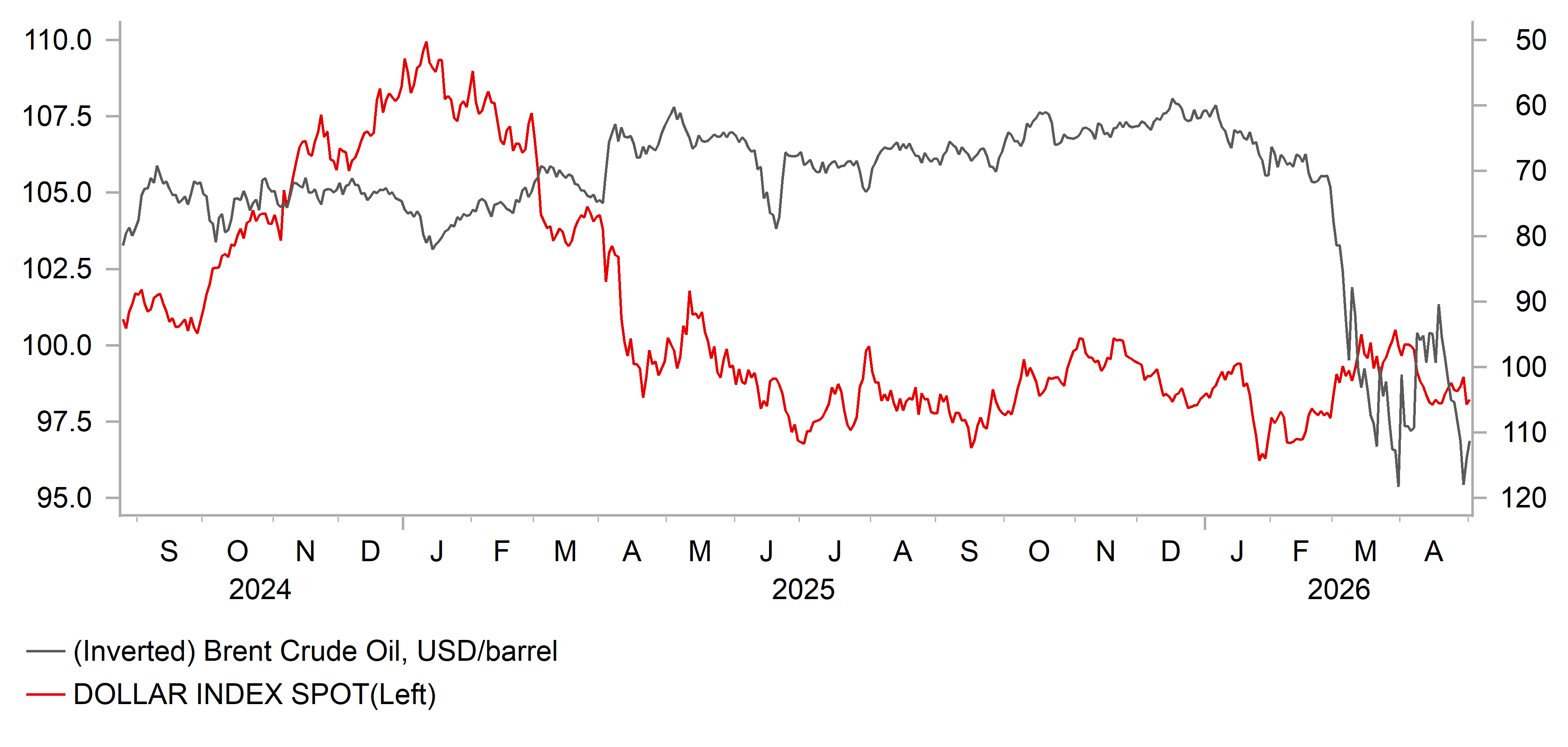

The US dollar, on a DXY basis, declined by 1.9% in April and given where Brent crude oil closed out April the US dollar move is certainly surprising. We would point to the resilience in risk assets as an important factor in limiting the appetite for buying the dollar. While Brent gained by 15% in April and hit a new high since the conflict began, the S&P 500 advanced by 10.4%. We see two factors helping explain this. Firstly, crude oil prices simply have not yet reached levels that justify pricing more notably the risk of global recession. In inflation-adjusted terms, crude oil prices remain relatively low. Secondly with close to one-third of US companies having reported Q1 earnings results, S&P 500 companies are on track for a 15% YoY gain in earnings growth, the sixth consecutive quarter of double-digit earnings growth. However, we believe this risk dynamic could change abruptly and if crude oil prices continue to advance, we would expect a bigger equity market correction and we would assume with that would come a more notable gain for the US dollar.

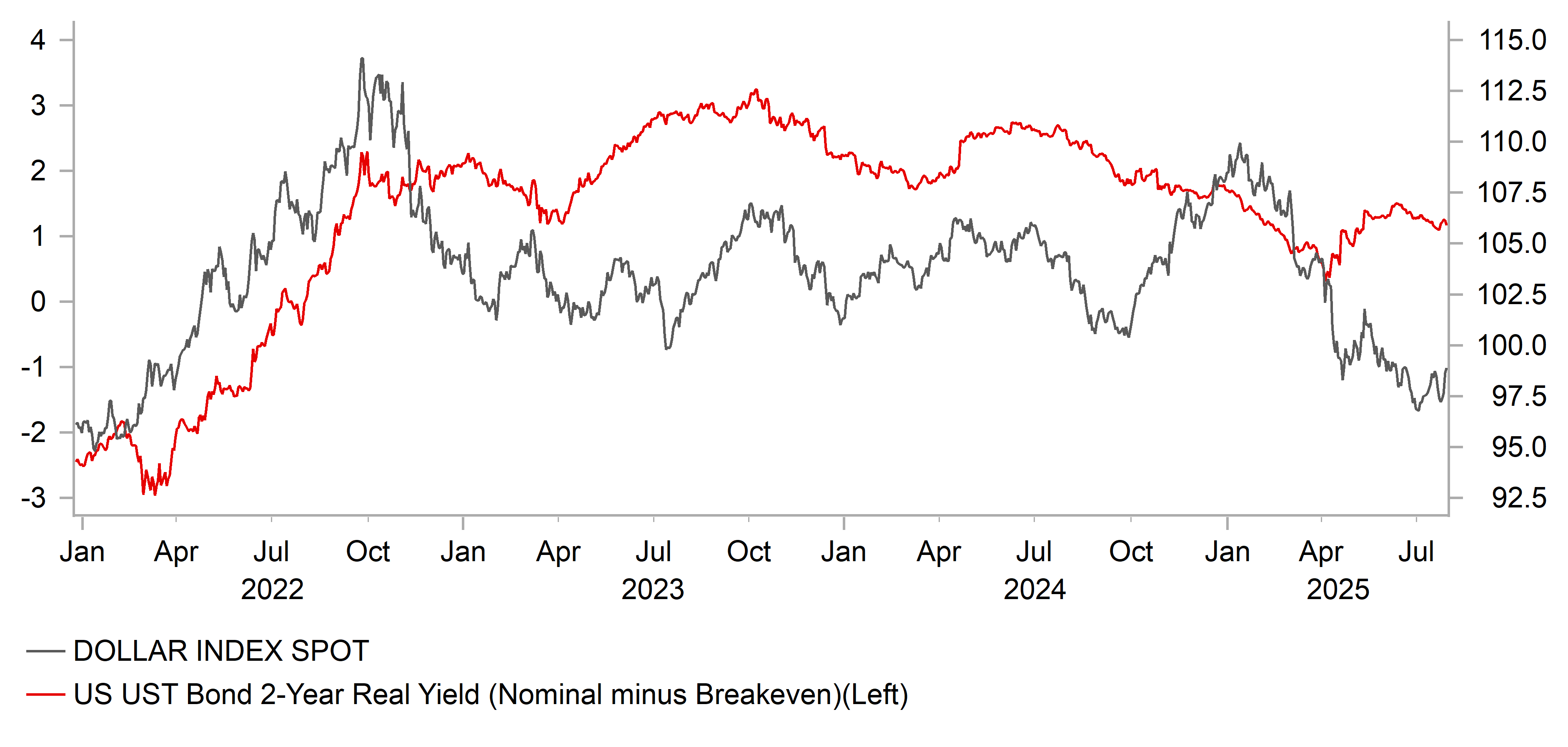

Front-end yields did increase in April with the FOMC meeting revealing a shift of sorts toward a more hawkish stance. Three FOMC members dissented to the wording in the statement that implied the bias remains to cut rates further. Steve Miran dissented the other way, favouring a 25bp cut. With Fed Chair Powell confirming he will remain on the Board of Governors after he steps down as Chair, the required room for Kevin Warsh to come on to the board will mean Miran has to leave, resulting in some degree of shift to a less dovish composition of the FOMC board. We still see scope for rate cuts toward the end of the year in a scenario in which crude oil prices retrace lower on de-escalation. Still, the risk to that view is that the Strait of Hormuz remains closed for longer and inflation is higher but mixed with weak labour market condition means the Fed stays on hold for longer.

We see risks of renewed military escalation in the Middle East that could see crude oil extend gains and prompt a bigger risk-off move. While the dollar has performed poorly given the current backdrop we still see scope for dollar gains over the short-term on the assumption of a bigger risk-off move. We still though assume we get to a de-escalation scenario around end-Q2 and expect oil prices to gradually decline in H2. The fundamental backdrop for the dollar remains poor – cyclical & Trump related policy uncertainties – and hence assume dollar depreciation resumes in H2 2026.

INTEREST RATE OUTLOOK

| Interest Rate Close | Q2 2026 | Q3 2026 | Q4 2026 | Q1 2027 |

Policy Rate | 3.64% | 3.63% | 3.38% | 3.13% | 3.13% |

3-Month T-Bill | 3.66% | 3.65% | 3.30% | 3.10% | 3.10% |

10-Year Yield | 4.37% | 4.25% | 4.00% | 3.88% | 3.88% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

Powell’s last FOMC meeting and developments in the Iran War have moved markets and our view incrementally less dovish. At the latest FOMC meeting rates remained unchanged and they kept the “additional” qualifier in the statement (which denotes an easing bias). This outcome revealed heightened divisions within the Fed, as several dissenters favored removing the dovish bias. Overall, this will make it more difficult for Warsh to convince the board of early rate cuts and reduces the likelihood that the Fed will cut in July. Unless financial markets experience acute tightening and/or war inflation effects fade quickly, it’s challenging to see imminent cuts at this point. Therefore, we have changed our rate forecast to include one less cut, with two cuts later in the year, given our view that restrictive policy is adversely impacting small-mid sized firms, housing, and interest rate sensitive sectors. While the war in Iran keeps oil prices and headline inflation elevated in the short term, we expect mild passthrough impacts to core inflation as higher oil prices spur demand destruction. We have shifted our rate forecast up by 12.5-25bps across the curve at various points for the forecast horizon to reflect a Fed on hold for longer.

(George Goncalves)

DXY VS. BRENT CRUDE OIL

Source: Bloomberg, Macrobond & MUFG GMR

DXY VS. REAL US 2YR YEILDS

Source: Bloomberg, Macrobond & MUFG GMR

Japanese yen

| Spot close 30.04.26 | Q2 2026 | Q3 2026 | Q4 2026 | Q1 2027 |

USD/JPY | 156.66 | 158.00 | 156.00 | 154.00 | 152.00 |

EUR/JPY | 183.73 | 181.70 | 184.10 | 184.80 | 182.40 |

|

| Consensus | Consensus | Consensus | Consensus |

USD/JPY |

| 157.00 | 155.00 | 153.00 | 152.00 |

EUR/JPY |

| 184.00 | 184.00 | 184.00 | 181.00 |

MARKET UPDATE

In April the yen strengthened versus the US dollar in terms of London closing rates from 159.00 to 156.66. However, the yen weakened marginally versus the euro from 183.23 to 183.73. The BoJ at its meeting in April kept the key policy rate unchanged at 0.75%, following the 25bp hike in December, the second 25bp rate hike since 2007. The BoJ is also continuing with the policy of cutting JGB monthly purchases and as was previously announced, the pace of reduction was reduced from JPY 400bn per quarter to JPY 200bn per quarter effective from April.

OUTLOOK

The yen strengthened in April with all of the gain coming on the last trading day of April after Vice Finance Minister for International Affairs Atsushi Mimura gave a “final warning” against speculative selling of the yen. The MoF has not formally confirmed that yen-buying intervention took place, but the 5-big figure drop in USD/JPY following his warnings is a strong indication that intervention took place. The Nikkei reported that intervention took place, usually a credible source. We are unconvinced that this will prove successful. The intervention has taken place against a backdrop of a large energy-related terms of trade shock and a notable rise in global yields relative to Japan. The MoF has cited speculative yen selling as a factor (if intervention took place) but IMM data and OTC margin retail positioning data suggest speculative short yen positions are a lot smaller than in 2024 when intervention last took place.

The yen had weakened in April (prior to the final day) despite the BoJ providing a stronger signal that it could well be in a position to raise the policy rate, possibly at the next meeting in June. The vote for unchanged rates in April was 6-3, highlighting a growing shift toward a hike. We believe the updated forecasts from the BoJ are also a strong indication on the need for a rate hike. As you would expect following the surge in energy prices, the CPI forecasts for this fiscal year were increased notably but the FY27 forecasts were also raised considerably with the core-core annual CPI rate revised from 2.1% to 2.6%. The FY28 forecast was 2.2%. The message from these forecasts is clear to us – the price stability mandate has been met, and the risks are skewed to the upside. The BoJ statement also referred to paying “due attention” to ensuring there is no upside deviation from the price stability goal. The market reaction to the BoJ communications was muted in part due to Governor Ueda’s perceived caution on signalling a rate hike – he stated that the certainty of meeting our baseline “has declined quite significantly”. Based on our assumption of de-escalation and a gradual resumption of energy supply, we see inflation conditions as being consistent with the BoJ hiking its key policy rate by 25bps in June.

Higher global yields and resilient risk appetite is an attractive mix for selling the yen. There are risks of a retracement back higher through the 160.00-level again but we see intervention and the probability of a June rate hike from the BoJ as curtailing the upside scope from here and ultimately then expect gradual yen appreciation.

INTEREST RATE OUTLOOK

| Interest Rate Close | Q2 2026 | Q3 2026 | Q4 2026 | Q1 2027 |

Policy Rate | 0.75% | 1.00% | 1.00% | 1.25% | 1.25% |

3-Month Bill | 0.81% | 1.10% | 1.10% | 1.30% | 1.30% |

10-Year Yield | 2.53% | 2.50% | 2.50% | 2.60% | 2.60% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The higher inflation risks due to the continued closure of the Strait of Hormuz continue to put upward pressure on yields with the 10-year JGB yield increasing 18bps to close at 2.53%. The macro backdrop of rising energy prices, continued loose monetary policy and an undervalued yen is certainly conducive to a continued grind higher in yields. An added danger for longer-term yields would be a decision by the government to increase support measures for households dealing with another rise in the cost of living. The BoJ at its meeting in April was again protrayed as a central bank being overly cautious in raising rates with the danger now being that fears over being behind the curve are rising again. The core-core annual CPI forecast for FY27 at 2.6% and at 2.2% in FY28 suggest a need to hike and bring the real policy rate closer to a neutral range for R*. Even in a scenario of a gradual retracement in crude oil prices following the re-opening of the Strait of Hormuz we see rate hikes as required and hence we expect to see a continued gradual rise in the 10-year JGB yield over the coming quarters.

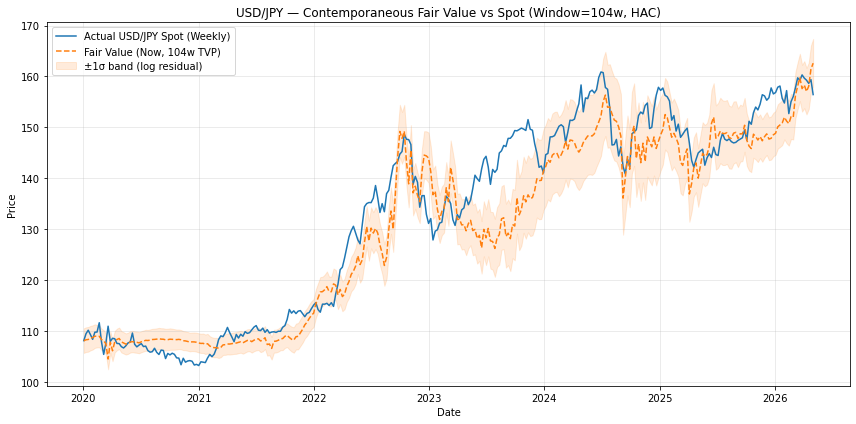

USD/JPY FAIR VALUE MODELLING

Source: Bloomberg & MUFG GMR

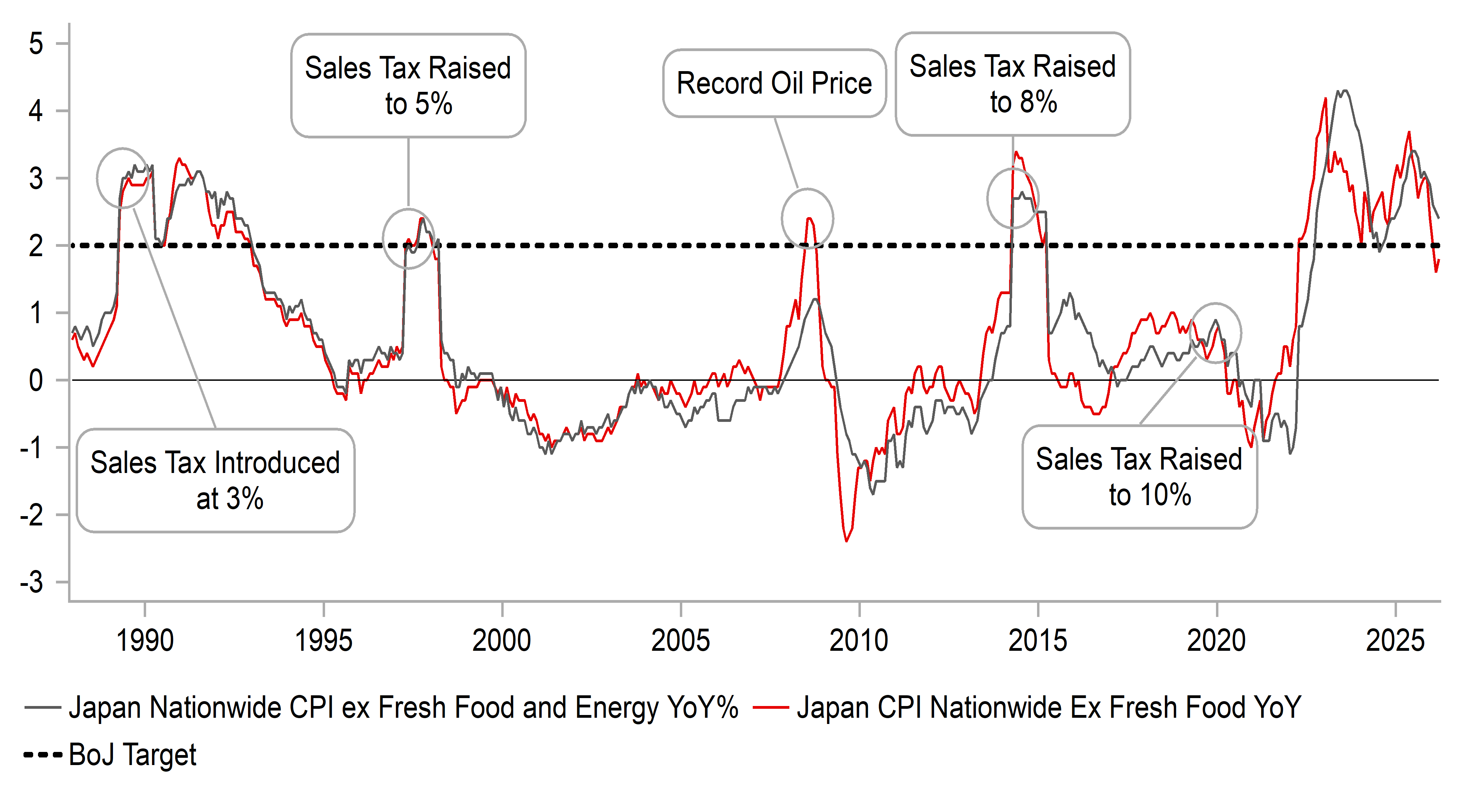

CORE CPI VS. BOJ TARGET

Source: Bloomberg, Macrobond & MUFG GMR

Euro

| Spot close 30.04.26 | Q2 2026 | Q3 2026 | Q4 2026 | Q1 2027 |

EUR/USD | 1.1728 | 1.1500 | 1.1800 | 1.2000 | 1.2000 |

EUR/JPY | 183.73 | 181.70 | 184.10 | 184.80 | 182.40 |

|

| Consensus | Consensus | Consensus | Consensus |

EUR/USD |

| 1.1700 | 1.1900 | 1.2000 | 1.2000 |

EUR/JPY |

| 184.00 | 184.00 | 184.00 | 181.00 |

MARKET UPDATE

In April the euro strengthened against the US dollar in terms of London closing rates from 1.1524 to 1.1728. The ECB at its meeting in April left the deposit rate unchanged at 2.00% - the level reached following 100bps of cuts last year. The cumulative easing amounted to 200bps over 2024-25. QT will continue this year with the ECB’s projected maturities from both APP and PEPP expected to result in a EUR 500bn reduction in balance sheet holdings.

OUTLOOK

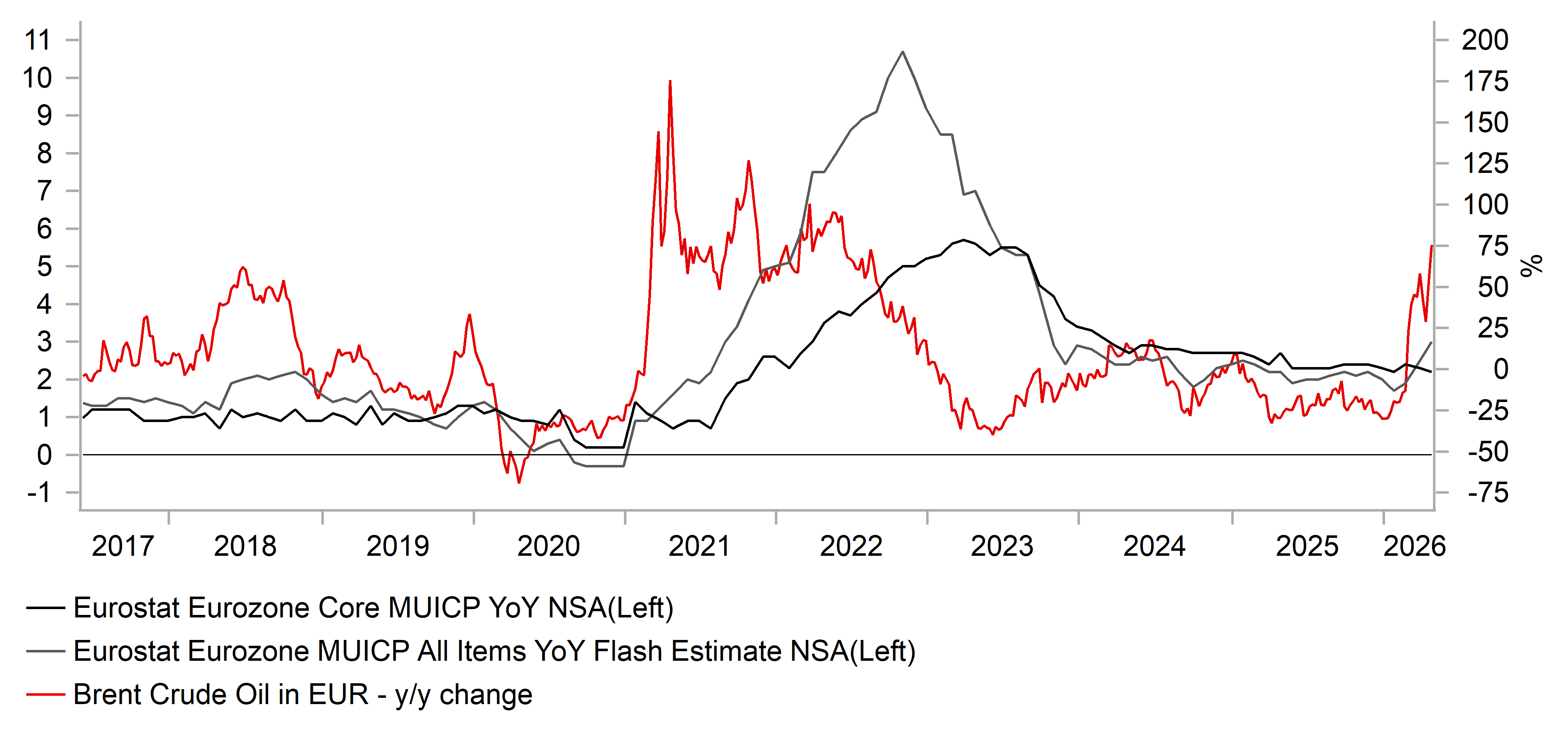

The euro advanced in April versus the US dollar, like all G10 currencies but the euro lagged the rest of G10 and advanced versus the dollar by less than all the other G10 currencies, although the yen’s outperformance reflected probably yen-buying intervention at month-end. The more subdued gain for the euro reflects the potential uncertainties that lie ahead of the Strait of Hormuz remains closed for longer than expected. Europe is more vulnerable to refined fuel shortages with exposure to the Middle East significant. Around 50% of the EU’s imported jet fuel comes via the Strait of Hormuz with about 20% of imported diesel impacted. The focus now for the euro-zone economy and potentially then for the euro is the possible tipping point in which scarcity of refined products begins to hit economic activity. Argus, the independent energy market intelligence provider, cites increased output at the Amsterdam-Rotterdam-Antwerp as helping keep diesel supplies strong, but inventories are also now being run down with diesel and other gasoil inventories down 11% in the last two weeks, hitting an eight-month low. The IEA estimates a tipping point in jet fuel becoming scarce sometime in June. The risks of macroeconomic impact are rising, and hence the risks are skewed over the near-term to the euro drifting lower.

Moving beyond that tipping point with the Strait of Hormuz still closed would certainly result in risk assets getting hit as investors reassess the risk of recession. That scenario would probably not deter the ECB from hiking and the communication from ECB President Lagarde following the meeting in April was certainly consistent with a rate hike being delivered in June. Lagarde stated “I know the direction rates are heading” and added that no resolution to the conflict by June would be “significant”. The ECB, Lagarde admitted in April, had debated various options including a rate hike. The OIS market is now priced to reflect the ECB acting to curtail upside inflation risks. A hike in June and September are fully priced. We had initially assumed a rate hike in April and June and have now pushed those hikes out – to June and then another in September.

The risk of military re-escalation is high but the Strait of Hormuz remaining closed further into Q2 is likely to lead to greater risk aversion and risks of economic disruption in Europe is growing and we believe will see EUR/USD move lower. We maintain that de-escalation will then take place and see scope for EUR/USD to retrace back higher to the 1.2000-level by year-end.

INTEREST RATE OUTLOOK

| Interest Rate Close | Q2 2026 | Q3 2026 | Q4 2026 | Q1 2027 |

Policy Rate | 2.00% | 2.25% | 2.50% | 2.50% | 2.50% |

3-Month Bill | 2.15% | 2.45% | 2.60% | 2.55% | 2.50% |

10-Year Yield | 3.04% | 3.10% | 3.00% | 2.90% | 2.70% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The 10-year German bund yield was close to unchanged in April, closing 4bps higher at 3.04% with the yield dropping 7bps on the final trading day of April following the ECB policy meeting. The ECB meeting coincided with some decline in crude oil prices and the rates market was already well priced for rate hikes to come and with the meeting communications already aligned with market pricing we saw some retracement in the 10-year. We are maintaining our call for two ECB rate hikes but now expect those to be delivered at the June and September meetings. The resilience of global equity markets makes the prospect of rate hikes more likely but there are risks both ways. A longer closure of the Strait of Hormuz and a more damaging hit to economic activity could see a bigger hit to risk assets that provides a disinflationary force to counter some of the inflation risks which could mean the 10-year Bund yield is lower than expected. Rate hikes from the ECB should also help contain longer-term yields and if ECB rate hikes are delivered and this coincides with de-escalation and a gradual decline in energy prices, then we see scope for 10-year yields to ultimately decline modestly from 2H onwards.

HEADLINE CPI VS. CORE VS. BRENT CRUDE OIL

Source: : Bloomberg, Macrobond & MUFG GMR

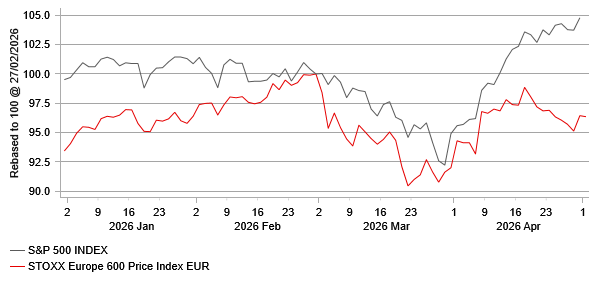

US VS. EZ EQUITY PERFORMANCE

Source:: Bloomberg, Macrobond & MUFG GMR

Pound Sterling

| Spot close 30.04.26 | Q2 2026 | Q3 2026 | Q4 2026 | Q1 2027 |

EUR/GBP | 0.8638 | 0.8750 | 0.8800 | 0.8850 | 0.8900 |

GBP/USD | 1.3578 | 1.3140 | 1.3410 | 1.3560 | 1.3480 |

GBP/JPY | 212.71 | 207.70 | 209.20 | 208.80 | 204.90 |

|

| Consensus | Consensus | Consensus | Consensus |

GBP/USD |

| 1.3400 | 1.3500 | 1.3500 | 1.3600 |

MARKET UPDATE

In April the pound strengthened versus the dollar in terms of London closing rates, moving from 1.3203 to 1.3578. In addition, the pound strengthened against the euro from 0.8728 to 0.8638. The MPC at its meeting in April left the key policy rate unchanged at 3.75%, after six 25bp cuts since August 2024.

OUTLOOK

The pound advanced in April and was the third best performing G10 currency in April with only the Australian dollar and Norwegian krone outperforming. The pound may have been supported by the notable jump in yields with the Gilt yield curve jumping far more than in Europe or the US. Gilt investors remain more sensitive to inflation risks in the UK and market-based inflation expectations have jumped more in the UK. The 5y5y inflation swap rate is up close to 15bps on a year-to-date basis, more than the gains in the euro-zone or US. The data in the UK has been mixed but GDP readings suggest that the economy was stronger than expected going into the Middle East conflict – the 3mth/3mth GDP gain in February was 0.5% with industrial production up 0.5% MoM in February. However, the sentiment data does point to the probability of a more abrupt downturn if the Middle East conflict drags on. The CBI Business Optimism index fell from -19 in Q1 to -65 in Q2, which when covid is excluded, was the worst reading since Q3 1980.

The BoE at its meeting in April revealed renewed divisions over the policy outlook with a 8-1 vote to keep rates on hold – Huw Pill voted to hike the key policy rate by 25bps. The Monetary policy Report was also released, and the BoE laid out scenarios as a guide to possible monetary actions ahead. All three scenarios indicated the probable need for a rate hike. The middle scenario, closest to our assumption of de-escalation and a gradual decline in energy prices involved the MPC hiking between two and three occasions. We now expect two rate hikes.

PM Starmer has been politically wounded ahead of the local elections taking place on 7th May. The parliamentary vote on whether Starmer should face an ethics inquiry was won by the government, but 15 Labour MPs voted with the opposition and 53 Labour MPs did not vote. His backbench support is weakening, and Labour is expected to perform poorly in the local elections. The risk of a leadership challenge is certainly growing and a move to remove Starmer over the summer ahead of the annual political party conference season is high. If this was to happen at a time of a further rise in crude oil prices, a renewed sell-off in the Gilt market could certainly begin to play a role in undermining pound performance.

Yields has played a role in providing the pound with support, but political instability and fiscal risks could well begin to de-stabilise the Gilt market once again and result in the pound losing its support from higher yields. We see scope for the pound to underperform the euro as the US dollar weakens more broadly.

INTEREST RATE OUTLOOK

| Interest Rate Close | Q2 2026 | Q3 2026 | Q4 2026 | Q1 2027 |

Policy Rate | 3.75% | 4.00% | 4.25% | 4.25% | 4.00% |

3-Month Bill | 3.96% | 4.15% | 4.35% | 4.30% | 3.95% |

10-Year Yield | 5.01% | 5.10% | 5.00% | 4.80% | 4.50% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The 10-year Gilt yield initially decline in April on hopes of a ceasefire leading to a peace deal but those hopes faded and the 10-year Gilt yield closed 9bps higher at 5.01% - it was the first time the 10-year Gilt yield closed above 5.00% since July 2008 before the worst phases of the Global Financial Crisis. The BoE’s Monetary Policy Report released at the April meeting revealed three scenarios that all likely required rate hikes. The middle scenario of energy prices declining in 2H but more slowly than implied by the current futures curve would require two-to-three rate hikes with the more severe scenario possibly requiring policy to be tightened “materially”. Our prior view was that the BoE would hike once but following the April meeting we have added one further rate hike and now assume a 25bp hike in June and August taking the policy rate to 4.25%. The OIS market is more than priced for this and hence we do not expect two hikes to lift the 10-year Gilt yield notably from current levels. If we do then get de-escalation and energy prices declining gradually in H2 we then see scope for a moderate decline in the 10-year yield from these historically elevated levels.

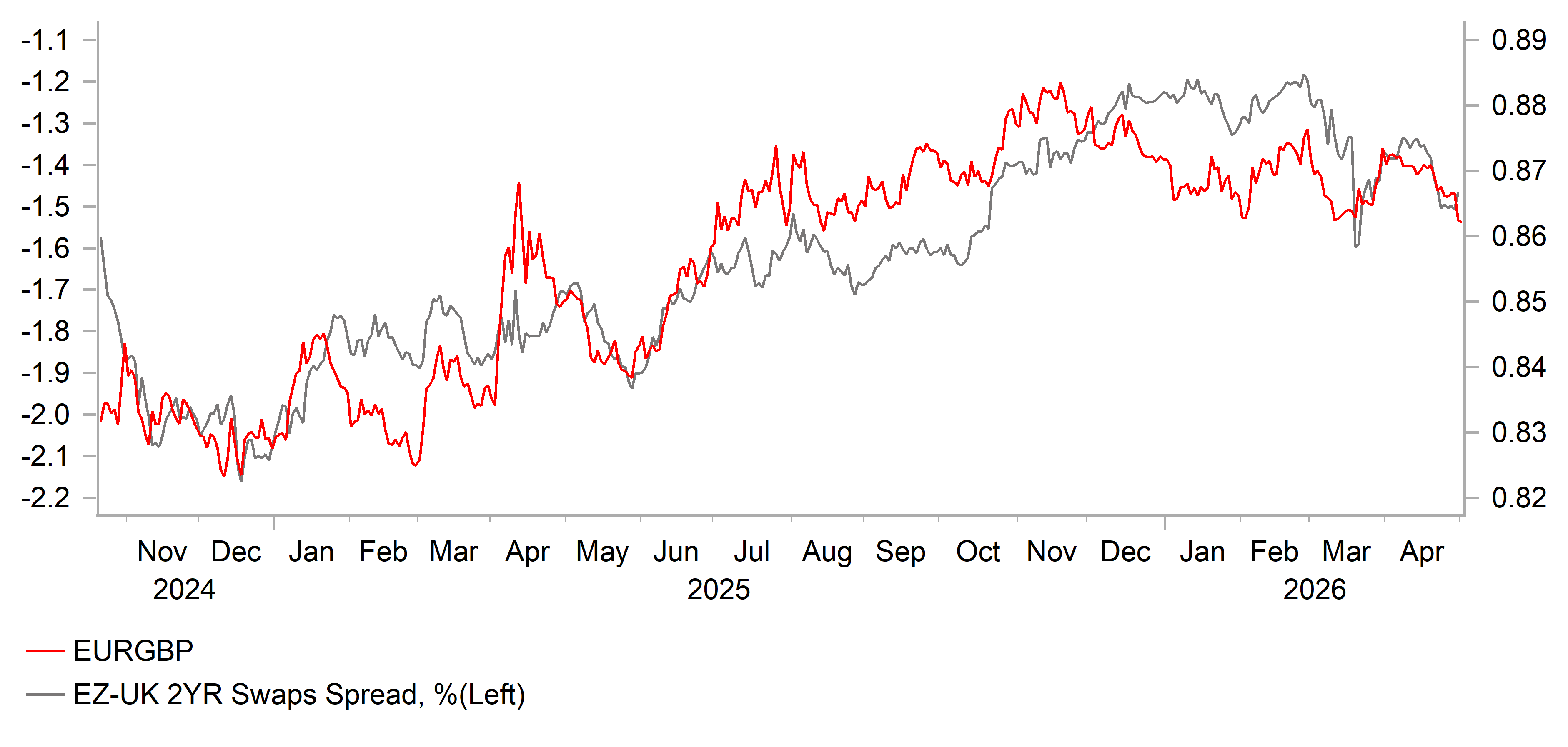

EUR/GBP vs SHORT-TERM YIELD SPREAD

Source: : Bloomberg, Macrobond & MUFG GMR

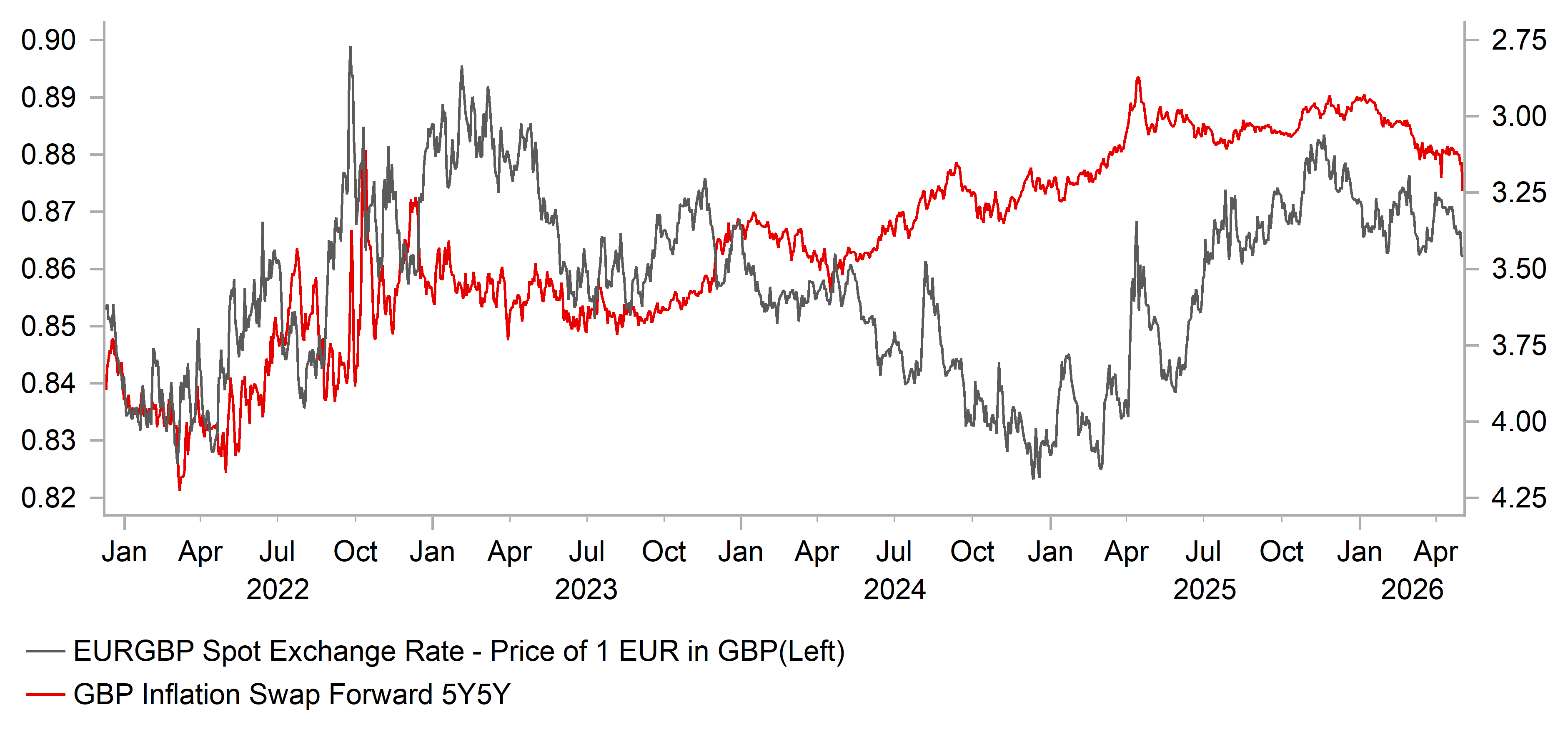

GBP/USD VS. GBP INFLATION SWAP FORWARD (INVERTED)

Source: : Bloomberg, Macrobond & MUFG GMR

Chinese renminbi

| Spot close 30.04.26 | Q2 2026 | Q3 2026 | Q4 2026 | Q1 2027 |

USD/CNY | 6.8277 | 6.8500 | 6.8300 | 6.8000 | 6.7800 |

USD/HKD | 7.8330 | 7.8300 | 7.8200 | 7.8200 | 7.8200 |

|

| Consensus | Consensus | Consensus | Consensus |

USD/CNY |

| 6.8500 | 6.8000 | 6.7800 | 6.7500 |

USD/HKD |

| 7.8200 | 7.8000 | 7.8000 | 7.8000 |

MARKET UPDATE

In April, USD/CNY moved from 6.8975 to 6.8277. On 20th April, the PBoC maintained the 1Y and 5Y LPRs steady at 3.00% and 3.50% respectively. In late April, the PBoC Governor Pan mentioned it would continue to address ‘involution-style’ competition among financial institutions, and proactively defuse the risks related to local government financing platforms debts, and small to medium-sized financial institutions.

OUTLOOK

China’s Q1 GDP positive surprise (5.0%yoy) provides a buffer against a potential negative shock ahead from the Middle East conflict. The main growth driver came from the government’s push on project construction funded by this year’s front-loaded bond issuance and fiscal stimulus from last fall, but private consumption remained subdued. As a result, the growth contribution from gross capital formation increased to 1.9ppts in Q1 whereas the consumption contribution remained unchanged at 2.4ppts of overall GDP. Strong exports and IP remained a key support in Q1 though the net exports contribution decreased likely due to a higher base last year. The growth headwind lies ahead however with elevated energy prices and energy supply disruption from the Middle East conflict. Firstly, elevated energy prices will weaken household purchasing power and confidence, and for producers, facing already weak end-demand, will struggle to pass on the higher input prices leading to a thinner profit margin, which does not bode well for employment and investment. Secondly, potential energy supply disruption will lead to reduced factory activity. Persisting elevated crude oil prices and supply shortages will likely further weigh on the Chinese real economy, as China relies on crude oil imports to satisfy 73% of its domestic consumption needs and around 54% of imports are from the Middle East. Notably, China’s April official composite PMI declined to 50.1 with weaker services and construction activities, although the manufacturing PMI held up with new export orders returning to expansion. Lastly, April Politburo meeting reaffirmed government’s supply-driven approach in driving growth with the mentions of stronger infrastructure push, expanding high-quality goods and services supply, and enhancing the security of energy resources.

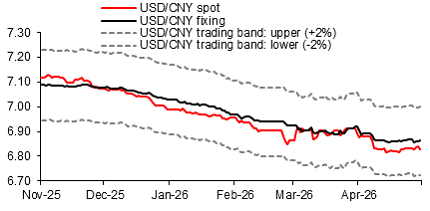

Following CNY appreciation on 8th April due to the US-Iran ceasefire announcement, USD/CNY has stabilized between 6.8200 and 6.8400. This was partly helped by the daily USD/CNY fixing being steady at around 6.8600, indicating the PBoC’s greater tolerance of two-sided CNY moves amid external uncertainties. The Iran war likely brings structural changes to the global economy, one of which is an increasing demand for China’s green products as many countries pursue energy diversification – this with the increased appeal of Chinese assets as a good diversifier to foreign investors will help support CNY in medium term. That said, CNY in the near term will likely be pressured by weaker growth caused by eroded real domestic demand.

INTEREST RATE OUTLOOK

| Interest Rate Close | Q2 2026 | Q3 2026 | Q4 2026 | Q1 2027 |

LPR 1Y | 3.00% | 2.90% | 2.70% | 2.70% | 2.70% |

7-Day Reverse Repo Rate | 1.40% | 1.30% | 1.10% | 1.10% | 1.10% |

10-Year Yield | 1.75% | 1.85% | 1.90% | 1.95% | 2.00% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

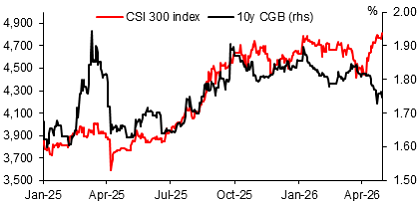

China’s government bond market in April benefitted from PBoC’s liquidity injection, which pushed money market rates such as DR007 and AAA 3M NCD even below 7-day reverse repo rate of 1.4% on occasions. That has exerted downward pressure on CGB yields across the curve, with the 10-year yield declining by 6bps to 1.75%. The lower funding cost will likely increase banks’ appetite to lend, which is consistent with the unconfirmed reports that the PBoC asked banks to expand lending in April from prior month. Given the government’s repeated emphasis on a targeted approach in driving growth and making effective investment, we see the liquidity injection probably as a short-term measure to counter the potential loan demand slowdown due to uncertainties over the Middle East conflict. In the longer term, longer-end bond yields should remain supported with gradual reflation and ongoing structural rebalancing though potential monetary easing and foreign demand for Chinese bonds may exert some downward pressures in 2H. Policy rate wise, we think it is more likely for PBoC to ease than not despite the pick-up in energy-induced inflation, as consumption and housing market recovery likely will remain sluggish.

CNY APPRECIATION TREND HAS SLOWED AS USD/CNY FIXING STEADIED

Source: : Bloomberg, MUFG GMR

MOVEMENT OF CSI 300 INDEX AND 10y CGB YIELD DIVERGED IN APRIL

Source: : Bloomberg, MUFG GMR