To read the full report, please download PDF.

USD selling curtailed by oil risk

FX View:

The key US inflation data releases this week were certainly factors that helped see some renewed dollar selling but the depreciation of the dollar was quite contained this week – bar oil-related FX most of the other currencies gained only modestly. Selling is certainly being contained by the risk of a further escalation in the conflict in the Middle East fuelling another rise in crude oil prices that in turn would likely bring forward pricing on a rate hike from the Fed. The inflation data this week certainly did not indicate a need for any monetary tightening, and if Middle East risks recede, the dollar will likely weaken more notably. Incoming UK PM Andy Burnham gave a speech today promising a pro-business economic policy agenda. The pound looks optimistically priced in our view and the fiscal challenge appears under-appreciated. The options market pricing for the pound also shows limited appetite for downside protection that we suspect leaves the pound vulnerable to an increase in fiscal risks and an increase in broader risk aversion that could prompt an increase in volatility across equities, rates and FX.

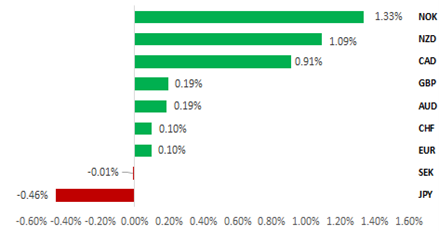

CRUDE OIL REBOUND THIS WEEK REFLECTED IN G10 FX PERFORMANCE

Source: Bloomberg, close on 17th July 2026 (Weekly % Change vs. USD)

Trade Ideas:

We are recommending a new long EUR/GBP trade idea and are maintaining a short USD/BRL trade idea.

JPY Flows:

This week we analyse the monthly Transactions in International Securities data. We highlight the overall subdued flows in net from Japanese investors and the substantial flows from foreign investors.

How Are Markets Interpreting a Burnham Premiership?:

This week we analyse the GBP options market flows to assess whether an impending Burnham premiership is attracting a meaningful political risk premium.

FX Views

GBP: Positive fundamentals or relative value?

The pound has weakened back modestly against the dollar today but remains close to the level versus the US dollar from just before the start of the conflict in the Middle East at the end of February. The US dollar and the pound are the two top performing G10 currencies since the conflict started. The pound has strengthened notably against many of the rest of G10, including the euro with EUR/GBP breaking below the 0.8500-level for the first time since June 2025. The pound is outperforming, moving in the opposite direction of MUFG forecasts despite increased political uncertainties with PM Starmer set to step down on Monday and be replaced by Andy Burnham. Why have we been wrong on the pound and does this outperformance warrant a change in view and forecasts?

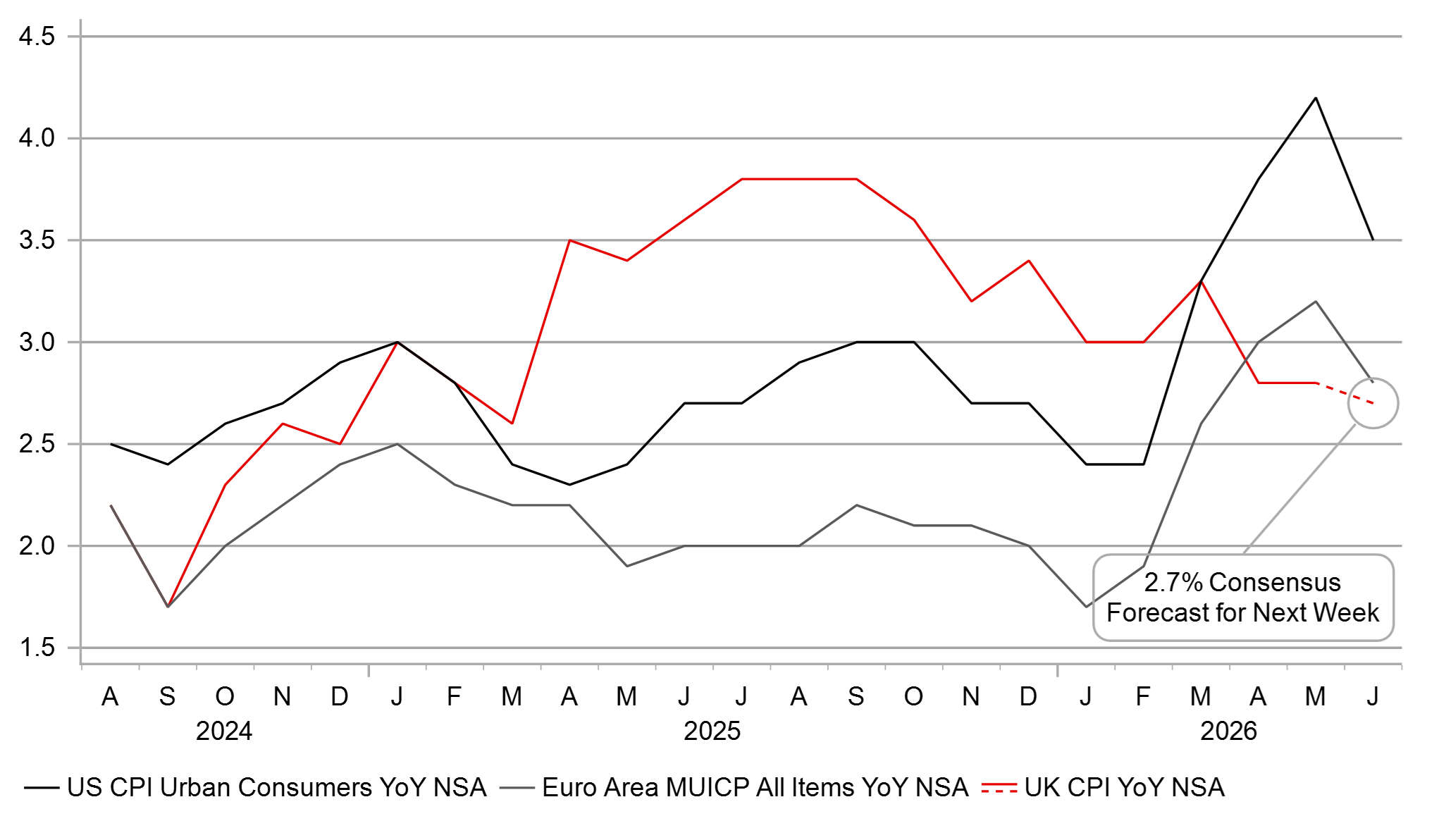

The biggest single surprise over recent months has been lower than expected inflation in the UK. The headline annual CPI rate has actually fallen from 3.0% in February before the conflict began to 2.8% in May and the June reading next week is expected to see a further modest drop to 2.7%. The core annual inflation rate is expected to fall to 2.5%. After the conflict began, based on a moderate scenario of higher crude oil prices, the annual CPI rate breaking above 4.0% looked very feasible. Energy inflation proved more fleeting than expected with a more benign energy price jump and quicker reversal, but housing services (OFGEM base-effect) and food prices all helped to soften overall inflation. The consequence of softer than expected inflation and the reversal of energy prices has been clear to see in inflation expectations. The 5y5y inflation swap rate fell 20bps in May and June and has rebounded just 5bps since the re-escalation of the conflict and the jump in crude oil. In fact, the 5y5y inflation swap rate is marginally below the level at the end of February, before the conflict began.

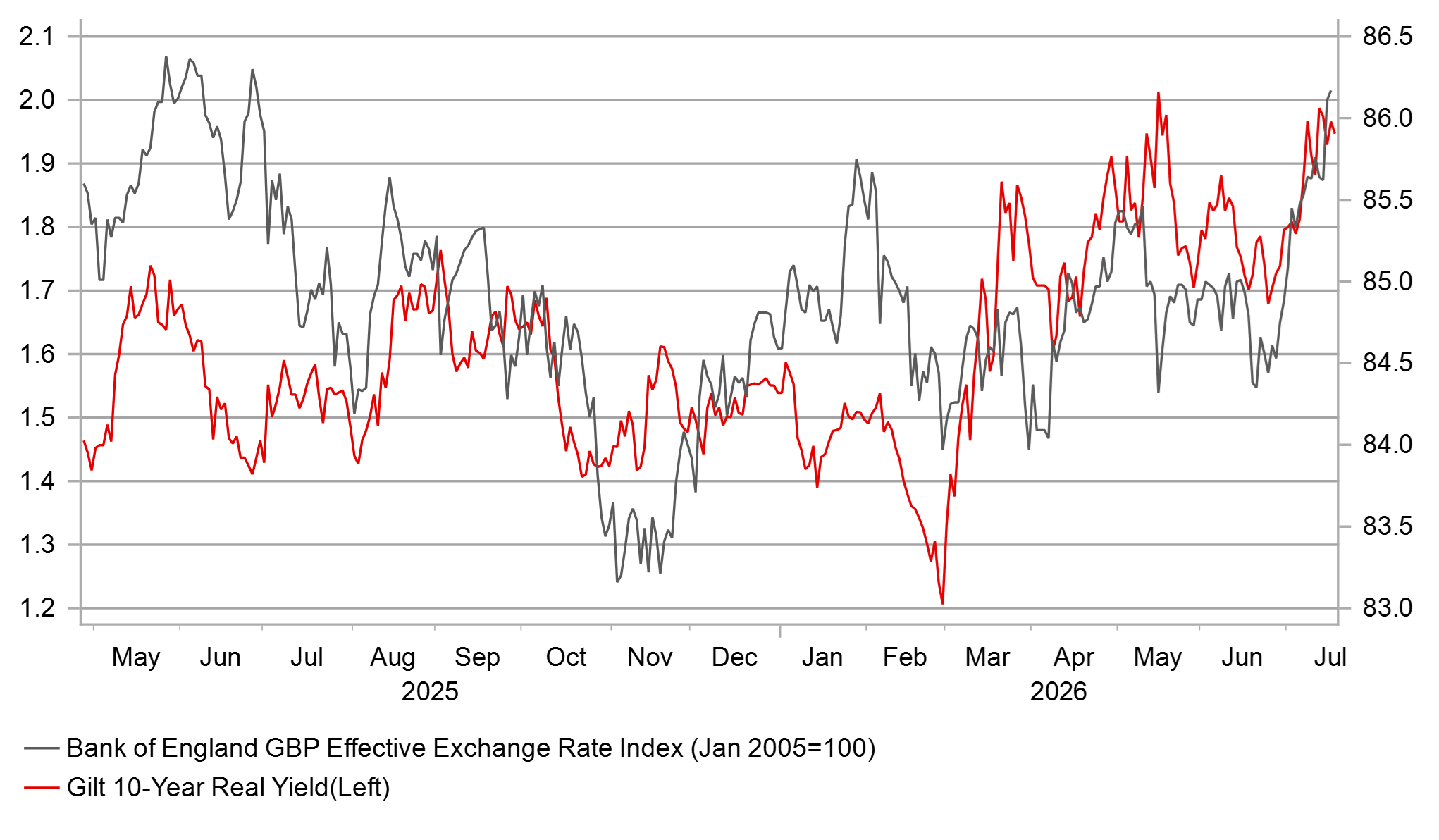

At a time of volatility in energy markets, UK inflation expectations have remained very contained. Given the move in Gilt markets what has transpired is a jump in real yields. With the 10-year Gilt yield close to 5.00% and stripping out the 5y5y inflation swap rate the 10-year real yield is close to 2%. With the inflation expectation component back at just below the pre-conflict level, the real yield has jumped by a similar amount to the nominal yield, about 75bps. We don’t think this jump relates to an improved outlook for growth and hence is capturing other non-inflation risks, including fiscal risks. The pound has performed well as investors appear to view the additional compensation for increased political risks as ample. Numerous factors could change to alter this – political fiscal developments could worsen, inflation expectations could rise which could alter the risk-reward profile related to the political uncertainty.

UK HEADLINE CPI SET TO BE LOWER THAN EZ & US

Source: Bloomberg, Macrobond & MUFG GMR

UK 10-YR REAL YIELD VS BOE TWI

Source: Bloomberg, Macrobond & MUFG GMR

Analysis, included in this FX Weekly further below, also suggests reduced concerns over political uncertainties in the options market. Looking at risk-reversals and implied vol structures informs us that pricing since around the time of Andy Burnham confirming he was running for parliament through to now initially showed increased demand for pricing downside GBP protection, but this has receded notably since.

The options pricing down potentially point to a degree of complacency. The pound may also have been helped by the ‘anyone but Miliband’ trade for who becomes Andy Burnham’s Chancellor. Investors were concerned over Ed Miliband becoming Chancellor given his more left leanings and the probable choice of Shabana Mahmood has likely helped the pound. But Mahmood has no experience and there are considerable challenges ahead. We estimate a GBP15bn drop in fiscal headroom due to higher inflation, weaker growth and the need for increased defence spending since the budget so to return to that headroom and find additional funds for any other spending could easily lack credibility and see investors’ fiscal concerns increase again. The fiscal risks may well be currently under-estimated.

Global financial market conditions have also been far more favourable than expected when the Middle East conflict first broke out. Global risk appetite has been remarkably resilient helped by a less disruptive rise in energy prices than feared and the continued AI-related surge in risk appetite. Low FX vol tends to coincide with a positive performance for the pound. But there are some near-term potential challenges for FX vol remaining low. Firstly, the conflict in the Middle East is escalating. The IEA estimates it is a matter of weeks before problematic supply issues emerge that could see crude oil prices surge further. Rates volatility would then return, lifting FX vol. In addition, the positive AI momentum is fading, and we are seeing much higher volatility in AI-related trades that could mark a larger correction lower.

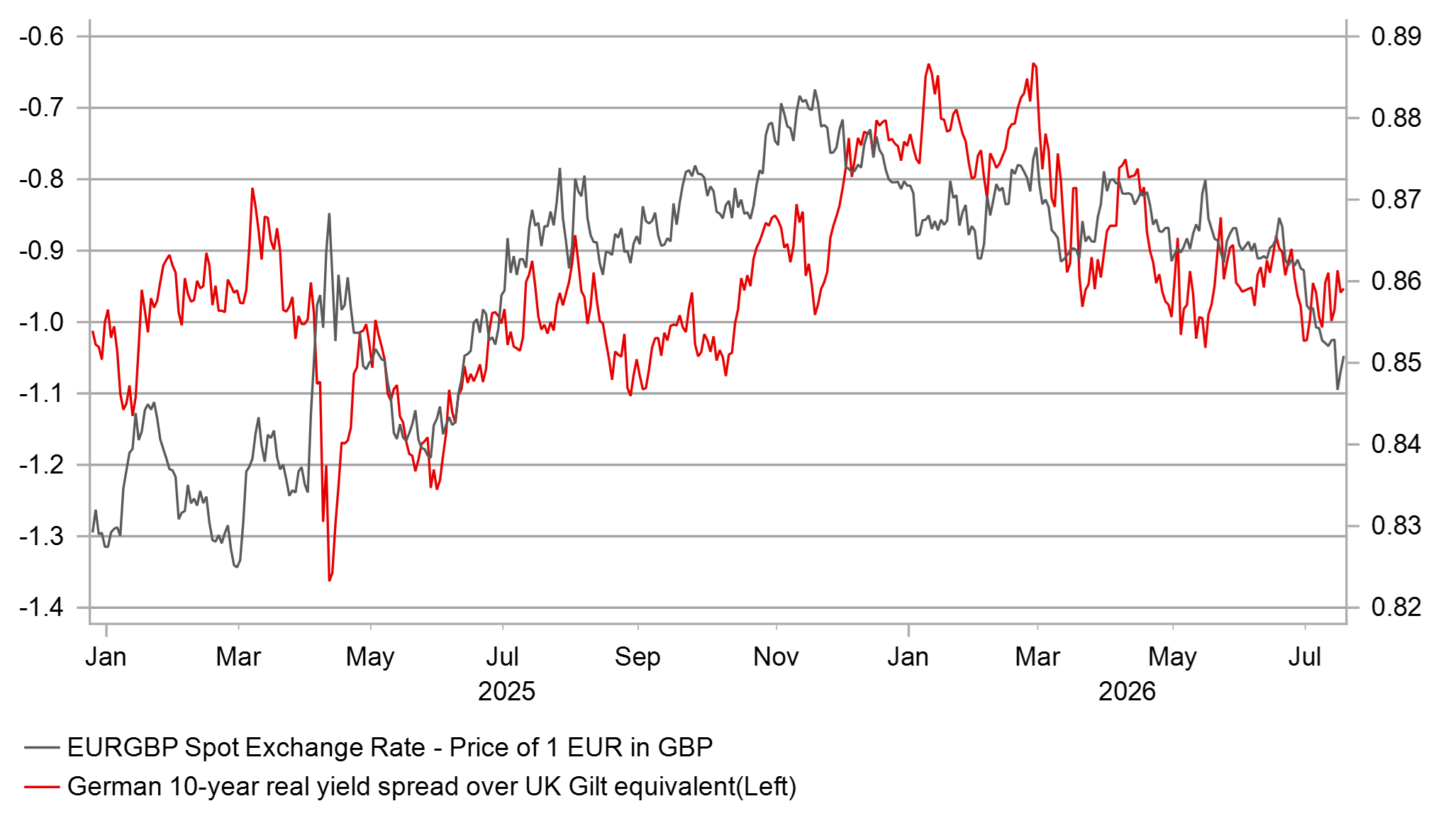

While we understand the reasons for the out-performance of the pound, we see numerous reasons for caution. While investors currently appear well compensated for fiscal risks, that could change quickly. The fiscal challenges are considerable and appear under-appreciated to us. There are now two 25bp rate hikes priced by March next year and if this escalation by into conflict in the Middle East is short-lived we doubt the BoE will hike given the recent favourable inflation backdrop. That should see yields move lower at a time when fiscal risks will persist, leaving GBP vulnerable to the downside. If we are wrong and the BoE hikes due to the energy inflation risks, the Fed and other central banks will likely also be hiking, and rates volatility would likely feed into an upturn in FX vol that tends to hit the pound. We suspect this period of pound outperformance will not last, primarily versus the euro.

EUR/GBP VERSUS 10YR EZ-UK REAL YIELD SPREAD

Source: Bloomberg, Macrobond & MUFG GMR

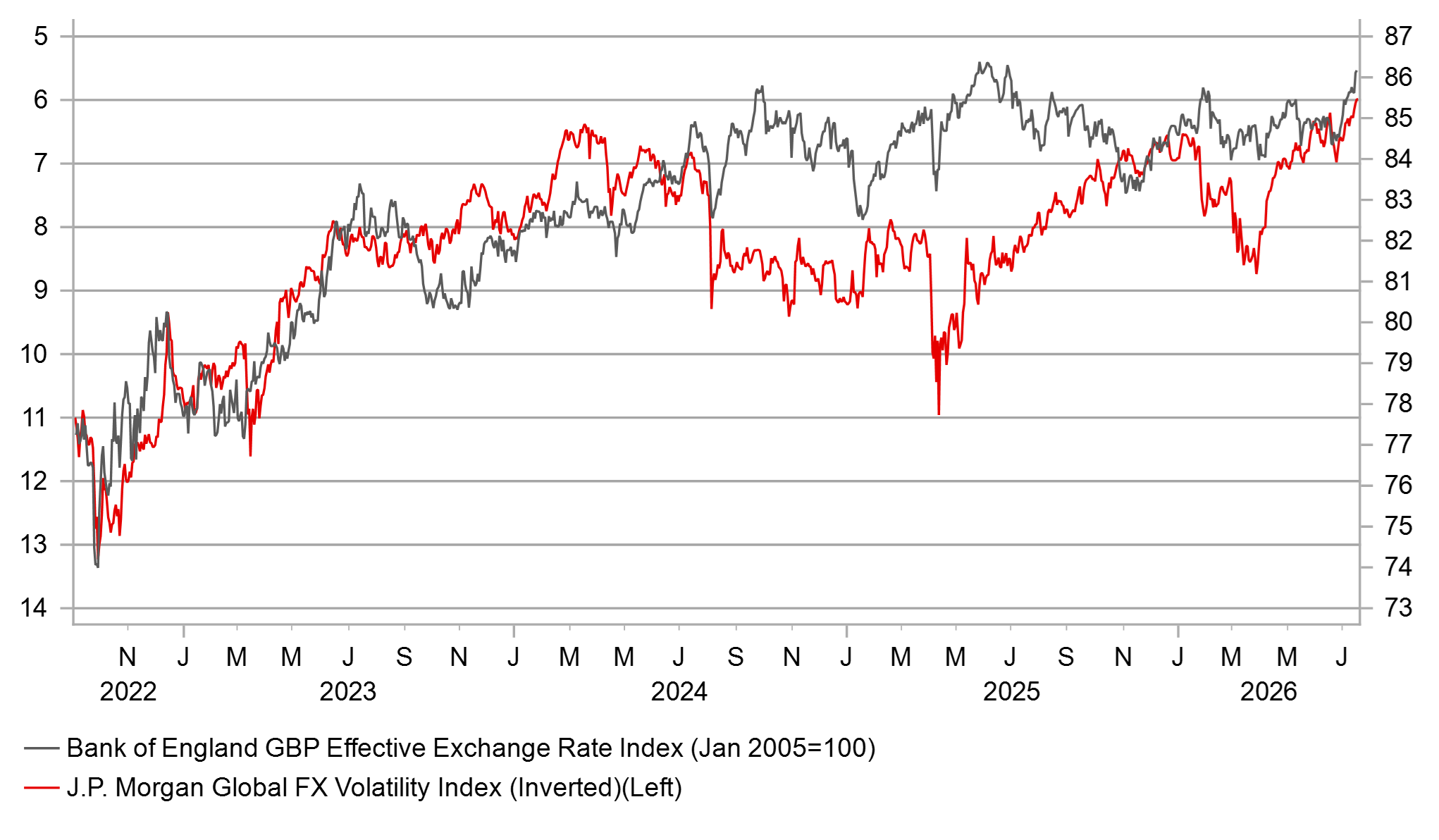

G10 FX VOL (INVERTED) VS BOE GBP TWI

Source: Bloomberg, Macrobond & MUFG GMR

USD: More evidence of slowing US inflation will weaken the USD

The USD has continued to correct modestly lower over the past week resulting in the dollar index falling back towards the 100.00-level. The USD has weakened against all other G10 currencies apart from the JPY which continues to underperform. Comments from Japanese officials including today from Prime Minister Takaichi signalling a potential policy shift to encourage domestic investors including the GPIF (click here) to further increase investment in domestic assets have so far failed to provide significant support for the JPY. The impact has been most evident so far in the JGB market where yields have fallen since late last week. The 10-year and 30-year yields are currently trading around 20bps and 25bps below recent highs.

At the same time, media reports suggest that the government is seeking to ease concerns that it could constrain the BoJ's ability to tighten monetary policy. Reuters has reported that the government has revised its economic policy blueprint to make it clear that decisions regarding specific monetary policy tools should remain the sole responsibility of the BoJ. This should help alleviate investor concerns that the BoJ could fall further behind the curve in responding to higher inflation. However, Prime Minister Takaichi will still have the authority to appoint two new Policy Board members next year when the terms of Hajime Takata and Naoki Tamura expire on 23rd July 2027. Both are generally regarded as hawkish by BoJ standards. In contrast, Prime Minister Takaichi's two recent appointments to the Policy Board, Toichiro Asada and Ayano Sato, are viewed as relatively dovish. While these appointments are unlikely to influence BoJ policy materially this year, next year's appointments could make it more difficult for the BoJ to continue normalising policy from the second half of 2027 onwards. Against that backdrop, it is even more important for the BoJ to continue raising rates over the next 12 months in order to restore confidence in the JPY.

In contrast to the continued underperformance of the JPY, the two best-performing G10 currencies this week have been the NOK and NZD. The NOK has rebounded alongside renewed military tensions in the Middle East, which have pushed Brent crude prices back above USD85/bbl. As a result, oil prices are now back over 20% higher than their pre-conflict levels. According to Bloomberg, tanker traffic through the Strait of Hormuz has slowed sharply once again, and there is still no clear indication of when the latest round of military strikes will come to an end. Under normal circumstances, we would have expected the USD to strengthen in response to higher energy prices. However, the release of significantly softer US inflation data this week has had a more powerful impact, dampening expectations for further Fed rate hikes in the near term. It was widely anticipated that headline inflation would ease, given that average gasoline prices fell by around 10% in June. The main surprise, however, was the broader-based nature of the disinflationary trend, with core inflation unchanged on the month. It was the largest downside surprise in core inflation since April of last year. Fed Chair Kevin Warsh has welcomed the improvement in inflation but stopped short of declaring victory, instead reiterating the Fed's commitment to restoring price stability. While the latest data do not completely rule out a Fed hike as soon as this month, the bar for further tightening has risen. The softer inflation backdrop gives the Fed more time to assess inflation risks over the summer before deciding whether additional tightening is warranted in the autumn. Admittedly, it will also become increasingly difficult politically to raise rates as the November mid-term elections draw closer.

YIELD SPREADS HAVE MOVED AGAINST USD

Source: Bloomberg, Macrobond & MUFG

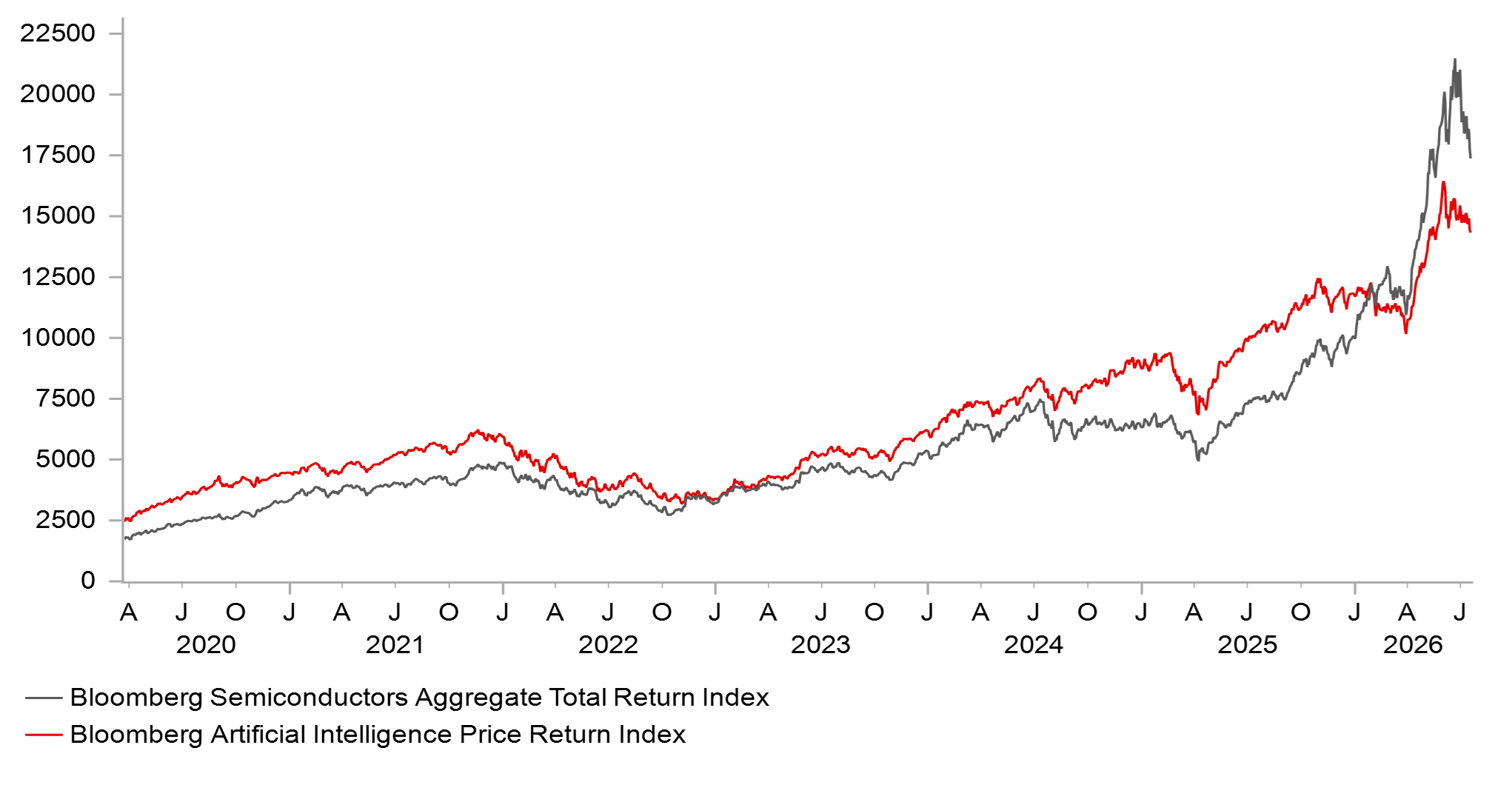

AI STOCKS ARE CORRECTNG LOWER

Source: Bloomberg, Macrobond & MUFG

The softer inflation data released over the past week supports our view that inflation will moderate over the summer, helping to ease pressure on the Fed to tighten policy further. This remains a key assumption underpinning our forecasts (click here) for renewed USD weakness into year-end. That said, it is becoming increasingly clear that Fed officials are prepared to tighten policy if inflation fails to cool as expected, suggesting that their tolerance for above-target inflation is nearing its limit. Over the past week, Governors Christopher Waller, Lisa Cook and Philip Jefferson have all indicated that they would be prepared to support further policy tightening if inflation does not begin to moderate. Dallas Fed President Lorie Logan even went a step further, stating that she already favours modestly higher interest rates to help lower inflation. At the same time, Fed officials have become more vocal about upside inflation risks associated with the AI investment boom. Fed Chair Kevin Warsh highlighted that high-tech spending has increased by almost 25% over the past four quarters. However, he does not necessarily view a one-off rise in prices as inflationary, arguing that stronger supply should eventually emerge in response to increased demand. Those relatively dovish remarks indicate he is likely to remain cautious about raising rates prematurely.

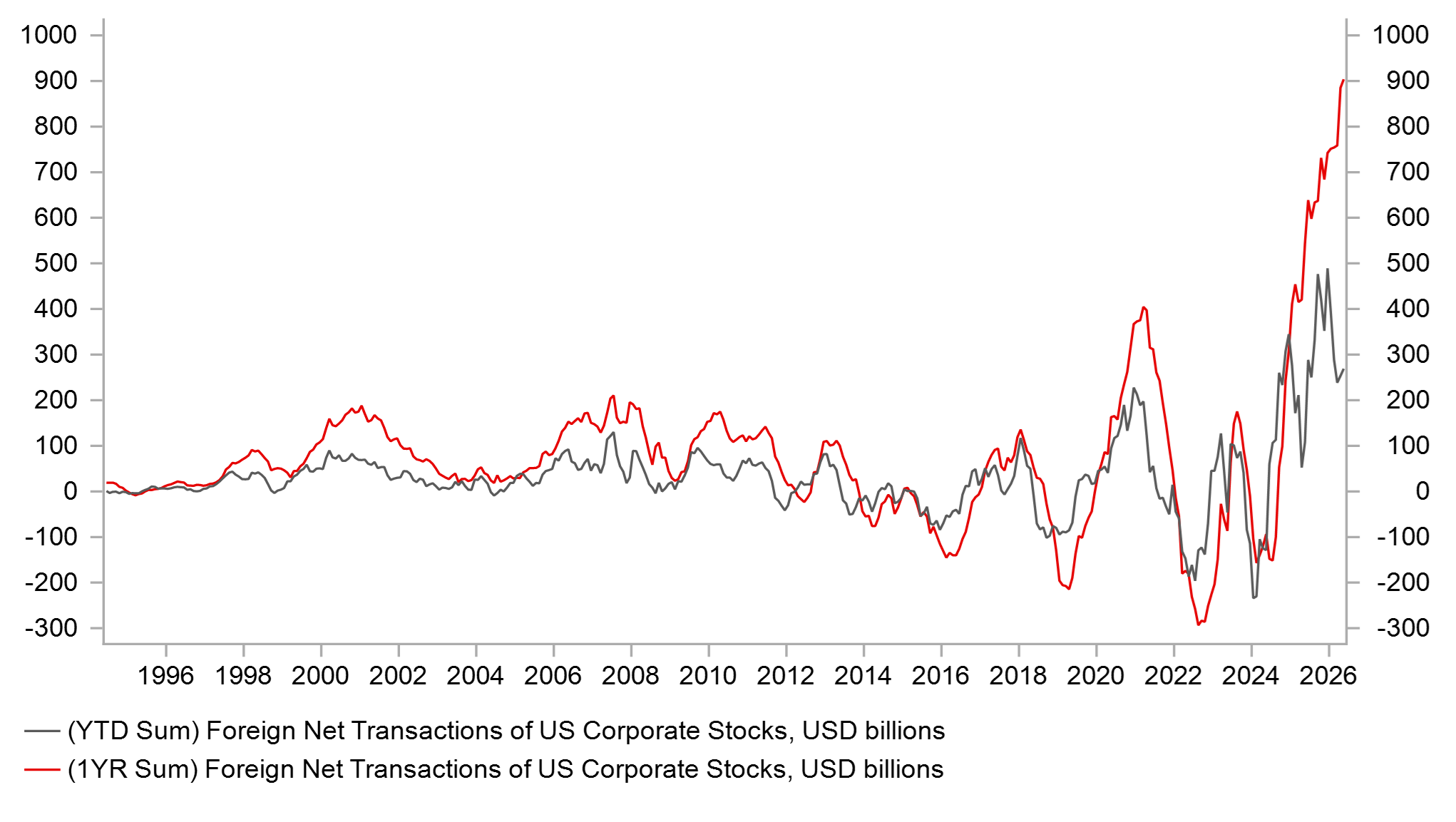

The performance of AI-related equities has attracted greater market attention over the past week as well. After posting strong gains in April and May, AI-related stocks have undergone a correction this month. Bloomberg's AI Price Return Index, which tracks the performance of the top 50 AI-related companies, peaked in early June and has since declined by around 13%. The correction has been even more pronounced for Bloomberg's Semiconductor Aggregate Price Return Index, which has fallen by almost 20% from its recent high. While equity market volatility has started to pick up, it remains close to year-to-date lows, with only limited spillovers into FX markets so far. As a result, financial conditions remain broadly supportive for FX carry trades. However, a deeper correction in AI-related equities would pose a greater challenge to carry strategies and could also weigh on the USD given current market positioning. The latest Treasury International Capital (TIC) data showed that foreign investors were significant buyers of US equities in April and May, with net purchases totalling USD244 billion. This lifted cumulative foreign purchases to USD904 billion over the past year.

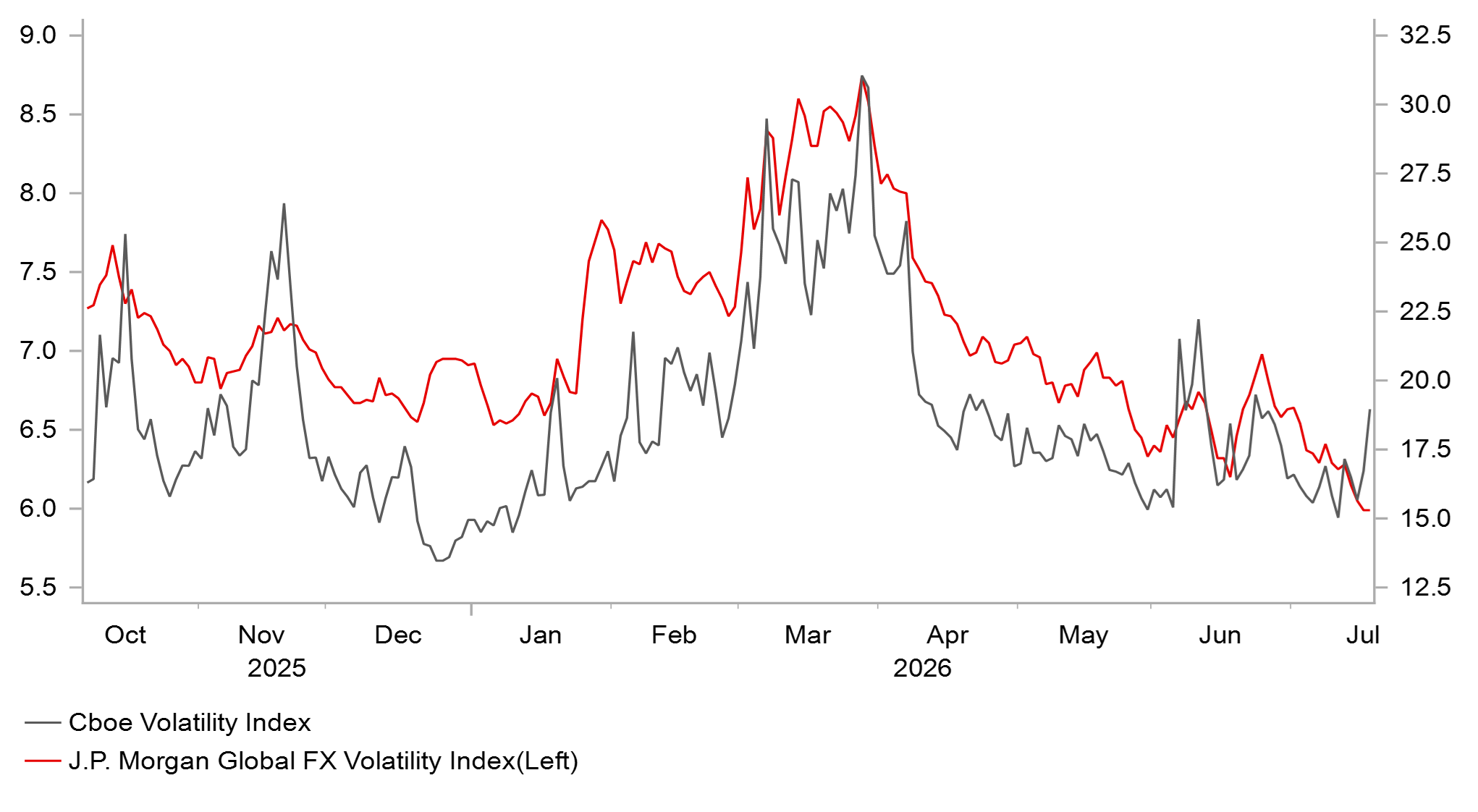

EQUITY & FX MARKET VOLATILITY ARE LOW

Source: Bloomberg, Macrobond & MUFG GMR

HEAVY INFLOWS INTO US EQUITIES

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

Ccy | Date | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EUR | 20/07/2026 | 10:00 | Construction Output MoM | May | -- | 0.6% | !! |

CAD | 20/07/2026 | 13:30 | CPI YoY | Jun | 3.1% | 3.2% | !!! |

NZD | 20/07/2026 | 23:45 | CPI YoY | Q2 | -- | 3.1% | !!! |

GBP | 21/07/2026 | 07:00 | Public Sector Net Borrowing | Jun | -- | 23.3b | !! |

GBP | 21/07/2026 | 07:00 | Payrolled Employees Monthly Change | Jun | -- | 2k | !!! |

EUR | 21/07/2026 | 09:00 | ECB Bank Lending Survey | !! | |||

EUR | 21/07/2026 | 10:00 | Germany ZEW Survey Expectations | Jul | -- | 10.5 | !! |

JPY | 22/07/2026 | 00:50 | Trade Balance | Jun | ¥38.3b | -¥378.6b | !! |

GBP | 22/07/2026 | 07:00 | CPI YoY | Jun | -- | 2.8% | !!! |

GBP | 22/07/2026 | 07:00 | PPI Output NSA YoY | Jun | -- | 4.0% | !! |

AUD | 23/07/2026 | 02:30 | Employment Change | Jun | 20.0k | 40.3k | !!! |

GBP | 23/07/2026 | 11:00 | CBI Business Optimism | Jul | -- | - 65.0 | !! |

EUR | 23/07/2026 | 13:15 | ECB Deposit Facility Rate | 2.25% | 2.25% | !!! | |

CAD | 23/07/2026 | 13:30 | Retail Sales MoM | May | -- | 0.5% | !! |

USD | 23/07/2026 | 13:30 | Initial Jobless Claims | -- | -- | !! | |

EUR | 23/07/2026 | 13:45 | ECB President Lagarde Press Conference | !!! | |||

EUR | 23/07/2026 | 15:00 | Consumer Confidence | Jul | -- | - 17.7 | !! |

JPY | 24/07/2026 | 00:30 | Natl CPI YoY | Jun | 1.6% | 1.5% | !!! |

SEK | 24/07/2026 | 07:00 | Unemployment Rate | Jun | -- | 9.4% | !! |

GBP | 24/07/2026 | 07:00 | Retail Sales Inc Auto Fuel MoM | Jun | -- | 1.2% | !! |

EUR | 24/07/2026 | 09:00 | S&P Global Eurozone Manufacturing PMI | Jul | -- | 51.4 | !! |

EUR | 24/07/2026 | 09:00 | S&P Global Eurozone Services PMI | Jul | -- | 49.4 | !! |

GBP | 24/07/2026 | 09:30 | S&P Global UK Manufacturing PMI | Jul | -- | 52.5 | !! |

GBP | 24/07/2026 | 09:30 | S&P Global UK Services PMI | Jul | -- | 48.8 | !! |

USD | 24/07/2026 | 14:45 | S&P Global US Composite PMI | Jul | -- | 51.9 | !! |

USD | 24/07/2026 | 15:00 | New Home Sales | Jun | 600k | 580k | !! |

USD | 24/07/2026 | 15:00 | Building Permits | Jun | -- | -- | !! |

Source: Bloomberg & MUFG GMR

Key Events:

The ECB will hold its final policy meeting before the summer break in the week ahead. We expect the ECB to leave rates unchanged after raising them by 25bps at its June meeting. Even prominent ECB hawks, including Bundesbank President Nagel, have indicated that back-to-back rate hikes are not necessary. The recent flare-up in tensions between the US and Iran has created a less favourable backdrop for the ECB, which remains concerned about the risk of second-round inflation effects stemming from the energy price shock. We expect the ECB to signal that it remains open to raising rates at least once more later this year. Such guidance would be consistent with our forecast for a further 25bp hike in September.

The main economic releases in the week ahead will come from the UK, including the latest labour market and June CPI reports. Payrolled employment has remained weak this year, contracting by an average of around 13.5k per month in 2026, although it did return to positive territory in May. The BoE has indicated that a softer labour market is helping to alleviate concerns about second-round effects from the energy price shock. Inflation data has also surprised significantly on the downside in recent months, prompting us to remove BoE rate hikes from our forecasts for this year. Reflecting this backdrop, the BoE recently lowered its own forecasts and now expects inflation to rise to just over 3.25% later this year.

The main UK political event in the week ahead is expected to be the formal appointment of Andy Burnham as Labour leader and Prime Minister. The constitutional handover is expected to take place on 20th July. UK media reports suggest that he has already selected Home Secretary Shabana Mahmood as the next Chancellor, helping to further ease investor concerns over UK fiscal policy alongside his commitment to stick to the government's fiscal rules.

Market attention will remain focused on inflation risks with the release of the latest CPI reports from Canada, New Zealand and Japan in the week ahead. Of the three central banks, the RBNZ and BoJ have indicated a greater willingness to raise rates further this year in response to upside inflation risks, particularly as policy rates in both economies remain in expansionary territory.