To read the full report, please download PDF.

USD is consolidating ahead of US CPI report

FX View:

The USD has continued to trade close to recent highs against other major currencies over the past week. The USD initially strengthened in response to renewed tensions in the Middle East, but its upward momentum was quickly tempered by the June FOMC minutes. The minutes suggested that the Fed is in no rush to raise rates as early as this month and is instead likely to take more time to assess the evolving inflation outlook. Attention will now turn to the release of the June US CPI report and semi-annual monetary policy testimony from Fed Chair Warsh in the week ahead. If underlying inflation pressures remain contained, it could prompt market participants to scale back expectations for Fed hikes, resulting in a reversal of the recent USD rally. It would also help to reduce pressure on Japanese policymakers to support the JPY. Finance Minister Katayama stepped up verbal intervention this week by stating that the government wants to encourage households, as well as pension funds including the Government Pension Investment Fund (GPIF), to increase their investment in Japanese financial assets. While a significant shift in asset allocation appears unlikely in the near term, the comments have helped to ease selling pressure on both JGBs and the JPY. Over the longer term, however, this policy shift could have more far-reaching implications for domestic capital flows and provide more support for Japanese financial markets.

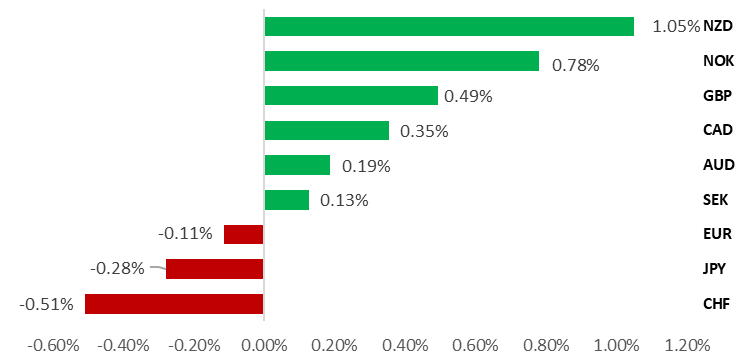

HIGH BETA G10 CURRENCIES REBOUND

Source: Bloomberg, close on 10th July 2026 (Weekly % Change vs. USD)

Trade Ideas:

We are recommending a new short USD/BRL trade idea in the week ahead to reflect favourable conditions for carry trades.

JPY Flows – High Frequency:

The MoF weekly cross-border flow data for the week ending last Friday was released yesterday, and the flows indicate a turnaround in demand for foreign securities, sway from bonds and into equities.

AI Demand vs Energy Inflation:

This week, we compare the impact of AI-driven demand and energy prices on FX, rates and broader financial markets.

FX Views

JPY: A significant policy turning point favouring home bias?

Today’s comment in a regular press conference by Finance Minister Katayama that the government intended to encourage households and pension funds, including GPIF, to invest in domestic assets is a very significant shift in policy direction that could prove meaningful over time. The yen has gained; equities are higher and JGB yields fell today which is understandable given the significance of the government’s intention. Any change will take time though but that should take away from the significance which could go some way in reshaping investor behaviours. It will not in isolation alter investor behaviour but could certainly play a role if other factors encouraging greater investments at home were to fall into place.

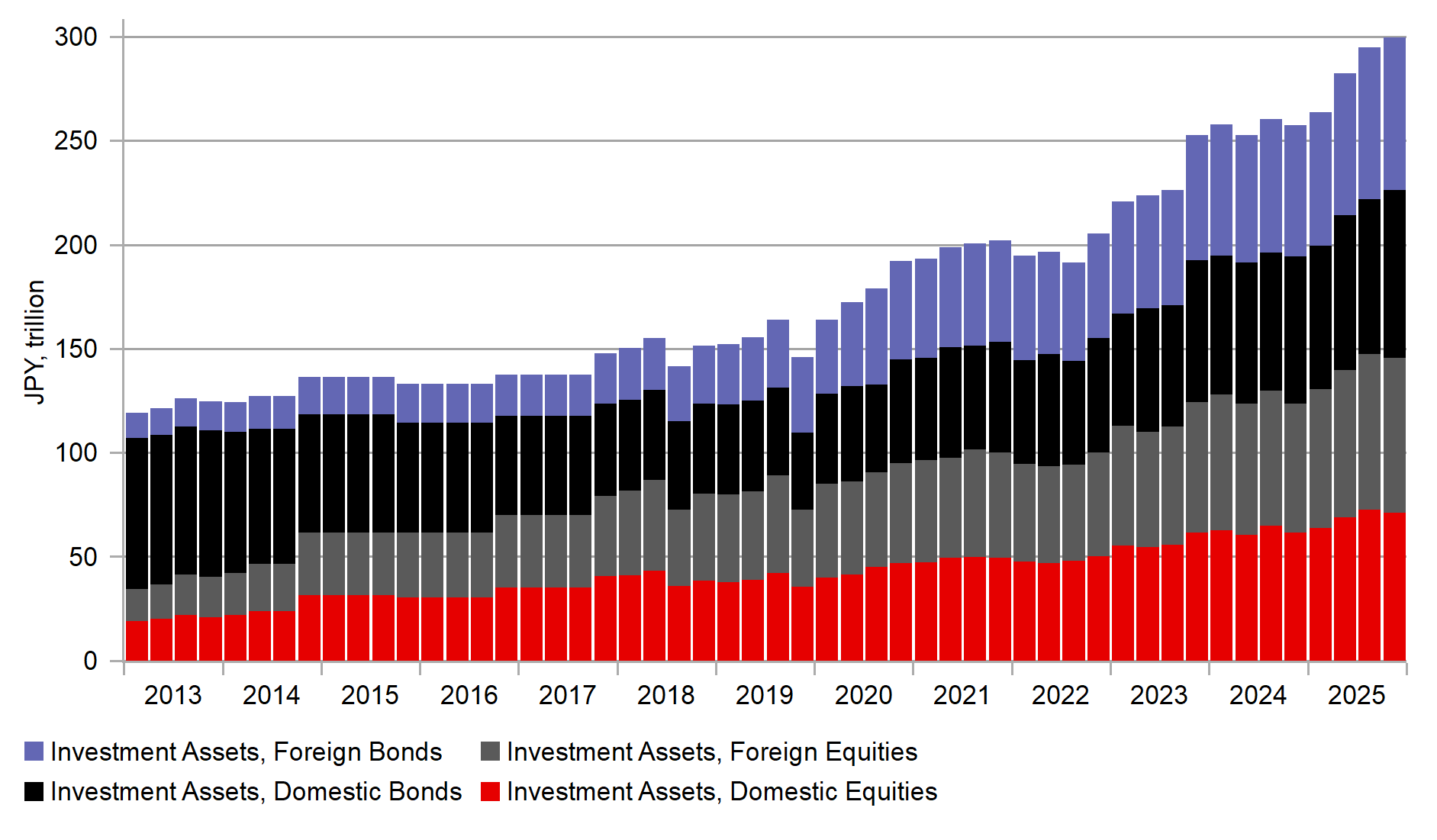

We must go back over a decade to understand the significance of this shift. In November 2013 in the early period under PM Abe and his Abenomics plan an export panel was launched to review the investment approach of public pension funds (essentially GPIF) and the findings included that the portfolio was too heavily dependent on domestic bonds that was inconsistent with Japan emerging from decades of mild deflation. Pension funds needed to diversify into riskier assets. GPIF reforms were often cited as part of the government’s reform program. In October 2014 a major shift in allocations was announced by GPIF – domestic bond allocation fell from 60% to 35%; domestic equities was increased from 12% to 25%; foreign equities from 12% to 25%; and foreign bonds from 11% to 15%. This would lift returns and improve confidence in the sustainability of Japan’s pension system leading to households reducing cautionary savings. It became one of the many key parts of the Abenomics reflationary program. It added to the yen negative sentiment which at that time was driving the yen weaker in response to Governor Kuroda’s huge quantitative easing program. In 2020 the allocations were altered to 25% across each composition.

While we certainly view this as potentially meaningful, we still have only had this comment made by Finance Minister Katayama at a regular press conference and hence to what extent any formal policy is being compiled is unclear. The MoF does not have the remit of setting the medium-term objectives of the GPIF – that resides with the the Ministry of Health, Labour and Welfare. So I think firstly we would need to see this cited more regularly as something being looked at from a policy perspective with the MHLW then formulating an updated objective. It is the GPIF’s Board of Governors that ultimately set the asset composition mix and all of this certainly points to no quick implementation of any new policy. In the meantime, investors will no doubt monitor the JSDA JGB flow data for any sign of increased buying by domestic investors. The data covering key domestic investors does not show any clear pick-up currently although Trust buying of super-long JGBs has picked up somewhat. Trust flows is where we would see pension fund flows, including GPIF. It will also be interesting to see if this announcement may encourage further foreign investor buying. Foreign investors remain a key source of demand for JGBs and if there is an expectation of greater domestic investor demand it may encourage further, perhaps more significant buying.

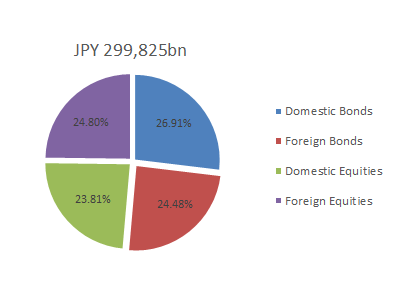

END-FY25 GPIF TOTAL ASSET VALUE & COMPOSITIONS

Source: Government Pension Investment Fund

GPIF ASSET VALUE & BREAKDOWN BY COMPOSITION

Source: Bloomberg, Macrobond & MUFG GMR

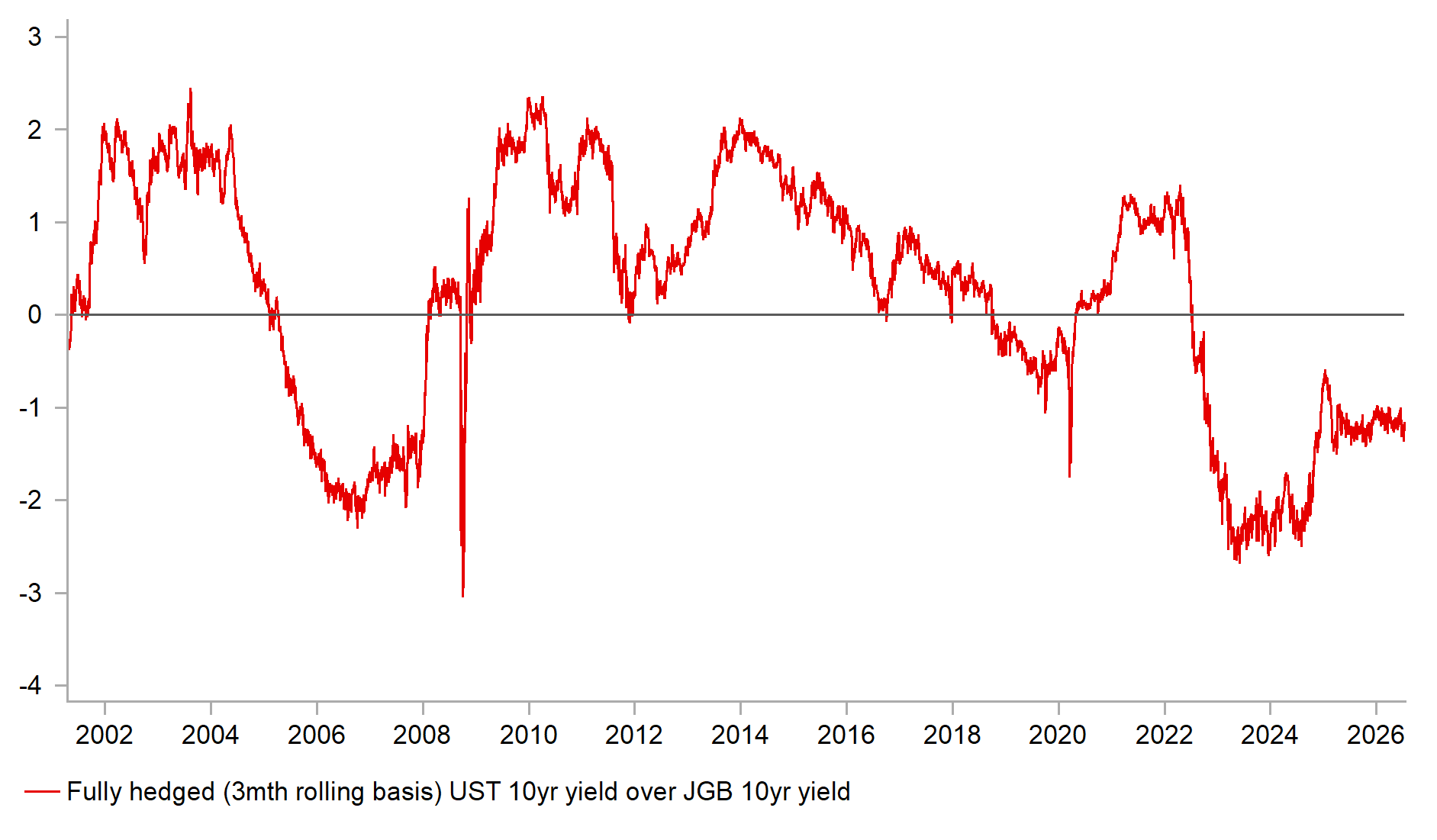

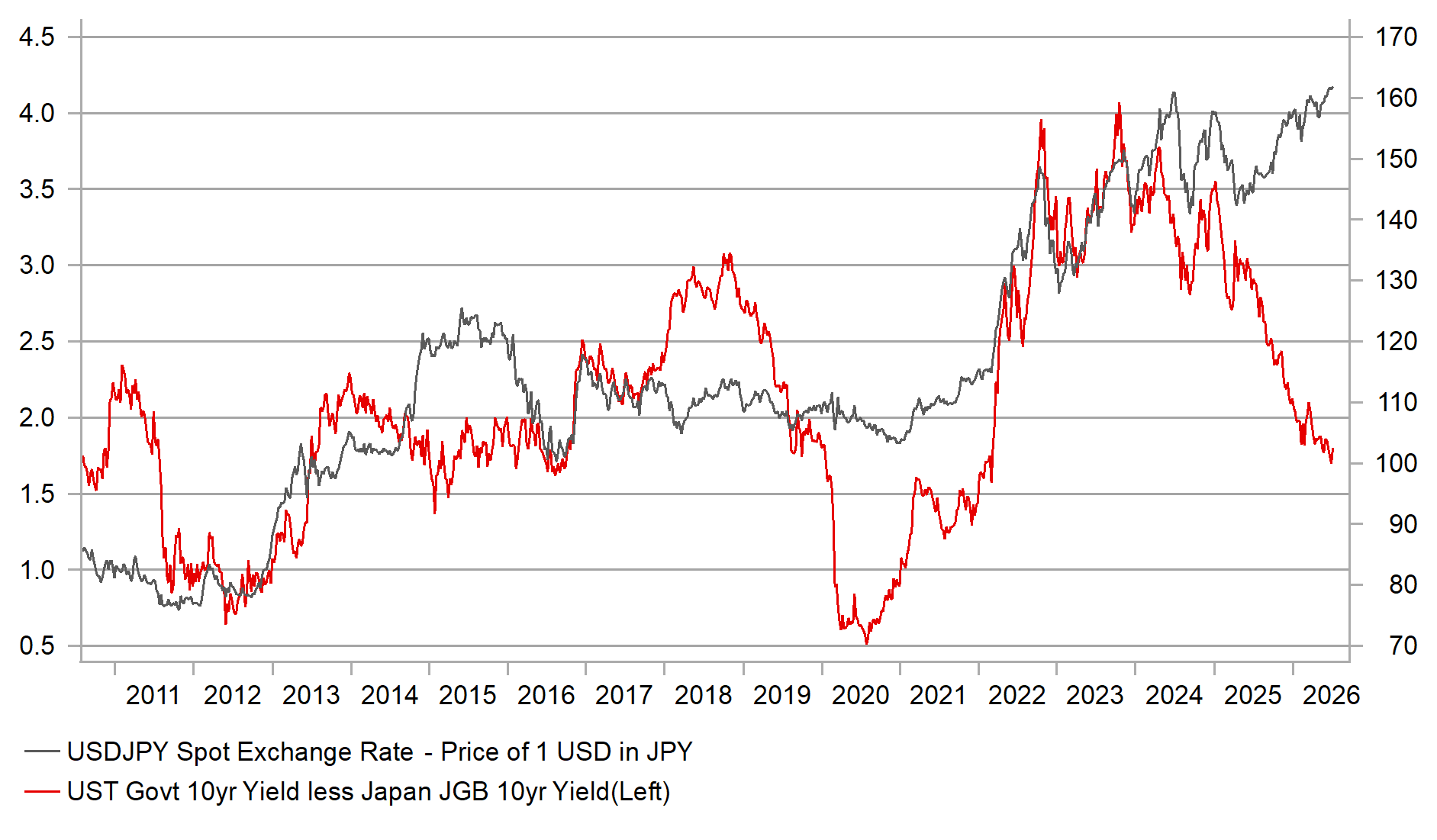

The continued steady rise in JGB yields must surely at some point start to offer Japanese investors an alternative to investing abroad. There has been a remarkable decline in the US 10-year yield premium over the equivalent JGB yield – the spread has fallen from 355bps around the start of 2025 to 180bps now, essentially retracing the entire move higher in the 10-year spread during the global inflation shock. Pre-global inflation shock, USD/JPY was trading below the 120-level. A fully hedged investment in a 10-year UST bond yields less than a 10-year JGB. What is clear from these developments is that yield still doesn’t matter and Japanese investors have continued investing in foreign bonds. Last year, Japanese investors bought JPY 12trn worth of foreign bonds. However, year-to-date (to June) Japanese investors have been net sellers – selling JPY 2,987bn. In the same period last year, Japanese investors bought JPY 6,792bn. However, this lack of outflow relates specifically to two months of heavy selling ahead of and immediately following the start of the conflict. In addition, looking at the JSDA data to assess domestic investor buying there has been no notable pick-up in buying of mid, long and super-long JGBs so yield can’t be the issue. Confidence in JGBs remains key and linked to that the monetary stance of the BoJ is containing inflation remains an issue.

It is notable that despite a BoJ rate hike in December last year and again in Juned this year, the 2s30s JGB curve is the only G4 curve that has steepened on a year-to-date basis. The message is clear – investors believe the BoJ is being too cautious. We believe to alter this, and thus help stabilise the yen and JGB yields, the BoJ needs to pick-up the pace of tightening. Even a moderate pick-up would be telling. We expect a 25bp hike in September and January 2027 which would send an important message to the markets. Measures of inflation (Tankan Output Price Index; PMI Service Input Price Index) have recently hit or matched record highs while the shunto wage agreement saw a Rengo confirm a wage increase of 5% or more for the third year in a row. The yen in particular needs stronger action before any turn stronger can materialise. FM Katayama’s comment today does indicate one important point – the government is more concerned about rising JGB yields. Allowing the BoJ to act more freely would prompt yen recovery, especially if the Fed’s next move is a cut (our view) and turnaround in the yen would be key element of improving confidence in price stability and the prospect of domestic investors investing more in JGBs.

FULLY HEDGED RETURN ON 10YR UST BOND OVER JGB

Source: Bloomberg, Macrobond & MUFG GMR

10-YR UST BOND SPREAD OVER JGB & USD/JPY

Source: Bloomberg, Macrobond & MUFG GMR

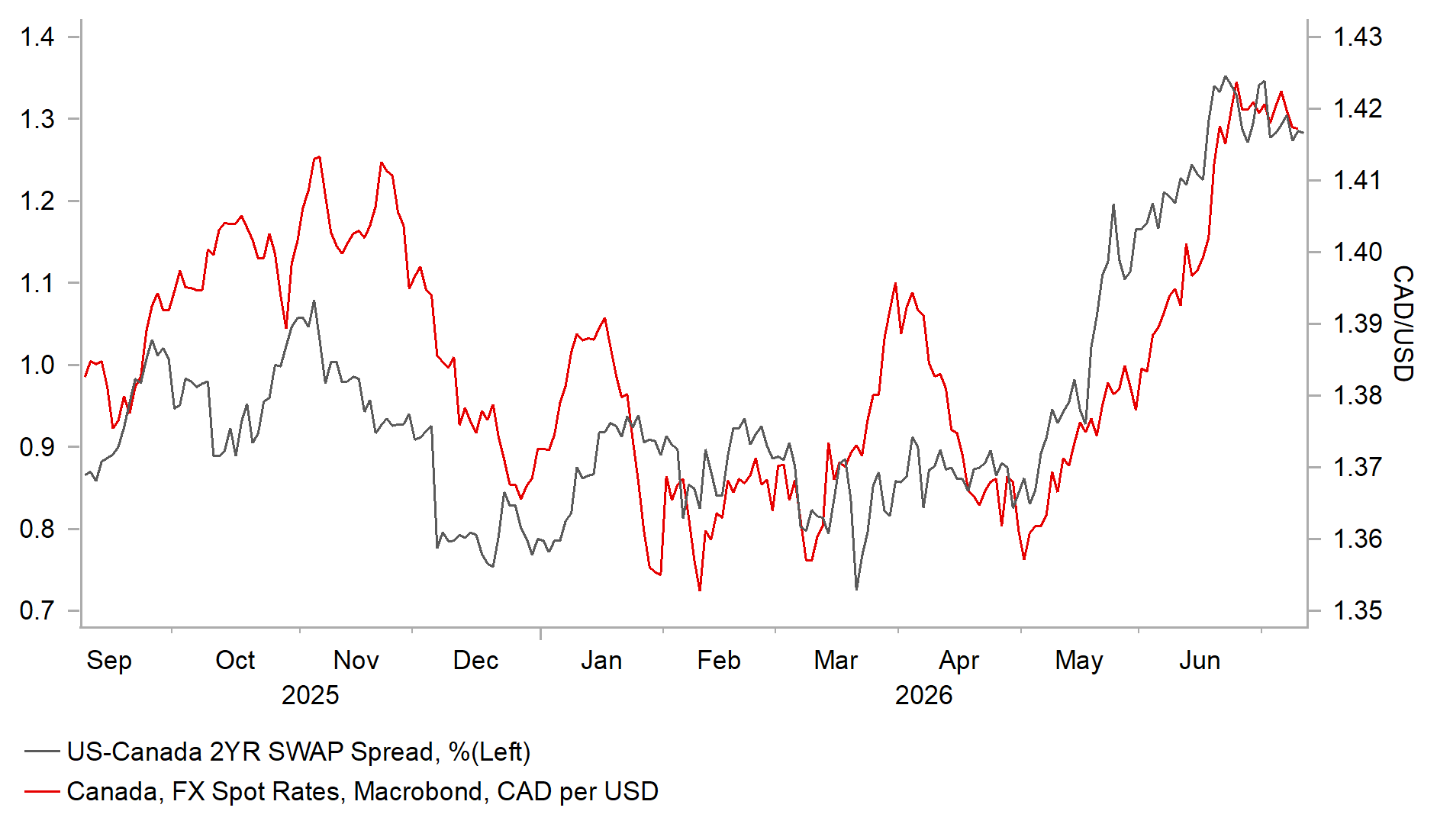

USD/CAD: Policy divergence & trade uncertainty remain key drivers

The USD has consolidated at higher levels over the past week, with the dollar index fluctuating around the 101.00 level. However, it has lost upward momentum over the past couple of weeks, raising doubts about whether the bullish breakout triggered by the hawkish June FOMC meeting can be sustained. Even so, the dollar index remains just over 1% higher since the June FOMC meeting. A similar pattern is evident in the US Treasury market, where 2-year yields remain around 10bps higher, helping to support the stronger USD. Both the USD and US Treasury yields have faced conflicting forces over the past week. Renewed tensions between the US and Iran pose the biggest risk to the ceasefire. The USD initially strengthened after Brent crude prices jumped back above USD80 per barrel, but have since retreated.

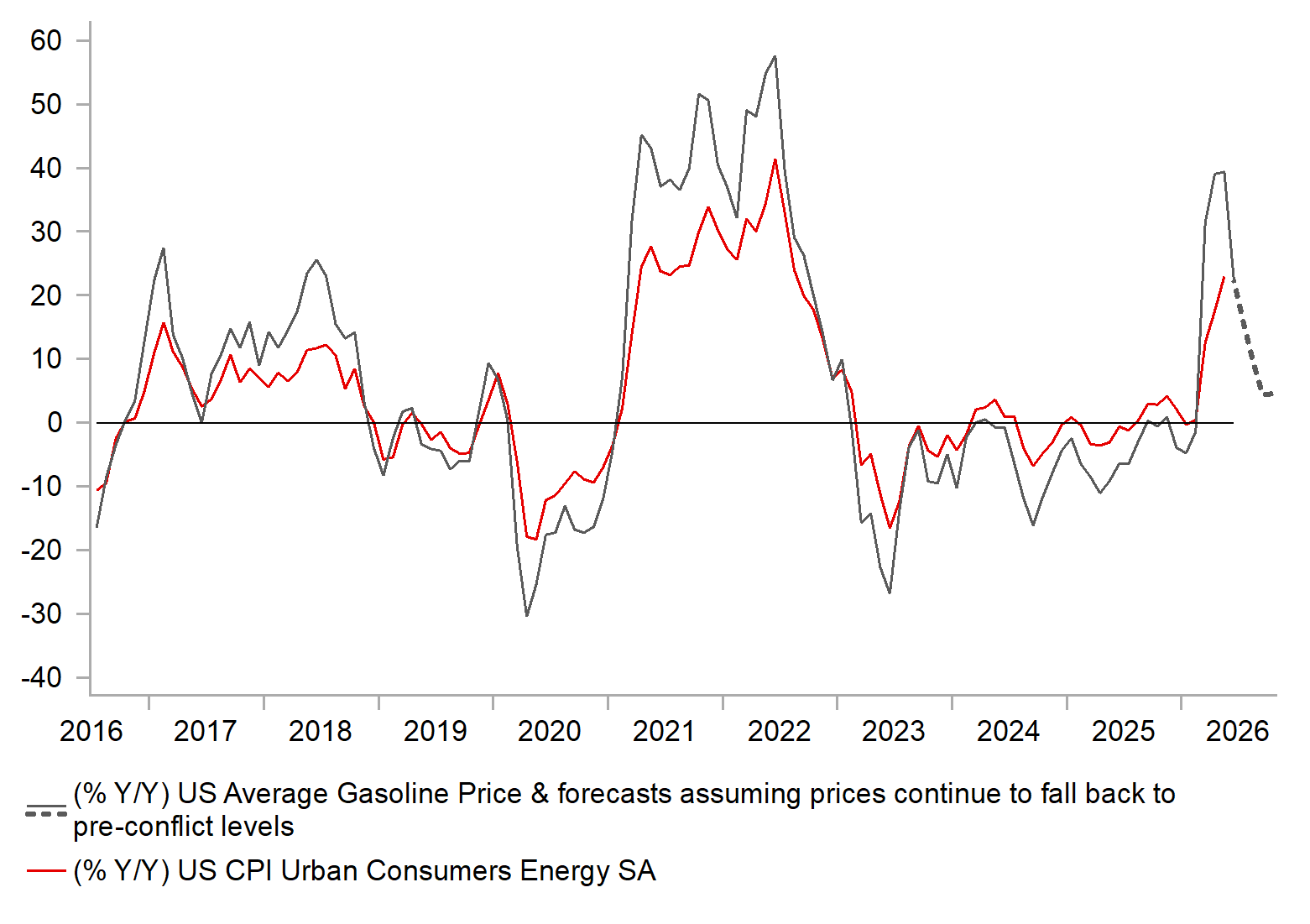

If lower oil prices are sustained, they should help to ease pressure on the Fed to raise rates, as headline inflation is likely to moderate over the summer. The release of the latest US CPI report for June in the week ahead could provide confirmation that headline inflation has already peaked. Headline inflation is expected to slow to 3.8% in June from 4.2% in May, helped in part by a roughly 10% decline in average US gasoline prices during the month. Market participants will also be watching closely for signs of second-round effects from higher energy prices feeding into underlying inflation. So far, core inflation has increased only modestly since the onset of the US-Iran conflict, accounting for just 0.3 percentage points of the 1.8 percentage point rise in the annual CPI rate since February. Another benign core reading, alongside easing energy inflation, would likely encourage market participants to pare back expectations for further Fed rate hikes, potentially weighing on the USD in the week ahead.

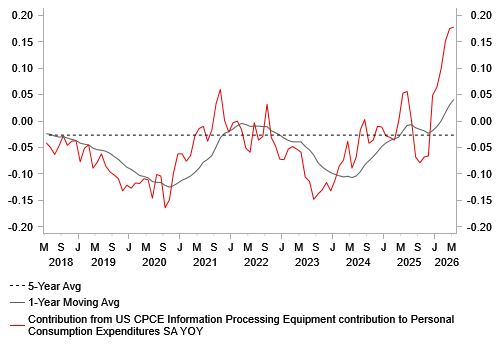

The release of the minutes from the June FOMC meeting indicated that the Fed is in no rush to raise rates as early as this month, given that only “a few” participants supported a rate hike in June. One inflation risk that is attracting increasing attention from Fed officials is the potential boost to demand from surging AI-related capital investment. New York Fed President Williams recently noted that, “if this creates a sustained impulse to demand relative to supply and inflation, then I do think that’s the kind of situation where you don’t look through this.” He added that, “on the other hand, if it doesn’t and things play out in a more benign way, I do think monetary policy is, and continues to be, well positioned.” A breakdown of the Fed’s preferred measure of inflation, the core PCE deflator, suggests that information-processing equipment has started to make a positive contribution, adding 0.18 percentage points to the annual inflation rate of 3.4% in May. This compares with an average annual contribution of -0.03 percentage points over the previous five years. At this stage, the additional upward pressure on core inflation remains relatively modest. However, it has the potential to exert a more meaningful influence on inflation and Fed policy going forward.

HAS US INFLATION ALREADY PEAKED?

Source: Bloomberg, Macrobond & MUFG

BUILDING INFLATIONARY IMPACT FROM AI ROLL OUT

Source: Bloomberg, Macrobond & MUFG

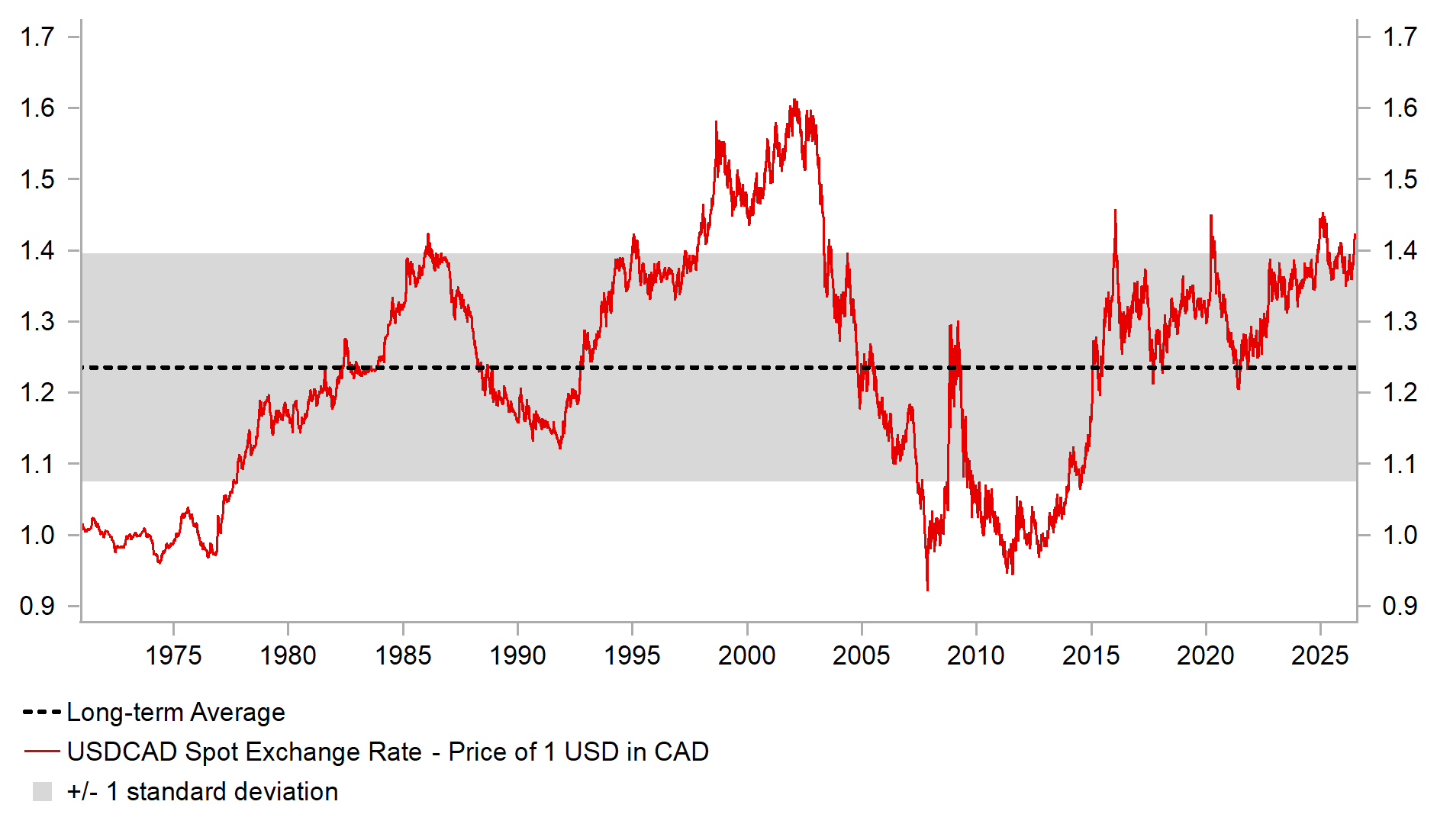

In contrast, market participants remain more confident that the Bank of Canada will keep rates on hold this year than they are about the Fed. As a result, short-term yield spreads have moved sharply against the CAD over the past couple of months, providing a key driver behind USD/CAD’s move back above 1.4000. The latest IMM report highlighted that short CAD positions remain among the most popular trades held by leveraged funds reflecting expectations for further weakness. Expectations that the BoC will remain on hold have been supported by the soft start to the year for Canada’s economy and labour market, although growth has shown signs of improvement in Q2. Even if economic activity is flat in June, Canada’s economy remains on track to expand at an annualized rate of around 2.3% in Q2, following two consecutive quarters of contraction. Canada’s economy has benefitted from the favourable terms of trade effects of higher energy prices. This helped Canada record its largest trade surplus in May in four years. The improvement in Canada’s trade balance has come at a time when trade policy uncertainty has returned to the forefront of market concerns, following the Trump administration’s decision not to renew the USMCA in its current form. While the agreement remains in force until 2036, it will now be subject to a new round of negotiations aimed at revising its terms (click here). Trade policy uncertainty is likely to remain a headwind for the CAD through the remainder of this year.

In light of these developments, we expect the BoC to signal that it remains open both to raising rates in response to upside inflation risks and to lowering rates should US trade restrictions and related uncertainty weaken growth sufficiently. While the rebound in growth during Q2 and the widening trade surplus should help alleviate concerns over downside risks to the economy, the trade policy backdrop remains challenging and is likely to discourage the BoC from adopting a more hawkish tone in the week ahead. US trade policy is likely to attract increased market attention in the coming weeks. The Section 122 tariffs imposed by President Trump after the Supreme Court struck down the IEEPA tariffs on 20th February are due to expire on 24th July. These measures applied a broad 10% surcharge on imports from all countries for a period of up to 150 days. The tariffs are unlikely to be extended, as doing so would risk fresh legal challenges. Instead, they are expected to be replaced by Section 301 tariffs linked to alleged forced labour concerns. The relevant investigation, launched in June and covering 60 economies, is expected to result in proposed duties of between 10% and 12.5%. In addition, the Trump administration has initiated a separate Section 301 investigation into excess industrial capacity and production practices across 16 of its largest trading partners. This inquiry is expected to provide the basis for further tariffs on top of those related to forced labour. The upcoming changes to US trade policy are not expected to result in a significant shift in aggregate tariff rates. As a result, we continue to believe that the inflationary impact from last year’s tariff increases should gradually fade, creating additional scope for the Fed to keep rates on hold.

LEVELS ABOVE 1.4000 TEND TO BE SHORT-LIVED

Source: Bloomberg, Macrobond & MUFG GMR

USD/CAD TO CORRECT LOWER IF FED DOESN’T HIKE

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

Ccy | Date | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

USD | 13/07/2026 | 17:30 | Fed's Waller Speaks at NYABE | !! | |||

USD | 13/07/2026 | 19:00 | Federal Budget Balance | Jun | -- | -$292.6b | !! |

GBP | 13/07/2026 | 19:00 | BoE Chief Economist Pill Speaks | !! | |||

JPY | 14/07/2026 | 05:30 | Industrial Production MoM | May F | -- | 0.5% | !! |

USD | 14/07/2026 | 11:00 | NFIB Small Business Optimism | Jun | 95.5 | 95.3 | !! |

USD | 14/07/2026 | 13:30 | CPI YoY | Jun | 3.9% | 4.2% | !!! |

USD | 14/07/2026 | 15:00 | Fed Chair Warsh testifies | !!! | |||

GBP | 14/07/2026 | 19:00 | BoE Governor Bailey Speech | !!! | |||

CNY | 15/07/2026 | 03:00 | GDP YoY | 2Q | 4.5% | 5.0% | !!! |

CNY | 15/07/2026 | 03:00 | Retail Sales YoY | Jun | -0.1% | -0.6% | !! |

CNY | 15/07/2026 | 03:00 | Industrial Production YoY | Jun | 4.6% | 4.5% | !! |

SEK | 15/07/2026 | 07:00 | CPI YoY | Jun F | -- | 0.7% | !! |

EUR | 15/07/2026 | 10:00 | Industrial Production SA MoM | May | -- | 0.1% | !! |

USD | 15/07/2026 | 13:30 | PPI Final Demand YoY | Jun | -- | 6.5% | !! |

USD | 15/07/2026 | 13:45 | Fed's Williams Delivers Remarks | !! | |||

CAD | 15/07/2026 | 14:45 | Bank of Canada Rate Decision | 15-Jul | 2.25% | 2.25% | !!! |

USD | 15/07/2026 | 19:00 | Fed Releases Beige Book | !! | |||

GBP | 16/07/2026 | 07:00 | Monthly GDP (MoM) | May | -- | -0.1% | !!! |

CHF | 16/07/2026 | 08:30 | SNB Summary of June Decision | !! | |||

USD | 16/07/2026 | 13:30 | Retail Sales Advance MoM | Jun | 0.3% | 0.9% | !!! |

USD | 16/07/2026 | 13:30 | Initial Jobless Claims | -- | -- | !! | |

USD | 16/07/2026 | 15:00 | NAHB Housing Market Index | Jul | 35.0 | 35.0 | !! |

EUR | 17/07/2026 | 09:00 | ECB Current Account SA | May | -- | 15.7b | !! |

EUR | 17/07/2026 | 10:00 | CPI YoY | Jun F | -- | 2.8% | !! |

USD | 17/07/2026 | 13:30 | Import Price Index MoM | Jun | -- | 1.9% | !! |

USD | 17/07/2026 | 13:30 | Housing Starts | Jun | 1320k | 1177k | !! |

USD | 17/07/2026 | 14:15 | Industrial Production MoM | Jun | 0.2% | 0.1% | !! |

USD | 17/07/2026 | 15:00 | U. of Mich. Current Conditions | Jul P | -- | 47.7 | !! |

Source: Bloomberg & MUFG GMR

Key Events:

The BoC is expected to leave rates on hold in the week ahead. Market participants are comfortable with the view that the BoC will keep rates unchanged for most of this year, supported by weak cyclical momentum in the Canadian economy at the start of the year and softer labour demand. While growth appears to have picked up in Q2, there is still scope for the BoC to look through the energy price shock. At the same time, the Bank has indicated that downside risks to growth stemming from trade policy uncertainty leave the option of further rate cuts on the table. The US decision not to extend the USMCA deal on 1st July was widely expected, but persistent trade uncertainty is likely to remain a headwind to growth.

The main economic data release in the week ahead will be the latest US CPI report for June. The report is expected to show that headline inflation slowed to 3.9% in June from 4.2% in May, reinforcing the view that inflationary pressures may have peaked. The average gasoline price fell by more than 10% in June following the agreement between the US and Iran to reopen the Strait of Hormuz. Market participants will also be closely watching core inflation measures to assess whether underlying price pressures are strengthening outside the volatile energy component. Evidence of softer inflation would help to dampen expectations for further Fed rate hikes this year. Fed Chair Warsh will also provide further insights on the US economy and policy when he speaks before Congress when delivering the semi-annual testimony on monetary policy.

The release of the latest activity data from China is expected to confirm a further loss of growth momentum in Q2. Quarterly GDP growth is forecast to slow to 1.0% in Q2 from 1.3% in Q1, highlighting the ongoing drag from weak domestic demand. Consumer spending remains subdued, with the annual rate of retail sales growth expected to remain in negative territory in June for a second consecutive month. The data would reinforce concerns that domestic demand continues to weigh on China's economic recovery.