To read the full report, please download PDF.

Bond markets in focus – USD to strengthen further

FX View:

The US dollar gained 1.4% last week (DXY), the biggest gain since the first week following the start of the conflict in the Middle East. For much of the time after that initial gain, the dollar has underperformed expectations given the jump in crude oil prices. A muted move in US yields partially explained that (along with strong equity market performances) and last week the 2-year yield in the US increased for the fourth consecutive week and by close to 20bps. This is now having a more notable FX influence with expectations of Fed rate hikes increasing. A rate hike by January next year is now 85% priced and this increased conviction is providing the dollar with increased support. In this context, the FOMC minutes, released on Wednesday will prove important and will likely reveal a growing opposition to rate cuts amongst FOMC members. We see scope for the dollar to advance further over the short-term with the Gilt market looking more vulnerable and hence GBP at a greater risk than say JPY given the threat of intervention could curtail JPY selling.

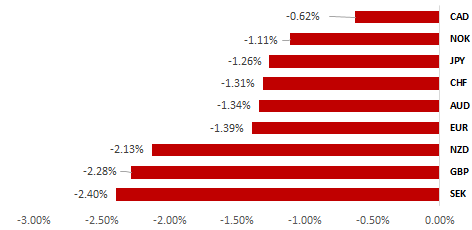

BROAD-BASED USD STRENGTH AS INFLATION FEARS LIFT YIELDS

Source: Bloomberg, close on 15th May 2026 (Weekly % Change vs. USD)

Trade Ideas:

We are maintaining long AUD/SEK and short GBP/CHF trade ideas.

JPY Flows:

The monthly Transactions in International Securities data for April was released last week and after a record sale of Japanese equities by foreign investors in March April saw record buying.

GMR Economic Indicators:

US Inflation is increasingly cost-driven and energy-led, supporting higher yields and near-term USD strength. However, the absence of clear Fed validation is helping to cap further upside for now.

FX Views

USD: Yield influencing FX again as Fed seen hiking

The US dollar advanced by 1.4% last week, the biggest weekly gain since the first week of the conflict in early March. It was a bad mix for bond markets last week with Brent crude oil advancing by nearly 8%, the Strait of Hormuz remaining closed, strong inflation data prints and the start of Kevin Warsh as Fed Chair. Warsh has yet to be sworn in so Powell’s term has been extended temporarily. To accommodate incoming Fed Chair Warsh, given Jay Powell is staying on as a governor, Steve Miran will step down. Hence, the board of governors has become a little more hawkish. Miran stated that he was excited about the changes to come under Warsh, which are expected to include changes to how the Fed communicates to the market and uses forward guidance and changes to the Fed’s balance sheet policy. But the change in leadership has come just as inflation data shows the immediate impact of the conflict. Both the CPI and PPI reports for April were stronger than expected. The 2-year UST bond yield jumped 19bps last week, closing above the 4.00% level for the first time since June last year. The OIS market now shows a 25bp hike is now fully priced by the March 2027 meeting. Fed Chair Warsh’s first public comments as Chair will be crucial for the markets and any hint of being concerned over inflation risks could have a notable near-term impact on market expectations and prompt a further pricing of rate hikes. That’s the near-term risks which would propel the US dollar further stronger.

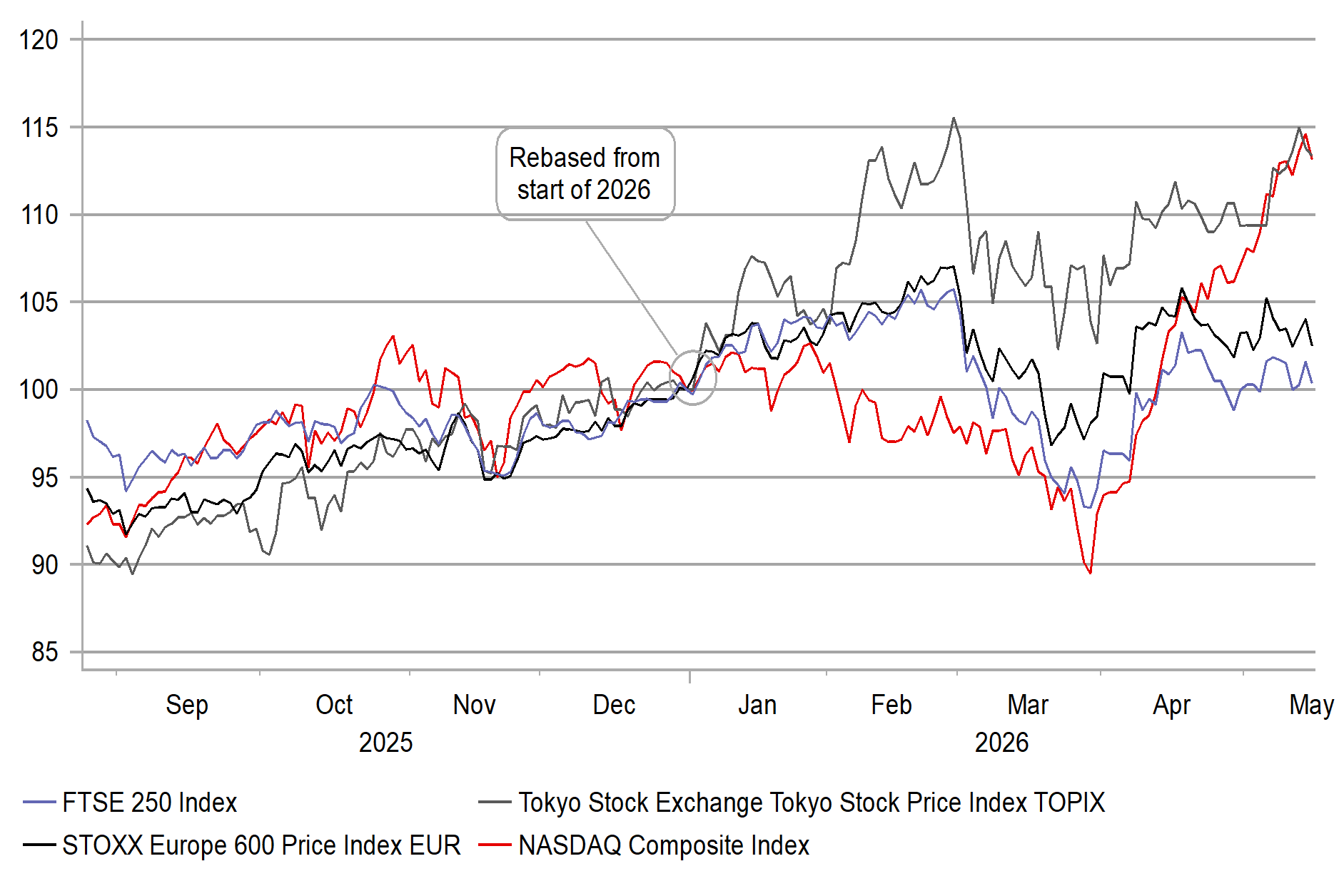

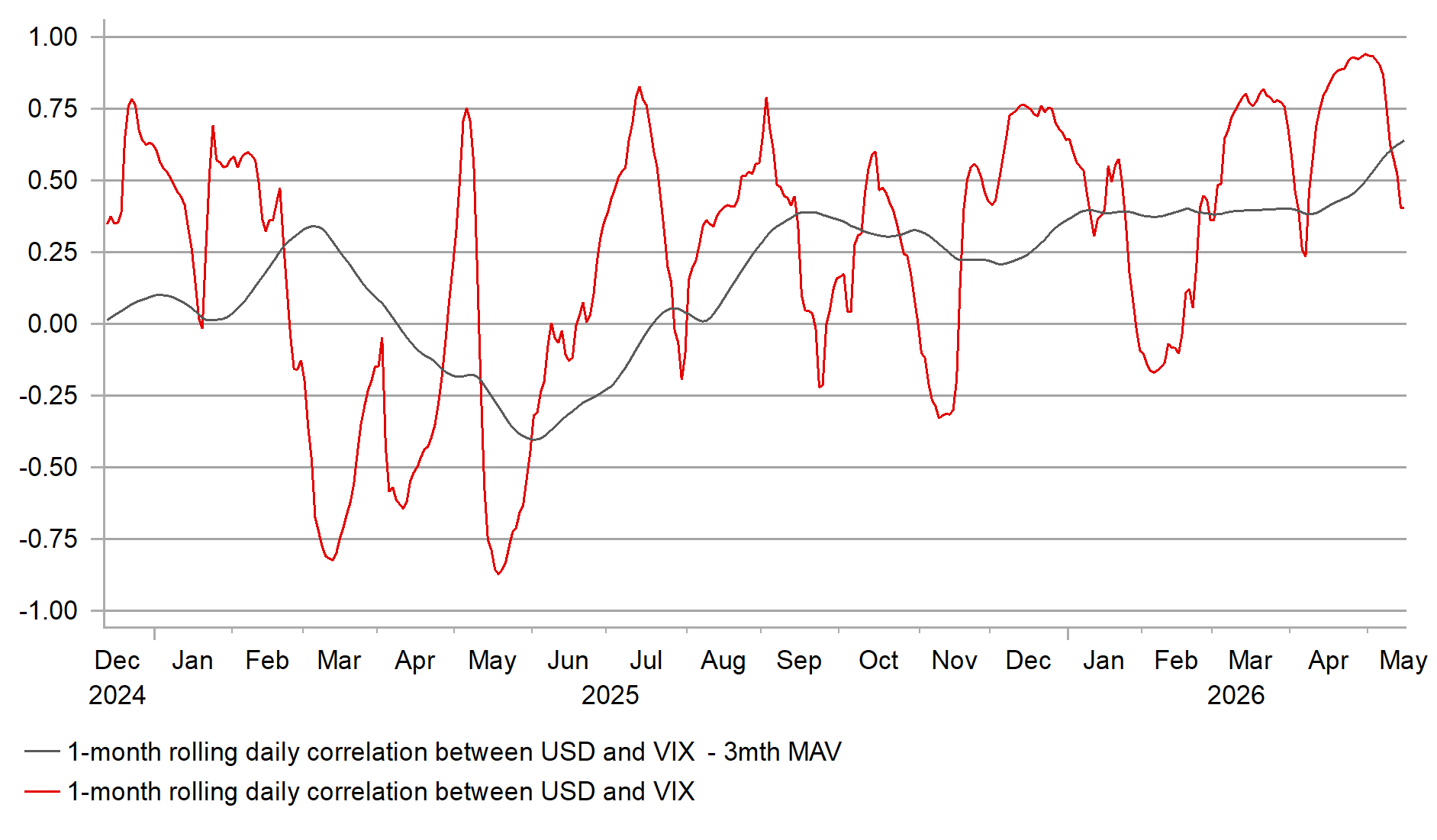

The sheer scale of equity market advance on AI optimism is not sustainable and with the corporate earnings reporting for Q1 ending, we may be about to see a period of more subdued momentum. The Nasdaq closed on Friday 26.1% from the close toward the end of March fuelled by a huge 27.7% increase in YoY corporate earnings with 89% of companies reported. The tech sector alone saw YoY earnings growth of 50.7% while semiconductors & semiconductor equipment saw YoY growth in earnings of 99%. All of this very positive news is now in the price and hence the strength in risk appetite may fade somewhat, especially if other factors (rising yields & crude oil) continue. Our rolling daily correlation (30-days) between risk (VIX) and the dollar has started to weaken while the correlation between DXY and 2-year US-DXY spreads has started to pick up. This makes sense and if pricing for Fed rate hikes continues to pick up, the yield/FX correlation is likely to strengthen further and drive the dollar stronger.

Kevin Warsh was confirmed last week in the Senate by a vote of 54-45 – the most divided Senate confirmation vote for a new Fed Chair. Warsh made clear in his nomination hearing that Fed policy required a “regime change”. In November he argued in the WSJ that AI will be a “significant disinflationary force” which is probably the reasoning he used when he no doubt agreed with President Trump that rates be cut going forward. But the crucial question for the markets is – how quickly will Warsh begin to push for lower rates? If the Strait of Hormuz remains closed and energy prices rise, we would assume the focus will be initially elsewhere. The FOMC minutes from the April meeting will be released on Wednesday and we may well see a growing concern over inflation risks that would likely make Warsh cautious on opening up a policy disagreement with FOMC colleagues at the outset of his tenure. He may instead push quickly to alter guidance norms, suggest fewer speeches and possibly quickly attempt to discard the median dots profile. A more balanced assessment of inflation risks by the new Chair is a very plausible scenario given where the risks lie currently and that could offer further impetus to higher US yields over the coming weeks.

US & JAPAN GAINS FUELLED BY TECH; EUROPE LAGS

Source: Bloomberg, Macrobond & MUFG GMR

USD CORRELATION WITH RISK HAS WEAKENED

Source: Bloomberg, Macrobond & MUFG GMR

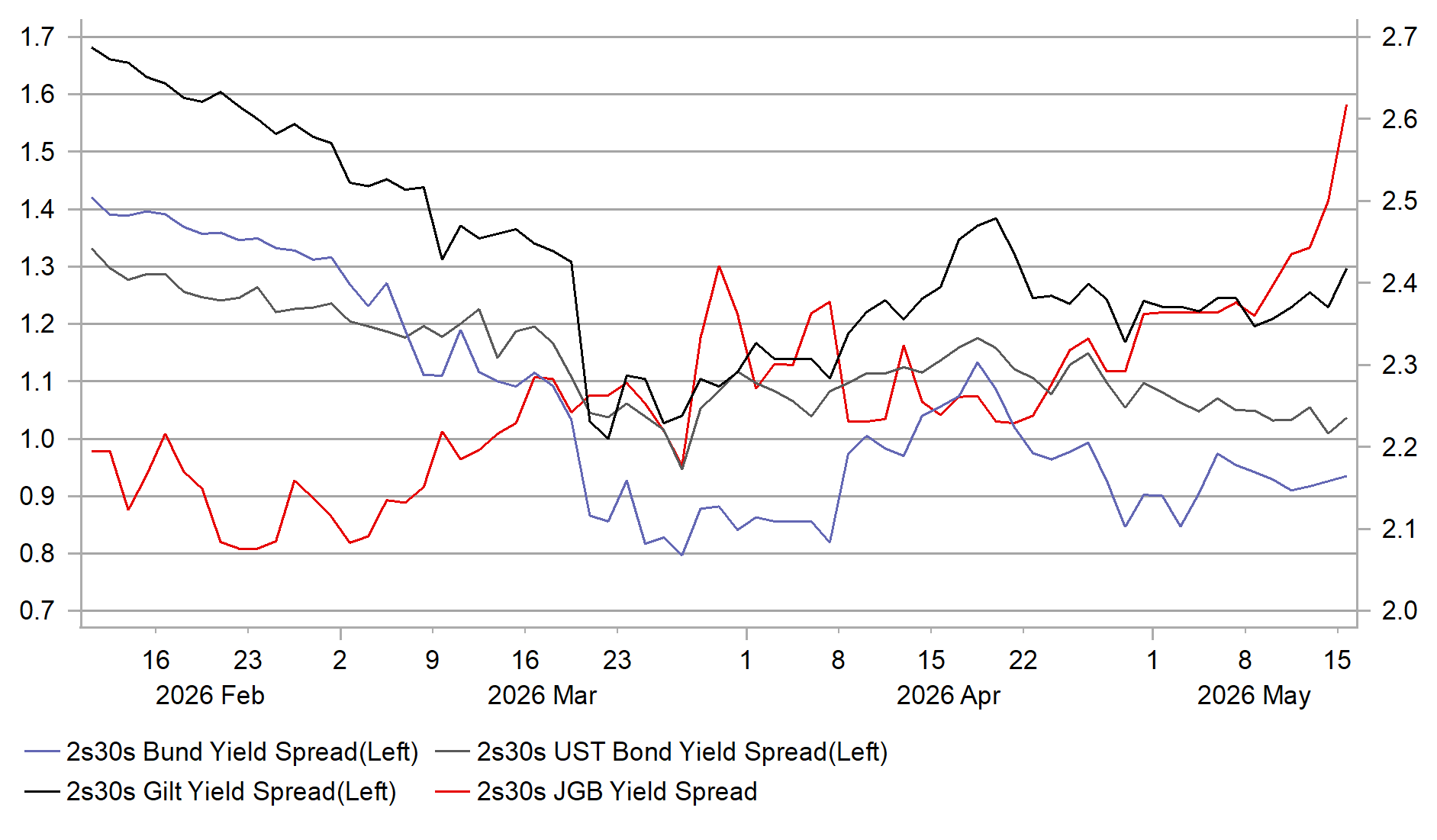

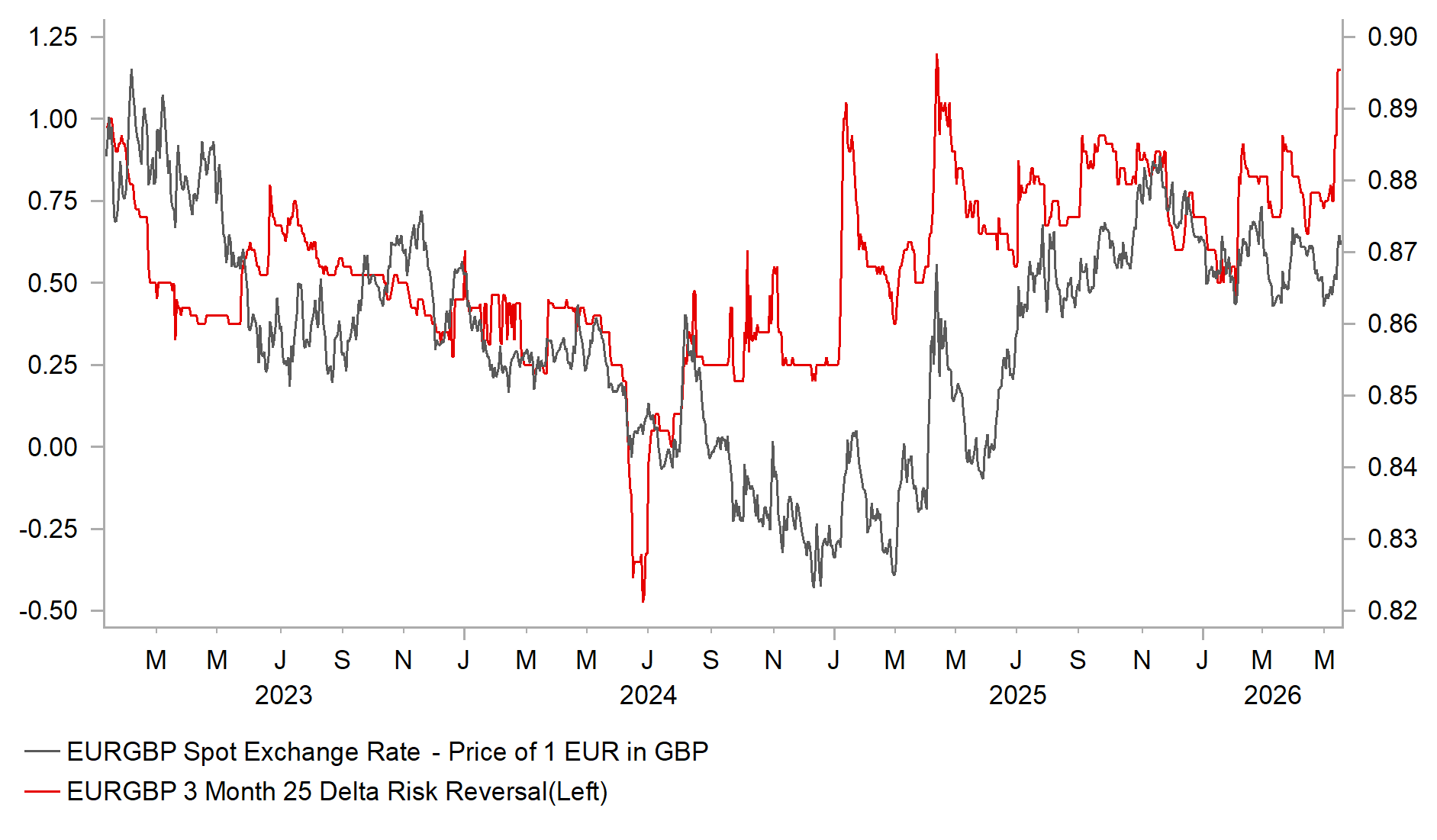

While it could be argued that yields in the US are rising for positive reasons – resilient growth, AI-related equity market surge and higher inflation, the sell-off in fixed income in Japan and the UK are for less positive reasons. The BoJ is increasingly seen as behind the curve with the real policy rate still below a range of neutral R*. Today, PM Takaichi confirmed that the government will compile another supplementary budget to support households. The JGB market response was as expected today – the 2s30s JGB spread has widened by 32bps this month alone and is 56bps steeper since the conflict began. 2s30s in the US, the UK and Germany have flattened since the conflict began. The BoJ needs to act to restore confidence. Intervention also looks highly likely to fail with risks of further action considerable. The 30-year Gilt yield jumped nearly 20bps on Friday and fiscal uncertainties are likely to persist for months as Andy Burnham first seeks to win a seat in parliament and then potentially a leadership challenge. Burnham is known for his support for increased borrowing to fund public investment spending for social housing and infrastructure. A change in the government fiscal rules could be pursued which will inevitably destabilise the Gilt market further. That said, comments over the weekend that a Burnham premiership would continue to stick to the current fiscal rules has helped stabilise the Gilt market so far today.

We see further global bond market instability as the primary risk over the short-term and with crude oil prices drifting further higher and the risks of re-escalation in the conflict in the Middle East, inflation fears will continue to intensify. European rates markets look better priced for that scenario than the US and hence we could see further US yield rises relative to Europe, driving the US dollar further stronger. Risk appetite could also fade somewhat given Q1 corporate earnings reporting is near completion. The pound is currently the second worst performing G10 currency this month and in a scenario of further global bond market selling we would expect the pound to continue to underperform versus the dollar and relative to other G10 currencies.

2S30S JGB CURVE STEEPENING SHARPLY

Source: Bloomberg, Macrobond & MUFG GMR

EUR/GBP RISK-REVERSAL HIGHEST SINCE APRIL ‘25

Source: Bloomberg, Macrobond & MUFG GMR

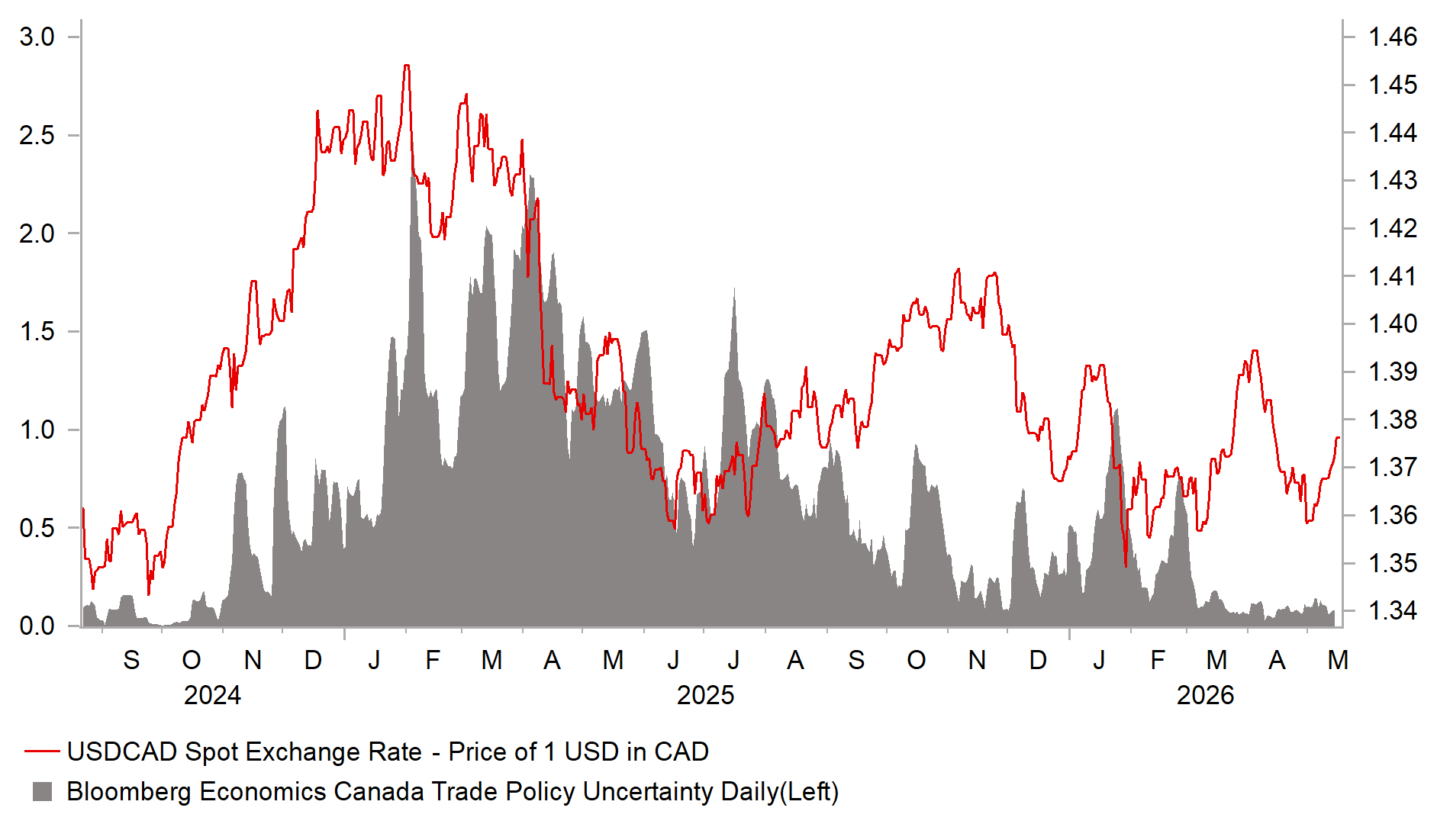

CAD: Will upcoming USMCA trade review threaten USD/CAD stability?

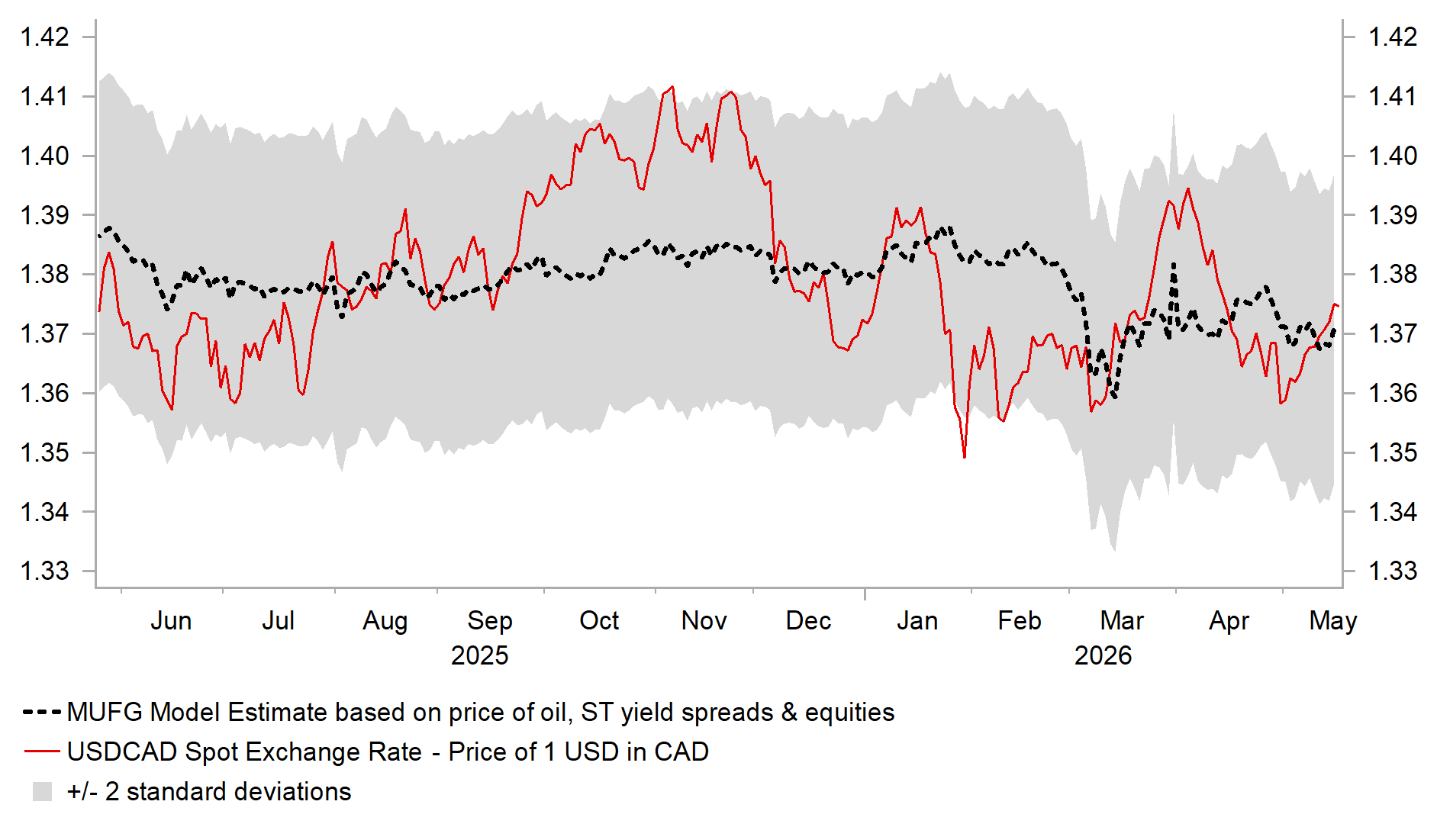

The CAD has weakened against the USD over the past week, after USD/CAD failed to break below the lower end of the 1.3500–1.3900 trading range that has persisted for most of this year. The USD has been supported both by the lack of progress in negotiations between Iran and the U.S. to end the conflict and reopen the Strait of Hormuz, and by a recent run of upside U.S. economic data surprises that has prompted a more hawkish repricing of Fed rate expectations. Our short-term valuation model for USD/CAD incorporating oil prices, yield differentials, and equity market performance, suggests that fundamentals are currently unlikely to drive a breakout from the current 1.3500–1.3900 trading range in the near term.

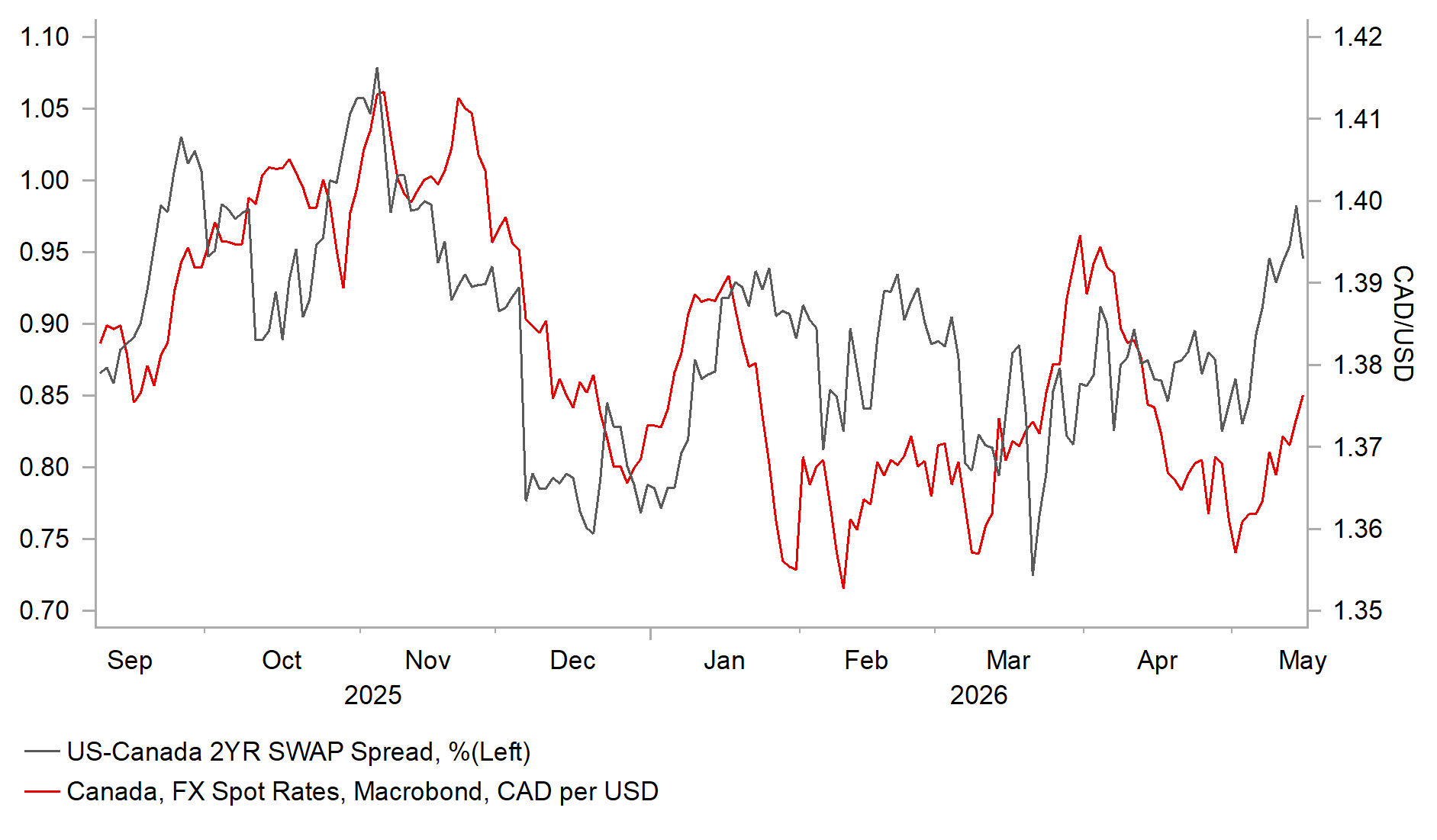

Fundamental support for the CAD from higher energy prices is currently being offset by a widening in yield differentials against Canada. A recent run of softer Canadian economic data has dampened market expectations that the BoC will tighten policy in response to the energy price shock. The labour market has remained weak at the start of the year, with employment declining in three of the past four months, for a cumulative loss of around 112k jobs. While the economy appears to have returned to growth in Q1 following a contraction of 0.6% in Q4, the broader outlook remains subdued. We expect growth to slow further to around 1.2% in 2026, down from 1.7% in 2025. This combination of weak growth and a soft labour market should provide the BoC with greater scope to look through higher inflation, even with the policy rate already at the lower end of its estimated neutral range of 2.25%–3.25%. At its latest policy meeting, the BoC indicated that, if oil prices decline and U.S. tariffs remain unchanged, the current policy stance would remain appropriate. However, if energy prices stay elevated, further tightening could still be required to prevent a more persistent inflationary impulse. Conversely, a material escalation in U.S. trade restrictions on Canada could prompt rate cuts to support growth.

Trade policy uncertainty is likely to rise in the coming months ahead of the 1st July deadline for the USMCA review. The agreement signed during President Trump’s first term is designed to run for 16 years, expiring on 1st July 2036. Under Article 34.7, the U.S., Mexico and Canada are required to conduct a formal review at the six‑year mark on 1st July 2026. The review is expected to involve a substantive renegotiation of key provisions, including regional value content rules, minimum U.S. content requirements, and the treatment of China—particularly in the context of the USMCA’s non‑market economy clause, which constrains deeper trade integration with China. The Centre for Strategic & International Studies (CSIS) has outlined several potential pathways for the review, highlighting a wide range of possible outcomes depending on the degree of consensus among the three parties.

FUNDAMENTALS FAVOUR USD/CAD STABILITY

Source: Bloomberg, Macrobond & MUFG GMR

YIELDS SPREADS SUPPORTING HIGHER USD/CAD

Source: Bloomberg, Macrobond & MUFG GMR

First, all three countries could agree to extend the USMCA for a further 16 years, through to 2042, with only targeted updates to modernize the agreement without altering its core architecture. This would likely be the most supportive outcome for regional supply chains and capital investment, as it would provide more certainty. While Canada and Mexico have signalled support for a clean extension, this outcome appears unlikely given the U.S. has clearly indicated a preference for more substantive changes. Second, Canada and Mexico could face pressure to make meaningful concessions to the Trump administration in exchange for reducing U.S. tariffs and securing an extension of the agreement. Under this scenario, negotiations could extend into late 2026 or beyond, prolonging policy uncertainty. Some concessions could be costly for Canada and Mexico, particularly in areas such as rules of origin and market access, while also resulting in trade policy uncertainty dragging on for longer.

Third, if no agreement is reached this year to extend the USMCA, the treaty would move into a cycle of annual reviews. While the agreement would remain in force, its future would become more uncertain, creating a recurring “cliff edge” that could discourage long-term investment. Fourth, if trilateral consensus proves unattainable, the parties could pivot to bilateral agreements between the U.S. and Mexico, and the U.S. and Canada, as a fallback option. Such an outcome would likely fragment the current framework and disrupt highly integrated North American supply chains. Fifth, it is also possible that one country could decide to withdraw early from the agreement, which requires six months’ notice. The Trump administration has previously used the threat of withdrawal as leverage to extract concessions and accelerate negotiations. This would represent the most disruptive outcome for regional trade and investment. Across these scenarios, the CSIS assesses that a “painful extension” involving protracted negotiations and meaningful concessions is the most likely outcome followed by “serial annual reviews”. By contrast, the most disruptive outcome, “early withdrawal”, is judged as the least likely but can’t be completely ruled out.

In this context, trade policy uncertainty is likely to become a bigger headwind for the Canadian economy in the second half of the year. The CAD could weaken more if market participants become fearful about the risk of potential USMCA withdrawal, although any such move by the Trump administration would likely be initially interpreted as a negotiating tactic aimed at extracting concessions from Canada and Mexico. Heightened trade policy uncertainty is one potential trigger that could see USD/CAD test the top of the current trading range between 1.3500 and 1.3900. Other likely scenarios including shifting to annual reviews or pivoting to bilateral trade deals would also be disruptive for regional trade and economies but pose relatively less downside risks for the CAD. Our baseline remains a “painful extension” later in 2026, involving concessions from Canada and Mexico that help secure an eventual renewal of the agreement. Under this scenario, CAD weakness should be more contained.

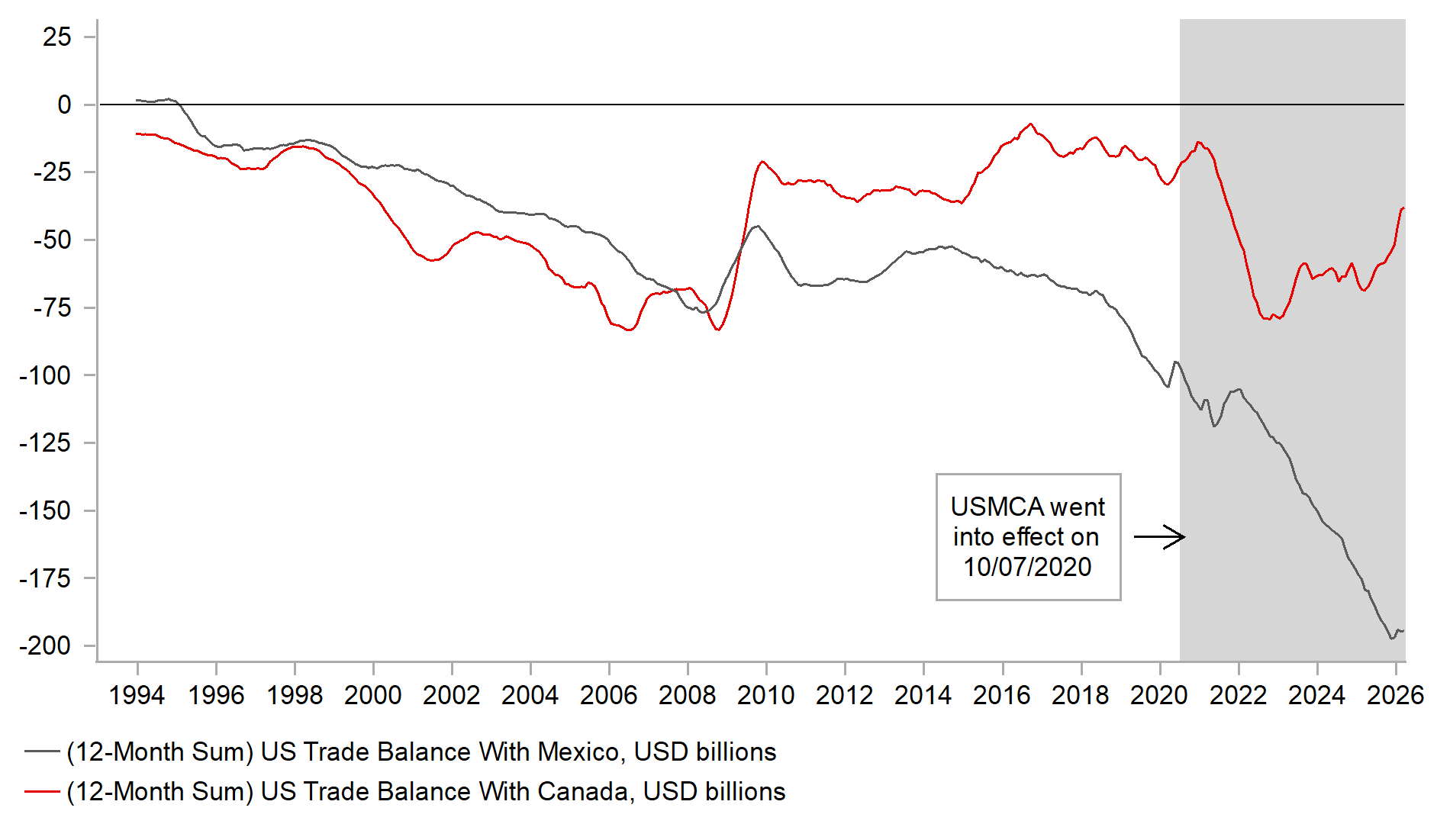

MUCH WIDER US TRADE DEFICIT WITH MEXICO

Source: Bloomberg, Macrobond & MUFG GMR

TRADE UNCERTAINTY LESS OF A HEADWIND FOR CAD

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

Ccy | Date | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

JN | 16/05/2026 | Tbc | BOJ Deputy Governor Himino Speaks | !!! | |||

UK | 18/05/2026 | 08:35 | BoE member Greene Speaks | !! | |||

UK | 18/05/2026 | 09:30 | BoE member Mann Speaks | !! | |||

US | 18/05/2026 | 15:00 | NAHB Housing Market Index | May | 34.0 | 34.0 | !! |

JN | 19/05/2026 | 00:50 | GDP Annualized SA QoQ | 1Q P | 1.6% | 1.3% | !!! |

AU | 19/05/2026 | 02:30 | RBA Minutes of May Policy Meeting | !!! | |||

UK | 19/05/2026 | 07:00 | Payrolled Employees Monthly Change | Apr | -- | -11k | !!! |

EC | 19/05/2026 | 10:00 | Trade Balance SA | Mar | -- | 7.0b | !! |

EC | 19/05/2026 | 13:00 | ECB's Lane Speaks | !! | |||

CA | 19/05/2026 | 13:30 | CPI YoY | Apr | 2.9% | 2.4% | !!! |

US | 20/05/2026 | 00:00 | Fed's Paulson Speaks | !! | |||

UK | 20/05/2026 | 07:00 | CPI YoY | Apr | -- | 3.3% | !!! |

EC | 20/05/2026 | 10:00 | CPI YoY | Apr F | -- | 3.0% | !!! |

US | 20/05/2026 | 19:00 | FOMC Meeting Minutes | -- | -- | !!! | |

JN | 21/05/2026 | 00:50 | Trade Balance | Apr | -¥69.2b | ¥667.0b | !! |

AU | 21/05/2026 | 02:30 | Employment Change | Apr | 21.8k | 17.9k | !!! |

EC | 21/05/2026 | 09:00 | ECB Current Account SA | Mar | -- | 24.9b | !! |

EC | 21/05/2026 | 09:00 | Eurozone Manufacturing PMI | May P | 51.5 | 52.2 | !!! |

EC | 21/05/2026 | 09:00 | Eurozone Services PMI | May P | 48.4 | 47.6 | !!! |

UK | 21/05/2026 | 09:30 | UK Manufacturing PMI | May P | -- | 53.7 | !!! |

UK | 21/05/2026 | 09:30 | UK Services PMI | May P | -- | 52.7 | !!! |

US | 21/05/2026 | 13:30 | Initial Jobless Claims | -- | -- | !! | |

US | 21/05/2026 | 13:30 | Housing Starts | Apr | 1420k | 1502k | !! |

US | 21/05/2026 | 13:30 | Building Permits | Apr P | 1385k | 1363k | !! |

US | 21/05/2026 | 14:45 | US Composite PMI | May P | -- | 51.7 | !! |

JN | 22/05/2026 | 00:30 | Natl CPI YoY | Apr | 1.7% | 1.5% | !!! |

UK | 22/05/2026 | 07:00 | Public Sector Net Borrowing | Apr | -- | 12.6b | !! |

GE | 22/05/2026 | 07:00 | GDP SA QoQ | 1Q F | 0.3% | 0.3% | !!! |

UK | 22/05/2026 | 07:00 | Retail Sales Inc Auto Fuel MoM | Apr | -- | 0.7% | !! |

GE | 22/05/2026 | 09:00 | IFO Business Climate | May | -- | 84.4 | !! |

CA | 22/05/2026 | 13:30 | Retail Sales MoM | Mar | 0.7% | 0.7% | !! |

Source: Bloomberg & MUFG GMR

Key Events:

Prime Minister Takaichi’s call for another supplementary budget has unsettled JGB market participants at the start of this week. Investors will be watching closely for any indication of the potential size of the package and the associated level of debt issuance. Fiscal concerns are contributing to higher yields in Japan, alongside recent hawkish remarks from BoJ member Kazuyuki Masu, who indicated that it would be desirable to raise the policy rate at the “earliest possible stage” if incoming data do not point to a clear economic downturn. The release of Japan’s April CPI report in the week ahead will provide further insight into how the recent energy price shock is feeding through to inflation.

UK political developments are also expected to remain in focus in the week ahead. With Prime Minister Starmer set to face a leadership challenge, market participants will be watching closely to see who enters the contest. Potential candidates must secure the backing of 81 MPs to participate, after which Labour Party members and affiliates will vote to select the new leader. The timetable for the vote remains unclear. At the same time, the latest UK labour market and CPI reports are due for release. Another upside inflation surprise would tilt the BoE further towards tightening policy in response to the energy price shock.

In the US, the main data release will be the minutes from the April FOMC meeting. At that meeting, the Fed held rates steady and maintained its easing bias, although three regional Fed presidents dissented against keeping forward guidance unchanged. The minutes are likely to provide further insight into how close the Fed is to dropping its easing bias. However, with Kevin Warsh set to take over as Fed Chair in June, the minutes may appear more dated than usual.