To read the full report, please download PDF.

Is the USD approaching a pivot point?

FX View:

The USD has been consolidating at higher levels over the past week, remaining close to the highs recorded since the Middle East conflict began in late February. The week ahead could prove to be an important near-term pivot point for the USD. There is growing investor optimism that the US and Iran may soon reach an agreement to end the conflict and reopen the Strait of Hormuz. If a deal is announced as early as this weekend, it could put downward pressure on the USD. At the same time, the Fed will hold its first policy meeting under new Chair Kevin Warsh. This meeting should provide greater clarity on how Fed policy is likely to respond to the energy price shock. If Warsh signals a willingness to look through the inflation shock and keep rates on hold, it could reinforce USD weakness following a US-Iran deal. In contrast, if he indicates that rate hikes may be required, it could open the door for the USD to strengthen further. Meanwhile, the BoJ is expected to raise rates and maintain its path of gradual tightening. On its own, this policy update is unlikely to provide significant support for the JPY, although it could be reinforced by lower energy prices following a US-Iran deal.

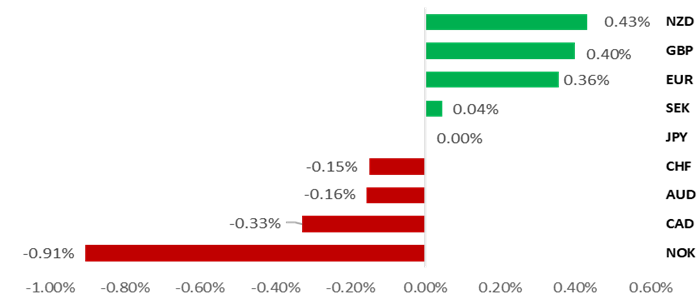

G10 COMMODITY CURRENCIES UNDERPERFORM

Source: Bloomberg, close on 12th June 2026 (Weekly % Change vs. USD)

Trade Ideas:

We have closed our long GBP/CHF trade idea. We are waiting to establish new recommendations after this week’s event risks have passed.

IMM FX Positioning:

Our positioning z‑scores indicate that short NZD and long AUD positions are the most stretched relative to their levels over the past two years.

Analysing Market Reaction to Fed Chair Transitions:

Warsh inherits a relatively muted macro backdrop favouring gradual policy changes. Analysing historical market reactions around the first Fed Chair press conferences, US front-end yields tend to move immediately as markets rapidly reprice while the USD reacts with more of a lag.

FX Views

G10 FX: Middle East deal optimism builds ahead of pivotal FOMC meeting

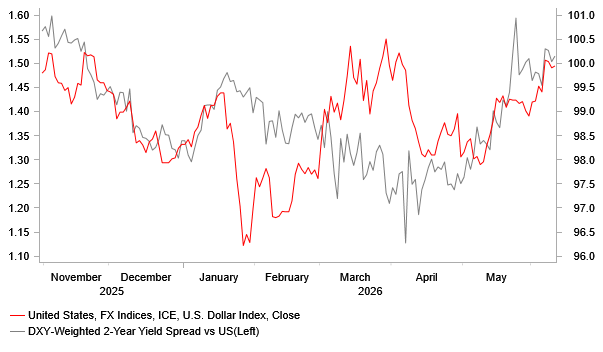

The USD has continued to trade at stronger levels this week, with the dollar index moving back above the 100.00 level following the release of the May nonfarm payrolls report. A third consecutive month of robust US employment growth has helped to ease concerns about downside risks to the labour market. As a result, there is now less justification for the Fed to lower rates further. This should encourage the Fed to place greater emphasis on upside risks to inflation when setting monetary policy. The US rates market has adjusted accordingly, pricing in a higher probability that the Fed’s next policy move will be a hike rather than a cut. US yields have been rising over the past month, more so than in other developed fixed income markets, leading to a renewed widening of yield differentials in favour of a stronger USD. At the same time, the influence of yield differentials on FX market performance has strengthened.

The latest US economic data have, on balance, surprised to the upside for both activity and inflation, reinforcing market expectations of a more hawkish Fed policy update at the upcoming FOMC meeting. Following dissents from three Fed Presidents (Cleveland Fed President Hammack, Dallas Fed President Logan, and Minneapolis Fed President Kashkari) at the April FOMC meeting, removing the easing bias this month appears to be a logical next step. The updated Summary of Economic Projections is also likely to show reduced support for further rate cuts. The previous set of projections in March indicated that 12 out of 19 FOMC participants favoured at least one rate cut by the end of this year, while 11 out of 19 anticipated at least two cuts by the end of next year. If the easing bias is removed, it is unlikely that a majority will continue to support at least one cut this year. Market participants will also be watching closely for evidence of growing support for rate hikes. In April, only one FOMC participant projected higher rates in 2027 and 2028.

However, the biggest unknown is how Fed policy and communication will evolve under the leadership of the new Fed Chair, Kevin Warsh, who will preside over his first FOMC meeting. There is a widely held view that Chair Warsh will signal a willingness to look through the energy price shock and instead emphasise the disinflationary impact of stronger productivity growth. This would leave the door open to rate cuts once the worst of the energy shock has passed. This outlook is a key reason why we continue to expect the Fed’s next policy move to be a rate cut rather than a hike, supporting our forecast for further USD weakness heading into 2027 (click here). Warsh’s first press conference as Fed Chair will serve as an important test of that view. If he instead signals that rate hikes are under consideration in response to the energy price shock, it could open the door for a stronger USD.

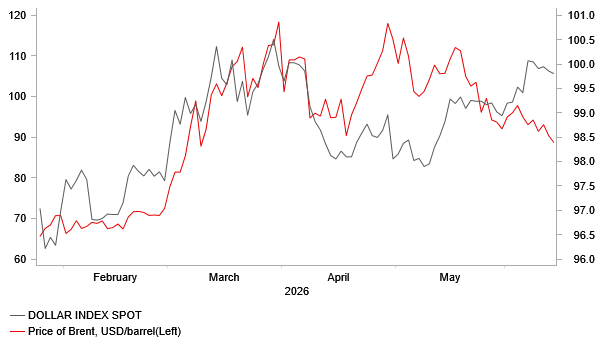

LOWER OIL PRICE TO WEIGH ON USD IF DEAL

Source: Bloomberg, Macrobond & MUFG GMR

WIDENING YIELD SPREADS SUPPORTING USD

Source: Bloomberg, Macrobond & MUFG GMR

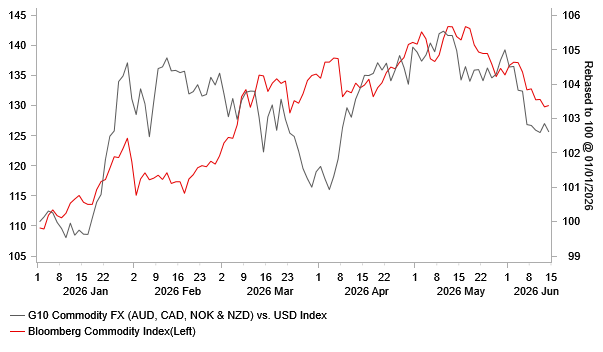

The outlook for Fed policy remains closely tied to developments in the Middle East. There is growing optimism toward the end of this week that the US and Iran are nearing a deal to end the conflict and reopen the Strait of Hormuz. Bloomberg has reported that a senior Iranian official suggested an agreement is likely, citing an unnamed G7 official. A memorandum of understanding could be signed as early as this Sunday, ahead of next week’s G7 Summit in France from 15th-17th June. Energy prices have already responded to the prospect of the Strait reopening, with crude oil falling back toward the low-to-mid USD 80s per barrel. A faster normalisation of energy supplies in the Middle East would help dampen upside inflation risks, thereby giving the Fed more scope to look through higher inflation in the coming months. The combination of lower energy prices and a scaling back of Fed rate hike expectations is likely to weigh on the US dollar. At the same time, a broader correction lower in commodity prices is underway, contributing to the recent underperformance of G10 commodity currencies such as the NOK, CAD, and AUD. Bloomberg’s commodity price index peaked on 18th May and has since fallen by just over 10%, retracing almost two-thirds of its earlier gains linked to the Middle East conflict. A deal would also reinforce favourable conditions for FX carry trades by dampening market volatility.

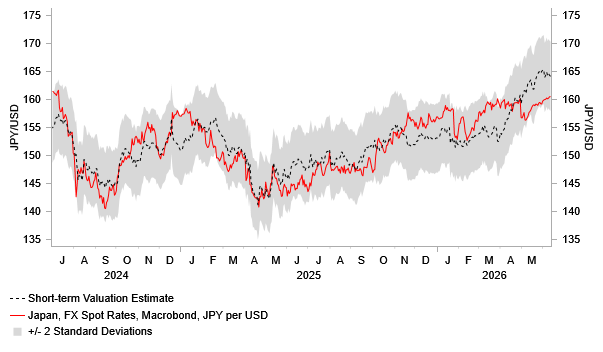

Policymakers in Japan will be hoping that a US-Iran deal helps to ease selling pressure on the JPY if the Strait of Hormuz reopens soon and energy prices continue to decline. It should also give the BoJ greater confidence to continue normalising monetary policy after holding back from raising rates in April in response to heightened uncertainty in the Middle East. Media reports from Japan this week have strongly signalled that the BoJ is preparing to raise rates at its upcoming policy meeting. It has since been reported that Governor Ueda will not attend due to ill health, although this is not expected to alter the policy decision. Deputy Governor Himino will chair the meeting, while Deputy Governor Uchida is scheduled to stand in for the Governor at the post-meeting press conference. Governor Ueda is expected to submit his views in writing, suggesting that the direct impact on the rate decision should be limited. However, a change in speaker can affect how the same message is perceived by markets, increasing the risk of larger moves in Japanese rates and the JPY. Some market participants may anticipate a slightly more hawkish tone from Deputy Governor Uchida compared with Governor Ueda. Even so, we expect updated guidance to reiterate that further gradual tightening is likely if the economy evolves in line with expectations, with another hike likely later this year. The Japanese rates market is already well priced for this scenario, which should limit support for the JPY. If the JPY continues to weaken, pushing USD/JPY further above 160.00, we would then expect verbal intervention to pick up again following the BoJ’s policy meeting.

G10 COMMODITY CURRENCIES CORRECTING LOWER

Source: Bloomberg, Macrobond & MUFG GMR

INTERVENTION HAS PREVENTED EVEN WEAKER JPY

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

Ccy | Date | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EUR | 15/06/2026 | 10:00 | Industrial Production SA MoM | Apr | -- | 0.2% | !! |

EUR | 15/06/2026 | 10:00 | Trade Balance SA | Apr | -- | 3.5b | !! |

USD | 15/06/2026 | 14:15 | Industrial Production MoM | May | 0.2% | 0.7% | !! |

JPY | 16/06/2026 | Tbc | BOJ Target Rate | 1.00% | 0.75% | !!! | |

AUD | 16/06/2026 | 05:30 | RBA Cash Rate Target | 4.35% | 4.35% | !!! | |

EUR | 16/06/2026 | 10:00 | Germany ZEW Survey Expectations | Jun | -- | -10.2 | !! |

EUR | 16/06/2026 | 10:00 | Labour Costs YoY | 1Q F | -- | 3.4% | !! |

USD | 16/06/2026 | 13:30 | Import Price Index MoM | May | -- | 1.9% | !! |

USD | 16/06/2026 | 13:30 | Housing Starts | May | 1440k | 1465k | !! |

EUR | 16/06/2026 | 14:10 | ECB's Lane Speaks | !! | |||

GBP | 17/06/2026 | 07:00 | CPI YoY | May | -- | 2.8% | !!! |

GBP | 17/06/2026 | 07:00 | PPI Output NSA YoY | May | -- | 4.0% | !! |

SEK | 17/06/2026 | 08:30 | Riksbank Policy Rate | 1.75% | 1.75% | !!! | |

EUR | 17/06/2026 | 09:00 | ECB Wage Tracker | !!! | |||

EUR | 17/06/2026 | 10:00 | CPI YoY | May F | -- | 3.2% | !! |

USD | 17/06/2026 | 13:30 | Retail Sales Advance MoM | May | 0.4% | 0.5% | !! |

USD | 17/06/2026 | 19:00 | FOMC Rate Decision (Upper Bound) | 3.75% | 3.75% | !!! | |

USD | 17/06/2026 | 19:30 | Fed Holds Press Conference | !!! | |||

GBP | 18/06/2026 | 07:00 | Makerfield by-election | !!! | |||

GBP | 18/06/2026 | 07:00 | Payrolled Employees Monthly Change | May | -- | -100k | !!! |

CHF | 18/06/2026 | 08:30 | SNB Policy Rate | 0.00% | 0.00% | !!! | |

CHF | 18/06/2026 | 09:00 | SNB's Schlegel Speaks | !!! | |||

NOK | 18/06/2026 | 09:00 | Deposit Rates | 4.25% | 4.25% | !!! | |

EUR | 18/06/2026 | 09:00 | ECB Current Account SA | Apr | -- | 14.9b | !! |

GBP | 18/06/2026 | 12:00 | Bank of England Bank Rate | 3.75% | 3.75% | !!! | |

USD | 18/06/2026 | 13:30 | Initial Jobless Claims | -- | -- | !! | |

JPY | 19/06/2026 | 00:30 | Natl CPI YoY | May | 1.5% | 1.4% | !! |

GBP | 19/06/2026 | 07:00 | Public Sector Net Borrowing | May | -- | 24.3b | !! |

GBP | 19/06/2026 | 07:00 | Retail Sales Inc Auto Fuel MoM | May | -- | -1.3% | !! |

CAD | 19/06/2026 | 13:30 | Retail Sales MoM | Apr | -- | 0.9% | !! |

EUR | 19/06/2026 | 15:30 | ECB's Lane Speaks in London | !! |

Source: Bloomberg & MUFG GMR

Key Events:

There is a busy schedule of G10 central bank policy updates in the week ahead, including meetings from the BoJ (Tuesday), RBA (Tues), Riksbank (Wednesday), Fed (Wednesday), SNB (Thursday), Norges Bank (Thursday), and BoE (Thursday).

The BoJ has indicated that it is planning to raise rates by 25bps in response to upside inflation risks, even as uncertainty related to the Middle East conflict remains elevated. At the same time, media reports suggest that the BoJ is considering pausing QE tapering from FY2027. The Bank is currently reducing monthly JGB purchases by JPY 200 billion per quarter. Updated guidance is likely to signal that further tightening will be warranted if the economy evolves in line with expectations. We therefore expect another rate hike later this year.

The Fed’s upcoming policy meeting is likely to attract even more attention than usual, as it will be the first under the leadership of new Chair Kevin Warsh. Market participants will be listening closely for signals on how he intends to respond to the energy price shock. It is widely assumed that he will favour looking through the near-term increase in inflation and keeping rates on hold. However, hawkish voices on the FOMC are becoming more prominent. Following three strong NFP reports, the Fed is expected to drop its easing bias at the upcoming meeting. Updated economic projections are also likely to show reduced support for further rate cuts.

The BoE has recently signaled that it is not in a rush to begin raising rates and is expected to leave policy unchanged in the week ahead. The latest UK CPI and employment reports will be released ahead of next week’s MPC meeting. MPC member Megan Greene has indicated that she could join Chief Economist Huw Pill in voting for a rate hike. The Makerfield by-election will determine whether Andy Burnham becomes an MP and can then formally challenge Prime Minister Keir Starmer.