Yield differentials reinforcing the US dollar’s upward momentum

EUR/USD: Diverging ECB-Fed policy expectations trigger break out of range

The US dollar’s upward momentum has continued at the start of this week resulting in EUR/USD falling to a low of 1.1361 overnight. The pair has now broken out of the 1.1400 to 1.1800 trading range that had been in place over the past year providing a bearish technical signal. The move lower in EUR/USD has been driven by the recent divergence in market expectations for ECB and Fed policies. While the US rate market has moved to price in multiple Fed rate hikes, the euro-zone rate market has become less confident over the need for further ECB rate hikes. The paring of ECB rate hike expectations was encouraged further yesterday by the releases of mixed PMI surveys from Europe for June. The composite PMI surveys for the euro-zone revealed a pick-up business confidence supported by the lower energy prices, although at 49.5 was still still consistent economic stagnation in Q2. It adds to evidence showing that the euro-zone economy has slowed in response to the energy price shock. The unexpected drop in the German services PMI by 1.3 points to 46.8 in June added to growth concerns in the region. The good news is that the energy price shock appears likely to be smaller than initially feared given the price of oil has almost returned to pre-conflict levels sooner than expected. In contrast, the US economy appears to have been less negatively impacted by the energy price shock. The US composite PMI picked up to 52.2 in June.

The combination of weaker growth in the euro-zone and lower energy prices is helping to ease pressure on the ECB to hike rates further. President Lagarde stated at the start of this week that “we see no evidence yet of de-anchoring of inflation expectations or second-round effects that warrant a more forceful policy response at this stage”. She added that the ECB “can adjust our policy response as the shock evolves and ensure it remains proportionate”. The comments suggest that the ECB will stick to their current path for a measured policy response. We are still sticking to our forecast for one final ECB hike in September, although acknowledge that balance of risks has shifted recently in favour of less rather more hikes.

Recent comments from ECB Chief Philip Lane have indicated that they want to keep the door open for at least one final hike. He warned yesterday that a “range of forward-looking signals point to inflationary pressures in the coming months” and that “in this environment, our focus remains clear: to ensure that inflation stabilizes at our 2% target in the medium-term”. He added that even in the ECB’s milder scenario for developments in the Middle East, inflation was set to remain above target “for long enough to warrant a measured response”. He is wary that that there is “some momentum in wages”. The relatively hawkish comments quickly follows his comments from last week that the ECB’s estimate of the upper end of the neutral policy range was risen by 25bps up to 2.50%. It indicated that the ECB can hike rates one more time without moving policy into restrictive territory. The divergence in monetary policy expectations between the ECB and Fed is likely to continue to encourage a lower EUR/USD in the near-term, although we doubt it will be sustained if the Fed does not follow through with rate hikes this year.

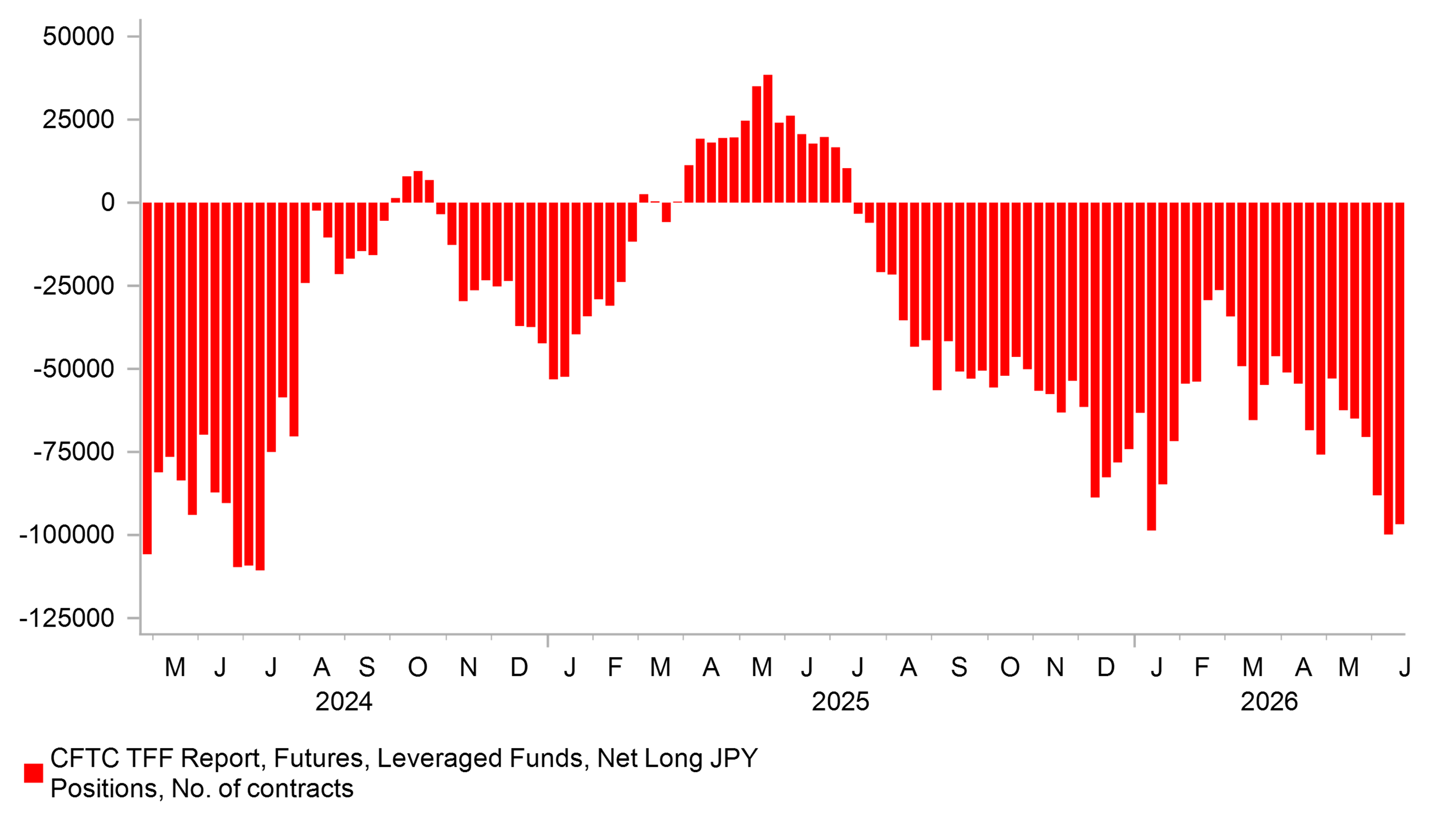

SPECULATIVE JPY SHORTS REMAIN ELEVATED

Source: Bloomberg, Macrobond & MUFG Research

JPY: BoJ minutes suggest potential for faster rate hikes

The yen continued to trade close to recent lows against the US dollar with USD/JPY still holding below the July 2024 high of 161.95. The heightened threat of intervention is helping to slow the pace of yen weakness after it was reported that Finance Minister Katayama held a call with Us Treasury Secretary Scott Bessent earlier this week (click here). After the call, Finance Minister Katayama told reporters that the two had agreed to take “bold steps” on currencies if needed, and said the two nations are increasingly “aligned” on foreign exchange rate policy. It has encouraged speculation that the US could even join Japan in undertaking joint intervention which would be more effective at pushing down USD/JPY. It has been some time since the US took part in join intervention in March 2011 after the tsunami hit Japan.

Pressure on Japan to intervene again to support yen has increased after the BoJ’s latest rate hike failed to disrupt the weakening trend. The release of the minutes overnight from the June policy meeting indicated support for further rate hikes. the BoJ has become less concerns over downside risks to growth while many members expressed awareness of upside risks to prices. The minutes suggested that one or two members may propose voting for another hike as soon as September or October. One member noted it is desirable ”to consider whether to raise the policy interest rate as appropriate with intervals of a few months in mind”. The Japanese rate market is now pricing in around 16bps of hikes by October. However, market expectations for the BoJ to speed up rate hikes have not yet triggered a stronger yen.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

GE | 09:00 | IFO Business Climate | Jun | 85.5 | 84.9 | !! |

US | 13:30 | Current Account Balance | 1Q | -$208.9b | -$190.7b | !! |

CA | 18:30 | Bank of Canada Summary of Deliberations | !! | |||

US | 19:00 | Fed's Cook Gives Pre-Recorded Opening Remarks | !! |

Source: Bloomberg & Investing.com