Intervention threat stepped up as USD/JPY moves close to July 2024 high

JPY: Speculation picks-up over possibility of joint US-Japan intervention

The major foreign exchange rates have remained relatively stable overnight with the US dollar continuing to trade close to year-to-date highs. The stronger US dollar has been encouraged by the hawkish repricing of Fed rate hike expectations, and the scaling back of US policy risk premium following last week’s FOMC meeting. Kevin Warsh’s first FOMC meeting as Chair has helped to further dampen concerns over the threat to the Fed’s independence when setting monetary policy. The adjustment higher in US yields is creating a more challenging backdrop for risk assets in the near-term after strong gains in recent months. The biggest pullback was evident overnight in the South Korean equity market which fell by over 8.0% and triggered trading to halt for 20 minutes. According to Bloomberg, foreign investors sold more than USD2.6 billion of Kospi-shares by mid-day. The sell-off was led by AI/tech stocks such as SK Hynix and Samsung Electronics. It comes before memory chipmaker Micron Technology’s quarterly earnings results are released later this week. So far there has been limited spillover in the foreign exchange market. USD/KRW remains broadly flat on the day.

The South Korean won continues to trade at weak levels similar to the yen. Yesterday USD/JPY moved to within touching distance of the high from July 2024 at 161.95 but failed to break above. It is viewed as important level among market participants encouraging renewed speculation that Japan could intervene again soon to support the yen. At the same time, intervention speculation has been encouraged by media reports that a phone call was held yesterday between Japanese Finance Minister Satsuki Katayama and US Treasury Secretary Scott Bessent. After the call, Finance Minister Katayama told reporters that the two had agreed to take “bold steps” on currencies if needed, and said the two nations are increasingly “aligned” on foreign exchange rate policy. The phone call was described as a follow-up to last week’s G7 meeting. The comments will encourage expectations that the Japan and the US could intervene together to lower USD/JPY which would likely prove more effective than the recent unilateral action undertaken by Japan in late April and early May. However, any attempt from the US to weaken the US dollar would be somewhat inconsistent the recent move higher in US yields driven by the Fed’s policy update casting doubt on whether joint intervention will take place at the current juncture. If it does take place it would send a powerful signal that the Trump administration is not happy with an even stronger US dollar helping to limit scope for further near-term gains.

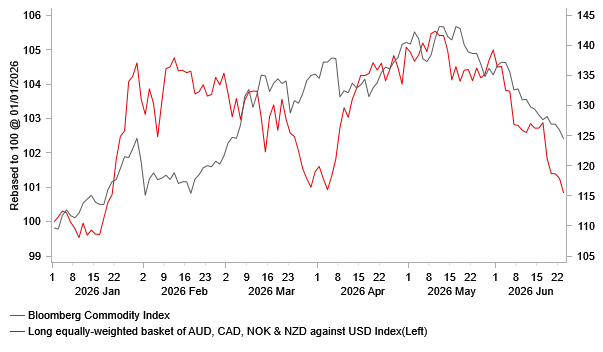

At the same time, the recent correction lower for commodity prices has continued overnight which has contributed to the underperformance of commodity related currencies over the past month. Bloomberg’s commodity price index has now fallen by almost 13% from last month’s peak leaving it only around 3-4% higher than pre-Middle East conflict levels from late February. Higher US real rates driven both by the hawkish repricing of Fed rate hike expectations and lower market-based measures of inflation expectations are creating a more challenging backdrop for commodities such as gold, alongside the US-Iran deal which is helping to ease supply concerns in the energy market. The price of oil has continued to fall further bellow USD80/barrel after the US issued a 60-day licence yesterday allowing Iran to sell oil on the international market in response to the first round of negotiations between the US and Iran over the weekend that were described as “very, very good” by US Vice President JD Vance. The developments are supportive for our long/USD/NOK trade idea recommended in the latest FX Weekly report (click here).

G10 COMMODITY CURRENCIES CONTINUE TO UNDERPERFORM

Source: Bloomberg, Macrobond & MUFG Research

GBP: Fiscal policy changes in focus after Prime Minister Keir Starmer resigns

The pound has strengthened modestly over the last 24 hours after it was confirmed yesterday that UK Prime Minister Keir Starmer has resigned after losing the support of Labour MPs. He set the stage for leadership contest to take pace to choose the next leader of the Labour party, although it appears more likely that Andy Burnham will become the next leader in the absence of other challengers. Health Secretary Wes Streeting who had previously planned a leadership challenge decided to stand aside yesterday issuing support for Andy Burham to be the next leader. He stated that the time had come to “roll up our sleeves and help him deliver the change our party and our country needs”. It followed talks between Wes Streeting and Andy Burnham in recent days. It has encouraged speculation that Wes Streeting will be given an important role in Andy Burnham’s new cabinet potentially as the new Chancellor. Market participants would look favourably upon the appointment of Wes Streeting as the next Chancellor given he is from the centre-left of the Labour party which could help to reduce the risk of a bigger lurch to the left in fiscal policies. The initially positive reaction from gilts and the pound yesterday are consistent with that view. If no alternative leadership candidate emerges in the coming weeks, then Andy Burnham could be confirmed as Prime Minister as early as 17th July. Various media reports have stated that Andy Burnham is expected to give a speech on fiscal policy next week although the exact timing and details haven’t formally been confirmed yet. It will be a key event risk for gilts and the pound.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

DE | 08:30 | German Manufacturing PMI | (Jun) | 50.3 | 50.1 | !! |

DE | 08:30 | German Services PMI | (Jun) | 49.0 | 48.1 | !! |

EU | 09:00 | Services PMI | (Jun) | 48.6 | 47.7 | !! |

EU | 09:00 | Manufacturing PMI | (Jun) | 51.6 | 51.6 | !! |

GB | 09:30 | Services PMI | (Jun) | 50.1 | 49.3 | !!! |

GB | 09:30 | Manufacturing PMI | (Jun) | 53.5 | 53.9 | !!! |

EU | 09:30 | ECB's Lane Speaks | - | - | - | !! |

DE | 09:35 | German Buba Mauderer Speaks | - | - | - | !! |

GB | 09:55 | BoE Breeden Speaks | - | - | - | ! |

CA | 14:00 | BoC Gov Macklem Speaks | - | - | - | !! |

US | 14:45 | Services PMI | (Jun) | 51.1 | 50.7 | !!! |

US | 14:45 | Manufacturing PMI | (Jun) | 54.6 | 55.1 | !!! |

GB | 18:30 | BoE MPC Member Dhingra Speaks | - | - | - | ! |

Source: Bloomberg & Investing.com