Relative yield moves can see US dollar gains extended

USD: Crude oil stays lower; ex-US data turns weaker

Crude oil prices are lower by about 4% from the start of the week with US Secretary of State Marco Rubio yesterday confirming that “we’ve made some good progress”. Pakistan negotiators have travelled to Iran and Rubio believes there are “good signs” – so in all likelihood the financial markets will once again go into the weekend (a long one with bank holidays in the UK and the US) with hope that a deal can soon be reached. But the US dollar remains close to recent highs underlining the limited FX reaction to the rising optimism. The appetite for buying non-dollar currencies has been somewhat muted by more compelling evidence of the negative economic impact from the rise in energy prices since the conflict began. The reasoning for rate hikes outside of the US has weakened on the back of weaker inflation prints as well.

The Canadian dollar is the worst G10 performing currency this week, followed by the yen and the Australian dollar. Yesterday, front-end yields in Australia fell by close to 10bps on weaker than expected employment data – the OIS market shows pricing for the next RBA hike has been pushed back to November. Front-end yields are also lower in Canada following a weaker than expected CPI print for April. That data on Tuesday was followed by a weaker CPI print in the UK that triggered a notable rally in the Gilt market. The weak inflation theme continued today in Japan with the nationwide CPI data weaker than expected. The core-core CPI YoY rate fell from 2.4% to 1.9% in April, the weakest YoY rate since September 2023. It was the biggest drop in one month since April 2021 and will raise doubts over the necessity of the BoJ raising rates in June. Yields are only modestly softer in Japan, and we do not expect this print to alter the prospects of a BoJ rate hike. Much of the drop is base-effect related and given the level of the policy rate balanced against the risk from energy prices and the instability in the JGB market we see the case for hiking as still very compelling.

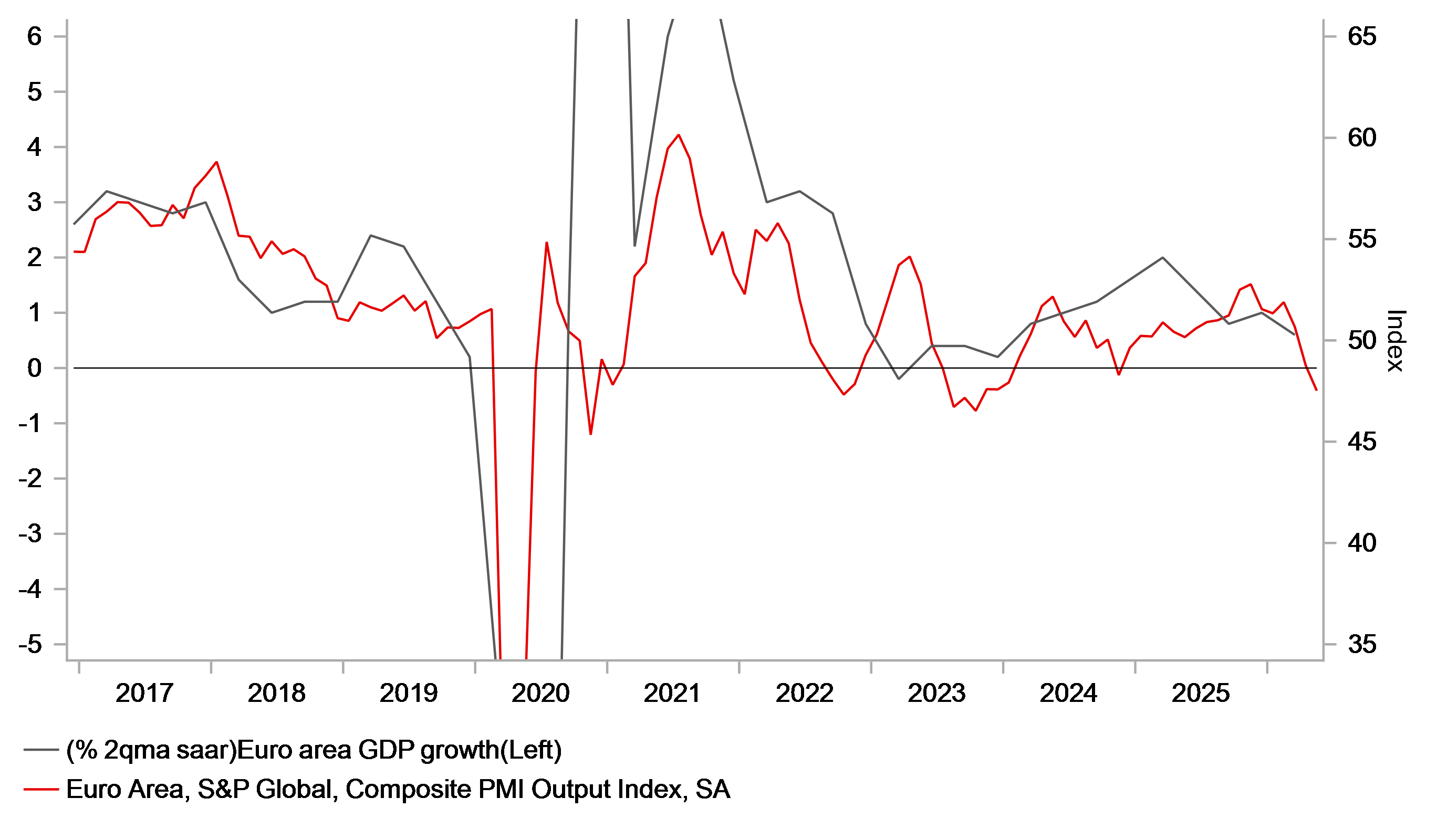

The evidence of slowdown in Europe has certainly built this week although we would argue that this will not have been a surprise for ECB officials. The Composite PMI has now fallen from 51.9 to 47.5 since the Middle East conflict began. The focus of the ECB will be in maintaining credibility and ensuring long-term inflation expectations remain anchored and moderating growth is unlikely to deter some near-term modest tightening of monetary policy. A sudden and credible end to the conflict that sees crude oil drop sharply could push the timing of a hike out but would unlikely be enough to cancel the need for a hike.

The flow of UK data has certainly been more consistently weaker this week although the weaker inflation that sparked a big Gilt market rally prompted pound strength. The pound is the second best performing G10 currency this week. A weak jobs report on Tuesday, followed by the weaker CPI print and then today a weaker retail sales report have resulted in close to a full 25bp hike being removed from OIS pricing. But close to two hikes remain priced which we see a still plausible. The CPI print was weaker but as we highlighted this week (here), the PPI data was a lot stronger than expected with hefty pipeline inflation still to come through. Still, while we expect rate hikes from the BoJ, ECB and BoE, the rise of US front-end yields relative to the rest of the world can run further and reinforce near-term positive US dollar momentum. Only a peace deal in the Middle East is likely to alter that momentum.

EURO-ZONE COMPOSITE SIGNALLING GDP SLOWDOWN

Source: Bloomberg, Macrobond & MUFG Research

MXN: Downside risks building

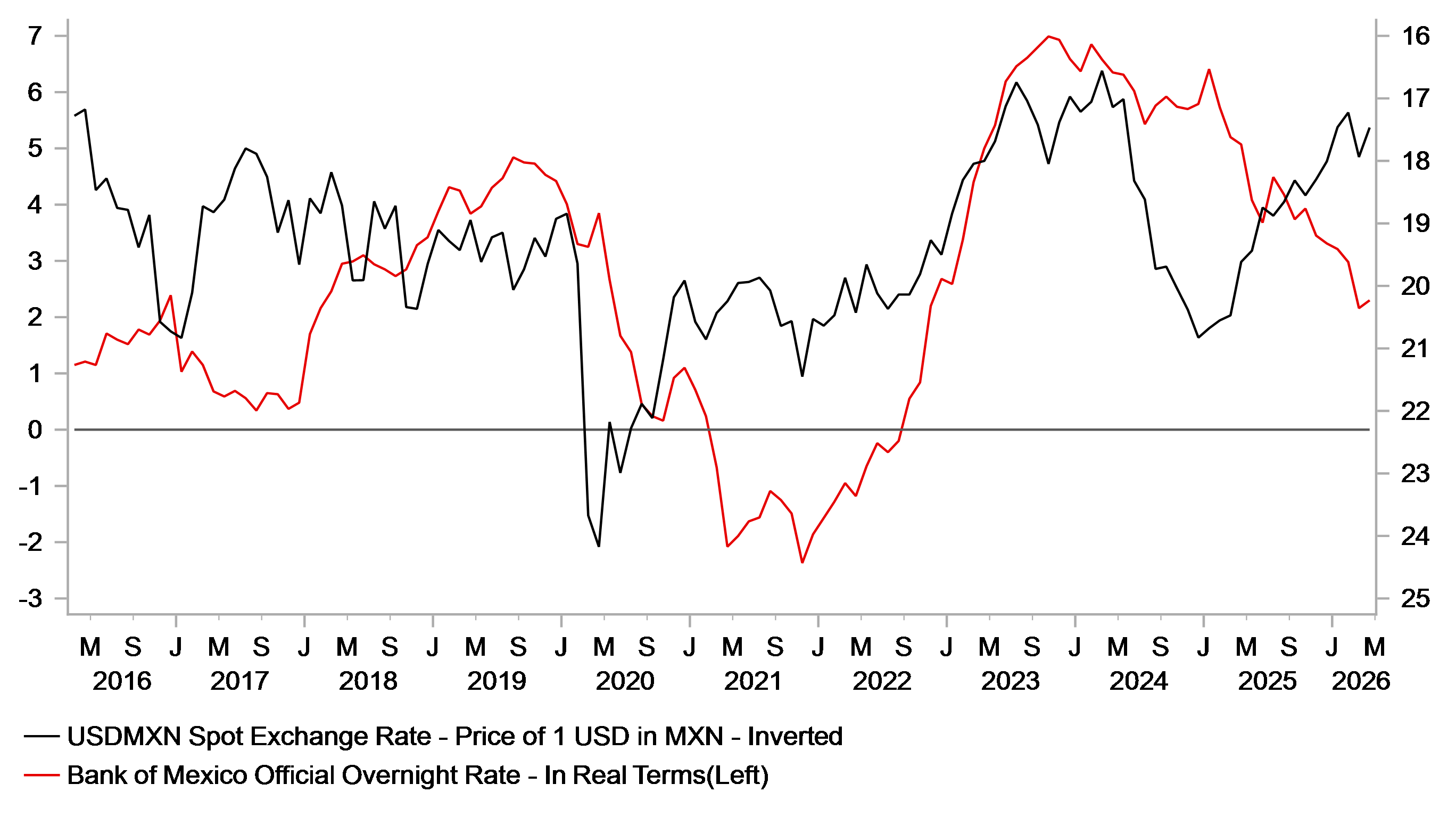

Mexico stands out to us this week in terms of newsflow highlighting building risks that the period of peso appreciation may struggle from here with greater macro challenges ahead. Firstly, Moody’s cut Mexico’s credit rating on Wednesday to Baa3 from Baa2, leaving the rating just one notch above junk. The outlook was raised from negative to stable with Moody’s citing “a sustained weakening in fiscal strength that accelerated in 2024 and that we expect to persist”. The Moody’s action followed the decision of S&P to lower its credit ratings outlook from stable to negative. Moody’s described the fiscal position as problematic in part due to Mexico’s “low growth environment”. An S&P downgrade would match Moody’s and Fitch’s current level. Secondly, Banxico yesterday released the minutes of the meeting on 7th May when the key policy rate was cut by 25bps to 6.50%. The minutes revealed increased concerns over economic conditions with the 0.8% Q/Q contraction in Q1 “notably weaker than anticipated”. “Most members” provided negative views on the economy with “some” members now expecting a “more moderate” recovery than previously expected. GDP growth did pick up at the start of Q2 with a 0.3% m/m gain in April. That pick up and still elevated inflation (4.45% YoY) led to other comments that indicated doubts over whether the current policy rate would help to achieve a return to the 3.0% inflation target, leaving Banxico’s hands tied from here.

This backdrop certainly leaves the peso more vulnerable to downside risks. An important source of risk appetite has been the strong US corporate earnings related to AI and that will help support risk conditions and low volatility. However, a re-escalation in the conflict in the Middle East would certainly hit the peso, and possibly now by more than other EM currencies. Carry has continued to provide demand for the peso from Leveraged Funds according to IMM data although there has been a notable reduction in long peso positions amongst the Asset Managers & Institutional Investors sector. The Leveraged Funds’ positioning in the last few weeks has been the highest since mid-January suggesting scope for peso underperformance if downside risks continue to build. Our current FX forecasts already highlight our own doubts over the sustainability of the peso appreciation trend with scope over the coming months for a rebound in USD/MXN toward the 18.000-level. Our USD/MXN forecasts out to Q1 2027 are all higher than current spot.

PESO SUPORT FROM BANXICO POLICY RATE IN REAL TERMS POINTS TO INCREASED DOWNSIDE RISKS

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

GE | 09:00 | German Ifo Business Climate Index | (May) | 84.2 | 84.4 | !! |

EZ | 09:30 | ECB President Lagarde Speaks | - | - | - | !!! |

EZ | 10:00 | Negotiated Wage Growth YoY | Q1 | 2.50% | 2.95% | !! |

CA | 13:30 | Retail Sales (MoM) | (Mar) | 0.6% | 0.7% | !! |

CA | 13:30 | Core Retail Sales (MoM) | (Mar) | 0.9% | 0.5% | !! |

CA | 13:30 | RMPI (MoM) | (Apr) | 2.7% | 12.0% | !! |

CA | 13:30 | RMPI (YoY) | (Apr) | - | 23.6% | ! |

CA | 13:30 | IPPI (MoM) | (Apr) | 1.2% | 2.4% | ! |

CA | 13:30 | IPPI (YoY) | (Apr) | - | 7.8% | ! |

US | 15:00 | US Leading Index (MoM) | (Apr) | -0.1% | -0.6% | ! |

US | 15:00 | Michigan 1-Year Inflation Expectations | (May) | 4.5% | 4.7% | !!! |

US | 15:00 | Michigan 5-Year Inflation Expectations | (May) | 3.4% | 3.4% | !!! |

US | 15:00 | Michigan Consumer Sentiment | (May) | 48.2 | 49.8 | !! |

US | 15:00 | Fed Waller Speaks | - | - | - | !!!! |

CA | 15:30 | BoC Senior Loan Officer Survey | (Q1) | - | 2.8 | ! |

Source: Bloomberg & Investing.com