USD continues to trade on a stronger footing

USD: Higher US yields continue to drive USD performance amid US-Iran talks

The US dollar has continued to trade at stronger levels overnight after breaking higher least week triggered by the hawkish repricing of Fed rate hike expectations. The dollar index briefly rose back above the 101.00-level on Friday for the first since May of last year. At the same time, the 2-year US Treasury yield has risen back above 4.20% for the first time since February of last year prior to President Tump’s “Liberation Day” tariffs announcement in April 2025. The latest price action highlights that the negative shock for the US yields and the US dollar from last year’s tariff hikes is reversing supported by building evidence that the US economy is continuing to grow solidly and downside risks for the labour market have eased. The recent run of positive US economic data surprises and hawkish Fed policy communication has encouraged market participants to price in almost a 50:50 probability of a rate hike as soon next month. With the US mid-term election taking place later this year in November, it could be easier for the Fed to hike rates sooner rather than later. In addition, if they hold off from hiking rates soon then slowing inflation from lower energy prices and the fading impact of tariff hikes should dampen the need for hikes later this year as well.

The hawkish repricing of Fed rate hike expectations has happened even as the price of oil has continued to decline over the past week in response to the US-Iran deal. Developments over the weekend have highlighted that the deal remains fragile with Iran threatening to close the Strait of Hormuz again if Israel continues to strike Lebanon. On the other hand, it has been reported that the US and Iran made “encouraging progress” in talks on a peace deal and will continue technical-level discussions this week according to mediators Qatar and Pakistan. The joint statement from Qatar and Pakistan stated that the parties agreed on a roadmap toward reaching a final deal in 60-days, established a communication line to avoid incidents and miscalculations, and creating a “de-confliction cell” involving parties and Lebanon to help ensure adherence to the cessation of military operations there. According to an official familiar with the discussions, a resolution to the fighting in Lebanon will be decisive for the success of the US-Iran talks in Switzerland. The price of Brent crude oil has fallen back towards support from the 200-day moving average which comes at around USD78.70/ barrel. The Norwegian krone has been the worst performing G10 currency since the US-Ian deal was announced. We see scope for a further krone weakness and recommended a new long USD/NOK trade idea in our latest FX Weekly report released on Friday (click here).

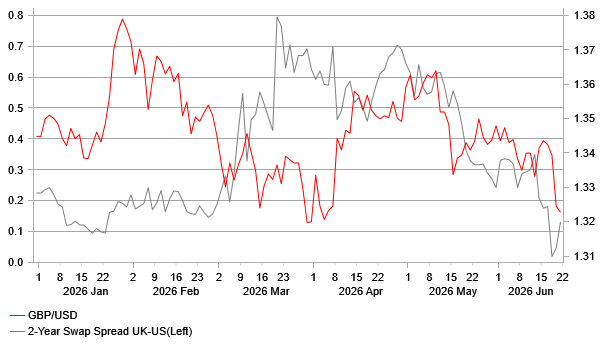

CABLE IS TESTING RECENT LOWS AROUND 1.3200

Source: Bloomberg, Macrobond & MUFG Research

GBP: Limited negative spillovers for GBP & gilts from UK political uncertainty

The pound has underperformed over the past week, with cable falling back below support at the 1.3200 level and EUR/GBP rising towards the 0.8700-level. This follows a recent failure to break below the bottom of the current narrow trading range between 0.8600 and 0.8800. The US–Iran deal has initially contributed to a weaker pound by lowering energy prices and UK yields. After failing to hold above resistance at 4.60%, the two-year gilt yield has declined towards support at 4.20%, reflecting a scaling back of BoE rate hike expectations. UK rate market participants are now less confident that the BoE will deliver multiple rate hikes and have pushed back the expected timing of a hike to later this year, likely in September or November. Alongside lower energy prices, evidence of softer inflation in May and a still-weak labour market are allowing the BoE more time to assess the impact of the energy price shock on the UK economy.

At last week’s MPC meeting, the BoE indicated that it now expects inflation to rise less this year to just above 3.25% in Q4. This is even lower than the BoE’s best-case scenario (Scenario A) outlined in April, when inflation was projected to reach 3.6% in Q4. Under Scenario A, the energy price shock was expected to be short-lived, with weak demand helping to offset inflationary pressures and there are no meaningful second-round effects. It would allow the BoE to continue to judge that the tightening in financial conditions, driven by higher market rates since the onset of the Middle East conflict, provides sufficient monetary restraint without the need for additional rate hikes. Reduced concern over upside risks to inflation was also evident among the majority of MPC members, who voted to keep rates on hold last week. The higher bar for further tightening has led us to revise our outlook: we have dropped our forecast for two rate hikes this year and now expect the BoE to leave rates on hold, unless second-round effects such as stronger wage growth begin to emerge.

This leaves room for UK yields to continue adjusting lower, putting further downward pressure on pound performance particularly against the US dollar, as US yields are currently moving higher to price in additional Fed rate hikes. At the same time, recent communication from ECB policymakers continues to signal readiness to deliver at least one more rate hike. Chief Economist Philip Lane made a timely intervention this week, noting that their estimate of the neutral policy rate has “crept up from 2.25% to 2.50%.” It highlights that the ECB believes it has scope to deliver one further hike without pushing policy into restrictive territory for the eurozone economy. This supports our decision to maintain our forecast for a final hike to 2.50% in September, despite the backdrop of lower energy prices. Recent developments have contributed to yield spreads moving against pound, reinforcing our view that EUR/GBP will rise towards the upper end of its current trading range between 0.8600 and 0.8800. Furthermore, the Fed’s shift away from forward guidance has injected more volatility into financial markets, making the risk-reward profile for FX carry trades relative less attractive although volatility is still low. The pound may also receive less support from carry-related demand if volatility picks up further.

Heightened political uncertainty in the UK could provide an additional near-term headwind for pound, although we expect any initial negative impact from political change to be modest. Andy Burnham’s by-election victory in Makerfield at the end of last week is likely to pave the way for him to be installed soon as the next leader of the Labour Party and Prime Minister. It now appears to be only a matter of time before Keir Starmer is replaced. Media reports over the weekend are suggesting that Keir Starmer could set out a timetable for his departure as soon as today. He has reportedly been reflecting on “political realities” that he no longer commands the support of the majority of Labour MPs. If he steps down, it would be up to Labour MPs to decide if Andy Burnham should win power by coronation or face a leadership contest. Either outcome is expected to lead to Andy Burham becoming the next Prime Minister.

In the recent past, the prospect of Andy Burnham becoming Prime Minister would have triggered a more pronounced sell-off in gilts and the pound. The relatively muted market reaction to the Makerfield by-election result suggests that market participants have become more comfortable with the potential policy changes under his leadership. Recent rhetoric appears designed to help stabilise the gilt market. Burnham has pledged to adhere to the government’s fiscal rules, limiting the scope for significant fiscal loosening. At the same time, it has been reported that he is expanding his team of economic advisers to strengthen the credibility of his policy platform. He has reportedly sought advice from former BoE Chief Economist Andy Haldane, former OBR Chair Richard Hughes, and former Goldman Sachs Chief Economist Jim O’Neill who are highly regarded by financial market participants. This helps to further ease concerns about the risk of a more disruptive shift to the left in policymaking. On the other hand, if Burnham proves overly cautious and avoids implementing more substantial policy changes, he may struggle to reverse the Labour Party’s declining public support. It leaves market participants waiting eagerly to see how fiscal policy evolves in the UK, with the Autumn Budget likely to be even more significant than usual.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 11:00 | ECB President Lagarde Speaks | - | - | - | !! |

DE | 12:00 | German Buba President Nagel Speaks | - | - | - | !! |

CA | 13:30 | Core CPI (YoY) | (May) | - | 2.1% | !! |

US | 14:00 | Fed Waller Speaks | - | - | - | !! |

EU | 15:10 | ECB's Lane Speaks | - | - | - | !! |

EU | 16:15 | ECB President Lagarde Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com