JPY downside risks building following G7 meeting

JPY: Rising US yields to force more intervention

Since the start of last week, the 10-year UST bond yield has jumped 30bps as investors reassess inflation risks and the potential scale of Fed response. Over that period the implied probability of a 25bp rate hike by year-end has gone from zero to around 80%. The US dollar is responding and the DXY index is 1.5% stronger – the biggest move since the initial period following the start of the US-Iran conflict. There is scope for yields to move further higher. While we maintain that the Fed will ultimately hike by less than many other G10 central banks, market pricing remains relatively low at this juncture – especially with the risks of a further jump in crude oil prices building.

The probable intervention in Japan that took place on 30th April and 6th May was always about buying time and hoping that external factors would turn in favour of a stronger yen. In previous interventions that happened – in 2022 and July 2024 US yields fell notably in the weeks following intervention and USD/JPY fell sharply. In April/May 2024 that didn’t happen and yields remained stable at elevated levels and intervention failed. This time, the external backdrop is even more challenging – US yields are rising sharply and in these circumstances the need for additional intervention is increasing by the day. Finance Minister Katayama reiterated at the G7 that Japan had the support for further action if required given the agreement and the G7 communique that repeated that excess currency volatility can have adverse economic impacts. US Treasury Secretary also stated that “FX volatility was undesirable”.

But it is also likely that the US believe the real issue is the monetary stance in Japan and Scott Bessent has been vocal in the past, criticising the excessively loose monetary stance, blaming it on the weakness of the yen. Bessent met with BoJ Governor Ueda at the G7 gathering in Paris and expressed confidence that Governor Ueda would “successfully” guide monetary policy. The BoJ is likely coming under increased US pressure to hike rates, and we suspect Ueda’s tone is set to turn hawkish ahead of the next BoJ meeting on 16th June. Yesterday he stated that “the pace of businesses passing on their costs is somewhat fast”. More comments like that and expectations of a June hike will increase further.

But the pricing for a hike is already showing an 80% probability, so it’s unlikely that a more hawkish BoJ at this stage will be enough to lift the yen. Signals of more hiking to do beyond June would help but that seems unlikely and hence developments in the Middle East, energy markets and US yields will remain key. Additional intervention looks like it may be needed even with the BoJ turning more hawkish.

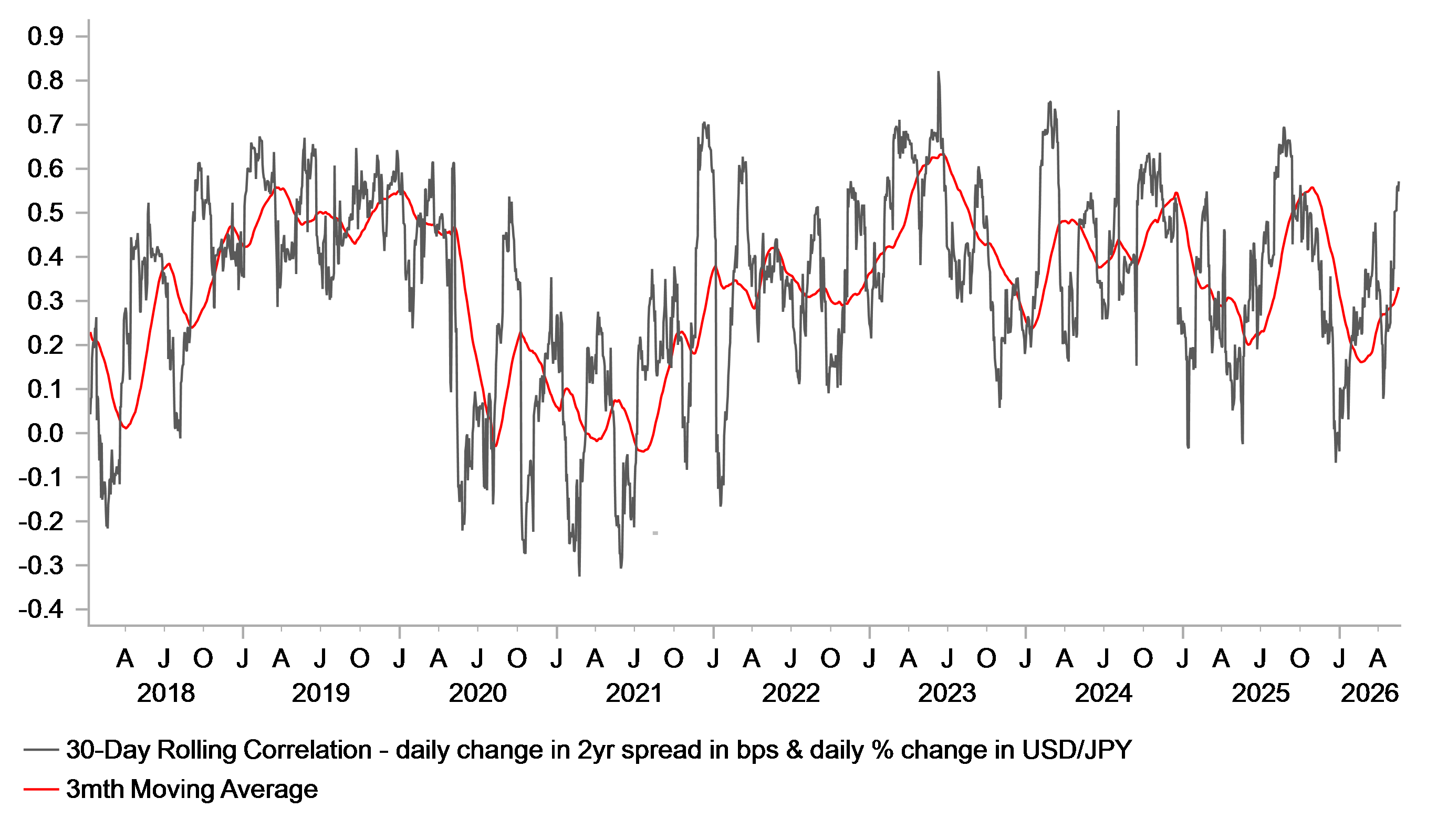

USD/JPY & 2Y US-JAPAN SPREAD CORRELATION IS STRENGTHENING AGAIN

Source: Bloomberg, Macrobond & MUFG Research

USD: FOMC minutes to reinforce yield momentum

In the week in which Kevin Warsh will be sworn in as Fed Chair (Friday) it’s not that surprising that President Trump has stated that “I’m going to let him do what he wants to do” although the real test will be in the weeks and months ahead and understandably we have a degree of scepticism in that being Trump’s approach if it turns out that Warsh is more hawkish than expected. As we highlighted in the FX Weekly (here), released on Monday, the risk is that Warsh does not start his tenure as President Trump probably hopes. With inflation concerns fuelling bond market selling, a dovish approach to monetary policy could well be counterproductive.

Incoming Fed Chair Warsh will also not want to open a chasm within the FOMC at an early stage either. Steve Miran, the uber-dove is gone, and other members are likely shifting to focusing more on inflation risks. The minutes from the FOMC meeting on 29th April will be released this evening and in all likelihood will confirm the more hawkish shift evident on the day of the meeting. The 2-year UST bond yield jumped 11bps in response to the FOMC statement and the press conference from Fed Chair Powell. With three FOMC members having dissented against the wording of the statement that suggested scope for additional rate cuts, the tone of the minutes are likely to more on the hawkish side. All three members (Kashkari, Logan and Hammack) have spoken since the April meeting and made clear that a neutral bias was more appropriate given a hike could be required if inflation risks continue to rise. The April inflation data will not have eased those risks.

There are other key Fed events this week in addition to the FOMC minutes tonight with a speech on the economy by Richmond Fed President Barkin tomorrow (17:20 BST) and crucially a speech by Governor Waller on the economy on Friday (15:00 BST). Barkin is a non-voter but Waller’s comments on inflation risks will be key given he previously held a more dovish view before turning more balanced since the conflict began. A further shift on Friday would be telling.

Does a sudden lurch lower in energy prices that eases the upward pressure on yields look likely? Only an imminent and credible peace deal being announced would do that and there is no clear evidence of that taking place. If the status quo continues, yields look set to continue rising. That is likely to continue helping strengthen the dollar. As we highlighted in the FX Weekly, the US dollar / rate spread correlation looks to be strengthening and with only a little move one rate hike priced in the US there is scope for that to increase further.

The 10-year US-EZ spread is breaking higher as pricing on Fed rate hikes increases and looks set to break back above 150bps for the first time since November last year when EUR/USD was trading around the 1.1500-level. There is certainly near-term scope for the dollar to extend further stronger especially if incoming Fed Chair Warsh was the convey a more hawkish stance over the coming weeks to more closely align himself with the apparent shift from a growing number of FOMC members.

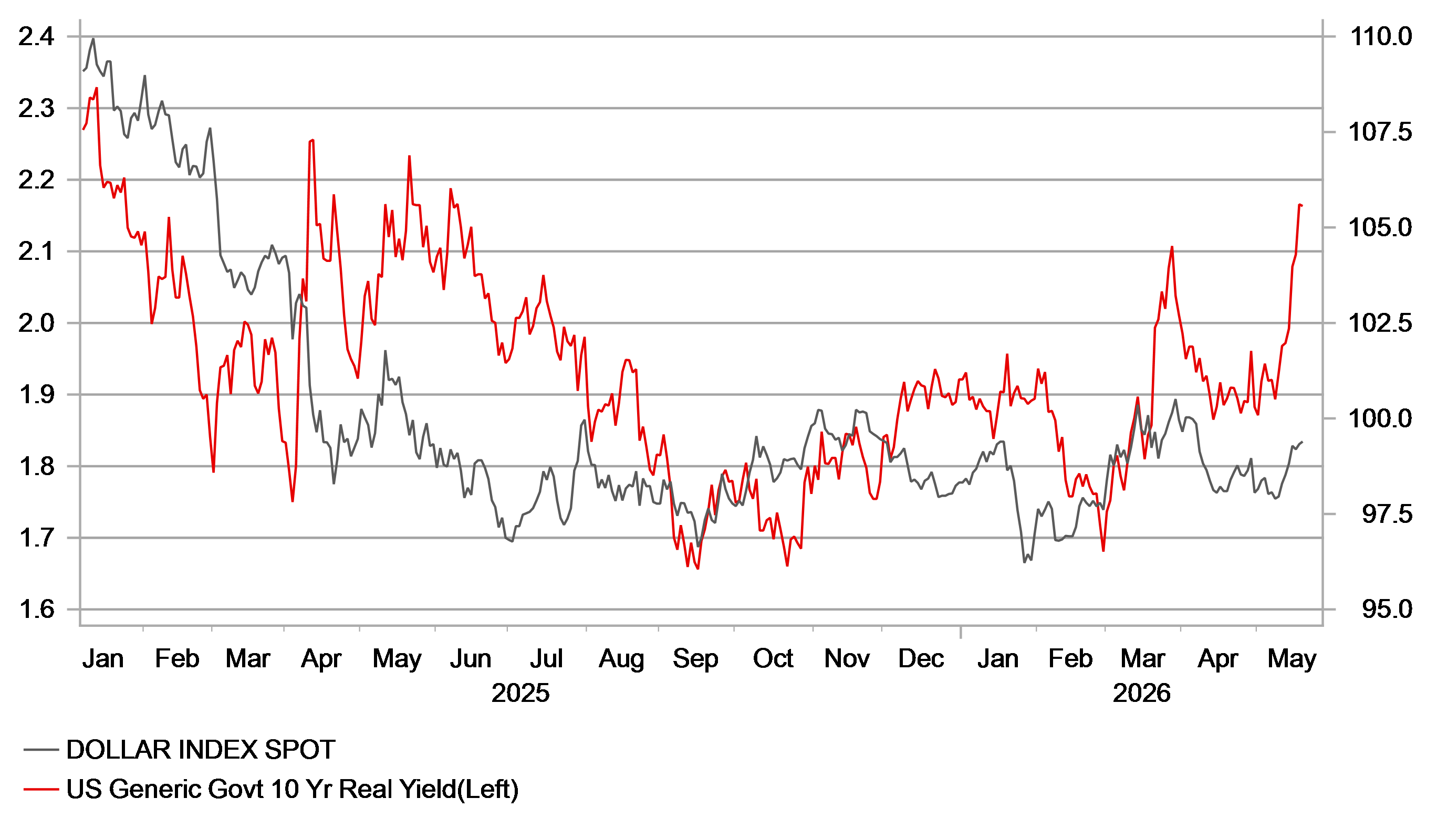

US 10-YEAR REAL YIELD BACK TO JAN 2025 LEVELS WILL FUEL FURTHER USD STRENGTH

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EZ | 10:00 | CPI (YoY) | (Apr) | 3.0% | 2.6% | !!! |

EZ | 10:00 | Core CPI (YoY) | (Apr) | 2.2% | 2.3% | !!! |

EZ | 10:00 | CPI (MoM) | (Apr) | 1.0% | 1.3% | !! |

EZ | 10:00 | Core CPI (MoM) | (Apr) | 0.9% | 0.8% | !! |

EZ | 10:00 | HICP ex Energy & Food (YoY) | (Apr) | 2.1% | 2.1% | !! |

EZ | 10:00 | HICP ex Energy and Food (MoM) | (Apr) | 0.8% | 0.7% | !! |

UK | 14:15 | BoE Gov Bailey Speaks | - | - | - | !!! |

UK | 14:15 | BoE MPC Member Mann | - | - | - | !! |

UK | 14:15 | BoE MPC Member Dhingra Speaks | - | - | - | !! |

US | 19:00 | FOMC Meeting Minutes | - | - | - | !!! |

Source: Bloomberg & Investing.com