US dollar’s key pillar of support is weakened

USD: Pressure eases notably on the Fed to hike

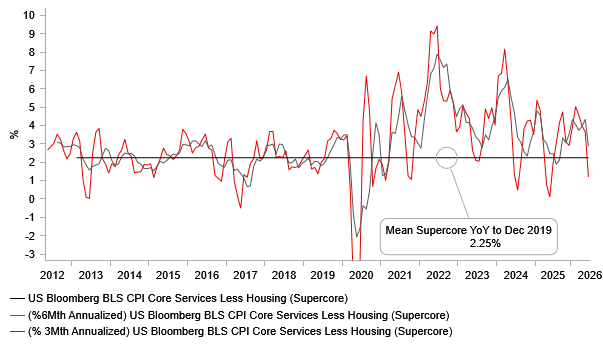

Following Fed Governor Waller’s comment on Monday that a strong core CPI print would compel the Fed to hike in the near-term, the CPI report released yesterday had become even more important for the financial markets. The fact that the CPI print was much weaker than expected has removed in an instant a key near-term driver of US dollar strength. We never agreed with the pricing of a possible July rate hike (or indeed through the rest of the year) and the CPI print has helped remove that nearly fully from close to a 50% probability to closer to 15% now. We wrote here last week (here) why we thought the CPI report could be weaker than expected and the three factors mentioned were evident in the weakness of the report. Tariff unwind in certain import-sensitive categories, weakening rents and energy disinflation were all elements explaining the weak CPI. Furnishings and apparel saw notable declines in annual rates. Slowing rents and energy disinflation helped as well.

The drop for the US dollar so far has been modest. Given the scale in which yields in the US had jumped and long US dollar positions had been built up over a relatively short period of time, we would have thought there was scope for a greater decline for the dollar. The testimony from Fed Chair Warsh looks to have curtailed the move weaker for the dollar. Just like following his first FOMC meeting, Warsh spoke with conviction in relation to the Fed achieving its 2% inflation goal. The CPI print was not “mission accomplished” and he wasn’t going to “cherry pick” data. He added that he was “doubling down” on the Fed’s inflation goal. We don’t really view this as “hawkish” given he is merely promising to focus on what is the legal mandate of the Federal Reserve. However, he again is emphasising his inflation fighting credentials that understandably is being interpreted that the bias should still be skewed to the Fed hiking rather than cutting while inflation remains this far from target (core 2.6% now).

There is also likely an element of market participants not yet being used to Warsh’s style. Previously we would very likely have heard a positive comment on the low inflation print that markets could have interpreted as “dovish”. But Warsh is not going to offer any forward guidance, and Warsh looks set to focus on the bigger picture rather than providing a running commentary on next monetary policy steps. The numerous reviews launched also gives Warsh cover to hold off on any strong message beyond reiterating the legal mandate of the Fed.

Despite the muted FX reaction, the scale of weakness in the CPI report certainly helps weaken on key pillar of support for the dollar – the prospect of a near-term hike. That can open up scope for further dollar depreciation. However, it is difficult to trade with conviction given the re-escalation in the conflict in the Middle East and the 13% surge in crude oil prices this week. But EUR/USD continues to struggle to sustain declines below the 1.1400 level and at the very least the CPI data reinforces the support around that level.

US SUPERCORE CPI SLOWS WITH 3MTH ANNUALISED RATE AT JUST 1.2%

Source: Bloomberg, Macrobond & MUFG Research

CAD: BoC on hold with inflation risks more contained

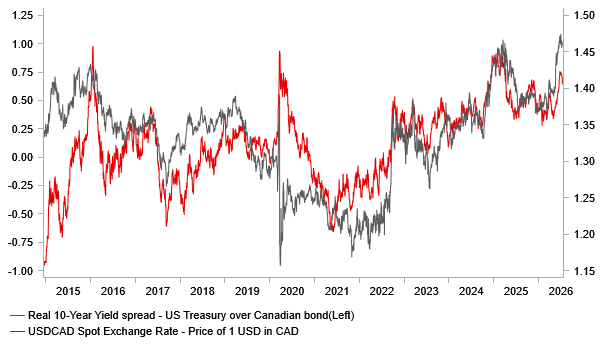

The Norwegian krone, the Canadian dollar and the Australian dollar are performing best behind the New Zealand dollar within G10 since the re-escalation of the conflict with the rebound in energy prices underlining the terms of trade driver of FX performance once again. The same three currencies are in the top four behind the pound covering the period since the conflict first began at the end of February. But from a relative monetary policy stance the Canadian dollar gained yesterday like the rest of G10 versus the US dollar and the 2-year nominal US-CA swap spread points to scope for some further modest gains. As stated above, the CPI print has certainly weakened the support for the dollar and CAD can benefit from that as well. For CAD this can be reinforced by the upturn in crude oil prices.

However, the macro backdrop certainly points to limits to CAD gains from crude oil and today the BoC monetary policy decision should highlight the scope for patience from the BoC given the mixed macro backdrop and weaker inflation. The need for a hawkish message is far less from Governor Macklem than from Fed Chair Warsh yesterday (notwithstanding the better US CPI data). The core CPI annual rate in Canada is at 1.6% while the median and trimmed rates are at 2.0% and 2.1% respectively. No doubt Macklem will acknowledge upside inflation risks since the restart of the conflict but equally the message will likely include Canada having scope to wait and assess given the current favourable inflation picture.

The BoC will also release its updated Monetary Policy Report today and this is likely to highlight a still substantial output gap while inflation could be tweaked higher. In April GDP was forecast to grow at 1.2% in 2026 with inflation at 2.3%. The Bloomberg consensus for growth is just 0.7% and inflation is higher at 2.6%.

With close to 20bps of tightening priced by the end of the year the risks appeared skewed to another cautious communication highlighting the scope for remaining on hold that may disappoint current rates market pricing. Nominal and real spreads, while recently moving in favour of lower USD/CAD are still at levels that point to downside risks for CAD. Trade uncertainty and signs of increased equity market volatility on AI concerns could also act to undermine CAD. The crude oil / Brent correlation is not particularly stable and with the BoC set to remain sidelined, CAD risks are skewed to the downside given the rates pricing (80% priced for hike by year-end).

10-YEAR REAL YIELD SPREAD US-CA CLOSE TO HIGHS

Source: Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EZ | 10:00 | Industrial Production (MoM) | (May) | 0.3% | 0.1% | !! |

EZ | 10:00 | Industrial Production (YoY) | (May) | -0.5% | 0.3% | ! |

UK | 11:30 | BoE MPC Member Pill Speaks | - | - | - | !!! |

US | 12:00 | MBA Mortgage Applications (WoW) | - | - | -2.2% | ! |

US | 13:30 | NY Empire State Manufacturing Index | (Jul) | 9.40 | 5.70 | !! |

US | 13:30 | PPI (MoM) | (Jun) | 0.0% | 1.1% | !!! |

US | 13:30 | Core PPI (MoM) | (Jun) | 0.4% | 0.4% | !!! |

US | 13:30 | PPI (YoY) | (Jun) | 6.2% | 6.5% | !! |

US | 13:30 | Core PPI (YoY) | (Jun) | 5.2% | 4.9% | !! |

CA | 13:30 | Wholesale Sales (MoM) | (May) | -0.7% | 0.6% | ! |

Source: Bloomberg & Investing.com