Fed inflation concerns will ease; US rates market mis-priced

USD: FOMC minutes old news

The FOMC minutes from the last meeting in June will be released this evening and we would caution against reading too much into the details of the minutes given the backdrop in the run-in to the meeting on 17th June are quite different to now. The dots were likely submitted at the end of the previous week (ending 12th June) and we would argue that the breakdown of the FOMC dots would not show nine pitching for a rate hike if the meeting took place now. Nymex crude oil ended the week of 12th June at USD 85pbl, so we have declined a further 17.5% since then. Retail gasoline prices have declined a further 7.5% since then and are back at a level not seen since mid-March. In addition, we have had a weaker than expected NFP report (incl the two-month revision NFP was -17k in June) underlining weaker labour market conditions.

Of more significance for the markets’ expectations of Fed policy was Fed Chair Warsh’s comment at the ECB forum in Sintra last week when he acknowledged that inflation risks were subsiding. An obvious statement given the energy backdrop but surely a reflection of an increased risk of the Fed turning less concerned going forward and hence inflation concerns expressed in the minutes this evening can’t be taken at face-value.

In that regard the OIS curve looks over-priced for rate hikes. There is still close to a 30% probability priced for a rate hike at the meeting on 29th July. Given the labour market data was weaker that pricing looks too high. Close to 40bps of hikes are priced by March 2027 and we see a greater prospect of a rate cut rather than a rate hike by that point. We do accept the risk of re-escalation of the conflict, continued problems related to the re-opening of the Strait of Hormuz (illustrated by today’s US strikes on Iran in response to Iran’s attacks on an LNG tanker) could alter the prospect of the Fed cutting rates but assuming energy prices do not rebound sharply, the rates market looks mis-priced.

The CPI data next week will be key for the July FOMC. But the prospects look good to us that next week should convey signs of the start of disinflation. Energy prices will ease while the implementation of tariffs that saw some sharp increases in import-heavy categories in June 2025 will fall out of annual calculations. Decelerating rents (in Zillow rental data) should also contribute to slower rents in CPI over the second half of the year.

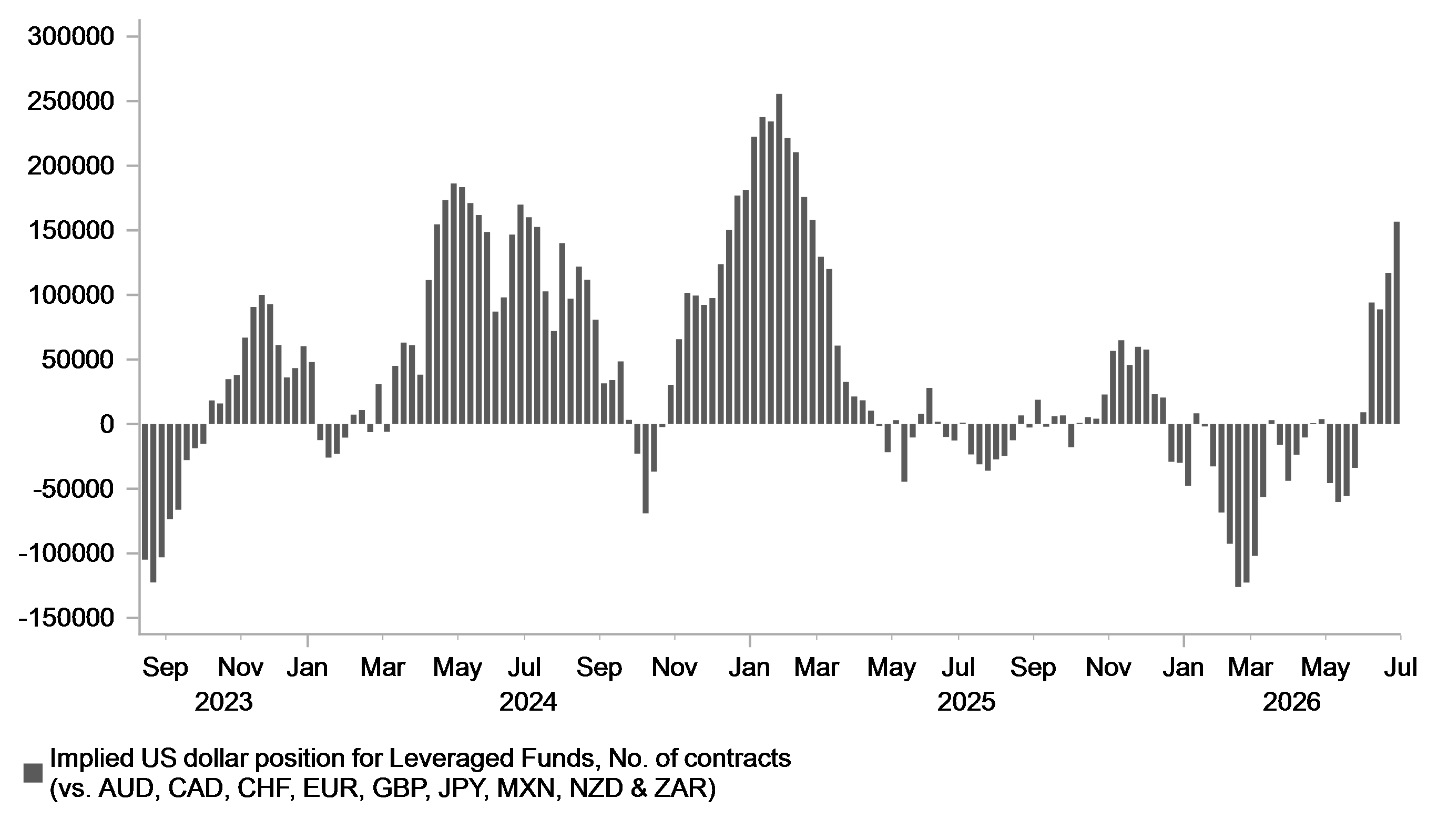

The FX market is increasingly being driven once again by rates spreads with our rolling correlations indicating that and the Fed rate hike pricing has been the key driver of renewed US dollar buying. A lot of this pricing appears driven by the perception that Fed Chair Warsh has been hawkish. But apart from reaffirming the pursuit of achieving the Fed’s 2% inflation goal there is limited evidence to point to of Warsh being particularly hawkish. Leveraged Funds have turned very long dollars very quickly with the flow of data not particularly compelling in backing that up while Warsh’s tag as a hawk is also not well backed up. Sentiment and positioning could well turn quickly if next week’s CPI data is softer and Fed Chair Warsh fails to live up to his hawkish tag at his first semi-annual testimony.

LEVERAGED MARKET HAS TURNED VERY LONG DOLLARS VERY QUICKLY

Source: Bloomberg, Macrobond & MUFG Research

USD: Renewed hostilities as FX vol remains contained

Asian equity markets are mostly lower today with crude oil prices rebounding in response to US strikes in Iranian targets that were triggered by Iranian attacks on tankers in the Strait of Hormuz. Crude oil has jumped by around 3% but equity market declines are generally modest which has resulted in FX volatility remaining relatively subdued. 1-month implied volatility in G10 FX has fallen back below the 6% level to around levels not seen since before the start of Russia’s invasion of Ukraine in 2022. Markets remain optimistically priced given the risks with conviction high that these US strikes do not mark the beginning of a more sustained increase in attacks. Iran has vowed “decisive action” in response to the strikes.

The only notable move for the US dollar this morning has been weaker versus the New Zealand dollar which was in response to the decision of the RBNZ to raise the key policy rate by 25bps to 2.50%, the first hike since May 2023. The OIS market yesterday had 18bps priced for today and 85bps over the coming twelve months. We expected this move, but have only two further hikes priced by March 2027, slightly less than implied by the OIS curve now. We view the RBNZ communication today as broadly consistent with a moderate pace of tightening ahead. There was certainly no sense of urgency or any surprise hawkish rhetoric. Two members indicated in the Record of Meeting that inflation risks were skewed to the upside but the majority saw risks as balanced. The economy remains fragile and the RBNZ appears to recognise that. The 2-year yield increased just 4bps today so follow-through NZD buying should be contained.

Finally, there has also been limited changes to implied vol level in GBP/USD on the back of the announcement from Nigel Farage that he will stand down as MP for Clacton but then contest the same seat in the by-election. This was to protest the investigations by the parliamentary standards committee into his finances on concerns he breached parliamentary rules. This will result in the investigation being suspended but if he wins (or loses) the investigation will restart. None of the other major parties are planning to contest the seat meaning this by-election will turn into something of a sham. This is particularly so given another by-election may ultimately be required if he is found guilty and suspended from parliament which could trigger a recall.

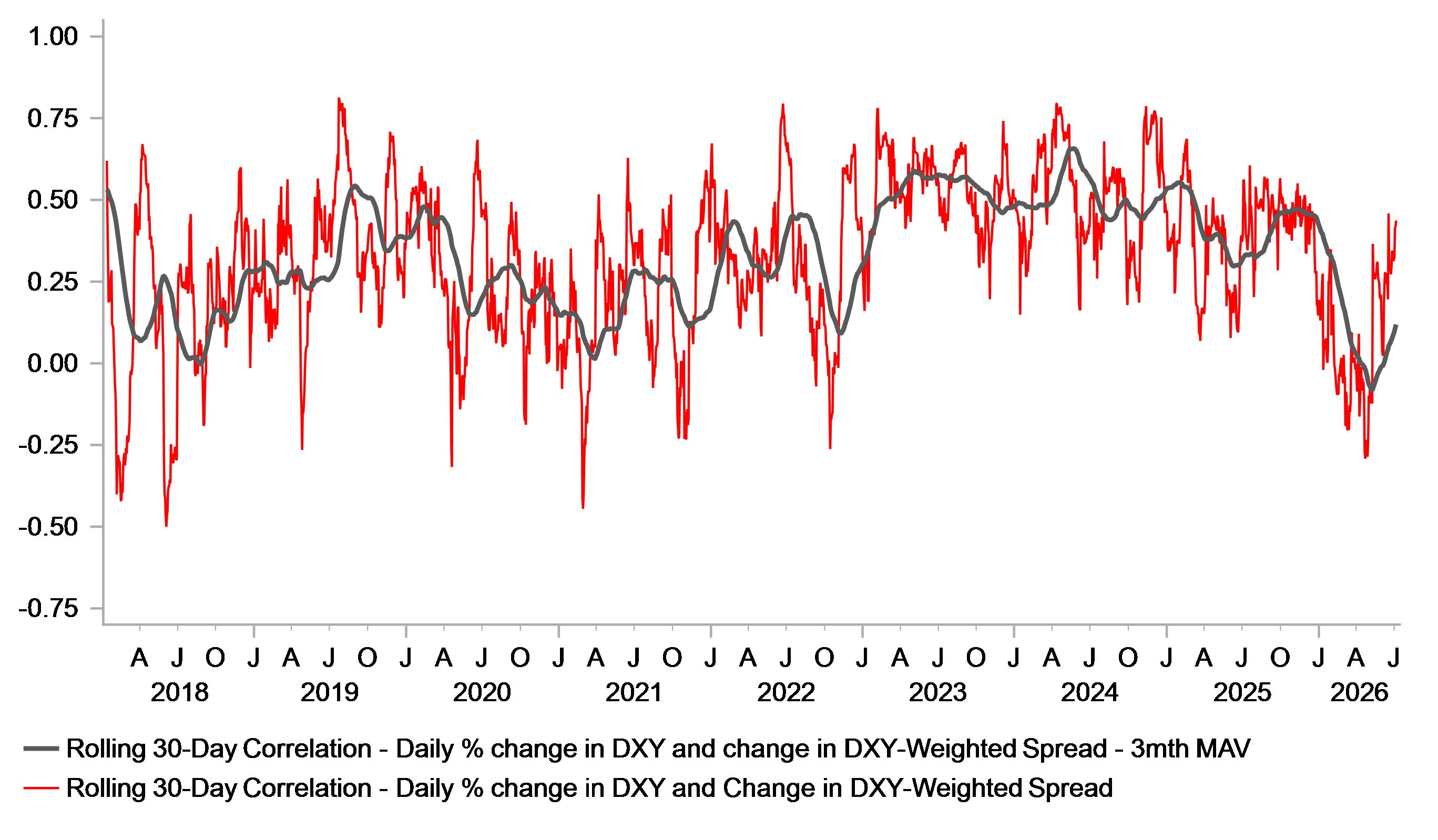

GBP volatility is more aligned to incoming PM Andy Burhnam’s expected economic policies and for now fiscal concerns remain contained. 10-year Gilt yields have retraced more notably lower from the recent peak (15th May) than in the US, Germany and Japan helped by the UK’s weaker inflation pick-up that is also helping to improve investor confidence and support the pound. If there is a G10 currency where yield spread continues to play less of a role in driving FX it’s the pound, which is the top performing G10 currency since the Middle East conflict began at the end of February.

US DOLLAR / YIELD SPREAD CORRELATION IS STRENGTHENING AGAIN

Source: Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

US | 12:00 | Mortgage Application WoW | 3rd Jul | 0.00% | ! | |

EC | 13:00 | ECB's Moulin speaks | !! | |||

US | 15:00 | Wholesale Inventories MoM | May F | 0.30% | 0.30% | ! |

EC | 17:00 | ECB's Kocher speaks | !! | |||

US | 19:00 | FOMC Minutes | !!!! |

Source: Bloomberg & Investing.com