Renewed Middle East tensions providing support for USD

USD: Upside inflation risks in focus ahead of semi-annual testimony

The US dollar has strengthened modestly at the start of this week encouraged by renewed military tensions between the US and Iran. The US Central Command stated that American forces had carried out a new round of attacks to degrade Iran’s ability to threaten shipping in the Strait of Hormuz. According to a post on X, Centcom confirmed that it hit dozens of targets including Iranian air-defence systems, coastal radar sites, and missile and drone capabilities. In response, Iran has targeted US military bases in Kuwait, Bahrain and Jordan according to Iranian media outlets. The latest escalation extends the series of tit-for-tat strikes over the past week with Iran’s retaliation widening to an increasing number of Arab states in the region. After targeting multiple commercial vessels passing through the Strait of Hormuz, Tehran has stated that it would now be closed “until further notice”. However, President Trump has claimed it remains open backed up by the Joint Maritime Information Centre who reported that as of yesterday it was still possible to transit the strait’s southern route. The unfavourable developments have prompted market participants to price back in a bigger geopolitical premium into the price of oil lifting Brent back up to USD80/barrel.

The spill-over effects into the foreign exchange market remain relatively modest far. A significantly higher price of oil has the potential to be a more powerful bullish catalyst for the US dollar now that the Fed has indicated recently that it considering raising rates in response to upside inflation risks. US inflation risks will be in focus in the week ahead when the latest US CPI report for June is released. The report is expected to provide confirmation that headline inflation may have already peaked. Headline inflation is expected to slow to 3.8% in June from 4.2% in May, helped in part by a roughly 10% decline in average US gasoline prices during the month. Market participants will also be watching closely for signs of second-round effects from higher energy prices feeding into underlying inflation. So far, core inflation has increased only modestly since the onset of the US-Iran conflict, accounting for just 0.3 percentage points of the 1.8 percentage point rise in the annual CPI rate since February. Another benign core reading, alongside easing energy inflation, would likely encourage market participants to pare back expectations for further Fed rate hikes, putting a dampener on US dollar strength in the week ahead.

One inflation risk that is attracting increasing attention from Fed officials is the potential boost to demand from surging AI-related capital investment. New York Fed President Williams recently noted that, “if this creates a sustained impulse to demand relative to supply and inflation, then I do think that’s the kind of situation where you don’t look through this.” He added that, “on the other hand, if it doesn’t and things play out in a more benign way, I do think monetary policy is, and continues to be, well positioned.” A breakdown of the Fed’s preferred measure of inflation, the core PCE deflator, suggests that information-processing equipment has started to make a positive contribution, adding 0.18 percentage points to the annual inflation rate of 3.4% in May. This compares with an average annual contribution of -0.03 percentage points over the previous five years. At this stage, the additional upward pressure on core inflation remains relatively modest. However, it has the potential to exert a more meaningful influence on inflation and Fed policy going forward. Further insights into the Fed’s thinking on inflation will be provided by Fed Chair Kevin Warsh when he testifies before Congress on Tuesday and Wednesday delivering the Fed’s semi-annual testimony on monetary policy.

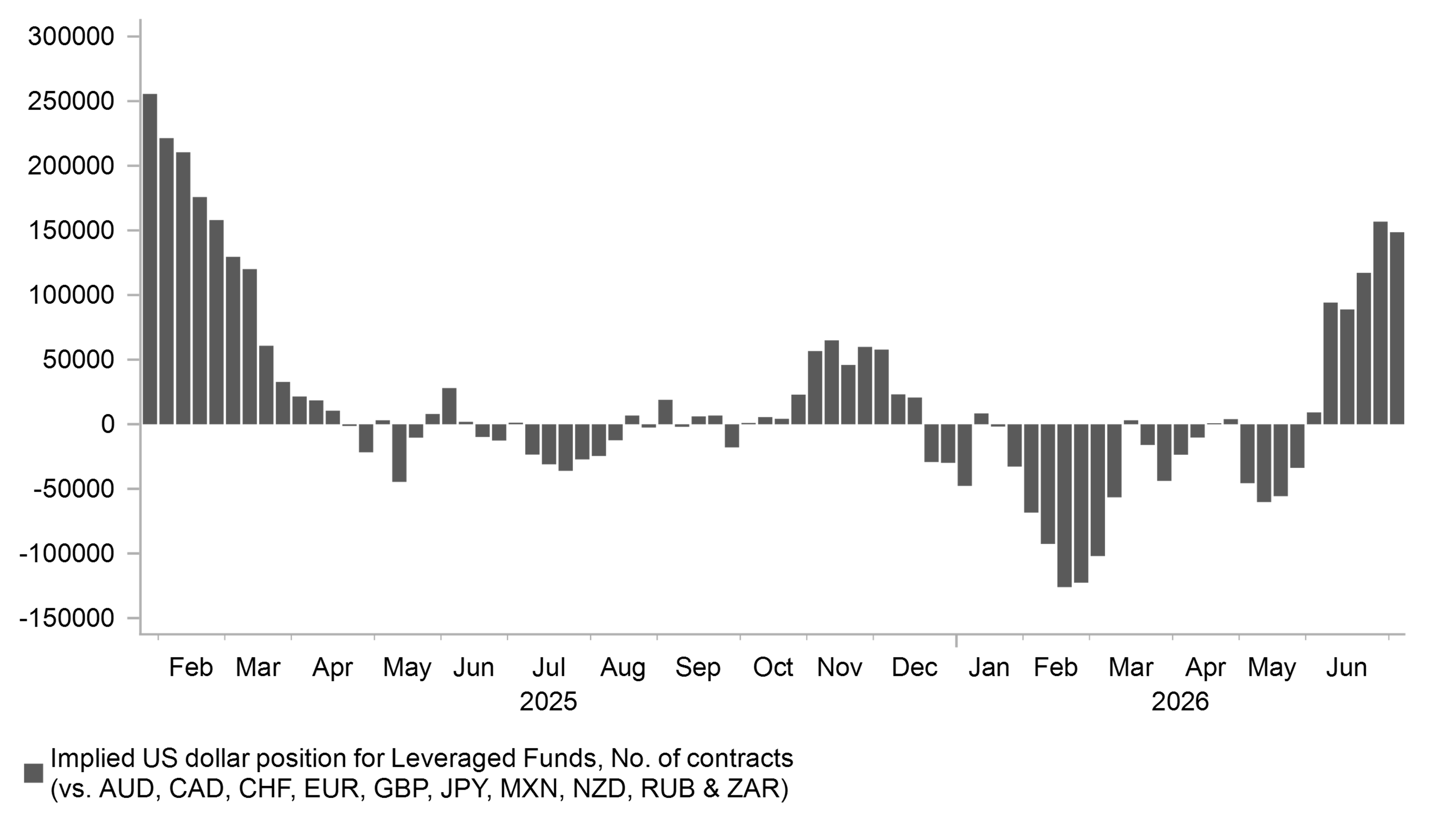

LONG USD POSITIONS REMAIN POPULAR AMONGST LEVERAGED FUNDS

Source: Bloomberg, Macrobond & MUFG Research

JPY: Higher energy prices weigh on yen after last week’s verbal intervention

The yen has re-weakened at the start of this week resulting in USD/JPY rising back above 162.00. All of the gains recorded on Friday after verbal intervention from Finance Minister Katayama have been reversed. At the same time, JGB yields have picked up but are still much lower. After the drop on Friday, the 10-year and 30-year JGB yields remain around 8bps and 10bps lower. The yen and JGBs were supported at the end of last week by comments from Finance Katayama who stated that “one priority is to encourage households, as well as pensions funds including the GPIF, to increase their investment in Japanese financial assets”. While we certainly view this as potentially meaningful, we still have only had this comment made by Finance Minister Katayama at a regular press conference and hence to what extent any formal policy is being compiled is unclear. The MoF does not have the remit of setting the medium-term objectives of the GPIF – that resides with the the Ministry of Health, Labour and Welfare. So we think firstly we would need to see this cited more regularly as something being looked at from a policy perspective with the MHLW then formulating an updated objective. It is the GPIF’s Board of Governors that ultimately set the asset composition mix and all of this certainly points to no quick implementation of any new policy.

Reuters has since reported overnight that Japan has no plans to overhaul GPIF asset allocation citing unidentified people with knowledge of government deliberations. The report did add though that government is exploring ways to boost investments within the existing allowable ranges of the benchmark portfolio. At the end of FY2025, the GPIF held 26.91% of its investment portfolio in domestic bonds and 23.81% in domestic equities. The current target asset allocations allow the GPIF to hold up to 31% for both domestic bonds and equities. So there is already significant room there for the GPIF for increase domestic asset holdings without having to change target allocations. For example, based on the total value of investment assets held at the end of FY2025 there was room to increase allocations to domestic assets (bonds & equities) by just under JPY34 trillion. Please see our latest FX Weekly report for more details (click here).

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

US | 10:25 | FOMC Member Bowman Speaks | - | - | - | !! |

DE | 13:00 | German Current Account Balance n.s.a | (May) | - | 13.8B | ! |

US | 17:30 | Fed Waller Speaks | - | - | - | !! |

EU | 17:45 | ECB's Schnabel Speaks | - | - | - | !! |

GB | 19:00 | BoE MPC Member Pill Speaks | - | - | - | !! |

US | 19:00 | Federal Budget Balance | (Jun) | -132.8B | -293.0B | !! |

EU | 22:00 | ECB President Lagarde Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com