Political uncertainty intensifying in UK weighing on GBP

USD/JPY: Japan & US discuss need for intervention during Middle East conflict

The US dollar has continued to trade at stronger levels at the start of this week reflecting investor unease over the lack of progress to bring an end to the Middle East conflict and re-open the Strait of Hormuz. The latest bout of investor unease was triggered by comments from President Trump calling Iran’s response to his peace proposal a “piece of garbage” and highlighting that he “didn’t even finish reading it”. According to a person familiar with the matter, Iran responded to last week’s US peace proposal by demanding the US lift their naval blockade of Iran’s ports while wanting to maintain a degree of control over traffic through the “Strait of Hormuz”. In order to increase pressure on Iran to reach a deal, President Trump warned that the current ceasefire is on “massive life support”. It has also been reported by Axios that President Trump was met with his national security team to discuss the war including the possible resumption of military action. The latest developments continue to highlight that ending the conflict and re-opening the Strait could take longer than expected, and result in a more disruptive outcome for the global economy and financial markets.

The rebound for the US dollar and the price of oil has helped to lift USD/JPY back up towards the 158.00-level overnight where the pair was trading prior to the last bout of suspected intervention from Japan on 6th May. It is making market participants nervous that Japan will step back in again soon to support the yen again. USD/JPY has since just dropped sharply by around 1 big figure from a high overnight of 157.75. According to media reports Japan has spent around USD10 trillion to support the yen, and further intervention will likely be required if the fundamentals factors that driven a weaker yen do not change soon. The Middle East conflict has triggered higher energy prices which have hurt Japan’s terms of trade, and yield spreads have moved against the yen recently as rate hikes have been priced in for other major central banks. The BoJ’s decision last month to delay hiking rates in response to heightened uncertainty over the Middle East conflict has not helped the yen.

Market participants are watching closely to see how the latest meetings between US Treasury Secretary Scott Bessent and Japanese officials will play out this week. He has previously called on Japan to speed up the pace of monetary tightening which would offer more support for the yen and has expressed concern over potential negative spillover effects from a sell-off in JGBs into the US Treasury market. After meeting with Finance Minister Katayama overnight, he posted “I am pleased to reaffirm the strong economic partnership between the US and Japan. The level of communication and coordination between our teams in addressing undesirable, excess volatility in currency markets continues to be constant and robust”. The comment indicates that the US remains supportive of Japanese intervention to support the yen. At the same time, Finance Minister Katayama similarly stated “regarding recent currency moves, we confirmed that Japan and the US have been coordinating very well and have maintained close communication. We also reaffirmed that we will continue to work closely together on currencies in line with the joint statement issued last September”. She believes that they have “full understanding” that intervention is among options for addressing excessive volatility in the foreign exchange market. It leaves the door open for further intervention to dampen yen weakness while the Middle East conflict remains unresolved.

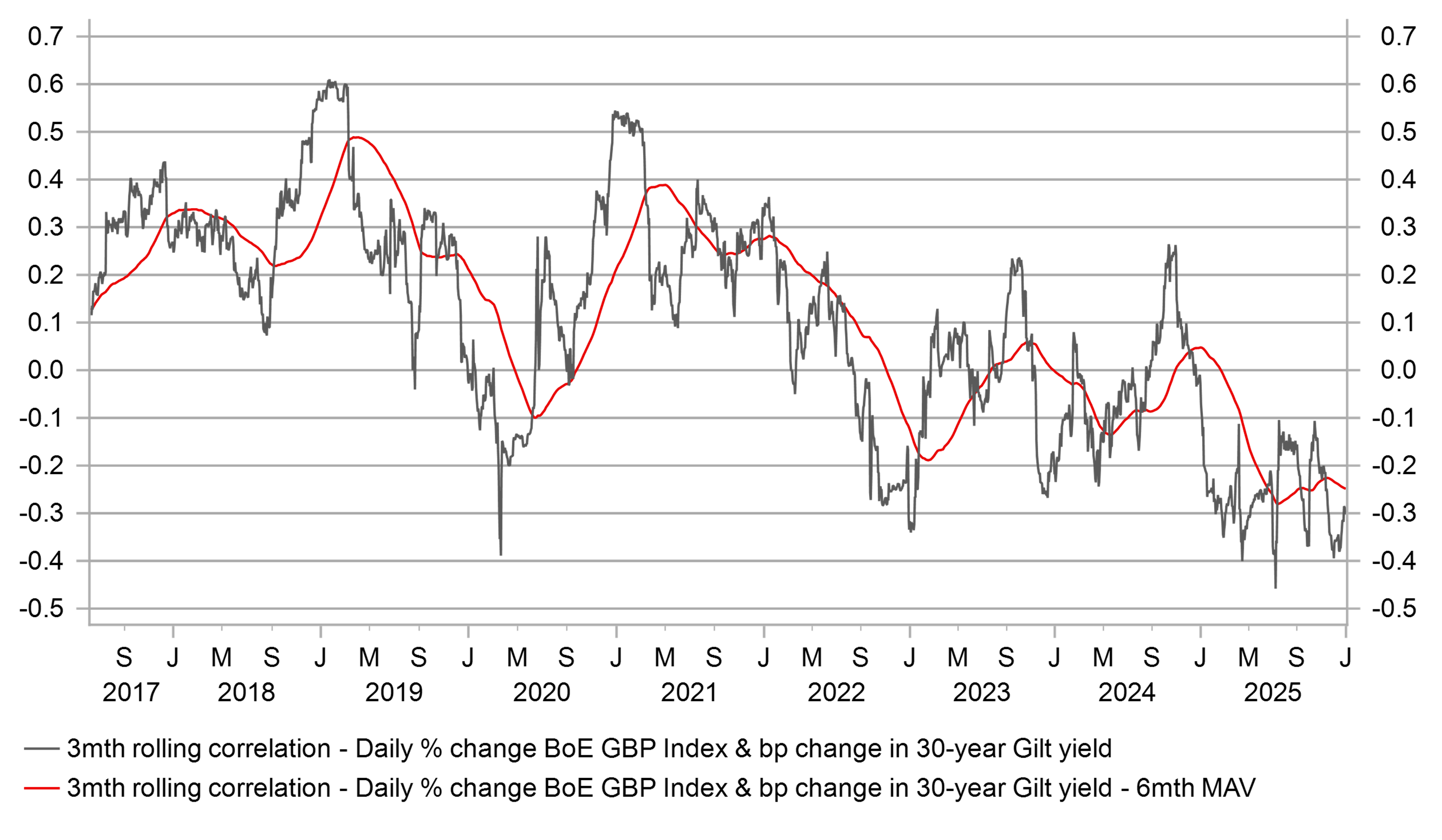

RISK OF SELL-OFF FOR GBP & GILTS IS INCREASING

Source: Bloomberg, Macrobond & MUFG GMR

GBP: Downside risks increase as UK political risks intensify

The pound has weakened further at the start of this week reflecting building political uncertainty in the UK after last week’s disappointing local election results for the government. Pound weakness has extended overnight resulting in EUR/GBP rising up to 0.8675 and cable has fallen towards 1.3550. It has triggered a sell-off in the Gilt market where 10-year and 30-year yields both increased by around 15bps. So far the market moves have been relatively modest but are beginning to reflect building unease over the future of Prime Minister Keir Starmer who is facing growing pressure from within the Labour party to step down.

It has been reported that 79 of Labour’s 403 MPs have now publicly called on the prime minister to step aside which is moving closer to the 81 MPs required to officially trigger a leadership contest. Prime Minister Starmer faces an important cabinet meeting today. Within the cabinet, it has been reported that Home Secretary Shabana Mahmood, Foreign Secretary Yvette Cooper and Defence Secretary John Healey are privately urging Starmer to consider plans for handing control to a successor. Pressure intensified yesterday on Starmer after four ministerial aides quit the government saying they no longer believed he could tun things around. The latest developments increasingly look like the end of the road for Keir Stamer as prime minister. A leadership contest whether immediate or more drawn out will add to political uncertainty in the near-term which is negative for the pound and gilts. The risk of a bigger sell-off will increase if Labour shift towards the left. We continue to recommend a short GBP/CHF trade idea in our latest FX weekly report (click here).

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

US | 08:15 | FOMC Member Williams Speaks | - | - | - | !! |

EU | 10:00 | ZEW Economic Sentiment | (May) | -21.6 | -20.4 | !! |

US | 11:00 | NFIB Small Business Optimism | (Apr) | 96.0 | 95.8 | ! |

US | 13:30 | CPI (YoY) | (Apr) | 3.7% | 3.3% | !!! |

US | 18:00 | Fed Goolsbee Speaks | - | - | - | ! |

Source: Bloomberg & Investing.com