To read the full report, please download PDF.

US/Iran deal optimism continues to weigh on USD

FX View:

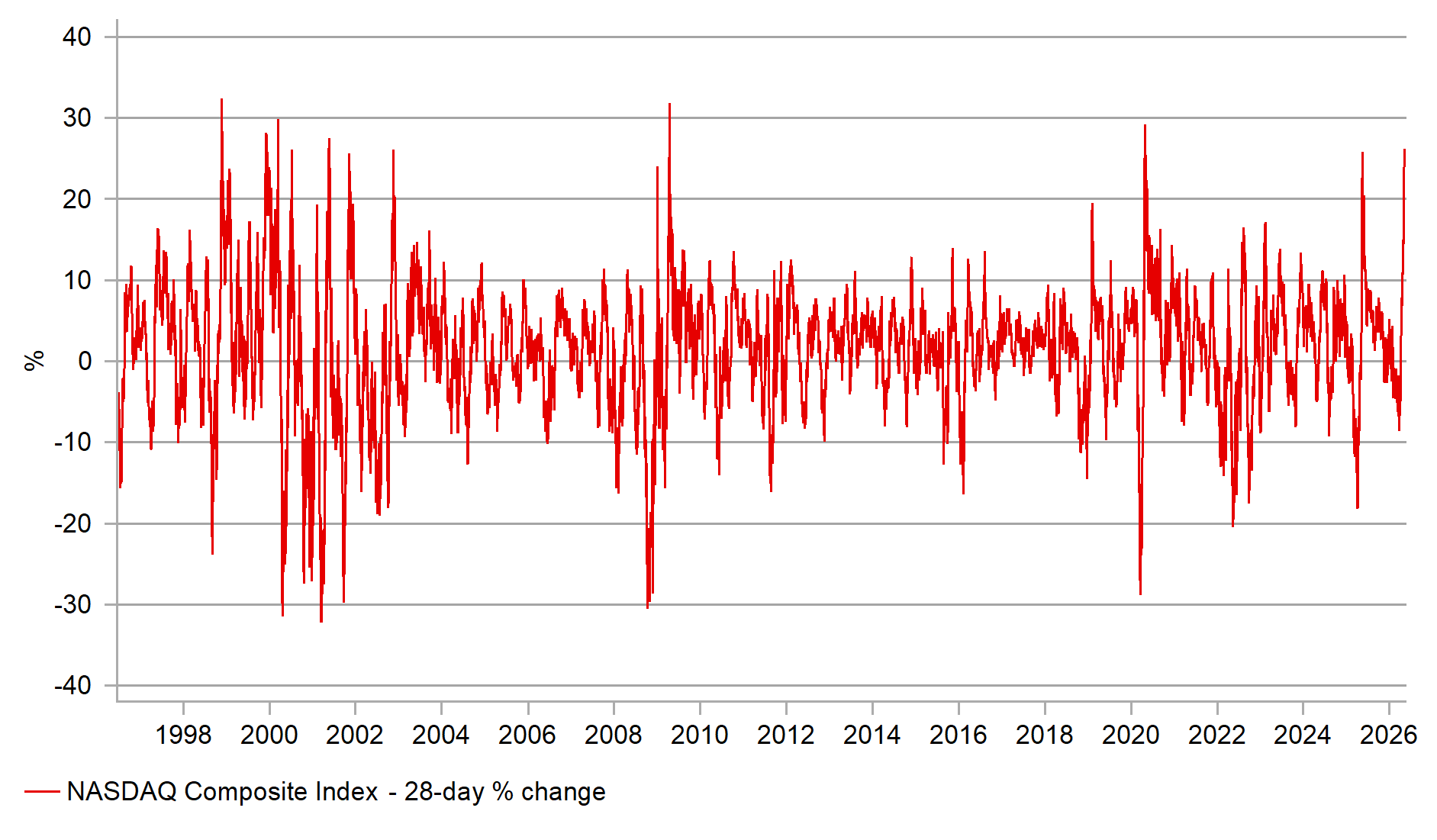

The US dollar weakened further last week with no resolution to the Middle East conflict in sight. Attacks in the Strait of Hormuz increased but the US maintains the ceasefire remains in place. That has seen oil prices drop over the last week. While much attention remains on whether a peace deal can be made, risk appetite has reached new levels with US equities closing last week at new highs. The Nasdaq Composite closed on Friday an incredible 26.2% higher from the most recent closing low on 30th March. There have only been moves of that magnitude during the dotcom boom/bust (1999-2001); the GFC and covid. The magnitude of such strong risk appetite is lifting global optimism and encouraging US dollar selling. A strong US jobs report was not enough to trigger US dollar strength. The could still see renewed gains and the longer the Strait of Hormuz remains closed the greater the potential of a turn in risk sentiment. President Trump confirmed over the weekend that the Iran response to US proposals was “totally unacceptable” raising the risk of fuel shortages becoming a bigger issue over the coming months.

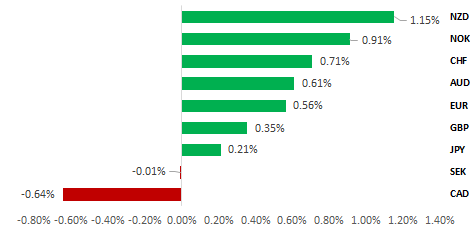

USD WEAKENS VERSUS MOST G10 AS CRUDE DROPS & EQUITIES RISE

Source: Bloomberg, close on 8th May 2026 (Weekly % Change vs. USD)

Trade Ideas:

We are recommending a new long AUD/SEK trade idea and maintaining a short GBP/CHF trade idea.

JPY Flows:

FDI outflows from Japan remain a key factor driving JPY weakness with data covering up to March. Foreign investors remain the consistent source of demand with fifteen consecutive months of net purchases.

FX Systematic Breakdown:

Systematic FX strategies such as Carry, Momentum, Value, and Volatility, generate excess returns over time, but their performance is regime dependent. This week we assess the underperformance of our systematic strategies given the current geopolitical backdrop.

FX Views

USD: Strong jobs data secondary for now

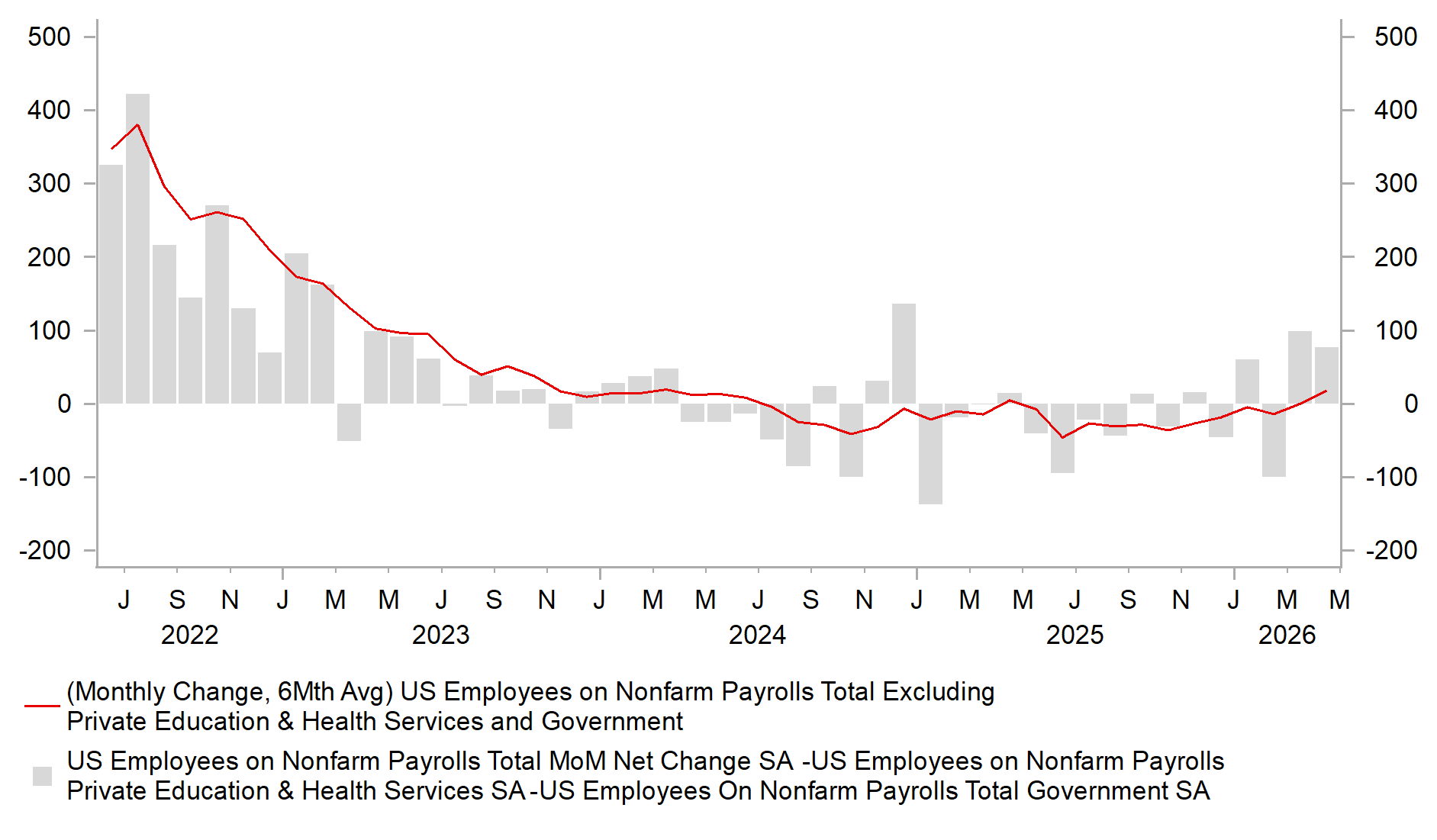

The US dollar remains weaker following the US employment report on Friday – the 115k increase in nonfarm payrolls on the face of it is certainly indicative of some signs of improving labour market conditions. With such a large set of data there is plenty of detail to analyse and some of the details provided some reason for caution. Firstly, wage growth was weaker than expected rising to 3.6%, below the expected 3.8% increase highlighting the looser labour market conditions. Secondly, while the unemployment rate was unchanged at 4.3%, the participation rate fell from 61.9% to 61.8% - if that hadn’t happened the unemployment rate would have risen. The underemployment rate also increased from 8.0% to 8.2%. Still, there is some emerging signs of better labour demand outside of the reliable education and health sectors. Private payrolls, excluding health & education increased by 77k in April, the third gain in four months. The 6mth average reached 18k, which was the biggest 6mth average rate since March 2024. The financial market response suggests the focus was on the details that pointed to still weak aspects of the labour market but likely also reflected expectations that the conflict in the Middle East would de-escalate further and see further declines in energy prices.

We would still conclude that downside risks to the economy remain more relevant at this stage of the cycle. The Michigan Consumer Sentiment index fell to a new record low on Friday with the cost of living concerns very likely the source of the latest downturn in confidence. This is coinciding with softening nominal wage growth that is set to translate into continued weak growth in real incomes. Weak real income growth will likely encourage the Fed to ease its monetary stance later in the year, assuming there is no escalation in the conflict that results in larger inflation increases. That backdrop for US consumers, the prospects of continued geopolitical uncertainties and the risk of renewed trade uncertainties with Trump threatening further tariff actions do not suggest a sustained pick-up in labour demand is imminent. The OIS curve remains largely flat with some modest tightening (+6bps) priced by March 2027. A flat curve on expectations of the Fed remaining on hold is supportive of continued strong risk appetite. The mixed jobs report saw the S&P 500 and the Nasdaq Composite close at new record highs on Friday. That remains a more dominant driver of FX than changes in front-end rate spreads. The Nasdaq is up a staggering 26% since the low on 30th March underlining the dominance of AI sentiment over Middle East conflict concerns.

The pound advanced versus the US dollar last week but weakened versus the euro although the moves were modest and since the conflict began, the pound remains the third best performing G10 currency. No doubt, just like the US dollar is underperforming due to strong global risk appetite, the pound tends to perform well in period of strong risk appetite and hence is benefitting from the current strength in global equities. The political risks may well be about to subside. Labour MP, Catherine West, has stated she will launch a challenge if Starmer’s cabinet do not, but the prospects of success are low. The big hitters appear reluctant to launch a challenge at this stage which certainly raises the prospect of Starmer surviving the summer period ahead of the party conference period in September/October. 30 Labour MPs have called for Starmer to step down but West will need 80 or so members in order to trigger a leadership challenge. Nobody in cabinet have publicly moved against Starmer and if he survives the coming days then he will likely be safe for now.

PRIVATE PAYROLLS EX-HEALTH/EDUCATION RISING

Source: Bloomberg, Macrobond & MUFG GMR

SURGE IN AI/TECH-RELATED EQUITY BUYING

Source: Bloomberg, Macrobond & MUFG GMR

Starmer is set to give a speech today (10am BST) and that is viewed as an attempt to ‘reset’ and provide some fresh impetus and policy direction. This will be follows on Wednesday by the King’s speech which will be another key part of Starmer’s attempt at a refresh and create some positive momentum. Tightening EU links and supporting youth employment are likely to be key aspects.

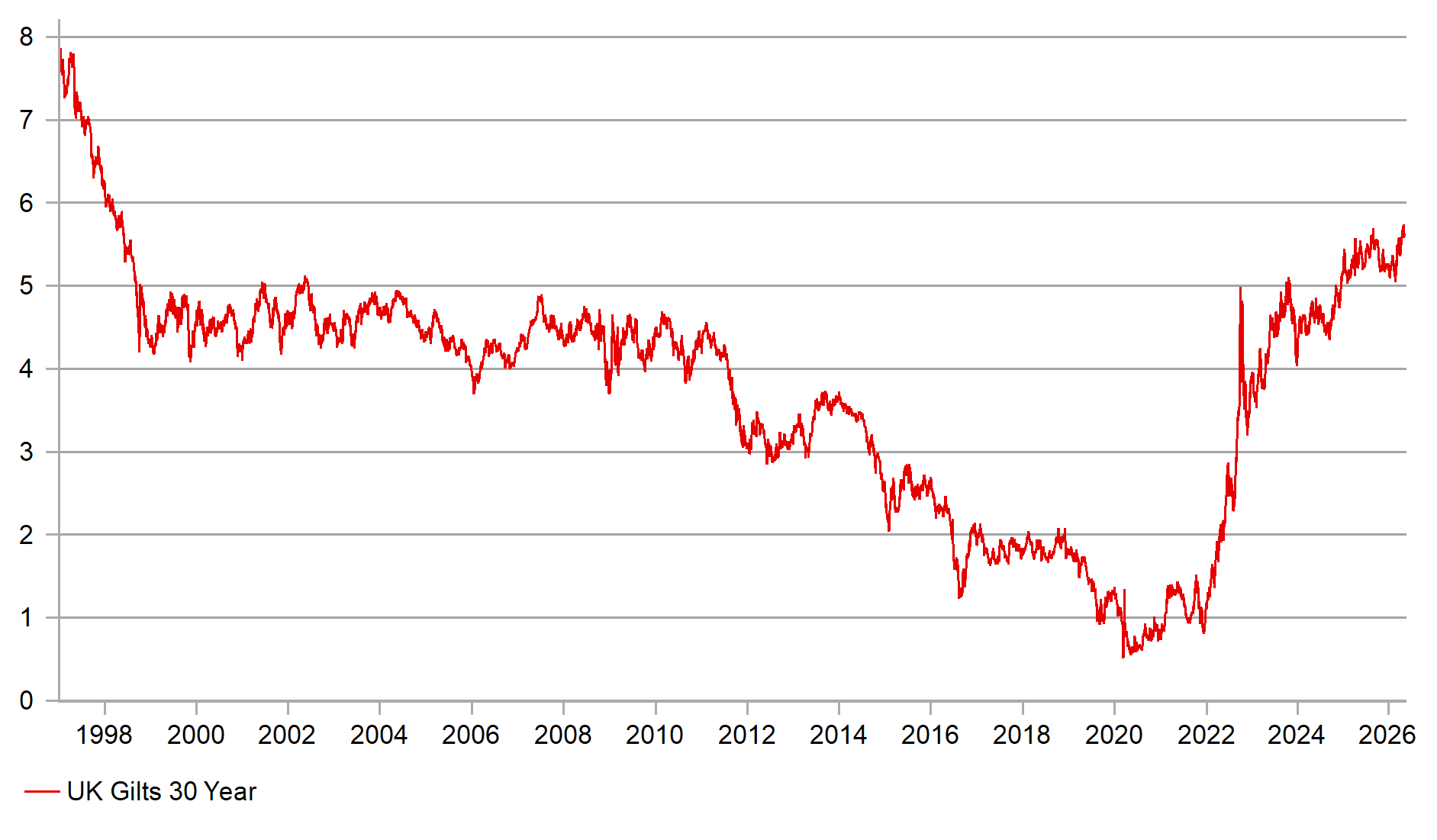

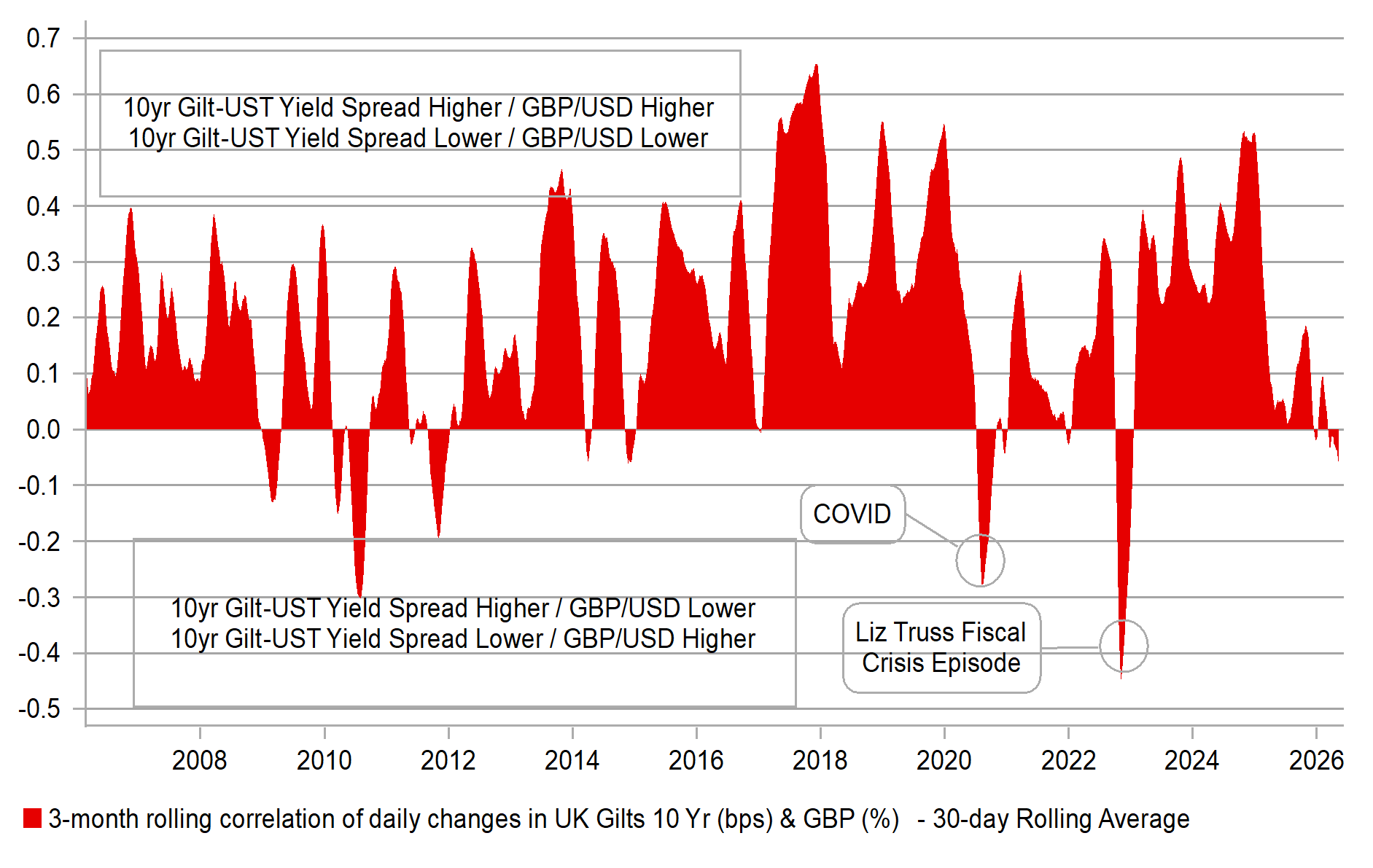

Perhaps the best case for arguing that PM Starmer’s cabinet colleagues and Labour backbenchers will not push to unseat him is the probable turmoil it would create in the financial markets. The Gilt market this morning is modestly underperforming with 10yr & 30yr yields up more than in Germany or the US. A challenge from someone to the left of the party would only reinforce expectations of fiscal slippage and there is a strong argument to be made that now, at this time of great geopolitical uncertainty and energy price risks, is not the time to unsettle the Gilt market. That would lead to accusations that the uncertainty is pushing up mortgage costs for households at a time of a renewed rise in the cost of living. We suspect that PM Starmer will survive for now but to some degree Starmer is at the mercy of international events. A worsening of the cost of living due to the conflict would increase his unpopularity and likely result in a leadership challenge, possibly over the summer before the party conference season in Sep/Oct.

The Trump response to the Iran response to US proposals to end the war as “totally unacceptable” leaves risks of a renewed energy price spike skewed to the upside. The US dollar is stronger today but only modestly and there remains time based on the very favourable global inventories available prior to the start of the war. But the Amsterdam-Rotterdam-Antwerp energy hub is seeing jet fuel inventories falling sharply to a six-year low. Most estimates suggest some time during June would be the critical point for refined fuel shortages in Europe so there remains a period of time before disruptions become evident. Still, with risks of disruption rising, the appetite for selling the dollar at these weaker levels is likely to diminish.

30-YEAR GILT YIELD BACK AT 1998 LEVELS

Source: Bloomberg, Macrobond & MUFG GMR

SIGNS OF FISCAL RISK PREMIUM EMERGING AGAIN

Source: Bloomberg, Macrobond & MUFG GMR

G10 FX: Are diverging central bank policies impacting FX performance?

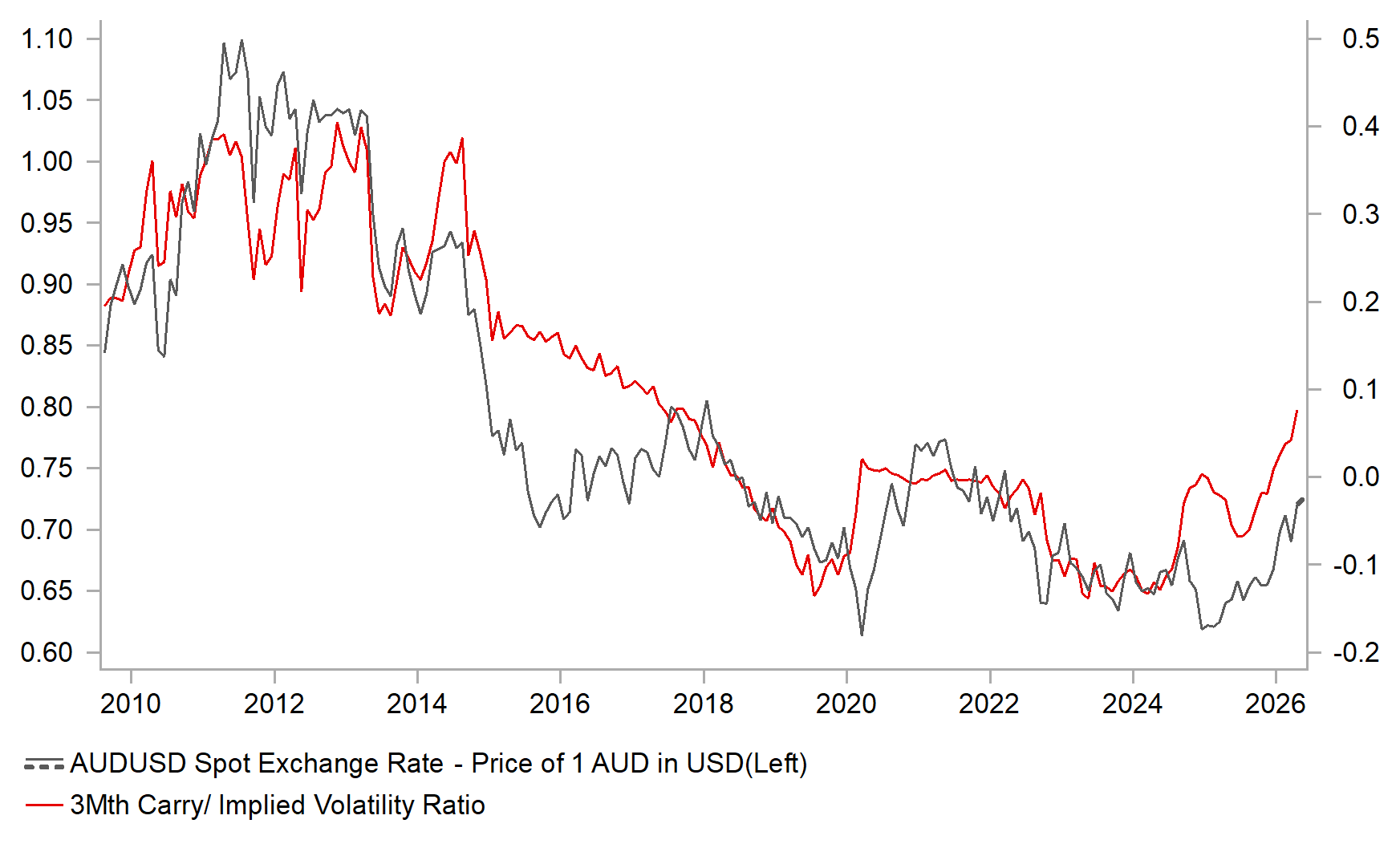

G10 FX performance has been mixed since the outbreak of the Middle East conflict at the end of February. The strongest performing currencies have been the commodity currencies, with NOK up 3.4% against the USD and AUD up 1.8%, while SEK (-2.2%) and CHF (-1.1%) have underperformed. In contrast, the major currency pairs of EUR/USD, GBP/USD, and USD/JPY remain within ±1.0% of their pre-conflict levels. Both AUD and NOK have benefited from improved terms of trade driven by higher energy prices, as well as from the hawkish responses by their domestic central banks to the energy price shock. Over the past week, the RBA and Norges Bank have both raised interest rates and signalled that further hikes remain possible this year.

For the RBA, this marked the third consecutive rate hike at the start of the year, lifting the policy rate to 4.35% which is the highest among G10 central banks. The RBA now assesses that policy is modestly restrictive, with the cash rate having moved above the upper bound of its estimated neutral range of 2.75%–4.25%. After delivering three consecutive hikes, the RBA has indicated that “policy is well placed” to respond to future developments. The updated guidance suggests that a pause is unlikely at the next meeting in June but the Australian rates market continues to expect at least one further hike by year-end. Higher yields are helping to make the AUD more attractive as a carry currency once again, and an additional hike would push the policy rate to its highest level since 2011. At the same time, financial conditions remain supportive for carry trades, as increased volatility in energy markets has not translated into a sustained rise in broader financial market volatility. Both G10 and EM FX volatility have declined toward pre-conflict lows. Investor optimism around a potential diplomatic resolution to the conflict and the reopening of the Strait, alongside strong US corporate earnings in Q1, have also helped drive global equity markets to new record highs boosting demand for high beta G10 commodity currencies.

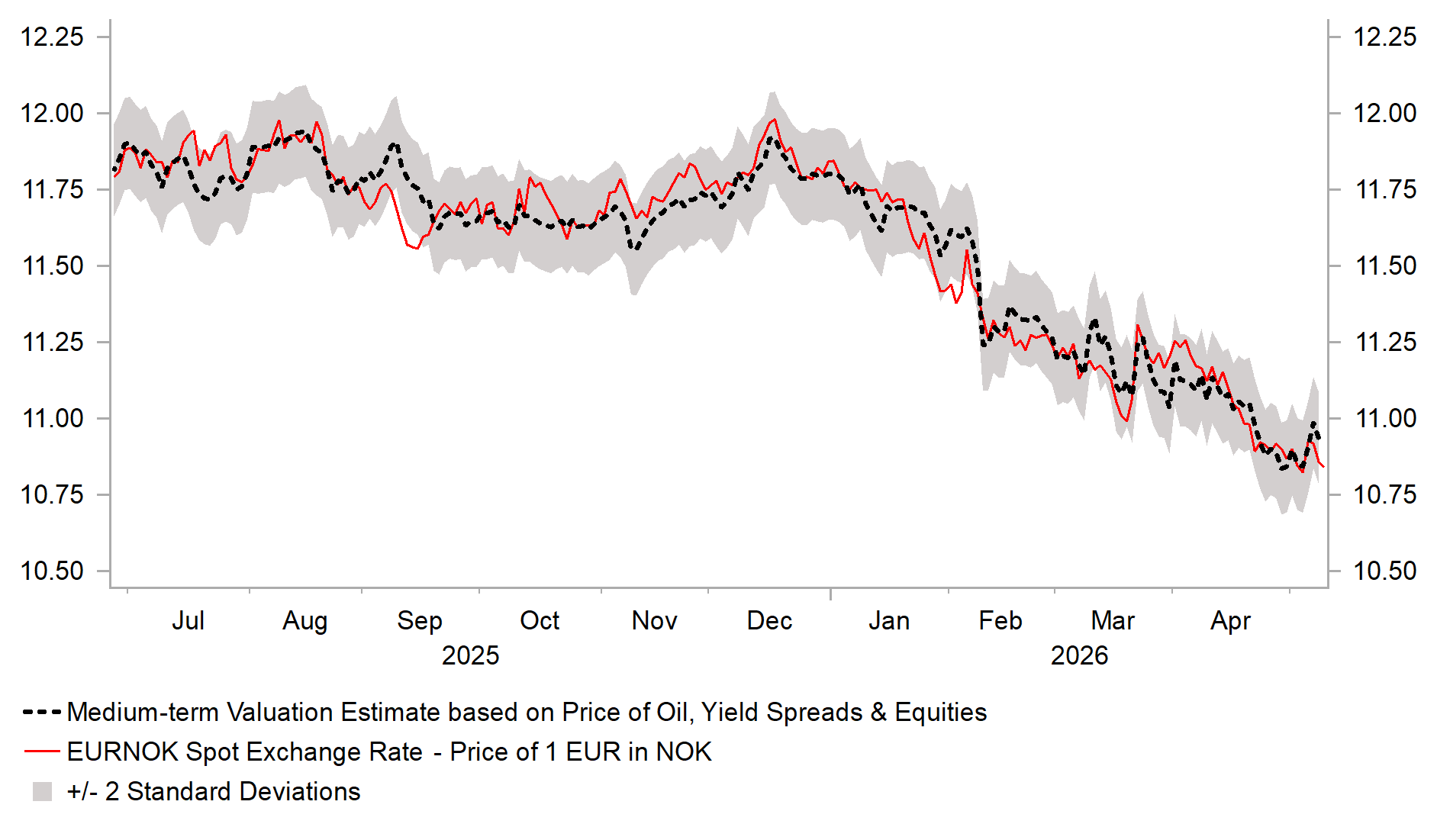

The Norges Bank became the second G10 central bank to raise rates since the onset of the Middle East conflict. The timing of last week’s 25bps hike was slightly earlier than expected by market participants and Norwegian economists surveyed by Bloomberg. However, it did not come as a significant hawkish surprise, as the Norges Bank had clearly signalled at its previous policy meeting in March that it “will likely be appropriate to raise the policy rate at one of the forthcoming meetings.” The Norges Bank maintained its prior guidance that the policy rate is likely to end the year in the 4.25%–4.50% range. The Norwegian rates market is also pricing in at least one additional hike this year. As in Australia, yields in Norway remain among the most attractive within the G10, reinforcing the NOK’s upward momentum. The currency has already posted strong gains, with its appreciation against the USD this year approaching 10%. The main downside risk to the NOK’s current upward trajectory would be a near-term agreement between the US and Iran to resolve the conflict and reopen the Strait, which could trigger a sharp correction lower in energy prices. Absent such a development, elevated yields and energy prices are likely to continue supporting the NOK.

IMPROVING CARRY APPEAL OF AUD

Source: Bloomberg, Macrobond & MUFG GMR

STRONGER NOK SUPPORTED BY FUNDAMENTALS

Source: Bloomberg, Macrobond & MUFG GMR

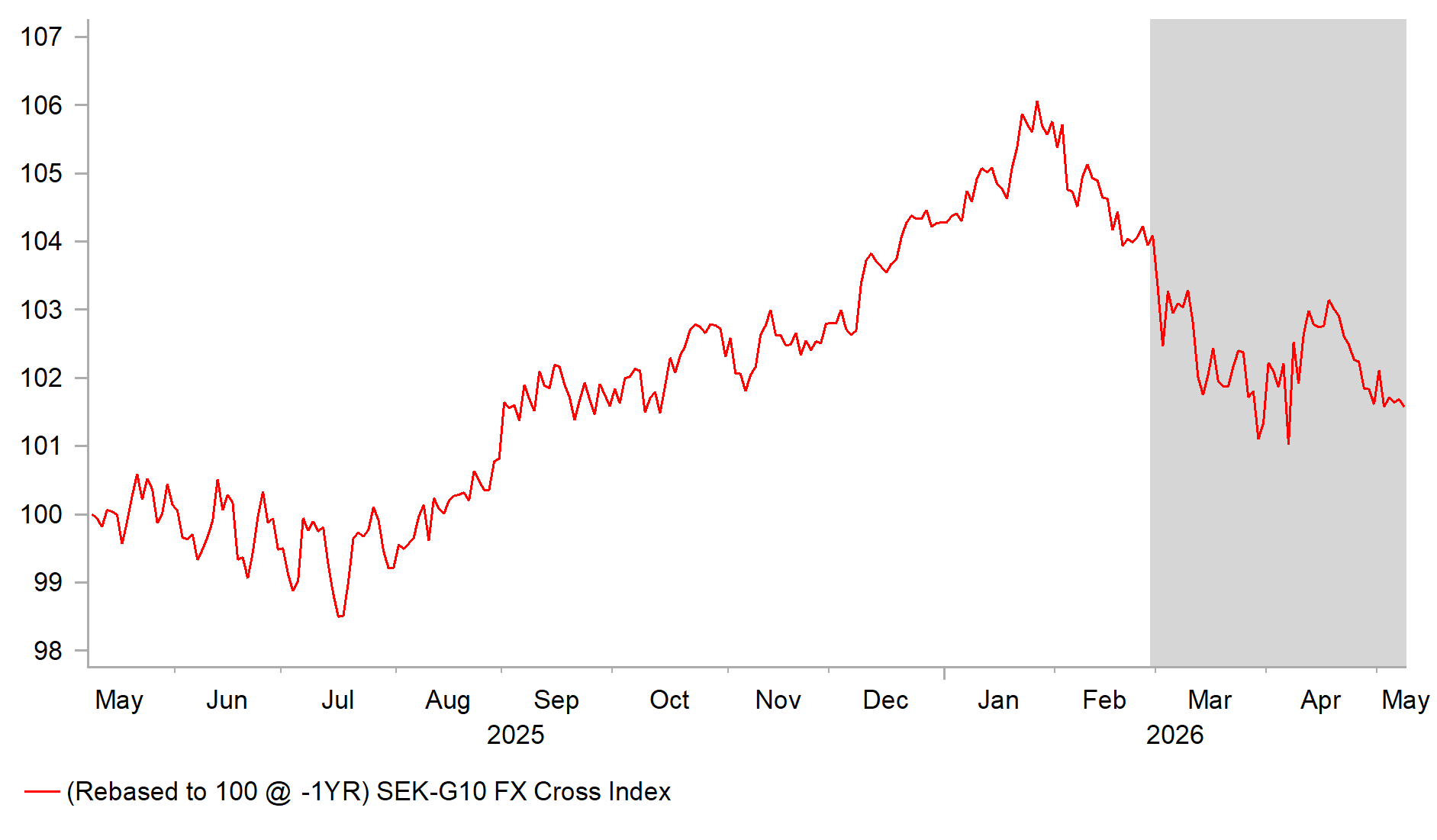

In contrast, the Riksbank in Sweden is not in a rush to follow the Norges Bank in raising rates. Recent weaker growth and softer inflation have given the Riksbank greater scope to look through the energy price shock. The latest CPI report showed headline inflation falling into negative territory in April, while core inflation (CPIF excluding energy) remained flat. These developments have provided the Riksbank with leeway to signal that the current policy rate offers a “good initial position” from which to adjust monetary policy if needed to safeguard the inflation target. The Riksbank did note though that it would consider raising the policy rate if the war were to have significant effects on the global economy and lead to a “broad and persistent” increase in inflation. This cautious guidance suggests that a rate hike is unlikely as soon as the next policy meeting in June. The Riksbank’s relatively dovish stance is contributing to the SEK’s underperformance, alongside the negative impact from higher energy prices. A similar pattern was observed during the last energy price shock in 2022 following Russia’s invasion of Ukraine. Even the recent optimism surrounding a potential agreement between the US and Iran to resolve the conflict and reopen the Strait has so far failed to generate a meaningful rebound in the SEK.

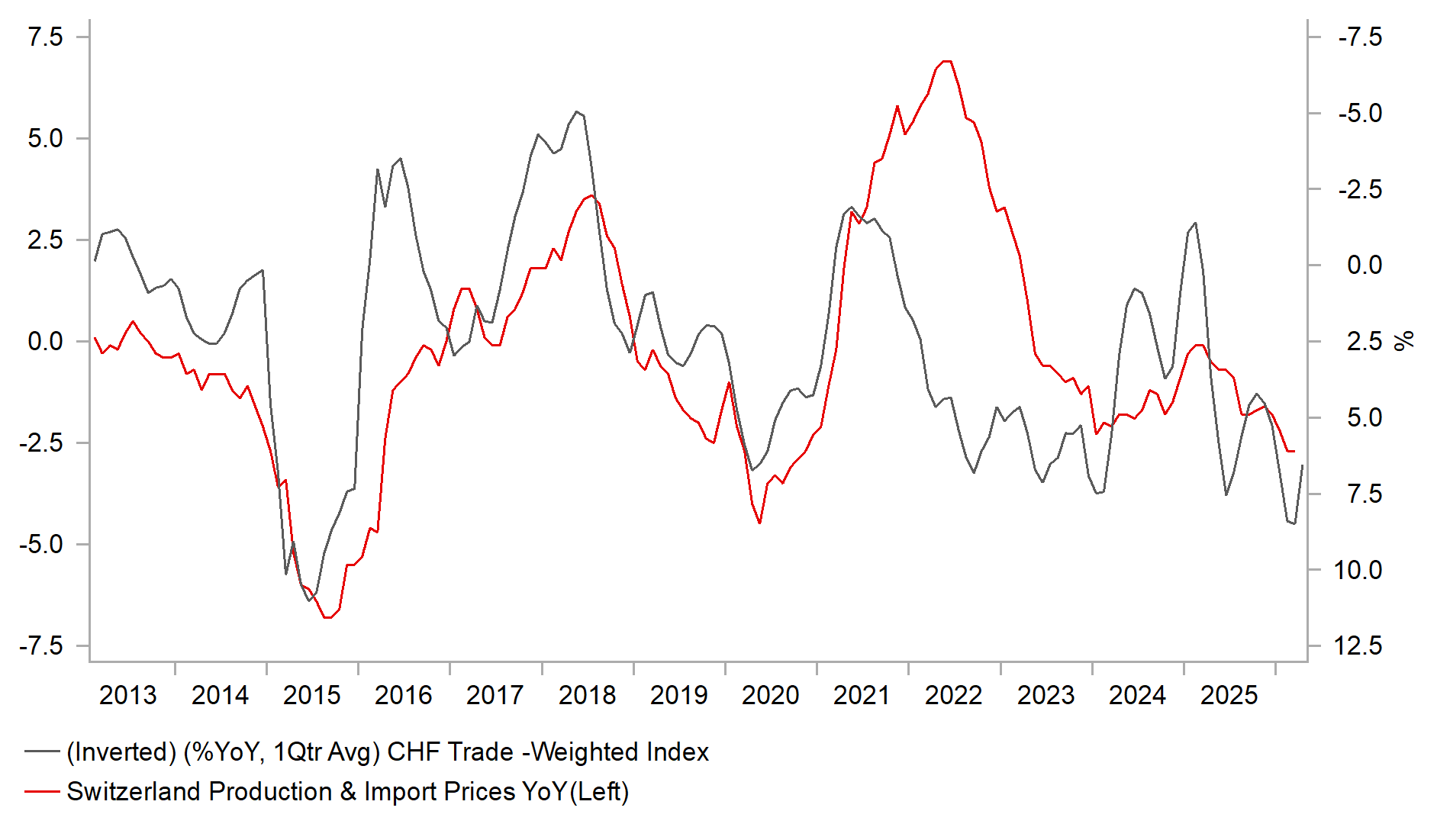

As in Sweden, inflation in Switzerland was running well below the SNB’s target before the energy price shock took hold. Initially, the SNB’s policy focus has been on the downside risks to inflation stemming from a stronger CHF, driven by safe-haven demand following the Middle East conflict. As a result, the SNB has continued to signal a much greater willingness to intervene in the FX market to weaken the currency. This timely and forceful pushback has contributed to the CHF’s underperformance since the conflict began. SNB Governor Martin Schlegel has also attempted to downplay the rise in headline inflation to 0.6% in April, up from 0.3% in March, stating that there has been “hardly any change” in medium-term price pressures. This view is, for now, supported by core inflation, which slowed to an annual rate of 0.3% in April. However, if the Strait of Hormuz remains closed for an extended period and leads to a more prolonged energy price shock, the SNB’s relatively dovish policy stance is likely to shift. This could open the door to rate hikes and a greater tolerance for a stronger CHF to contain upside inflation risks. Indeed, the Swiss rates market has already begun to price in a higher probability of an SNB rate hike by the end of this year.

NO RELIEF FOR SEK WHILE CONFLICT IS UNRESOLVED

Source: Bloomberg, Macrobond & MUFG GMR

STRONGER CHF HAS HELPED DAMPEN INFLATION

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

Ccy | Date | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

NOK | 11/05/2026 | 07:00 | CPI YoY | Apr | -- | 3.6% | !! |

USD | 11/05/2026 | 15:00 | Existing Home Sales | Apr | 4.05m | 3.98m | !! |

EUR | 12/05/2026 | 07:00 | Germany CPI YoY | Apr F | -- | 2.9% | !! |

EUR | 12/05/2026 | 10:00 | Germany ZEW Survey Expectations | May | -- | - 17.2 | !! |

AUD | 12/05/2026 | 10:30 | Australian budget | !! | |||

NOK | 12/05/2026 | 10:45 | Norway Revised 2026 Budget Published | !! | |||

USD | 12/05/2026 | 11:00 | NFIB Small Business Optimism | Apr | -- | 95.8 | !! |

USD | 12/05/2026 | 13:30 | CPI YoY | Apr | 3.8% | 3.3% | !!! |

USD | 12/05/2026 | 18:00 | Fed's Goolsbee Speaks | !! | |||

JPY | 13/05/2026 | 00:50 | Trade Balance BoP Basis | Mar | -- | ¥267.6b | !! |

EUR | 13/05/2026 | 06:30 | France ILO Unemployment Rate | 1Q | -- | 7.9% | !! |

SEK | 13/05/2026 | 07:00 | CPI YoY | Apr F | -- | -0.1% | !! |

EUR | 13/05/2026 | 07:45 | France CPI YoY | Apr F | -- | 2.2% | !! |

SEK | 13/05/2026 | 08:30 | Riksbank Publishes Minutes | !! | |||

EUR | 13/05/2026 | 10:00 | GDP SA QoQ | 1Q S | -- | 0.1% | !! |

EUR | 13/05/2026 | 10:00 | Industrial Production SA MoM | Mar | -- | 0.4% | !! |

EUR | 13/05/2026 | 10:00 | Employment QoQ | 1Q P | -- | 0.2% | !! |

USD | 13/05/2026 | 13:30 | PPI Final Demand MoM | Apr | 0.5% | 0.5% | !! |

USD | 13/05/2026 | 16:30 | Fed's Collins Speaks | !! | |||

GBP | 13/05/2026 | 18:00 | BoE's Mann Speaks | !! | |||

CAD | 13/05/2026 | 18:30 | Bank of Canada Summary of Deliberations | !!! | |||

GBP | 14/05/2026 | 00:01 | RICS House Price Balance | Apr | -- | -23.0% | !! |

GBP | 14/05/2026 | 07:00 | GDP QoQ | 1Q P | -- | 0.1% | !!! |

GBP | 14/05/2026 | 07:00 | Trade Balance GBP/Mn | Mar | -- | -£720m | !! |

USD | 14/05/2026 | 13:30 | Import Price Index MoM | Apr | -- | 0.8% | !! |

USD | 14/05/2026 | 13:30 | Initial Jobless Claims | -- | -- | !! | |

USD | 14/05/2026 | 13:30 | Retail Sales Advance MoM | Apr | 0.4% | 1.7% | !! |

GBP | 14/05/2026 | 16:15 | BoE Chief Economist Pill Speaks | !! | |||

CAD | 15/05/2026 | 13:15 | Housing Starts | Apr | 245.0k | 235.9k | !! |

USD | 15/05/2026 | 14:15 | Industrial Production MoM | Apr | 0.2% | -0.5% | !! |

Source: Bloomberg & MUFG GMR

Key Events:

Following a heavy recent schedule of G10 central bank policy updates, there are no meetings in the week ahead. As a result, market attention is likely to focus on both the latest developments in peace talks between the US and Iran, and upcoming major economic data releases. Market participants have been encouraged by media reports suggesting that the US and Iran are moving closer to a memorandum of understanding to end the war, followed by a gradual reopening of the Strait over a 30-day period. An agreement to end the war soon and reopen the Strait would represent the best-case scenario for the global economy and financial markets, helping to ease supply disruptions going forward. However, there remains a risk that negotiations could drag on as Iran seeks to secure more favourable terms as highlighted by new reports over the weekend.

One of the key economic data releases in the week ahead will be the latest US CPI report for April, alongside the US PPI and import price reports for the same month. These releases are expected to provide further evidence of the initial inflationary impact from higher energy prices. Higher energy prices had already contributed approximately 0.8 percentage points to headline inflation in March. However, it is still too early to assess second-round effects, with core measures of inflation expected to remain relatively stable. The Fed has indicated that it is willing to look through the near-term pickup in inflation but has begun to debate removing its easing bias.

The release of the latest GDP report for Q1 is expected to confirm that the UK economy performed more strongly than anticipated at the start of the year. Leading indicators also suggest that positive growth momentum has been sustained into the early part of Q2, despite the initial dampening impact of the energy price shock. At the same time, hawkish MPC members Catherine Mann and Chief Economist Huw Pill are scheduled to speak in the week ahead. Huw Pill voted for a rate hike at the April MPC meeting, while Catherine Mann has indicated that she is prepared to vote for higher rates if inflation outcomes and expectations continue to rise. The political fallout from last week’s UK local elections will also be closely monitored in the week ahead.