Renewed optimism over US-Iran deal weighs on USD

USD: US-Iran deal optimism offsets support from stronger US PPI report

The US dollar has continued to trade at modestly weaker levels overnight after yesterday’s sell-off triggered by a post from President Trump claiming that deal will signed shortly between the US and Iran to end the conflict and reopen the Strait of Hormuz. He stated that “discussions and final points have been, in both concept and great details, approved by all parties involved”, and the “timing and place of the signing to be announced shortly”. As a result, President Trump decided to cancel the scheduled strikes and bombings against Iran yesterday evening. It marked a quick turnaround in President Trump’s rhetoric after he had threatened earlier in the day to hit Iran “VERY HARD” and to take control of Kharg Island at some point soon. However, there has been no indication from Iran that a deal has been finalized. Iran’s semi-official new agency Fars stated that officials have not yet approved the text of any agreement with the US. According to Axios, the deal has been approved on the Iranian side at high levels but likely not by Supreme Leader Mojtaba Khamenei. The US-Iran memorandum of understanding President Trump claims will soon be signed would extend the ceasefire for 60 days, including in Lebanon, during which time nuclear negotiations would be held. It would reopen the Strait of Hormuz immediately without tolls. The signing ceremony could reportedly take place as early as this weekend according to President Trump. Further progress towards a deal to reopen the Strait would help to dampen upside risks for the US dollar in the near-term.

The US dollar has strengthened recently on the back of the hawkish repricing of Fed rate hike expectations. However, renewed investor optimism over a peace deal has triggered a correction lower for US yields overnight. The 2-year US Treasury yield dropped by around 9bps yesterday as market participants scaled back expectations for Fed rate hikes. The dovish repricing was encouraged by the price of Brent dropping back below USD90/barrel. The US rate market is now leaning more towards the Fed delivering one rather than two hikes in response to the energy price shock, while we continue to expect the Fed to leave rates on hold if a deal is reached soon. US inflation data released this week has provided mixed signals. Headline inflation jumped in May driven mainly by higher energy prices but there was little evidence of broadening price pressures in the latest CPI report. On the other hand, the release yesterday of the latest PPI report revealed stronger inflation pressures are building downstream. The components that feed into the Fed’s measure of inflation, the PCE deflator, were hot which has raised forecasts for the core PCE deflator in May. It has increased pressure on the Fed ahead of next week’s FOMC meeting to shift in a more hawkish direction,

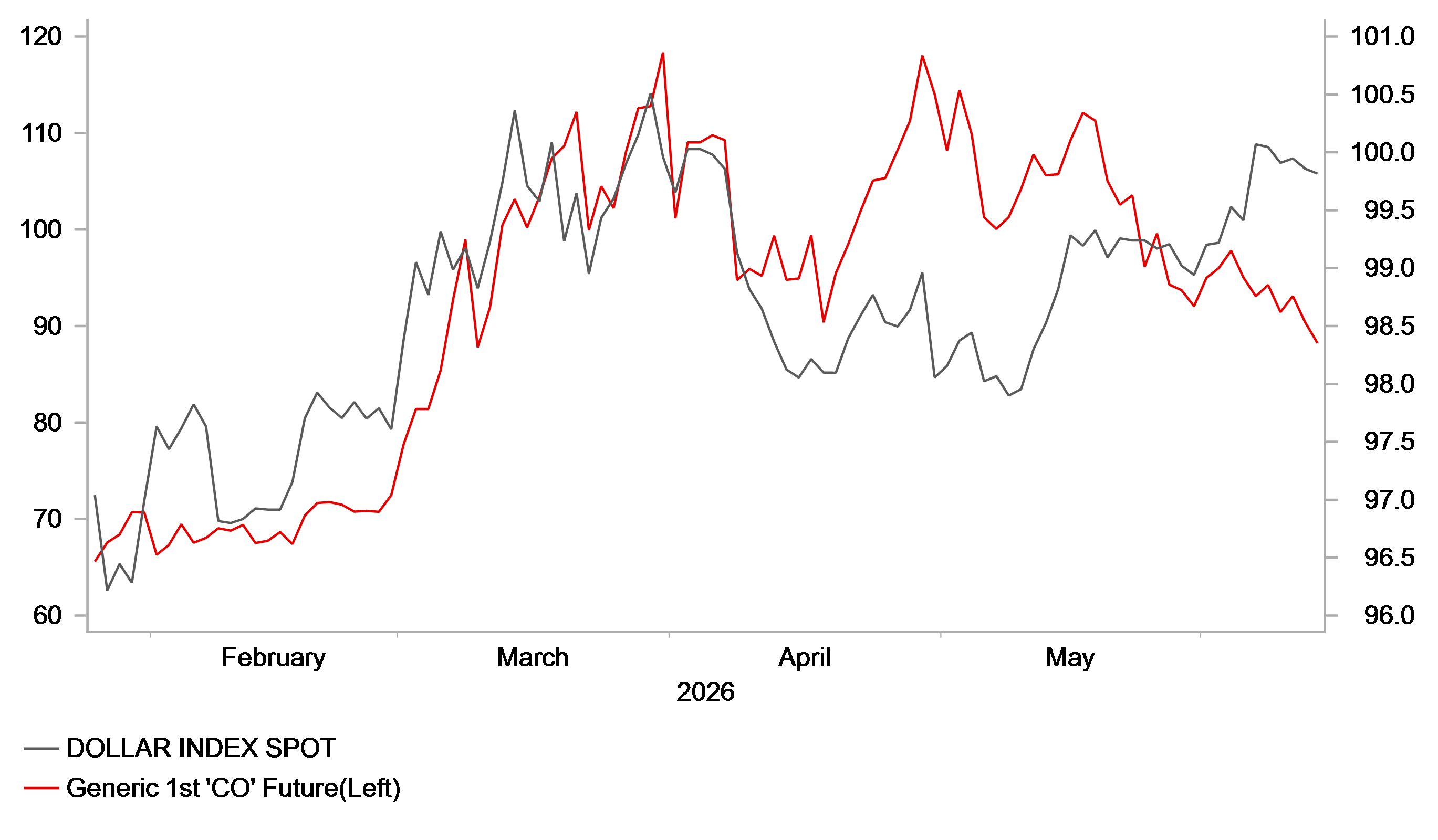

OIL PRICE CORRECTS LOWER AS USD IS CLOSE TO RECENT HIGHS

Source: Bloomberg, Macrobond & MUFG Research

EUR: ECB leaves door open to further hikes dependent on Middle East risks

Renewed US-Iran deal optimism has helped the euro to strengthen modestly against the US dollar, and lifted EUR/USD back up closer to the 1.1600-level. It marked a a reversal after the euro sold-off earlier in the day after yesterday’s ECB policy announcement. The ECB raised rates for the first time in response to the energy price shock but refrained from committing to back-to-back hikes in June and July. A Bloomberg report later in the day stated that officials aren’t ruling out a second rate hike as soon as next month according to people familiar with the situation due to concern over inflation triggered by the Iran war. But if the situation improves in the mean meantime, the ECB can still hold rates steady that month.

The probability of the ECB hiking again as soon as next month has fallen back below 50:50 encouraged as well by renewed optimism over a US-Iran deal. If the Strait of Hormuz is reopened soon it would ease pressure on the ECB to deliver further rate hikes. However, the euro-zone rate market is still leaning towards the ECB delivering two more hikes in the year ahead with the next hike fully priced by September. It provides a high hurdle for euro-zone yields to continue moving higher in the near-term unless the energy price shock intensifies. We continue to expect one more hike from the ECB this year. A deal to quickly reopen the Start of Hormuz would help to reduce downside risk for the euro and help keep EUR/USD in the current 1.1400-1.1800 trading range that has been in place over the past year. Please see our FX Focus report for more details on the ECB’s latest policy update (click here).

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

GB | 09:30 | Inflation Expectations | - | - | 3.2% | ! |

GB | 12:00 | NIESR Monthly GDP Tracker | - | - | 0.8% | !! |

CA | 13:30 | Manufacturing Sales (MoM) | (Apr) | 4.6% | 3.0% | ! |

US | 15:00 | Michigan Consumer Sentiment | (Jun) | 46.1 | 44.8 | !! |

DE | 15:30 | German Buba President Nagel Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com