Softer EUR heading into ECB policy update

USD: Softer US core inflation helps to dampen upside risks for US dollar

The major foreign exchange rates have continued to trade in narrow ranges overnight with the dollar index fluctuating around the 100.00-level. There has been little spill-over impact into the foreign exchange market from the renewed military strikes exchanged between the US and Iran in recent days. The US has carried out strikes against “multiple” targets in Iran from the second consecutive day. US Central Command has since declared the operation complete which targeted surveillance systems, air defence sites and communications networks in Iran. However, President Trump has threatened to carry out strikes again today if Iran does not sign a peace agreement according to a Fox News report. He also posted earlier in the day that the US military had supported the passage of “more than 200 commercial ships” through the Strait of Hormuz resulting in “more than 100 million barrels of oil” making it to market. Overall, the latest developments have significantly altered market expectations that the latest military conflict is likely to be contained although hopes for a quick deal to end the conflict and fully reopen the Strait of Hormuz continue to fade. The longer the Strait remains closed the higher the risk of a more disruptive outcome for the global economy and financial markets that would favour a stronger US dollar as well.

The other main development yesterday was the release of the latest US CPI report for May which provided further insight into the inflation impact from the energy price shock hitting the US economy. The report revealed that headline inflation picked up to 4.2% in May as expected mainly driven by higher energy prices. The contribution from energy to the annual rate of inflation jumped up to 1.5 percentage points in May up from 1.1 percentage points in April and 0.1 percentage points in February prior to the Middle East conflict starting. In contrast, measures of core inflation have increased only modestly so far providing reassurance that the pick-up in inflation is not yet broad-based. The positive continuing to annual headline inflation from core serves inflation has increased by around 0.2 percentage points since February and core goods inflation by around 0.1 percentage points. Admittedly, it still likely too early to see much evidence of broadening inflation pressures resulting from the energy price shock. Additionally, there was reassuring evidence that the inflation impact from last year’s tariff hikes is fading and fears over higher inflation from the AI infrastructure rollout did not materialize. Core goods inflation fell on the month for the first time this year, and PCs inflation normalized while smartphones and software prices were broadly flat. The report helps to ease some of the pressure on the Fed ahead of next week’s FOMC meeting. It has provided relief for financial markets that have moved recently to price in multiple Fed rate hikes and helps dampen upside risks for the US dollar.

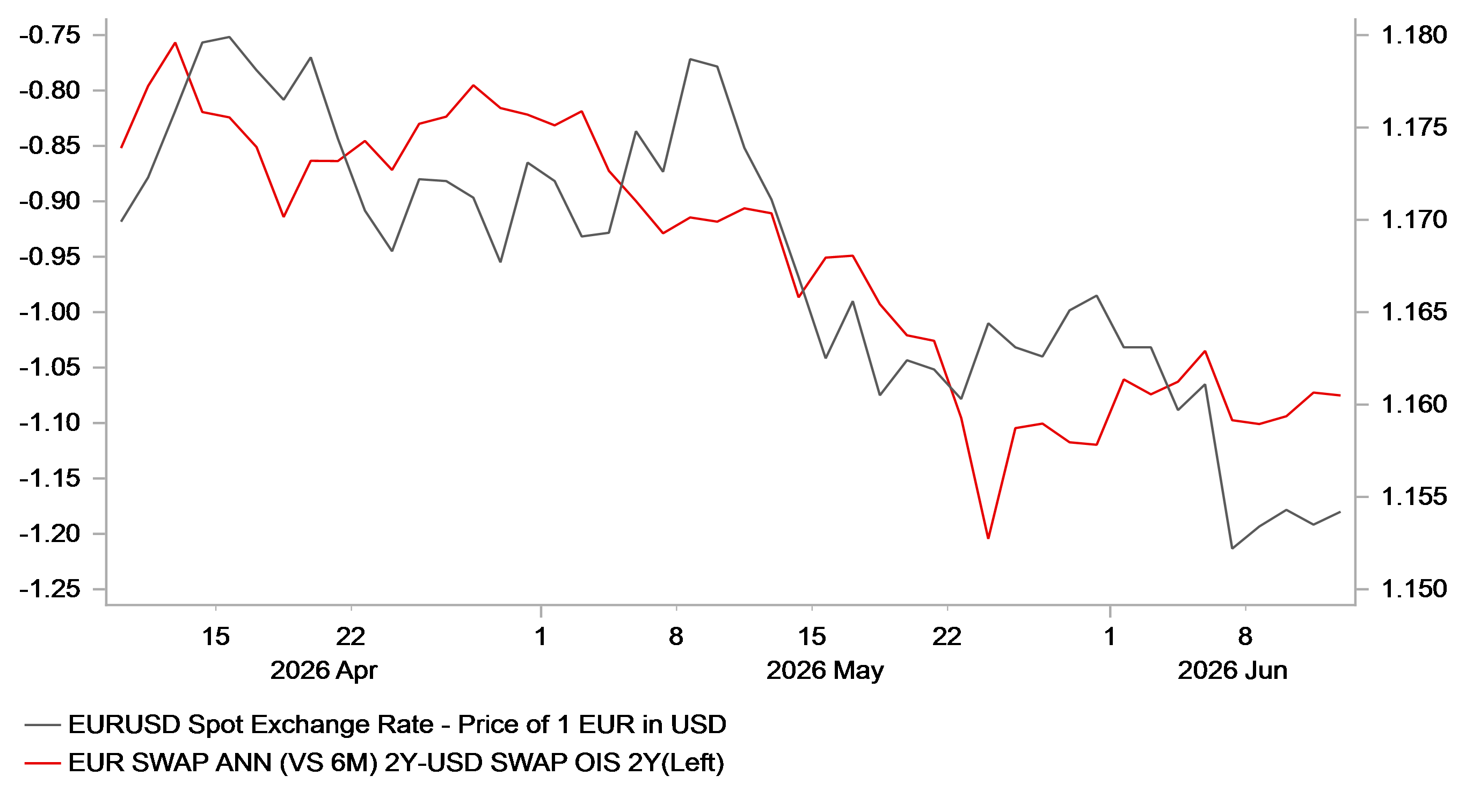

EUR/USD VS. SHORT-TERM YIELD SPREAD

Source: Bloomberg, Macrobond & MUFG Research

EUR: Will the ECB indicate it could deliver back-to-back rate hikes?

Market attention will now switch to the outlook for ECB policy today ahead of their latest policy update. Ahead of the meeting, the euro has been trading on a weaker footing with EUR/USD moving back towards the lower end of the 1.1400 to 1.1800 range that has been in place since the Middle East conflict started. EUR/USD has declined over the past month mainly driven by building expectations for tighter Fed policy. The 2-year US treasury yield has increased by almost 20 basis points over the past month compared to a more modest increase of around 7 basis points in the euro-zone. It reflects catch for US yields as market participants have become more confident that that Fed will not leave rates on hold during the energy price shock. In contrast, the euro-zone rate market had already moved to price in multiple ECB rate hikes curtailing further upside for yields in the near-term.

The euro-zone rate market is fully pricing in a 25bps rate hike form the ECB today. ECB officials have strongly signalled that they are likely to start hiking rates today supported by another upward revision to the ECB staff’s inflation forecasts. We expect President Lagarde to indicate that the outlook for the euro-zone economy is moving more in line with their adverse scenario which requires measured policy tightening. It fits with our own forecast for the ECB to deliver 50bps of hikes this year (click here). The main focus for market participants will be on the updated policy guidance given that there is currently around a 50:50 probability attached to back-to-back hikes in June and July. The euro could weaken modestly if President Lagarde does not signal that another hike is on the cards as soon as next month. It will be difficult to trigger a hawkish repricing with three rate hikes almost fully priced in for this year.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EC | 13:15 | ECB Deposit Facility Rate | Jun-26 | 2.3% | 2.0% | !! |

US | 13:30 | Initial Jobless Claims | 220k | 225k | !! | |

US | 13:30 | PPI Final Demand MoM | May | 0.7% | 1.4% | !! |

EC | 13:45 | ECB President Lagarde Holds Press Conference | !! |

Source: Bloomberg & Investing.com