Peace hopes keep US dollar under downside pressure

USD: Crude oil drops and Japan dollar selling pushes dollar weaker

The plan by the US to guide shipping vessels through the Strait of Hormuz (Project Freedom) has been abandoned before it ever really got going with President Trump citing the “Great Progress made toward a Complete and Final Agreement” with Iran that has helped to fuel renewed hopes of a peace deal to end the conflict. Brent crude oil has gapped lower this morning and is now down 6% from the peak yesterday. That has fuelled renewed US dollar selling, reinforced by the continued positive momentum in global equities. Korea’s Kospi index is up over 7% today helped by a 16% surge for Samsung and a valuation over USD 1 trillion as its semiconductor arm recorded huge profits fuelled by an incredible 48-fold jump in AI data centre orders. The AI euphoria seems fully justified and remains a key source of optimism for global growth that has played a role in supporting risk appetite and hindered gains for the US dollar.

When considering the past behaviours of the MoF / BoJ in Japan regarding intervention, there is a strong likelihood that the Japanese authorities contributed to the broad sell-off of the US dollar with another bout of USD/JPY selling intervention.

In all the past interventions, the MoF has never intervened just once. In 2022, intervention took place in September and October on a total of three separate trading days. In 2024, the MoF intervened twice at the end of April and beginning of May and then twice again in July 2024. Today, after hitting close to the 158-level, USD/JPY fell nearly three big figures and is of a scale that is consistent with actual intervention by the MoF. Finance Minister Katayama made clear on Monday that “bold action” can be taken in FX markets.

If action has been taken today, the selling of the US dollar would have been reinforced by the decline in crude oil prices and increased hope of progress toward a peace deal. But we believe there remains a danger that these bouts of intervention could prove the least successful of any of the previous periods of intervention mentioned above. The Japanese authorities are more at the mercy of unpredictable factors than in the past. How the Middle East plays out will be crucial on whether upside momentum in USD/JPY fades. While there is optimism today over progress toward peace that could change suddenly at any time.

Signs of continued China resilience have also helped undermine the dollar. The Australian and New Zealand dollars are the top performing G10 currencies today with the China PMIs stronger than expected fuelled by strong services. Ultimately whether the drop in crude oil prices can hold and progress can be made in resolving the conflict in the Middle East will determine whether the dollar selling will extend further over the short-term although other macro factors are certainly helping.

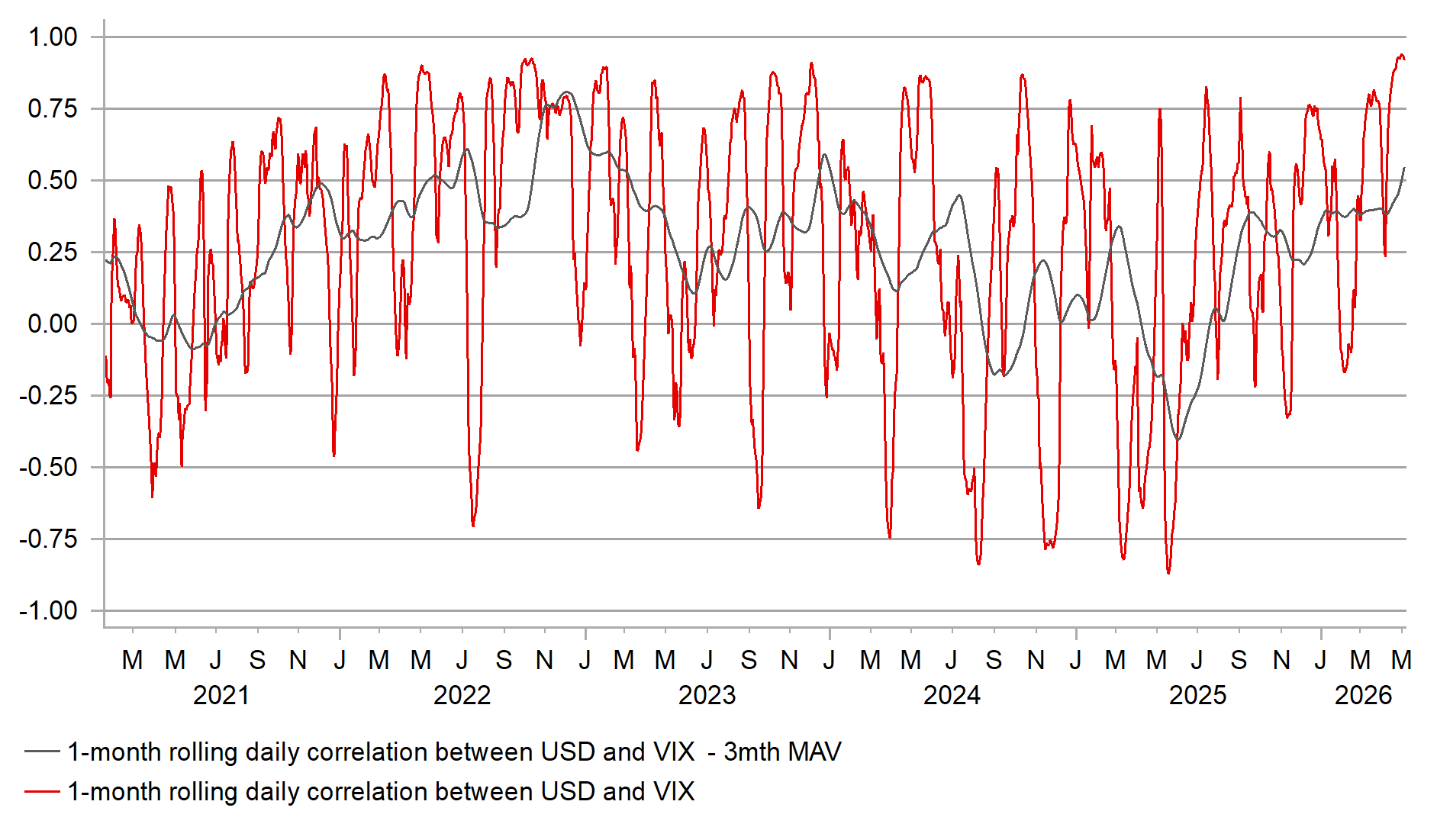

AI OPTIMISM KEEPS USD WEAK WITH USD/VIX CORRELATION NEAR RECORD

Source: Bloomberg, Macrobond & MUFG GMR

GBP: Building risks but pound shows resilience

The price action in the UK Gilt market yesterday was certainly reminiscent of previous episodes of political and fiscal uncertainties that prompted heavy bond market selling. The 10-12bp jump in Gilt yields across the curve in part reflected catch-up after yields increased on Monday when the UK markets were closed but the jump in yields yesterday was much more than the moves in Bunds or US Treasuries on Monday that pointed to further underlying reasons for the Gilt market sell-off.

Depending on where your starting point is for comparison there is some evidence that the scale of outperformance prior to the start of the conflict in the Middle East partially explains the bigger moves now. By that we mean, if you take for example say the movement in yields over the last 12mths, then the move in Gilt yields is comparable. From a year earlier, the 30-year German bund yield is up 60bps whereas the 30-year Gilt yield has risen by 43bps. The 30-year US Treasury yield is up 20bps. So the long-end of the Gilt curve has outperformed Bunds but underperformed Treasuries. But over most other longer periods, the Gilt yield moves have been larger, no doubt capturing the tumultuous period following the Brexit vote in 2016 and the political instability, fiscal concerns and inflation risks that partially came with that change. While the 30-year Bund yield is back to a yield last seen in mid-2011, the 30-year Gilt yield is around 160bps higher than mid-2011 levels.

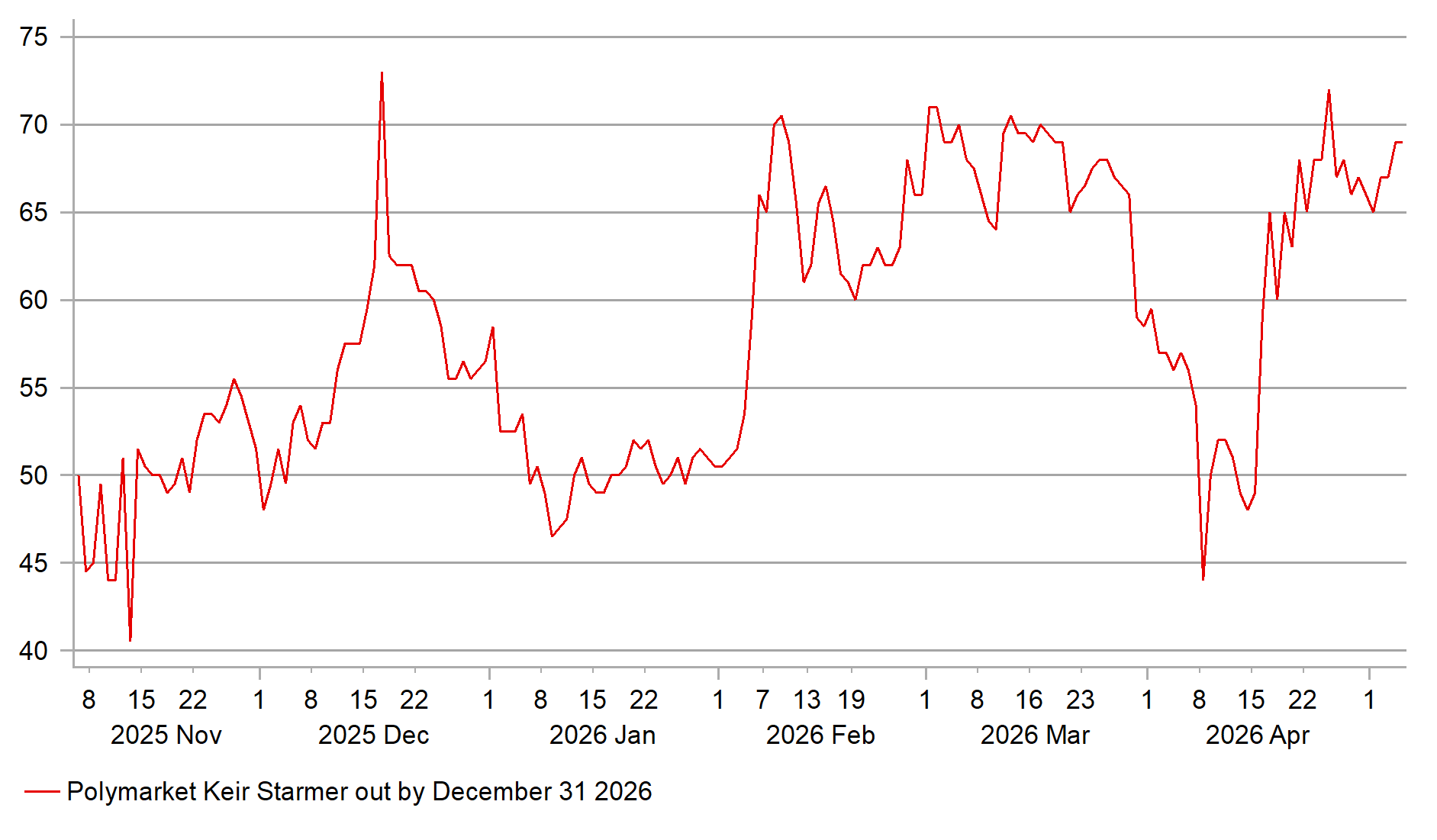

More political instability could be on its way and investors could well be positioning for the potential for renewed political instability that could follow Thursday’s local elections. We covered this topic in more detail in the latest FX Weekly (here). Polymarket shows a near 70% implied probability of PM Starmer not surviving through to the end of 2026, close to recent highs. The danger period will be from after the local elections this week (assuming Labour do as badly as widely expected) through to the Labour Party conference, scheduled for 27th-30th September. Current polling (pollcheck.co.uk) estimates Labour to lose 1,164 council seats (from 2,303); the Tories to lose 563 seats while the Lib Dems gain 121 and the Greens 456. Reform are the big winners gaining 1,401 seats. Some polls suggest Labour could do a lot worse.

So, the government is braced for large losses but at this juncture there is no obvious moves to suggest Starmer is under immediate threat. Angela Rayner remains the bookies favourite given Andy Burnham cannot run. In terms of popularity, Andy Burnham is by some distance the most popular, which may well deter any immediate attempt to remove Starmer. However, an MP stepping down at some stage could open up Burnham’s return to parliament. If the Greens and Lib Dems do better than expected that also could help reassure Labour MPs that Reforms support is not as widespread as feared. Still, uncertainties are high and in the context of potentially months of renewed political uncertainty, we continue to see increasing downside risks for the pound especially if crude oil prices rise sharply on the back of re-escalation in the Middle East.

IMPLIED PROBABILITY (POLYMARKET) OF PM STARMER BEING REMOVED FROM OFFICE BY YEAR-END

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

GE | 08:55 | German Services PMI | (Apr) | 46.9 | 50.9 | !! |

GE | 08:55 | German Composite PMI | (Apr) | 48.3 | 51.9 | !! |

EC | 09:00 | Services PMI | (Apr) | 47.4 | 50.2 | !!! |

EC | 09:00 | S&P Global Composite PMI | (Apr) | 48.6 | 50.7 | !! |

UK | 09:30 | Composite PMI | (Apr) | 52.0 | 50.3 | !! |

UK | 09:30 | Services PMI | (Apr) | 52.0 | 50.5 | !!! |

EC | 10:00 | PPI (YoY) | (Mar) | 1.6% | -3.0% | ! |

EC | 10:00 | PPI (MoM) | (Mar) | 3.3% | -0.7% | ! |

US | 12:00 | MBA Mortgage Applications (WoW) | - | - | -1.6% | ! |

US | 13:15 | ADP Nonfarm Employment Change | (Apr) | 116K | 62K | !!!! |

CA | 15:00 | Ivey PMI | (Apr) | 49.9 | 49.7 | !! |

EU | 16:30 | ECB's Lane Speaks | - | - | - | !!! |

US | 18:00 | Fed Goolsbee Speaks | - | - | - | !!! |

CA | 21:15 | BoC Gov Macklem Speaks | - | - | - | !!! |

Source: Bloomberg & Investing.com