To read the full report, please download PDF.

Assessing intervention impact amid US/Iran war

FX View:

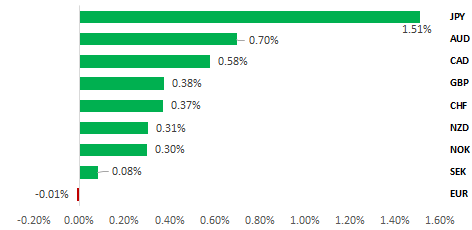

Despite probable intervention by the BoJ/MoF in Japan last Thursday to drive USD/JPY lower, the yen still ended April as the worst performing G10 currency after the US dollar and is also lagging the rest of G10 on a year-to-date basis. This week through tomorrow is the Golden Week vacation in Japan and the action last week likely reflected concern of a sharp yen sell-off during illiquid trading conditions that could have resulted in JGB market instability. We certainly doubt the action will have much lasting impact on strengthening the yen given the current fundamental backdrop, which remains conducive to a higher USD/JPY. This week UK local elections take place on Thursday with PM Starmer’s backbench support the weakest it has been since he became PM. Will he survive the expected bad result for the Labour Party and what might the implications be for the pound if we see renewed political instability in the UK over the coming months?

JPY OUTPERFORMED LAST WEEK WITH HELP FROM MOF/BOJ

Source: Bloomberg, close on 1st May 2026 (Weekly % Change vs. USD)

Trade Ideas:

We are maintaining a short GBP/CHF trade idea ahead of this week’s UK local elections.

JPY Flows:

This week we look at the JSDA super-long JGB flow data covering the latest data for March. Foreign investors remain the consistent source of demand with fifteen consecutive months of net purchases.

Price Action Analysis – UK political uncertainty:

Near‑term FX reactions are mixed, but leadership risk has tended to weigh on GBP over 1 to 3-week horizons.

FX Views

JPY: Intervention can cap USD/JPY rather than send lower

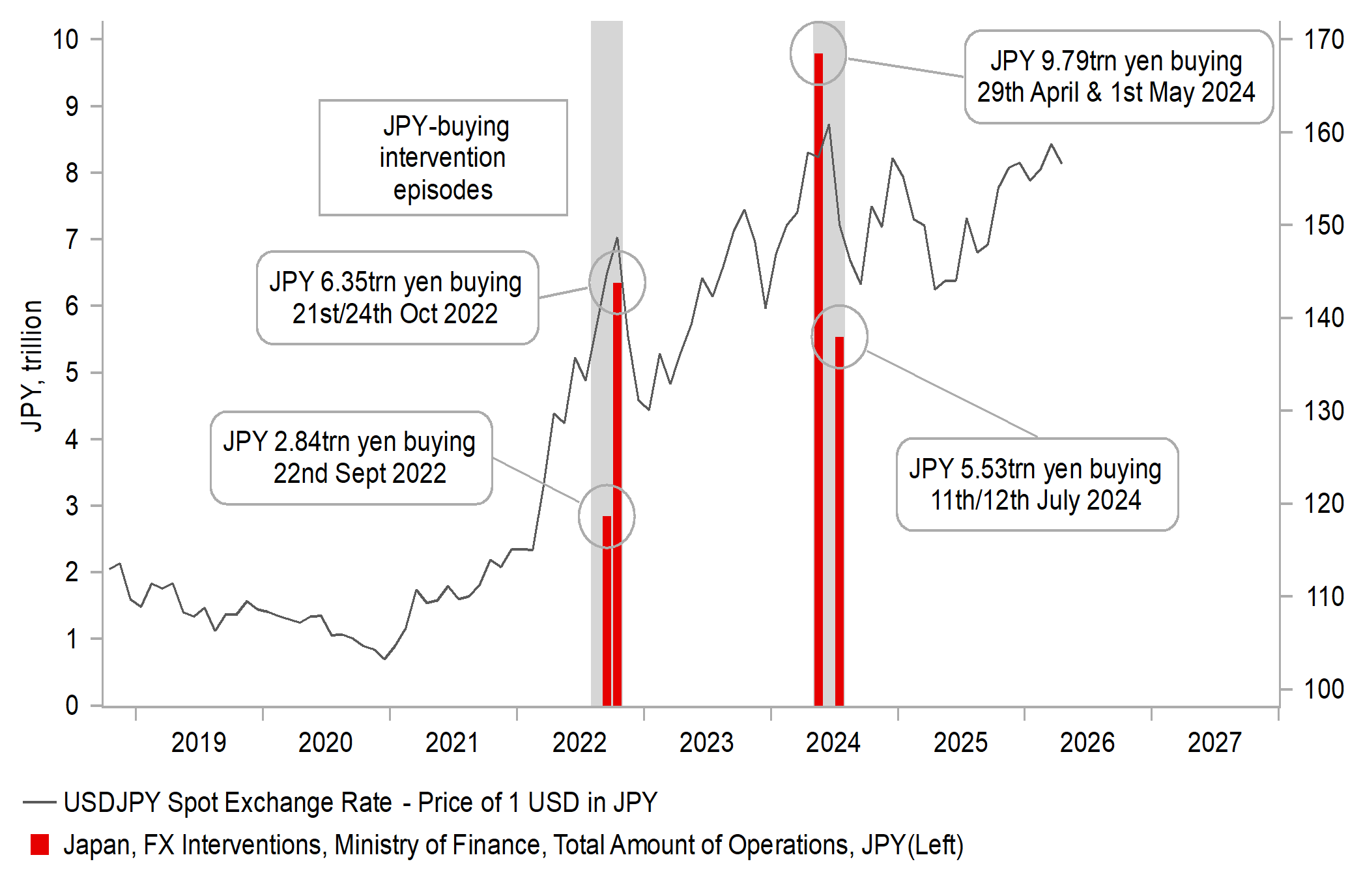

From the intra-day high to the low on Thursday last week, USD/JPY fell by about five big figures and most of that drop has been sustained. The move was highly likely to have been yen-buying intervention by the Japanese authorities after the break above the 160-level. It’s Golden Week in Japan this week with the market closed until Thursday and there was a danger of big swings in thin trading conditions if the MoF had decided to wait and risk needing to intervene this week. With another energy-price shock unfolding with USD/JPY trading around the 160-level leaves Japan in a difficult position and if this price shock was to get worse and investors were to price in Fed rate hikes along with the already priced hikes elsewhere across G10, the fundamental backdrop would strongly point to further upside momentum for USD/JPY and other crosses. With the Strait of Hormuz still closed and with risks skewed to further crude oil price rises the chance are that we will see either a renewed rise in USD/JPY quickly back to the intervention levels from last week or additional bouts of intervention over the coming days. ‘Successful’ intervention that sees a more sustained period of yen strength can likely only materialise in circumstances of de-escalation in the Middle East, the re-opening of the Strait of Hormuz and bigger declines in crude oil prices.

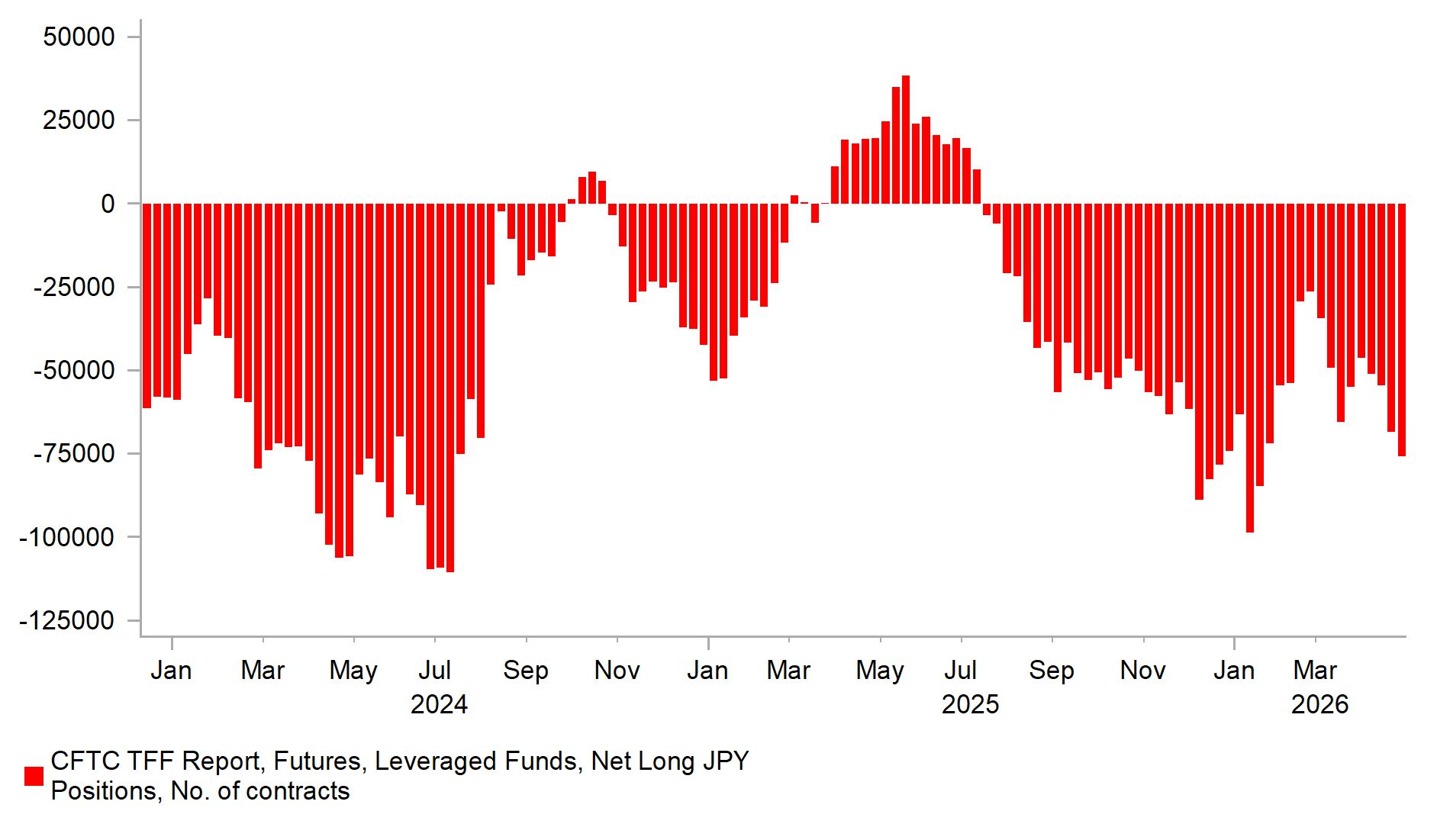

The IMM data to last Tuesday, released on Friday evening indicated a further pick-up in speculative yen selling. Leveraged Funds’ short yen positions have increased for four consecutive weeks reaching the largest since mid-January prior to the sharp drop when the Fed reportedly checked rates. With Asset Managers & Institutional Investors also selling yen, the total short position hit the largest since the last time the MoF/BoJ intervened in July 2024. OTC retail margin selling of the yen has also picked up with total short yen positions versus all currencies the largest since that same period – July 2024. While the largest since then, the short yen positions today are not as large and hence the follow-through yen buying now may be a lot less. The reports of escalation in the Middle East could certainly dilute the impact of the MoF’s intervention, especially if front-end yields in the US move further higher. It certainly seems unlikely that the broader macro backdrop after this intervention is going to turn favourable for the MoF in reinforcing US dollar selling momentum unless there is an extreme risk-off and sharp equity market declines that fuels Fed rate cut pricing.

There have been four periods of yen-buying intervention previously – (Sept 2022; Oct 2022; Apr/May 2024; and Jul 2024) with sharp declines in USD/JPY that soon followed the 2022 and Jul 2024 episodes. The intervention last week looks more likely to be like Apr/May 2024 when the fundamental backdrop resulted in limited decline in USD/JPY.

YEN BUYING INTERVENTION IMPACTS FADES OVER TIME

Source: Bloomberg, Macrobond & MUFG GMR

INCREASED SPECULATIVE YEN SELLING

Source: Bloomberg, Macrobond & MUFG GMR

GBP: Will UK local elections threaten recent GBP stability?

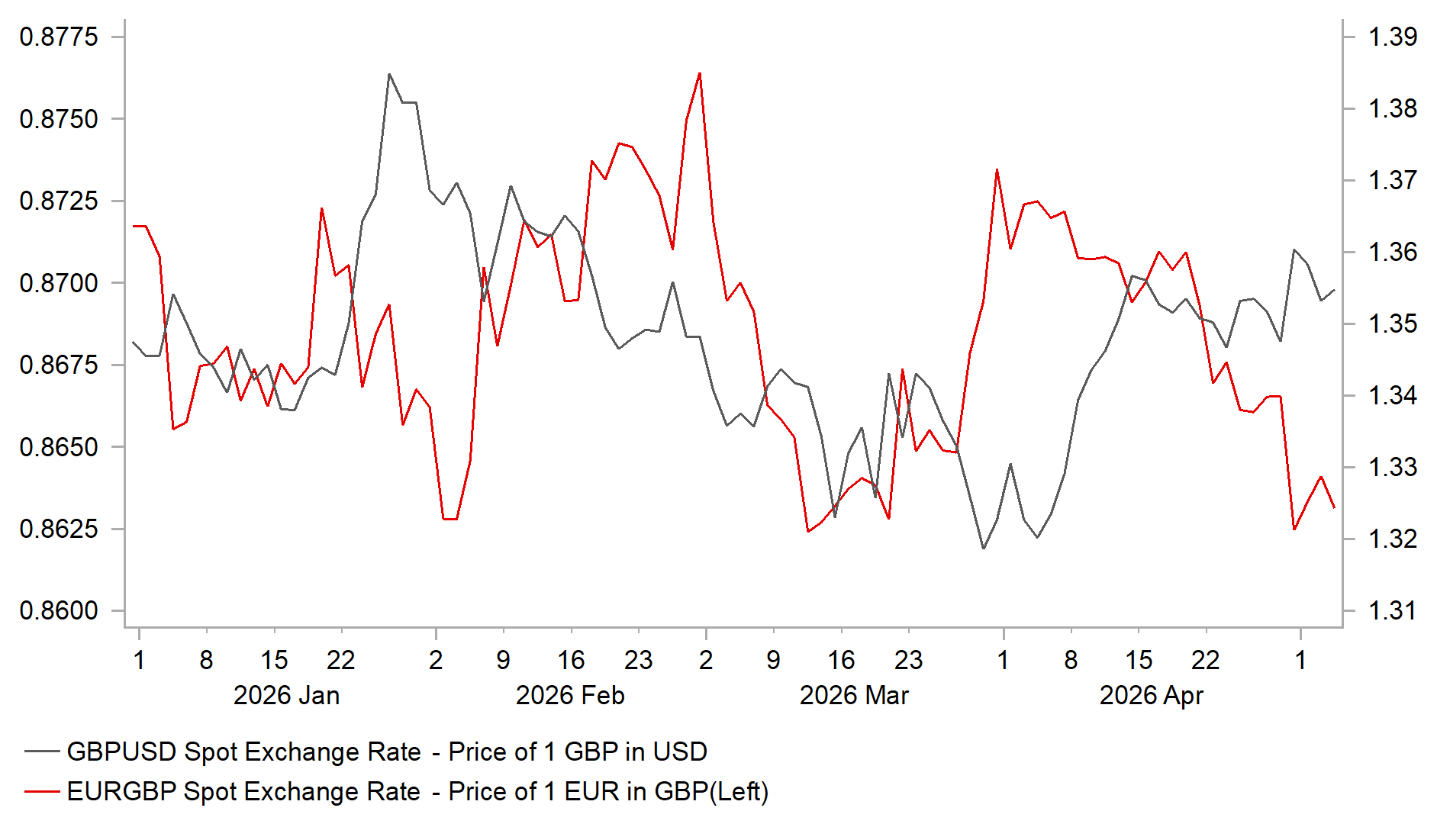

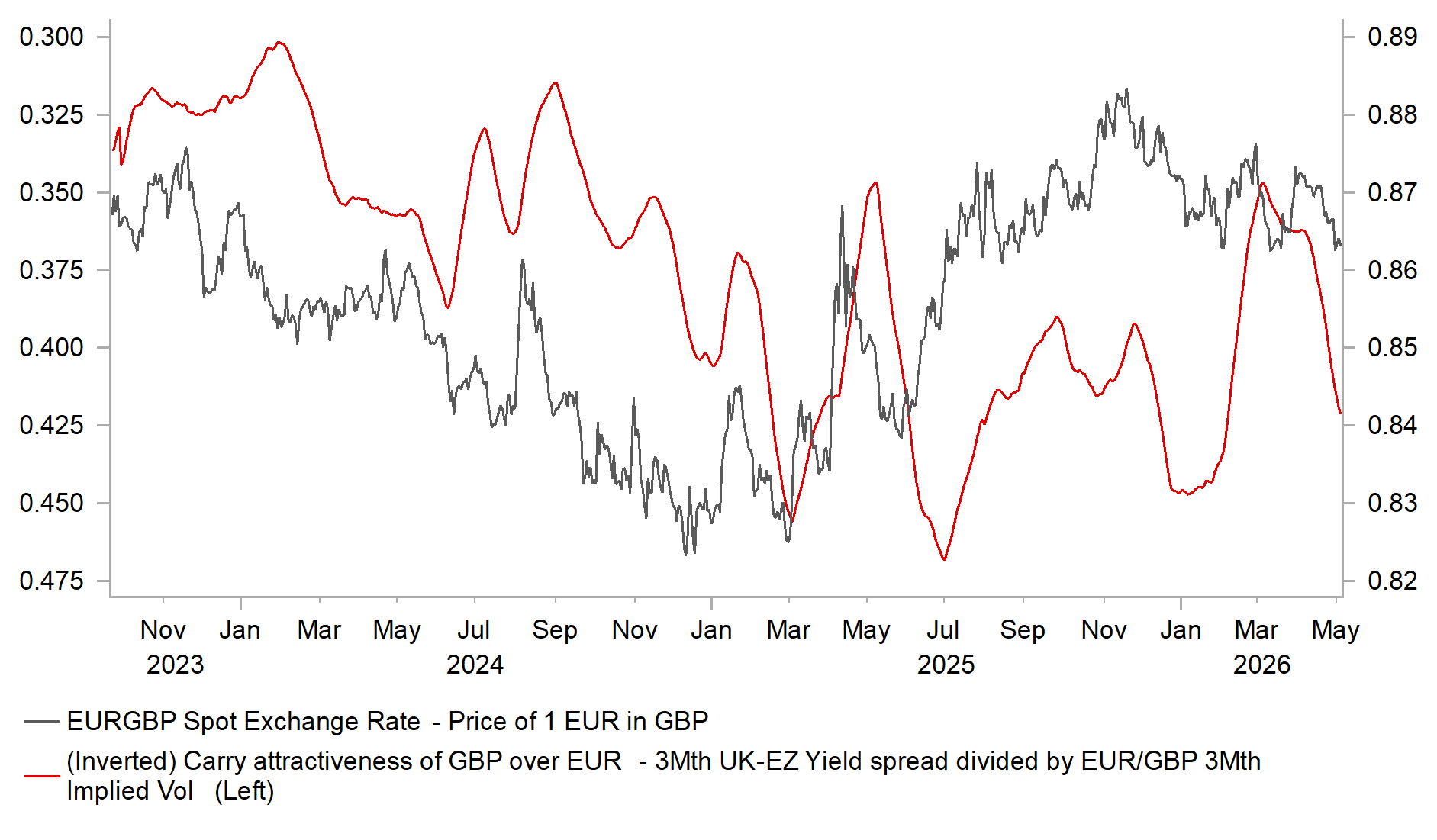

The GBP has continued to trade within narrow ranges against the major currencies of the EUR and USD over the past week. Cable reached a high of 1.3658 on 1st May but has since slipped back towards the 1.3500 level. At the same time, EUR/GBP has continued to grind lower, moving back towards support near recent lows just above 0.8600. Last week’s Bank of England policy update failed to provide a fresh catalyst for near‑term GBP direction. While UK rate markets have scaled back expectations for near‑term BoE rate hikes following the latest policy communication, this adjustment has not translated into a weaker GBP. Markets are assigning just over a 50:50 probability to a rate hike in June, down from around 80% ahead of last week’s MPC meeting. For 2026 as a whole, however, around three rate hikes remain priced in.

Governor Bailey described the initial market response to the Bank’s policy update as “very sensible”, implying satisfaction with current market pricing. This was pricing he had earlier encouraged by stating that the BoE was not sending a “clandestine message” that interest rates would rise. He also noted that much of the required policy tightening had already been delivered via tighter financial conditions. The upward shift in market expectations for interest rates has tightened financial conditions, helping to contain inflation pressures without the immediate need for further rate hikes. The BoE highlighted that the market‑implied path for Bank Rate has shifted higher by around 55bp on average over the next three years. This would offset much of the required tightening under scenarios A and B, where the Bank’s models and rules suggest between 0–75bp of tightening is needed. Scenario C, however, would still require a more forceful response of around 50–150bp. In our updated forecasts, we expect the BoE to validate the hawkish shift in market expectations and follow through with around 50bp of rate hikes, assuming the worst‑case Scenario C is avoided. We expect the BoE and the ECB to deliver a similar amount of tightening, contributing to a more stable EUR/GBP range between 0.8600 and 0.8800. EUR/GBP may test the lower end of this range if financial market volatility remains low and supportive of GBP carry demand.

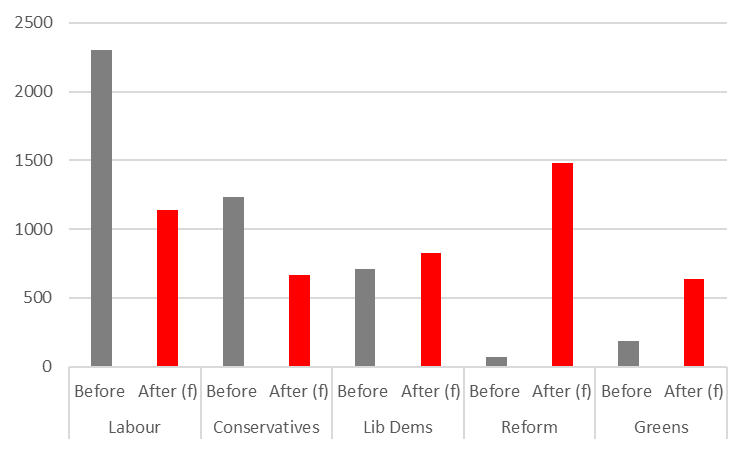

Domestic UK politics is one potential trigger for a pick‑up in near‑term GBP volatility, alongside ongoing developments in the Middle East. UK local elections are scheduled for Thursday 7th May, with more than 5,000 council seats being contested across 136 local authorities in England. Elections are also being held on the same day for the Scottish Parliament, the Welsh Senedd and six directly elected mayors in England. These local elections may attract more market attention than usual given Prime Minister Keir Starmer’s precarious political position. The Labour Party is expected to suffer significant losses, with polling experts forecasting that it could lose 50–75% of the seats it is defending (around 1,500–1,900 councillors). This could mark Labour’s worst‑ever local election performance in vote‑share terms. Such disappointing results, if confirmed, would heap further pressure on Prime Minister Starmer, whose net approval rating remains deeply negative at around ‑40 to ‑45, making him one of the least popular UK prime ministers at this stage of the political cycle. While the sharp downward momentum in his ratings has eased slightly, his leadership remains vulnerable to a poor set of local election results.

GBP HAS BEEN TRADING IN TIGHT RANGES

Source: Bloomberg, Macrobond & MUFG GMR

FAVOURABLE CARRY CONDITIONS SUPPORT GBP

Source: Bloomberg, Macrobond & MUFG GMR

We see a number of potential scenarios following the local elections. In the first scenario, the Labour Party suffers heavy losses of around 1,200–1,500 councillors. Reform UK and the Green Party make significant gains, but Labour remains broadly competitive at the national level. Prime Minister Starmer moves quickly to acknowledge the “difficult results” and signals a policy reset. He survives as Prime Minister, but with his authority diminished. In this scenario, Labour MPs prioritise leadership stability and there is no obvious successor able to command sufficient support within the party. The response is largely contained to a cabinet reshuffle. As a result, the local elections would have only a limited impact on the gilt market and GBP. We view this outcome as the current base‑case scenario. Polymarket is currently assigning around a 40% probability to Starmer losing his position by June, rising to around 68% by December.

However, if the Labour Party were to suffer even larger losses of around 1,700–2,000 councillors including the loss of major councils in London and the North, Prime Minister Starmer would find it much harder to survive beyond the short term. Such an outcome could trigger a leadership challenge, requiring the backing of at least 20% of Labour MPs (81 MPs). In this scenario, Prime Minister Starmer could choose to announce that he will step aside once a successor is selected, or a formal leadership contest could be initiated. A new leader could potentially be in place by the Labour Party’s annual conference in late September. The main potential leadership challengers include Health Secretary Wes Streeting, former Deputy Prime Minister Angela Rayner, and Greater Manchester Mayor Andy Burnham, although Burnham would first need to return to Parliament in order to participate in a leadership contest. Gilt yields and GBP would likely react more negatively if heightened political uncertainty were accompanied by increased fiscal risks, particularly in the event that Labour were to shift towards a more left‑leaning leader such as Rayner or Burnham. Looking at current FX options market pricing, market participants do not appear overly concerned about immediate downside risks for GBP ahead of the local elections. This aligns with our base‑case view that Prime Minister Starmer is likely to suffer political damage but ultimately struggle on as leader, thereby limiting the near‑term negative fallout for gilts and GBP. Nevertheless, poor local election results combined with Starmer’s continued low approval ratings would be likely to sustain speculation over his longer‑term future.

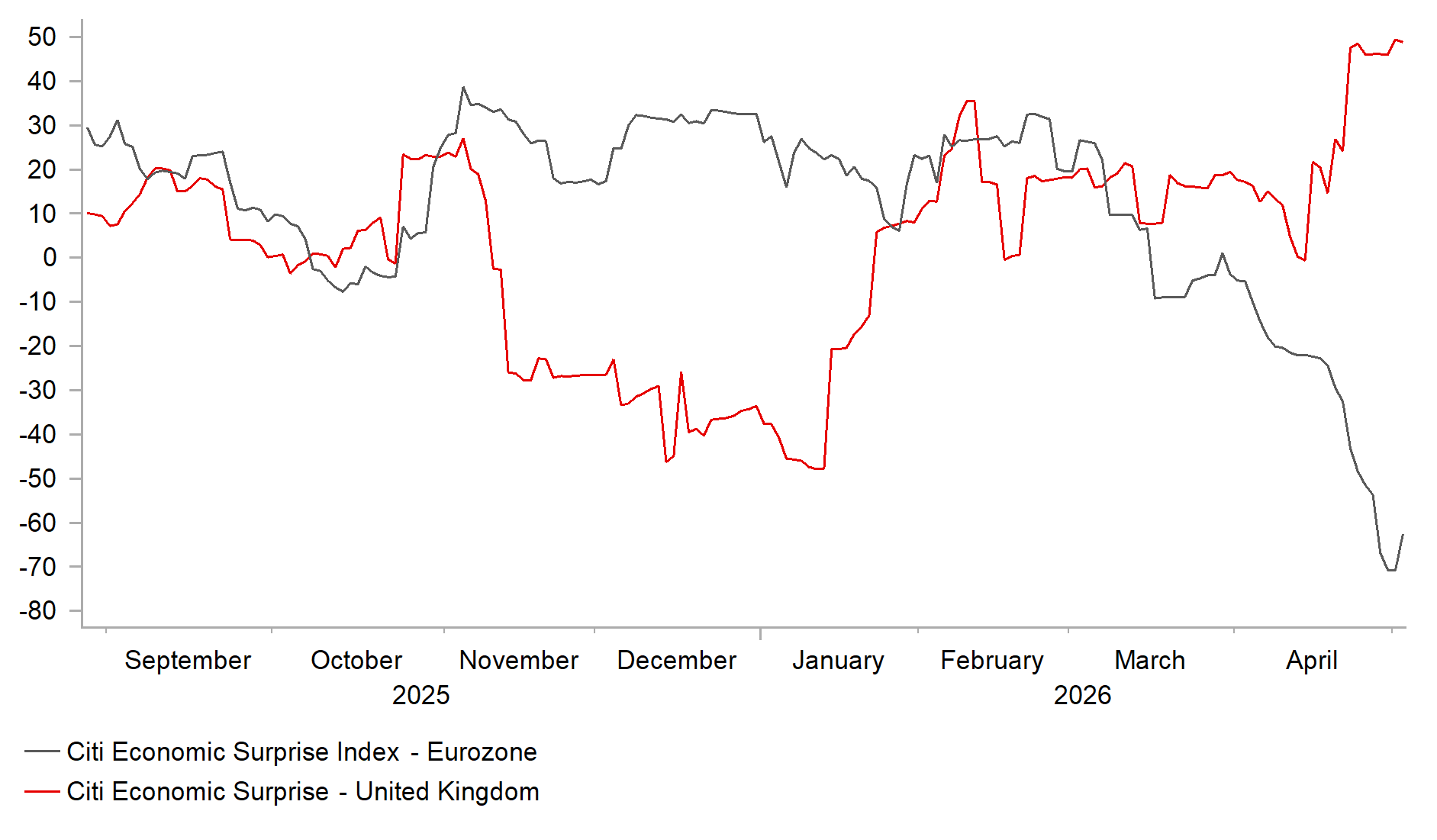

POSITIVE UK CYCLICAL MOMENTUM BOOST GBP

Source: Bloomberg, Macrobond & MUFG GMR

LABOUR FACING BIG LOSSES IN LOCAL ELECTIONS

Source: PollCheck

Weekly Calendar

Ccy | Date | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

USD | 05/05/2026 | 13:30 | Trade Balance | Mar | -$59.7b | -$57.3b | !! |

CAD | 05/05/2026 | 13:30 | Int'l Merchandise Trade | Mar | -1.97b | -5.74b | !! |

USD | 05/05/2026 | 15:00 | ISM Services Index | Apr | 53.7 | 54.0 | !! |

USD | 05/05/2026 | 15:00 | New Home Sales | Mar | 668k | -- | !! |

USD | 05/05/2026 | 15:00 | JOLTS Job Openings | Mar | 6803k | 6882k | !! |

EUR | 05/05/2026 | 16:40 | ECB's Lane Speaks | !! | |||

NZD | 05/05/2026 | 23:45 | Employment Change QoQ | 1Q | 0.3% | 0.5% | !! |

SEK | 06/05/2026 | 07:00 | CPI YoY | Apr P | 0.3% | 0.5% | !! |

EUR | 06/05/2026 | 09:00 | ECB Wage Tracker | !! | |||

EUR | 06/05/2026 | 09:00 | S&P Global Eurozone Services PMI | Apr F | 47.4 | 47.4 | !! |

GBP | 06/05/2026 | 09:30 | S&P Global UK Services PMI | Apr F | 52.0 | 52.0 | !! |

USD | 06/05/2026 | 13:15 | ADP Employment Change | Apr | 70k | 62k | !! |

USD | 06/05/2026 | 13:30 | Treasury Quarterly Refunding Announcement | !! | |||

USD | 06/05/2026 | 18:00 | Fed's Goolsbee Speaks | !! | |||

GBP | 07/05/2026 | 00:00 | UK Local Elections | !!! | |||

EUR | 07/05/2026 | 07:00 | Germany Factory Orders MoM | Mar | 1.0% | 0.9% | !! |

EUR | 07/05/2026 | 08:15 | ECB's Villeroy Speaks | !! | |||

SEK | 07/05/2026 | 08:30 | Riksbank Policy Rate | 1.75% | 1.75% | !!! | |

NOK | 07/05/2026 | 09:00 | Deposit Rates | 4.00% | 4.00% | !!! | |

EUR | 07/05/2026 | 10:00 | Retail Sales MoM | Mar | -0.4% | -0.2% | !! |

USD | 07/05/2026 | 13:30 | Nonfarm Productivity | 1Q P | -- | 1.80% | !! |

EUR | 07/05/2026 | 18:00 | ECB's Schnabel Speaks | !! | |||

USD | 07/05/2026 | 19:05 | Fed's Hammack Speaks | !! | |||

USD | 07/05/2026 | 20:30 | Fed's William Speaks | !! | |||

JPY | 08/05/2026 | 00:30 | Labor Cash Earnings YoY | Mar | 3.2% | 3.3% | !! |

EUR | 08/05/2026 | 07:00 | Germany Trade Balance SA | Mar | -- | 19.8b | !! |

EUR | 08/05/2026 | 07:00 | Germany Industrial Production SA MoM | Mar | 0.3% | -0.3% | !! |

USD | 08/05/2026 | 13:30 | Change in Nonfarm Payrolls | Apr | 60k | 178k | !!! |

USD | 08/05/2026 | 15:00 | U. of Mich. Sentiment | May P | 49.3 | 49.8 | !! |

Source: Bloomberg & MUFG GMR

Key Events:

Local elections will take place in the UK on Thursday. The results are likely to attract more market attention than usual given Prime Minister Starmer’s currently precarious position. The Labour Party is widely expected to perform poorly, with multiple pollsters predicting losses of between 1,500 and 1,900 councillors nationwide. This would equate to losing around 50–75% of the seats the party is defending. Such an outcome would significantly increase pressure on Prime Minister Starmer and could encourage a leadership challenge. Some commentators have even speculated that he might choose to step down.

The main economic data release in the week ahead will be the April nonfarm payrolls report. Private payroll growth has been volatile at the start of the year, adding to uncertainty about the health of the US labour market. However, looking through the monthly volatility, the three‑month average of private payroll growth picked up to 79k per month in Q1, a notable improvement from 26k per month in Q4. This has made the Federal Reserve more confident that the labour market is stabilising. Another strong employment report could encourage FOMC participants to drop their easing bias at the next policy meeting.

The Scandinavian central banks of the Norges Bank and the Riksbank are scheduled to provide policy updates in the week ahead. At its last policy meeting, the Norges Bank indicated that a policy rate increase would be needed at one of the forthcoming meetings. It is currently planning to raise rates by 25–50bp this year, although it remains unclear whether the hike will come this week or be delayed until June. On balance, we expect the Norges Bank to follow through on last month’s guidance and raise rates this week. By contrast, the Riksbank does not appear to be in a hurry to tighten policy in response to the energy price shock. Weaker-than-expected inflation at the start of the year has given the Riksbank more time to assess how the economy is being affected. We therefore expect the Riksbank to leave interest rates unchanged this week.