Yen rebound proves short-lived keeping pressure on Japanese policymakers

JPY: Japan policy concerns continue to weigh on yen & JGBs

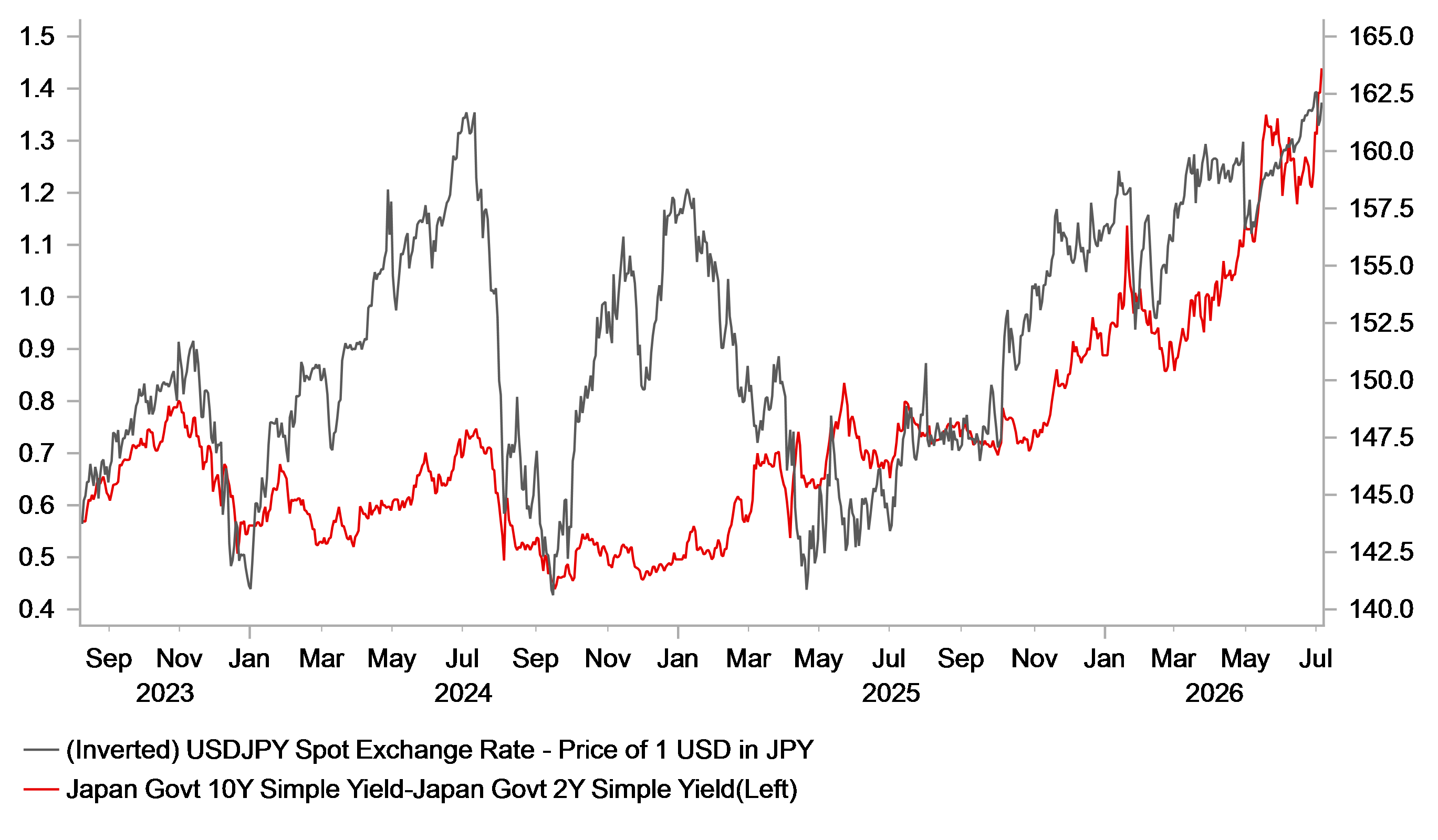

The yen has re-weakened at the start of this week resulting in USD/JPY rising back above 162.00 after hitting a low of 160.49 on Friday. There had been speculation at the end of last week that Japan could intervene again to support the yen during the US holiday when trading conditions were less liquid, but no action has been taken contributing to the yen giving back some its recent gains. Yen weakness overnight has coincided with further selling at the long end of the JGB market. The 10-year JGB yield has risen to a fresh year-to-date high of 2.83% after breaking above the high from 20th April. At the ultra-long-end the 30-year JGB is currently on track to close higher for the fifth consecutive day. The ongoing steepening of the Japanese yield curve stands in contrast to flatter curves in the US, UK and Germany. The combination of the weaker yen and rising long-term JGB yields reflects some renewed fiscal concerns in Japan, and concerns that the BoJ remains behind the curve in tightening monetary policy.

As we highlighted in our latest FX Weekly report (click here) the BoJ’s cautious approach is helping to fuel the perception of a government strategy to lower Japan’s debt burden through inflation, or that the BoJ is being constrained by fears over the burden of higher rates on servicing that debt, so called “fiscal dominance”. Higher inflation has been helping to boost nominal GDP growth which has lowered the ratio of debt to GDP. According to the IMF’s latest fiscal monitor, net debt in Japan as a % of GDP peaked at around 161% in 2020 and fell to around 137% in 2025. The IMF is currently forecasting that it will continue to fall towards 123% of GDP by 2031. Inflation in Japan is expected to accelerate through the 2H of this year and into next year. It will keep pressure on the BoJ to normalize monetary policy further.

We currently believe that the Japanese rate market is underpriced for further BoJ tightening. The BoJ’s recent communication has more clearly flagged upside risks to inflation including the faster pace of rising costs passing through to higher prices. We believe that the BoJ will increasingly take that policy needs to be tightened again sooner to address upside inflation risks. We now expect the policy rate to reach 1.50% by January 2027 with the next hike in September. There are currently only around 6bps of hikes priced in by September leaving room for short-term yields to keep moving higher. A faster pace of hikes could also help to address concerns over fiscal dominance flattening the JGB cure while providing more support for the yen. At the same time, the government also needs to clarify with detailed information what the fiscal implications will be of Prime Minister Takaichi’s ‘Technology Growth Strategy’ that targets JPY 370 trillion of investments over a 14-15 year period through most private sources. But what will be the public contribution? Ensuring that is kept to a minimum (estimated JPY 1 trillion per year) will be important for JGB sentiment which in turn for the yen.

STEEPER JGB YIELD CURVE & WEAKER JPY

Source: Bloomberg, Macrobond & MUFG Research

EUR: Euro area economy is proving more resilient than feared

EUR/USD is trading just above the 1.1400-level at the start of this week after one failed attempt break below on sustained basis at the end of last month. The pair is currently testing the bottom of the 1.1400-1.1800 trading range that has been in place over the past year. The euro has come more selling pressure in recent months driven by the initial negative impact of the energy price shock on investor sentiment towards Europe and, more recently, the scaling back of ECB rate hike expectations. Economic data releases from the euro area significantly undershot expectations in the first two-three months of the conflict. However, there have been some encouraging signs recently that the worst of the negative shock could be over with business confidence starting to rebound. The final composite reading rose back up to the 50.0-level in June from the low point of 48.5 in May. There is room for further improvement in the coming months given prior to the to the US-Iran conflict it was closer to the 52.0-level in February.

At the same time, it was revealed at the end of last week that the euro area economy appears to be holding up better than feared in Q2 as well. The stronger-than-expected industrial production data from France and Spain for May, together with notable upward revisions to the April figures, have prompted our European economist to revise higher his forecast for euro-area GDP growth in Q2 to 0.25%, up from a previous expectation of near-stagnation. The resilience of the euro area economy is a supportive development for the euro and should help to limit further selling pressure. In addition, a faster-than-expected reversal of the energy price shock should improve investor sentiment towards both the euro area economy and the euro over the remainder of this year. We expect improving cyclical momentum in the euro area to encourage EUR/USD to rebound back towards the top of the 1.1400-1800 trading range. We are also assuming still that the ECB will follow through and hike rates one final time in September even though upside inflation risks have eased significantly. While one final hike is far from a done deal, ECB officials including Chief Economist Philip Lane have continued to indicate that another 25bps remains on the cards.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

GB | 09:30 | Construction PMI | (Jun) | 40.1 | 38.2 | !!! |

EU | 09:30 | Sentix Investor Confidence | (Jul) | -14.5 | -13.4 | ! |

EU | 10:00 | PPI (YoY) | (May) | 5.7% | 4.9% | ! |

EU | 10:00 | Retail Sales (MoM) | (May) | 0.2% | -0.4% | ! |

US | 14:45 | Services PMI | (Jun) | 51.3 | 50.7 | !!! |

US | 15:00 | ISM Non-Manufacturing PMI | (Jun) | 54.2 | 54.5 | !!! |

CA | 15:30 | BoC Business Outlook Survey | - | - | - | !! |

EU | 16:00 | ECB's Schnabel Speaks | - | - | - | !! |

US | 16:00 | Fed Waller Speaks | - | - | - | !! |

EU | 17:00 | ECB President Lagarde Speaks | - | - | - | !! |

GB | 17:45 | BoE MPC Member Mann | - | - | - | !! |

EU | 19:30 | ECB's Lane Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com