To read the full report, please download PDF.

USD upside risks curtailed for now

FX View:

The US jobs report yesterday has altered the near-term risks and the turn in US momentum looks set to be maintained. There are limited event-risks next week with the next key events on 14th July – the US CPI data release and the first semi-annual testimony by Fed Chair Warsh. Weaker employment and further signs of disinflation will likely see the markets continue to pare Fed rate hike expectations reinforcing the turn in momentum back to a weaker dollar. That should mean better support at current levels for EUR/USD and it should buy the MoF in Japan further time without having to intervene to sell USD/JPY. We expect the BoJ to turn more hawkish and for the markets to increase pricing for a rate hike by September, which is currently only a 20% probability. Inflation is set to increase in Japan and the BoJ needs to do more to counter a renewed decline in short-end yields in real terms. Inflation is also set to rise in the euro-zone as well which will give credence to the view of a further rate hike from the ECB. With Fed rate hike pricing to decline, an extension of this renewed dollar weakness is most likely.

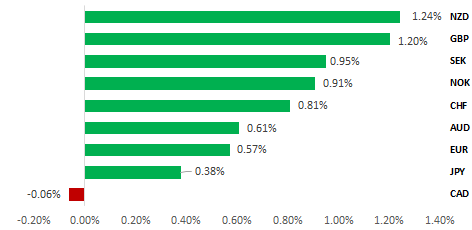

BROAD-BASED USD SELL-OFF FOLLOWING WEAK PAYROLLS REPORT

Source: Bloomberg, close on 14:00 BST on 3rd July 2026 (Weekly % Change vs. USD)

Trade Ideas:

We are closing our long USD/NOK trade idea after the USD lost upward momentum.

JPY Flows:

This week we analyse the Balance of Payments data. The latest data indicated a new record surplus when trade and investment income is combined. Japan managed to avoid any widening of its energy deficit

Historical Trading Range Breakouts for USD

Last month’s hawkish FOMC debut for new Fed Chair Kevin Warsh triggered a bullish breakout for DXY. We analyse whether the bullish breakout is likely to be sustained based on historical price action, and how far the bullish momentum could extend.

FX Views

JPY: BoJ to turn more pro-active

USD/JPY first broke through the previous high of 161.95 on Monday and that led to a new intra-day high of 162.84 being set on Wednesday – the highest level since 1986. Markets were jittery yesterday with risks of intervention by the MoF obviously high. USD/JPY corrected lower into payrolls yesterday and the weaker data led to a further extension lower. We cannot confirm if intervention took place but based on passed price action, the move this week was much more modest and hence not consistent with past episodes of intervention. Past confirmed interventions have tended to move USD/JPY lower by at least 4-5 big figures. Yesterday’s move was less than this and the drop was helped by the broad sell-off of the dollar. Nonetheless, focus on the BoJ has intensified as the FX move highlights once again the caution of the BoJ and the concerns that the BoJ monetary stance is being influenced by the desire of the Takaichi government to keep monetary tightening to a minimum.

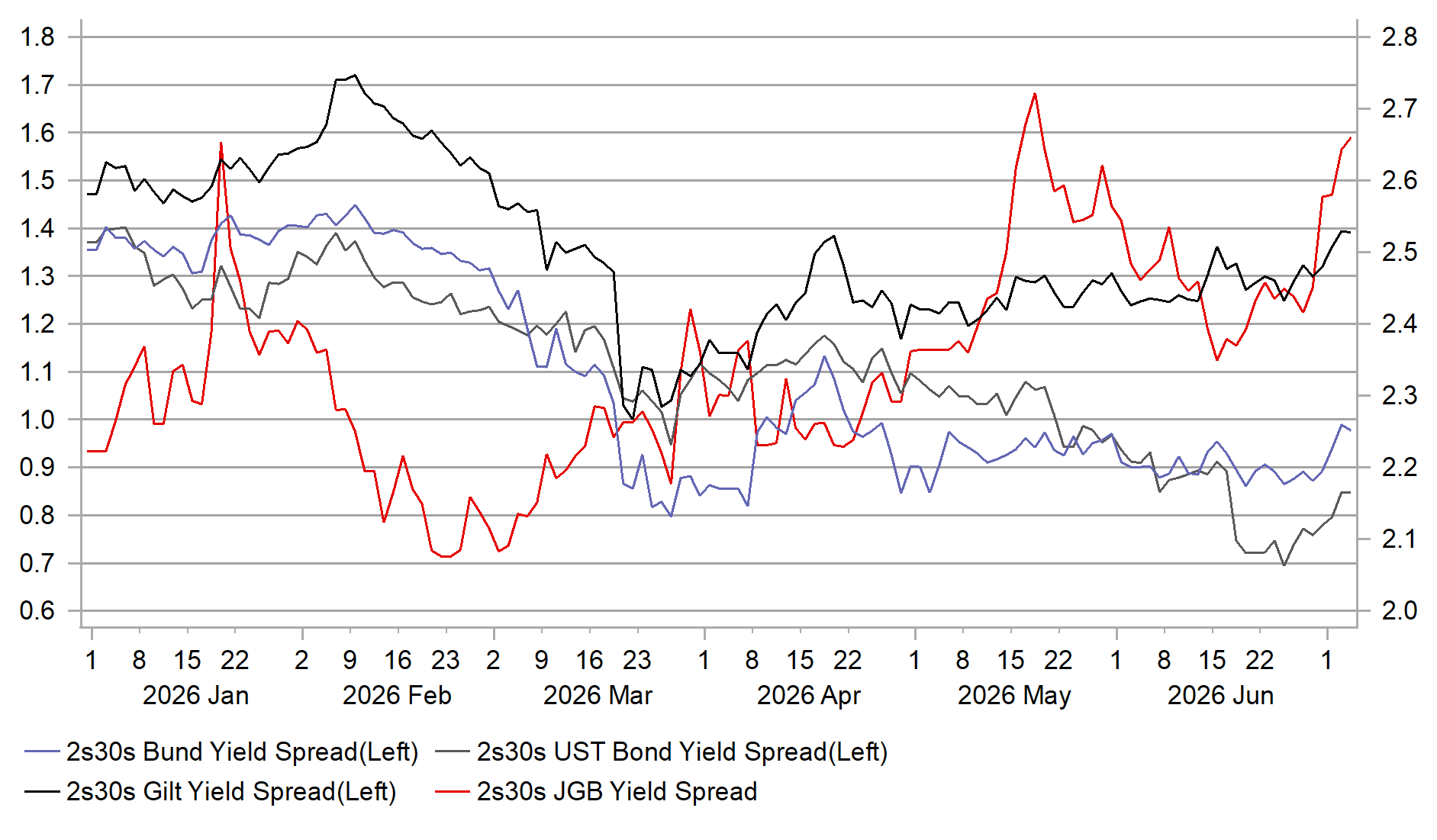

Given the scale of Japan’s debt burden, the cautious approach of the BoJ helps fuel the perception of a government strategy to lower Japan’s debt burden through inflation or that the BoJ is being constrained by fears over the burden of higher rates on servicing that debt (‘fiscal dominance’). Inflation is playing a role in boosting nominal GDP growth which is currently on a 5-year average basis at the strongest level since 1995. This is already helping lower debt-to-GDP levels. The IMF Fiscal Monitor in April shows debt-to-GDP at 228% in 2022 with the total projected to fall steadily to 193% by 2031. But long-term yields continue to rise in Japan due to the perceived BoJ caution. This year the JGB 2s30s spread 46bps to 266bps. The same spread in the US, UK and Germany narrowed. This steepening during a time of when the BoJ raised the policy rate is an indication that investors do not believe the BoJ is hiking enough to tackle inflation risks.

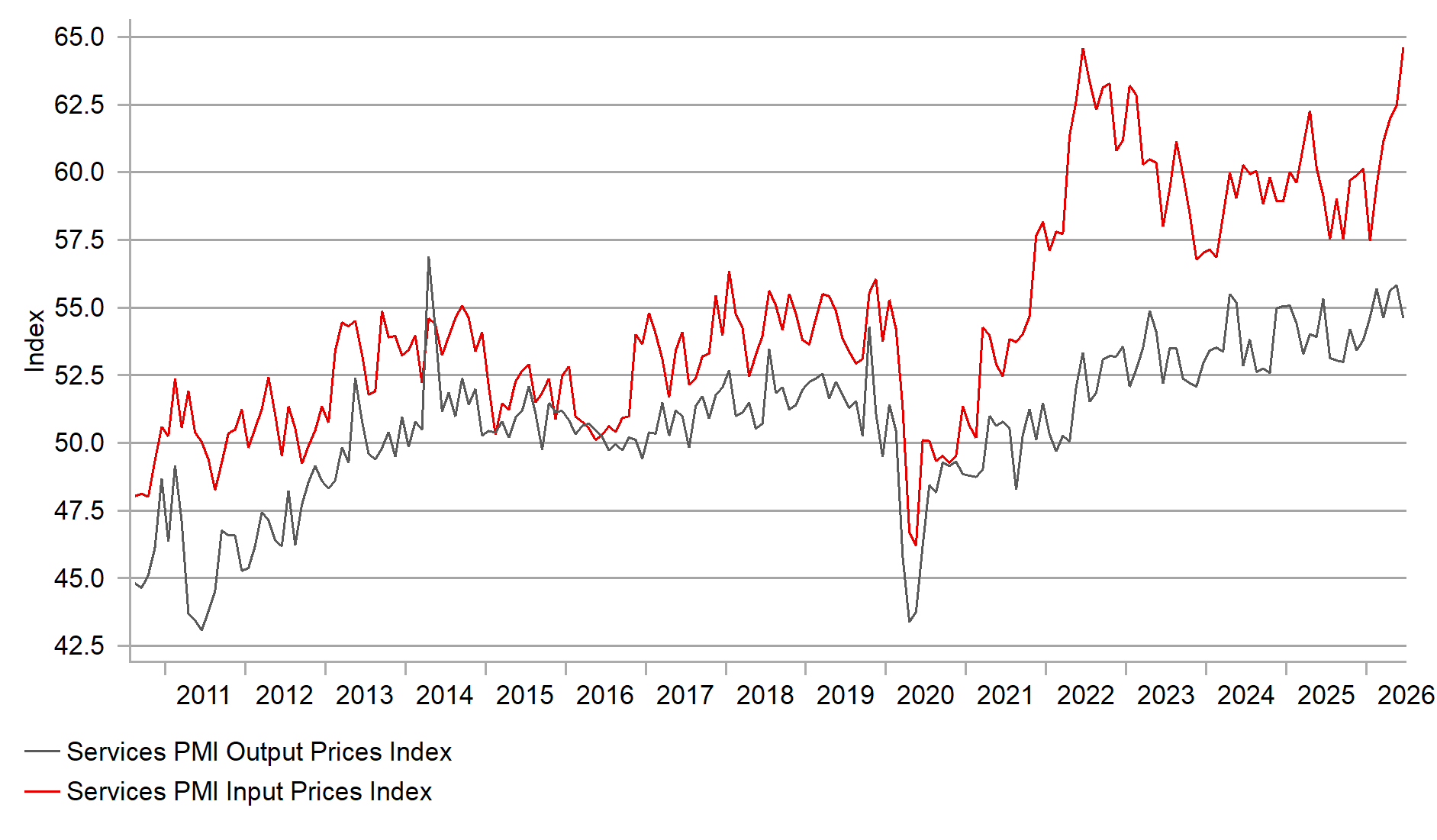

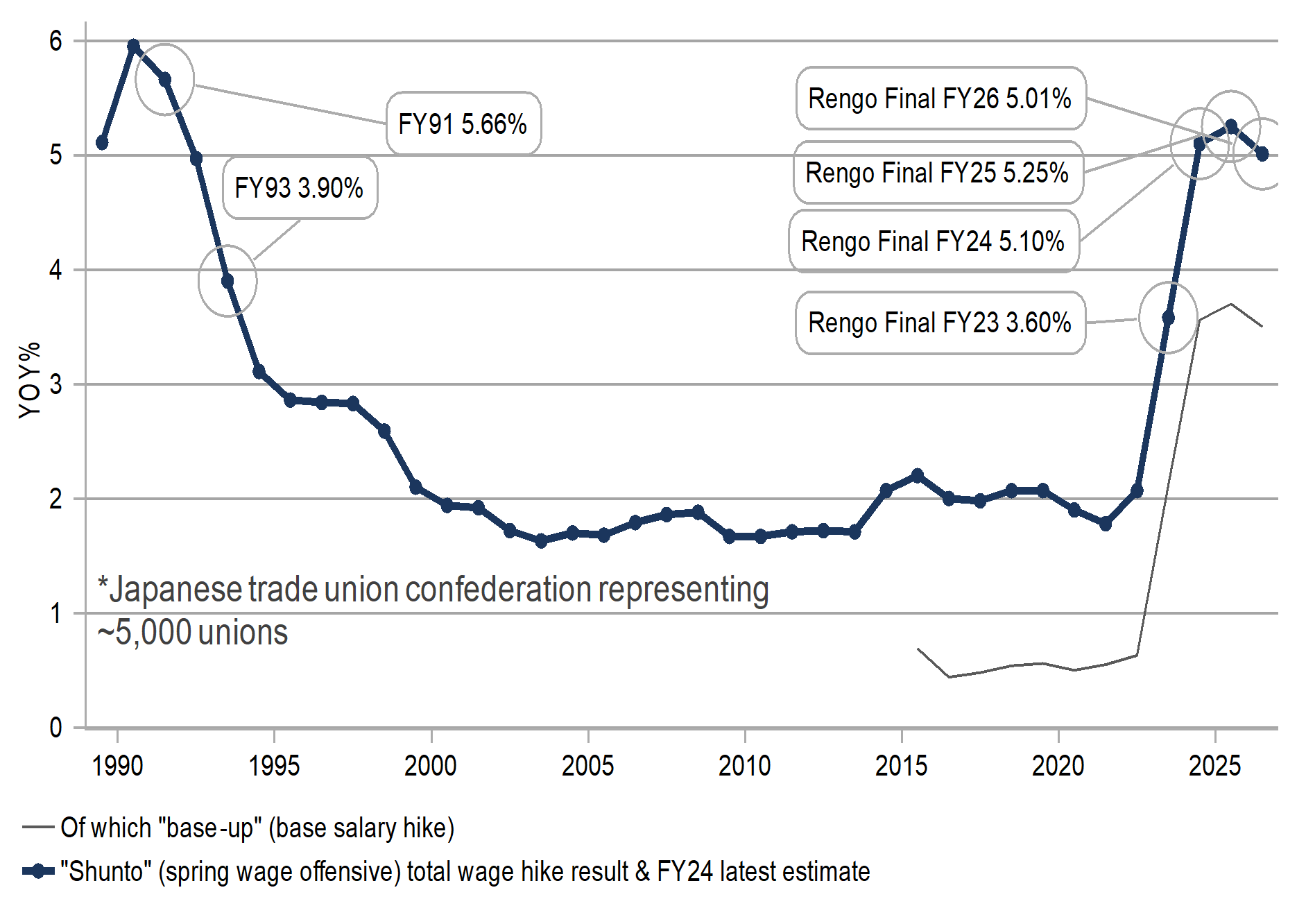

While the current level of inflation is below the 2% target, there is a strong consensus that inflation will accelerate through H2 and into 2027. Nationwide core annual CPI is currently at 1.4% but is set to re-accelerate. The BoJ projects a FY26 level of 2.8%, with a number of factors likely to see inflation pick up. Firstly, energy subsidies are a big factor suppressing inflation. When policy factors incorporated by the government are excluded, annual inflation is estimated to be around 0.7-0.8ppt higher. As those subsidies unwind, the annual CPI rates will accelerate notably. Secondly, Japan’s corporate sector price-setting behaviour looks to be pointing to passing through renewed energy-related costs going forward. The Tankan report this week revealed all enterprises’ output price index surged, breaking above the previous record highs set during the 2022 inflation shock and back in 1980. Furthermore, the services sector is looking more robust and key determinant of how wage growth can pass through to broader price pressures. The June services PMI jumped to 52.2 (from 50.0 in May) while the Input Price index surged to 64.6, matching the record high set in June 2022. With the Tankan suggesting greater appetite for passing input cost on, risks are increasing that inflation will broaden out through the services sector. Wage growth also looks set to reinforce sustained inflation. Today, the shunto wage negotiation period came to an end with the largest union umbrella group – Rengo (5,368 affiliated companies) – securing an average wage increase of 5.01%, above the 5% level for the third consecutive year for the first time since 1989-1991.

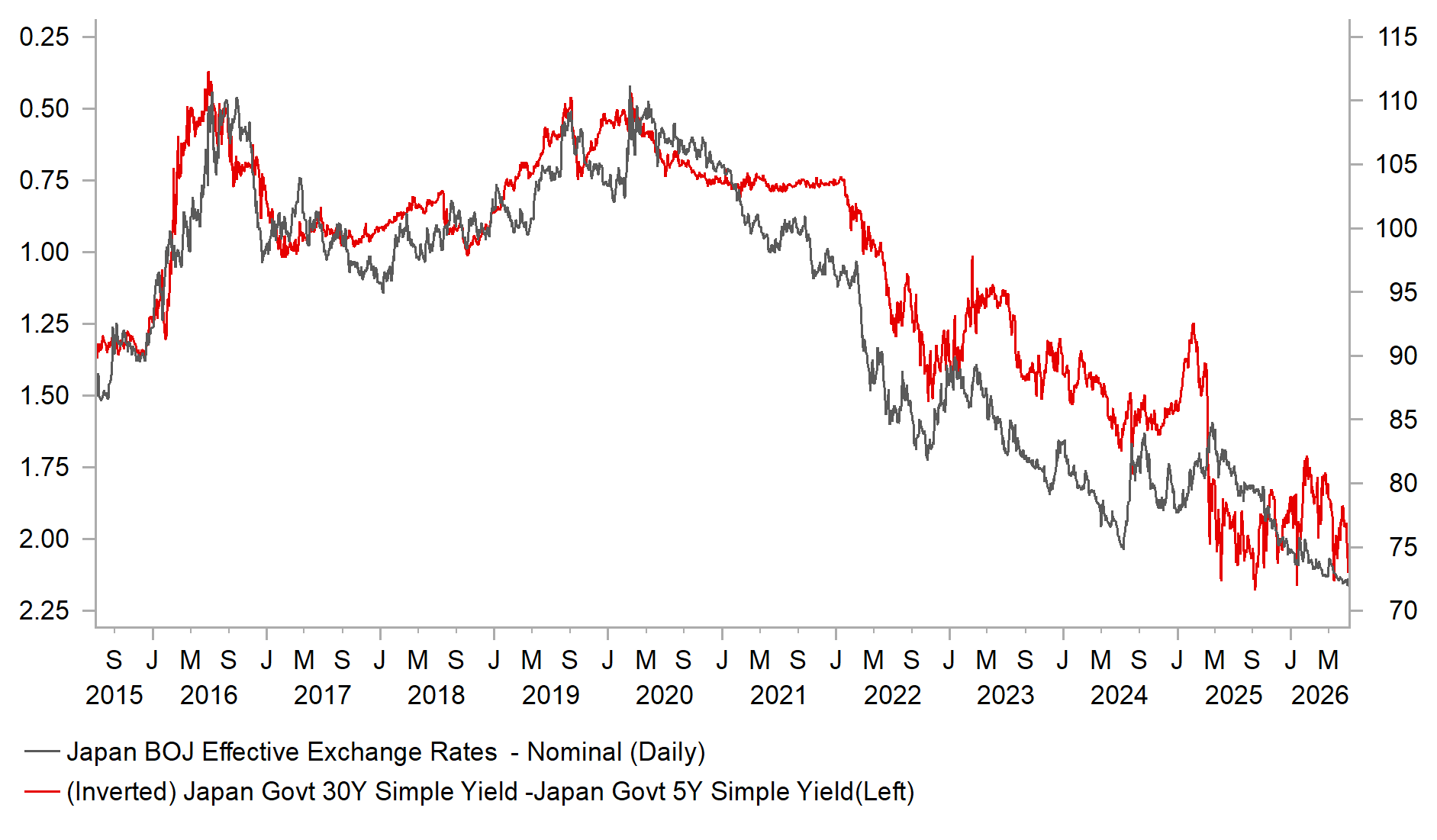

ONLY IN JAPAN HAS 2S30S STEEPENED THIS YEAR

Source: Bloomberg, Macrobond & MUFG

PMI SERVICES INPUT PRICE INDEX HITS RECORD

Source: Bloomberg, Macrobond & MUFG GMR

We believe the rates market is underpriced for what the BoJ will deliver. The BoJ has become clearer in its communication (for example when the BoJ hiked in June) that upside inflation risks are building. The statement and previous comments from Governor Ueda have highlight that cost pass-through in business-to-business transaction is proceeding “at a somewhat faster pace” underlines the focus on upside inflation risks. With YoY PPI up from 2.1% to 6.3% in just three months a quicker feed-through to CPI is an increased risk. BoJ hawks have also become more vocal with policy board member Tamaura stating in June that the BoJ needed to move to neutral “to avoid an overshoot” of inflation. Former BoJ Executive Director Yamamoto stated that the BoJ needed to move quickly and that December was too late. We believe the BoJ will increasingly take that view and expect the policy rate to reach 1.50% by January 2027 with the next hike in September. Only 5bps is priced by September and a full hike is not yet priced by year-end so front-end rates have scope to move higher.

Quicker BoJ action like we expect would go some way to limiting the downside risks for the yen. The weaker US jobs report has bought some time for the MoF and reduces the risk to some degree of the need for further intervention. Finance Minister Katayama today spoke on FX stating there was no change in policy but there was certainly less urgency in her comments than in the past that does suggest some degree of shift in strategy. USD/JPY implied vol is low and the move higher in USD/JPY has been gradual and this could be acceptable for now. The government also needs to clarify with detailed information what the fiscal implications will be of PM Takaichi’s ‘Technology Growth Strategy’ that targets JPY 370trn of investments over a 14-15yr period through most private sources. But what will be the public contribution? Ensuring that is kept to a minimum (estimated JPY 1trn p yr) will be important for JGB sentiment which in turn for the yen. Any upturn in inflation expectations and JGB yields could see renewed yen selling and if the US dollar was to rebound a move in USD/JPY to 165.00 is feasible. But our assumption based on our BoJ & Fed views is for any upside in USD/JPY to be brief before a turn back lower into the 150.00’s.

RENGO WAGE AGREEMENT OVER 5% AGAIN

Source: Bloomberg, Macrobond & MUFG GMR

A HALT TO JGB CURVE STEEPENING WOULD HELP JPY

Source: Bloomberg, Macrobond & MUFG GMR

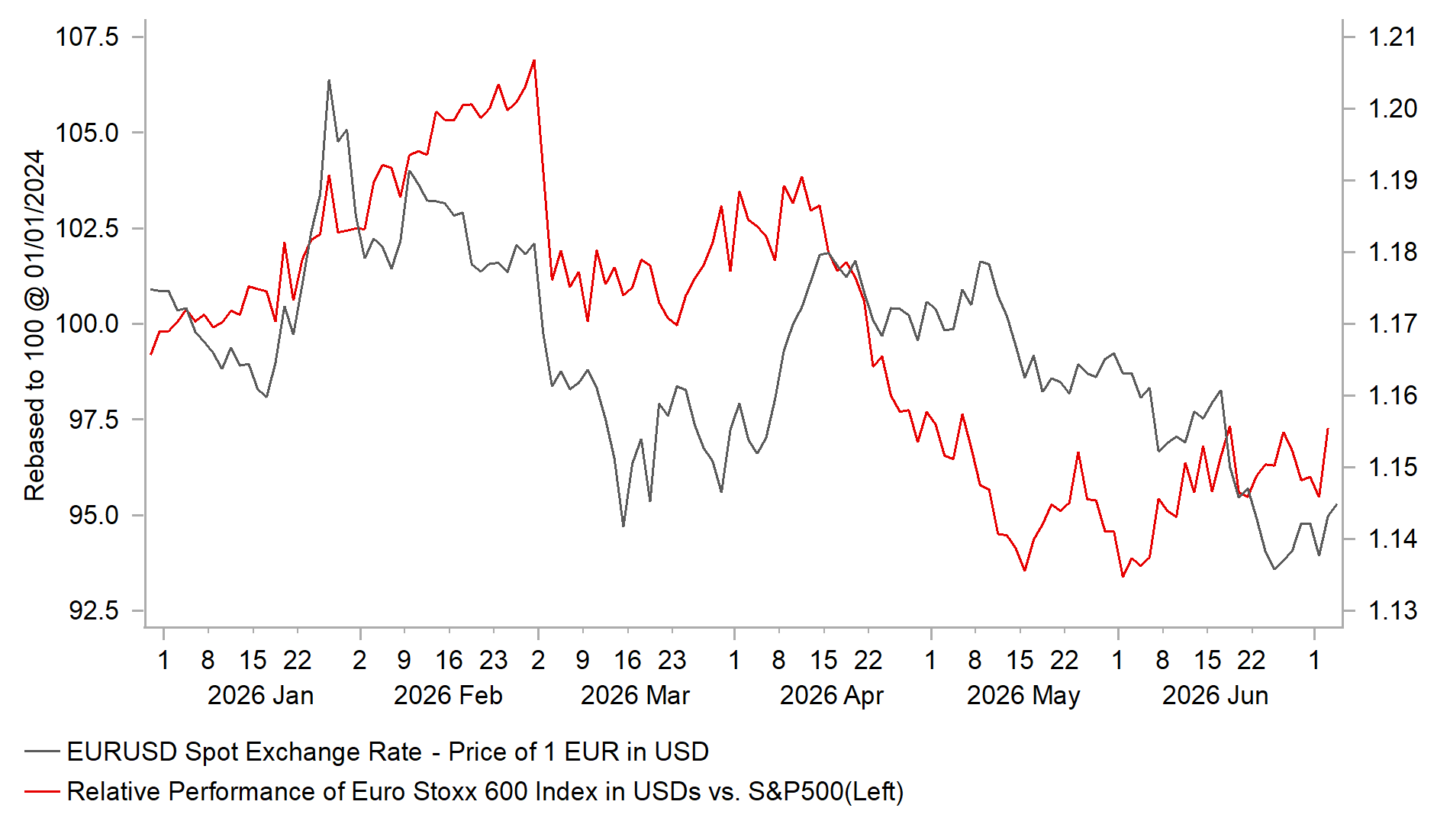

EUR: Is the stage set for the EUR to extend its correction lower?

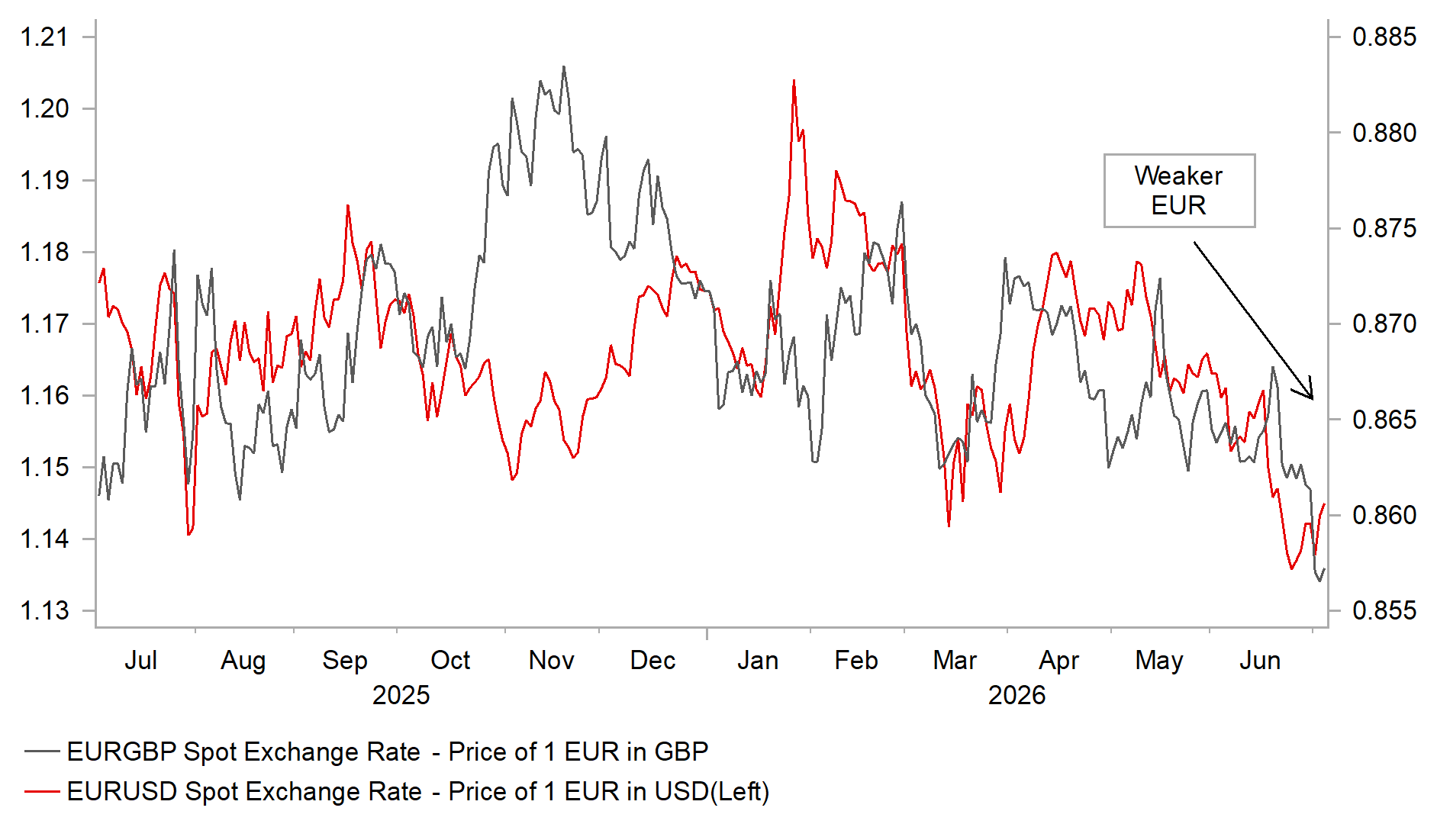

The EUR has recently underperformed against the other major currencies of the GBP, JPY, and USD. EUR/USD reached a peak of 1.1849 on 17th April before retreating to a low of 1.1325 on 24th June. The pair is now attempting to break decisively below the lower boundary of the 1.1400–1.1800 trading range that has largely contained price action over the past year. A similar pattern is evident in EUR/GBP. The pair reached a high of 0.8768 on 27th February, the day the US-Iran conflict began, but has since fallen to a low of 0.8546. This marks the first time EUR/GBP has broken below the lower end of the 0.8600–0.8800 range that has prevailed for most of the past year.

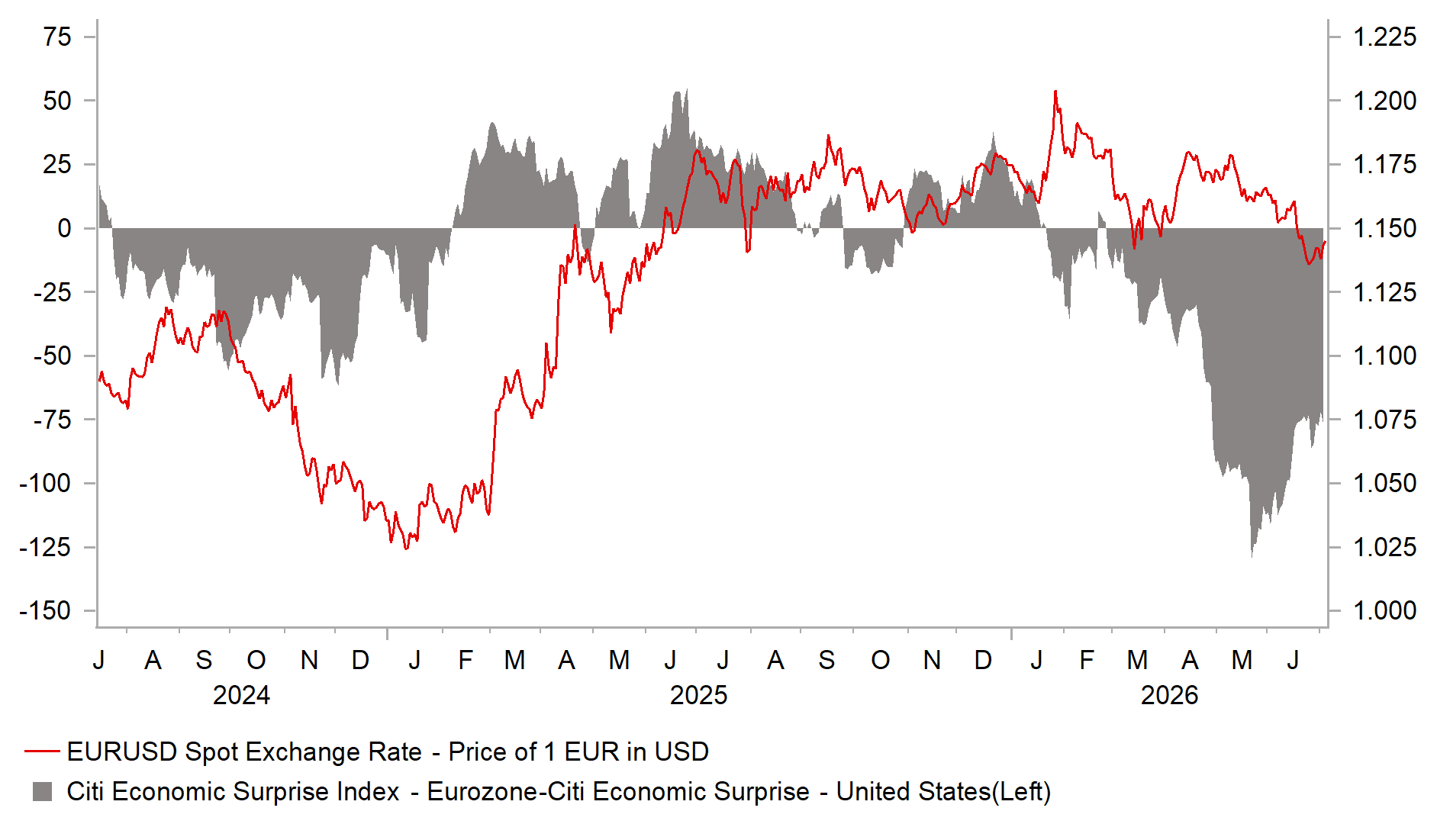

The EUR’s underperformance primarily reflects the initial negative impact of the energy price shock on investor sentiment towards Europe and, more recently, the scaling back of ECB rate hike expectations. In the first two to three months following the outbreak of the US-Iran conflict, euro-area economic data both the survey-based indicators and hard data have consistently surprised to the downside. However, the magnitude of those negative surprises has begun to ease in recent weeks, suggesting that the worst of the slowdown may now be behind us. Today’s stronger-than-expected industrial production data from France and Spain for May, together with notable upward revisions to the April figures, have reinforced that view. As a result, our European economist has revised higher his forecast for euro-area GDP growth in Q2 to 0.25%, up from a previous expectation of near-stagnation.

If confirmed, it would underscore that the euro-area economy is proving more resilient than previously feared. While the euro area economy contracted by 0.2% in Q1, this was largely driven by an outsized 12.1% decline in Ireland’s GDP. Excluding Ireland, the rest of the euro-area economy expanded by approximately 0.25% during the quarter. Moreover, euro-area growth for Q1 is likely to be revised higher after data released earlier this week showed that Ireland’s economy contracted by a smaller-than-previously-reported 7.0%. The resilience of the euro-area economy is a supportive development for the EUR and should help to limit further selling pressure. In addition, a faster-than-expected reversal of the energy price shock should improve investor sentiment towards both the euro-area economy and the EUR over the remainder of this year.

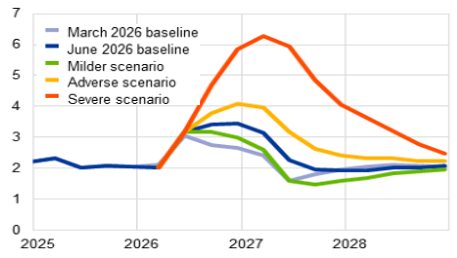

Another headwind for the EUR in recent months has been the scaling back of ECB rate hike expectations. In the immediate aftermath of the energy price shock, euro-area rate markets moved to price in the risk of a more “forceful” tightening cycle from the ECB, particularly as oil prices briefly surged above USD 120 per barrel in late April. At one point, markets were pricing in three to four ECB rate hikes. However, confidence in such an outcome has since diminished significantly, with oil prices having already retraced to pre-conflict levels. Following the ECB’s initial 25bp rate increase last month, markets are now pricing in only around 20bp of additional tightening by year-end. This dovish repricing has been reinforced by this week’s euro-area inflation data, which came in notably softer than expected. Headline inflation slowed to 2.8% in June, while core inflation eased to 2.4%. These latest readings suggest that inflationary pressures are weaker than the ECB anticipated. In its June projections, ECB staff forecast headline inflation at 3.2% for Q2 and core inflation at 2.4%. The combination of softer inflation and lower energy prices is more consistent with the ECB’s “milder” scenario. Under that scenario, headline inflation peaks at just above 3% before falling back below the ECB’s target in 2027, while core inflation gradually converges towards target over the coming years. As a result, markets have become less convinced that the ECB will need to deliver further tightening which is weighing on euro-zone rates and the EUR.

EUR IS TESTING BOTTOM OF RANGES OVER PAST YEAR

Source: Bloomberg, Macrobond & MUFG

EUR IS PAST WORST POINT OF ECONOMIC SURPRISES

Source: Bloomberg, Macrobond & MUFG

In light of these favourable developments, it is no longer clear that the ECB will need to hike rates again this year. Speaking at this week’s annual ECB Forum on Central Banking in Sintra, President Lagarde acknowledged that the risks to inflation and growth in the euro area are “probably more broadly balanced”. This marks a notable shift from the ECB’s assessment at its June meeting, when risks were judged to be tilted to the upside for inflation and to the downside for growth. For now, the ECB continues to pursue a strategy of “measured” policy tightening while leaving the door open to one final hike. The focus has increasingly shifted towards assessing whether second-round inflation effects begin to materialise. Chief Economist Philip Lane recently stated that policymakers need to evaluate “how the four months of energy-cost increases percolate into food inflation, and into services inflation”. He also suggested that there may still be room for one additional hike, noting that the upper end of the ECB’s estimated neutral policy rate range has risen by 25bp to 2.50%. At present, we are maintaining our forecast for one final 25bp hike in September, although we acknowledge that there is a rising probability the June hike could be a one-off.

In summary, the deterioration in investor sentiment towards the euro-area economy and the dovish repricing of ECB rate expectations help to explain why the EUR is currently threatening to break lower. EUR selling pressure has also been reinforced by investor optimism that the US economy is proving more resilient to the energy price shock than initially feared. However, softer US consumer spending in Q1 alongside slower employment growth in May and June, has tempered that optimism. Looking ahead, we expect investor pessimism towards the euro-area economy to gradually fade providing greater support for the EUR and helping it to establish a bottom. Our forecasts (click here) for EUR/USD and EUR/GBP to move back towards the upper end of their current trading ranges are also based on the important assumptions that both the Federal Reserve and the Bank of England keep policy rates on hold for the remainder of this year, before the door reopens to resume rate cuts in 2027.

INFLATION IS TRACKING “MILDER” SCENARIO

Source: ECB Staff Projections from June 2026

EZ EQUITIES HAVE STOPPED UNDERPERFORMING

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

Ccy | Date | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EUR | 06/07/2026 | 07:00 | Germany Factory Orders MoM | May | -- | -3.8% | !! |

EUR | 06/07/2026 | 09:30 | Sentix Investor Confidence | Jul | -- | - 13.4 | !! |

EUR | 06/07/2026 | 10:00 | Retail Sales MoM | May | 0.3% | -0.4% | !! |

USD | 06/07/2026 | 15:00 | ISM Services Index | Jun | 54.2 | 54.5 | !!! |

CAD | 06/07/2026 | 15:30 | BoC Overall Business Outlook Survey | 2Q | -- | - 0.4 | !! |

EUR | 06/07/2026 | 16:00 | Fed's Waller & ECB's Schnabel Speak | !!! | |||

GBP | 06/07/2026 | 17:45 | MPC member Mann Speaks | !! | |||

EUR | 06/07/2026 | 19:30 | ECB's Lane Speaks in Rome | !!! | |||

JPY | 07/07/2026 | 00:30 | Labor Cash Earnings YoY | May | -- | 3.6% | !!! |

EUR | 07/07/2026 | 07:00 | Germany Industrial Production SA MoM | May | -- | 0.4% | !! |

USD | 07/07/2026 | 13:30 | Trade Balance | May | -$78.8b | -$55.9b | !! |

CAD | 07/07/2026 | 13:30 | Int'l Merchandise Trade | May | -- | 2.72b | !! |

NZD | 08/07/2026 | 03:00 | RBNZ Official Cash Rate | 2.50% | 2.25% | !!! | |

SEK | 08/07/2026 | 07:00 | CPI YoY | Jun P | -- | 0.8% | !!! |

SEK | 08/07/2026 | 07:00 | GDP Indicator SA MoM | May | -- | 0.5% | !! |

EUR | 08/07/2026 | 12:30 | ECB's Nagel Speaks | !! | |||

USD | 08/07/2026 | 19:00 | FOMC Meeting Minutes | !!! | |||

GBP | 09/07/2026 | 00:01 | RICS House Price Balance | Jun | -- | -35% | !! |

CNY | 09/07/2026 | 02:30 | CPI YoY | Jun | -- | 1.2% | !!! |

EUR | 09/07/2026 | 07:00 | Germany Trade Balance SA | May | -- | 14.5b | !! |

EUR | 09/07/2026 | 12:30 | ECB Publishes Account of June Meeting | !! | |||

USD | 09/07/2026 | 13:30 | Initial Jobless Claims | -- | -- | !! | |

GBP | 09/07/2026 | 20:30 | MPC member Breeden Speaks | !! | |||

NOK | 10/07/2026 | 07:00 | CPI YoY | Jun | -- | 3.1% | !! |

EUR | 10/07/2026 | 07:00 | Germany CPI YoY | Jun F | -- | 2.3% | !! |

EUR | 10/07/2026 | 07:45 | France CPI YoY | Jun F | -- | 1.8% | !! |

CAD | 10/07/2026 | 13:30 | Net Change in Employment | Jun | -- | 87.8k | !!! |

Source: Bloomberg & MUFG GMR

Key Events:

The RBNZ's upcoming policy decision is widely viewed as a close call. According to Bloomberg, five New Zealand economists expect the RBNZ to begin tightening by raising the OCR by 25bps next week, while four economists expect rates to remain on hold. New Zealand rate market is currently pricing in around 18bps of tightening for next week's meeting and just over 60bps of cumulative hikes by year-end. This suggests that investors expect the RBNZ to signal a gradual tightening cycle rather than a one-off rate increase. Such an outcome would help move the OCR back towards neutral territory, which the RBNZ currently estimates to be between 2.50% and 3.50%. The RBNZ came close to raising rates at its May meeting. The decision to leave the OCR unchanged was split 3-3, with Governor Breman casting the deciding vote in favour of holding rates steady. The Bank also signaled that the OCR would likely need to increase sooner, and by more, than had been envisaged in its February projections. Inflation risks have eased somewhat since May, largely reflecting lower energy prices. However, a modest degree of further tightening still appears justified this year.

The release of the minutes from the hawkish June FOMC meeting will attract significant market attention in the week ahead. Investors will scrutinize the minutes for further insight into whether the Fed is seriously considering raising rates this year, potentially as soon as its next meeting later this month. The updated dot plot and comments from new Fed Chair Kevin Warsh have provided a hawkish policy signal. However, doubts remain as to whether the strong rhetoric surrounding the price stability component of the Fed's dual mandate will ultimately be backed by policy action. At the same time, Warsh has noted that inflation risks have eased over the past month, suggesting that the minutes from the 17 June FOMC meeting may already be somewhat backward-looking. As a result, investors will be looking for clues on how policymakers assess the recent improvement in the inflation outlook and whether it has altered the case for further tightening.

The main economic data releases in the week ahead include: (i) the latest ISM Services survey for June, (ii) Japan's labour cash earnings report for May, and (iii) Canada's employment report for June. The ISM Services survey has continued to signal that the US economy remains resilient in the face of higher energy prices, although consumer spending slowed by more than expected in the first quarter. In contrast, Canada's labour market has remained relatively soft this year, despite showing signs of improvement in May. This has strengthened market confidence that the Bank of Canada will refrain from raising rates this year in response to higher inflation.